Predicting the stock market will forever be an unsolved mystery. Investors can make decisions based on the facts at hand, yet none of them can have full certainty in the actual future market direction. And, if they do, we hope that they have a parachute on hand for when the inevitable plane crash occurs, because certainty does not always presage strong returns – in fact, it likely detracts. It is not adverse market conditions that derail compounding; it’s investors’ reactions to them.

Predicting the stock market will forever be an unsolved mystery. Investors can make decisions based on the facts at hand, yet none of them can have full certainty in the actual future market direction. And, if they do, we hope that they have a parachute on hand for when the inevitable plane crash occurs, because certainty does not always presage strong returns – in fact, it likely detracts. It is not adverse market conditions that derail compounding; it’s investors’ reactions to them.

One of the most infamous, and the only documented unsolved, air piracy cases in the history of aviation was that of D.B. Cooper. A thin, olive-skinned man who pulled off the first and only successful major skyjacking in the United States – one that was mimicked by others for years to come. After buying a plane ticket, day of, to fly from Portland to Seattle, D.B. Cooper handed a flight attendant a note stating that he had a bomb in his briefcase – demanding that he is given $200,000 and four parachutes. After successfully obtaining the ransom, the plane was directed to fly to Mexico. But, before getting to the destination, D.B. Cooper parachuted out the rear stairway, vanishing into a vast wilderness over Southwest Washington. To this day, his whereabouts remain unknown.

Some sleuths believe that the infamous D.B. Cooper immediately died on impact after his parachute failed to deploy. This is very synonymous with the main question being asked by the gumshoes of the market: Will the market rally get derailed early, parachuting into uncertainty, before the proverbial airplane can have a soft landing on a runway that feels like it continues to get shorter?

Before investors “jump” to conclusions on the answer to this question, which will continue to remain unsolved for now, there needs to be a reset in the overall perspective of the market. Keeping perspective is always more advantageous than pontificating outcomes through a crystal ball.

-

- Pullbacks are Normal and Healthy: Markets that go straight up without any volatility, much like 2023 and 2024, are the outlier, as those market conditions tend to be abnormal. Markets don’t move in a straight line;

-

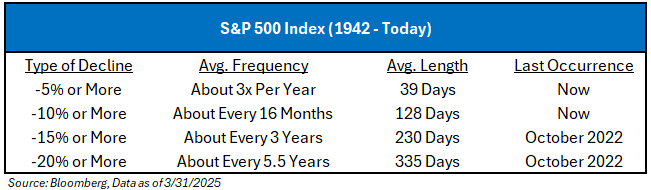

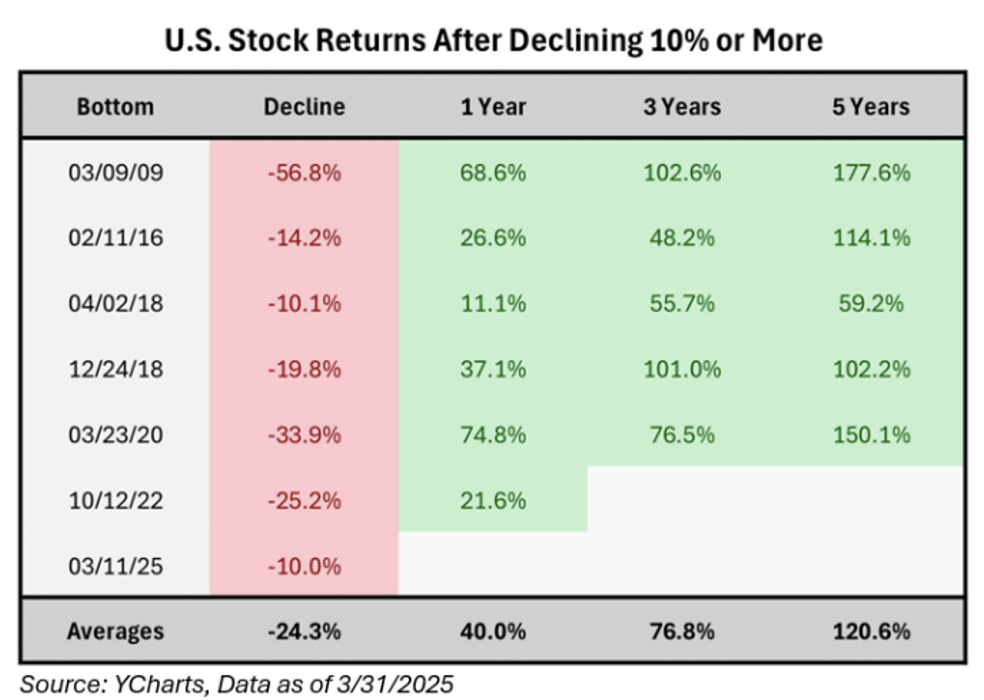

- All Bear Markets Start with a Correction, But Not all Corrections Turn into Bear Markets: Since World War II, there have been 39 instances where the S&P 500 declined by 10% or more. Only 13 of those events turned into bear markets, where losses exceeded 20% – i.e., only 33% of the time;

-

- Sentiment Surrounding the Market is Worse Than During Covid and the Great Financial Crisis: Yet, the market ended Q1 2025 at levels not seen since…September 2024…a mere 6 months ago. The market has officially pulled back by 10.0% in 2025, but during the two aforementioned periods, the peak-to-trough pullback was -33.79% and -54.91%, respectively; and

-

- Never Bet Against the Resiliency of Corporate America: Macro news can seem overwhelming, but just remember, it’s all about stocks, which are all about the underlying businesses. The S&P 500 grew earnings by 16% last quarter and continues to expect to grow closer to 11% during Q1 2025.

Perspective is key because consumer behavior is simple: investors hate losses and have little patience for Washington D.C. policies that might not immediately contribute positively to stock market returns.

Like D.B. Cooper, the future of the market will always remain an unsolved mystery. At the end of the day, investors need to focus on what they control and prepare for what they cannot. It is never beneficial to focus on short-term outcomes when investing for the long run. This is why Aptus is firm believers that investing with guardrails is the best way to win the long game, given the bad math of drawdowns. Understanding that drawdowns occur often and immediately recognizing the need to control and manage personal emotions during market drawdowns is the best elixir to efficiently compounding capital over longer periods of time. Remember, it’s one’s time in the market; not timing the market.

If you don’t control your emotions during turbulent periods, you may find yourself needing to hijack a plane for ransom money to conquer longevity risk. Remember, this has only been successfully implemented one time in U.S. history – and that’s if you believe that D.B. Cooper actually parachuted out of the back of an airplane unscathed.

Q1 2025 Market Recap

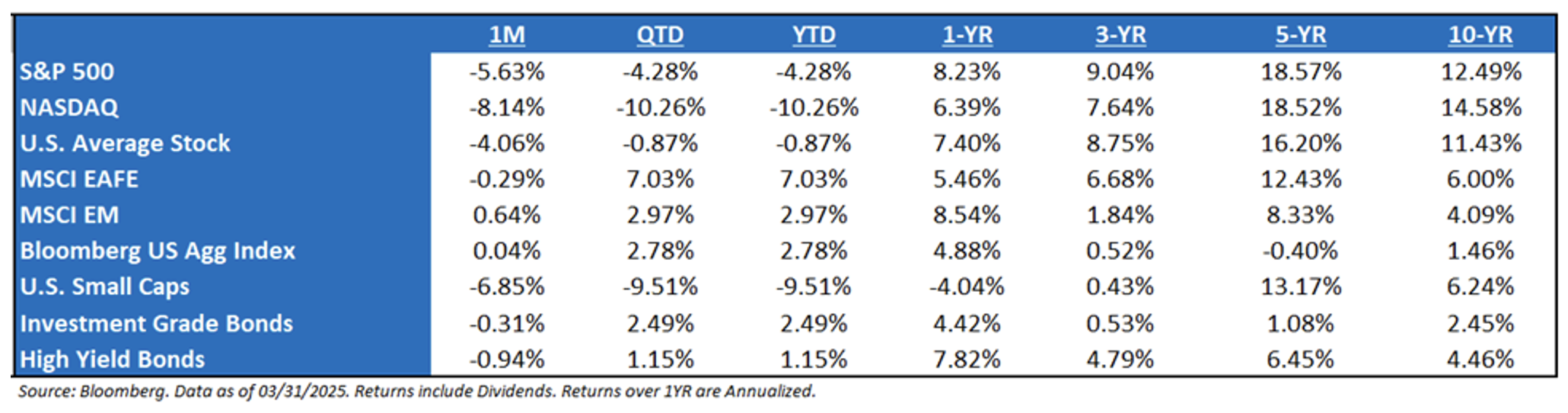

It may be hard to believe that the market was trading at all-time highs just a mere 6 weeks ago, but then policy hyperactivity started to overshadow the animal spirits. The first quarter of 2025 delivered a classic third-year bull market correction, falling 10% from its highs before rebounding and finishing only -4.28% in the quarter. The recent selloff has been centered around three prevailing culprits: momentum unwind, tariff uncertainty, and a growth slowdown. A key highlight of the quarter was the market broadening that drove the previously unloved International markets higher (+7.03%), as investors rotated from the Magnificent 7 (“Mag 7”) which became a funding mechanism into the cheaper areas of the market. Well, except U.S. Small Caps (-9.51%).

When investors take a step back, it’s stunning how much is going on right now – and, even if implied volatility has settled down, the market continues to digest a huge range of significant variables. The result will likely be a trading environment profoundly different from the past few years. But remember that investors need to invest in the world that we have; not the one that we want.

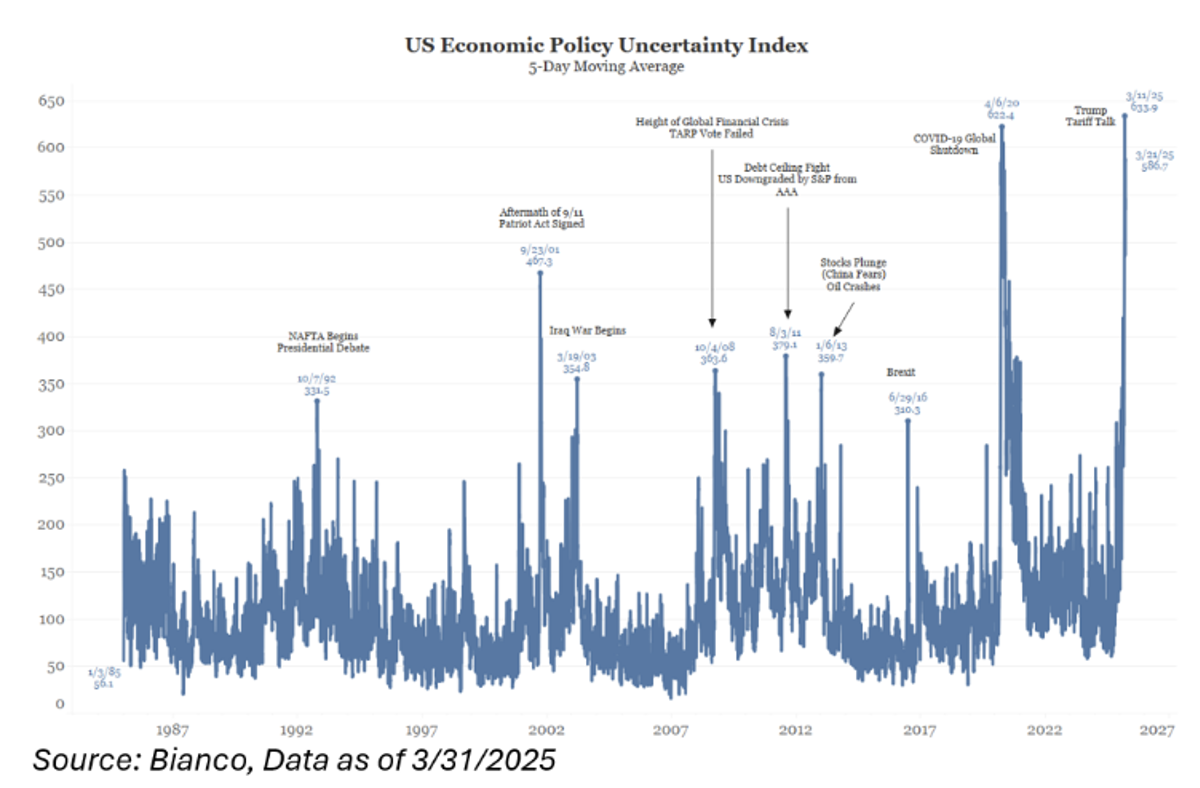

The single biggest obstacle in the market that remains is uncertainty. The market loves clarity and certainty, and when this characteristic is lacking, it tends to breed volatility. This cocktail of uncertainty has hit consumer and business confidence, that could ultimately slow the current economic momentum. Combine that with elevated earnings and a lot of bullish optimism entering the quarter, and you’ve got the recipe for a correction, which we saw in the S&P 500 during Q1.

Understanding the Drawdown

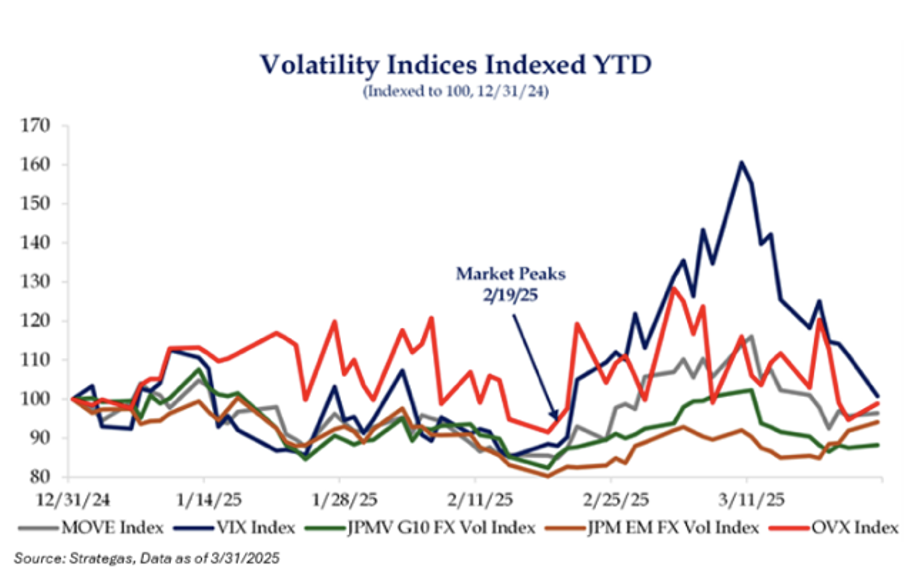

The root cause of the recent volatility can’t be boiled down to just one thing – it’s likely three. In order of contribution for the 10.0% pullback is: 1) momentum unwind, 2) expectation for slower growth, and 3) policy uncertainty. It may come as a surprise, but capital flows can significantly impact market pricing. In 2025, we’ve seen meaningful outflows from U.S. Mega-Caps into International equities.

1. The Momentum Unwind: The absence of follow-throughs across most major volatility indicators, including oil, interest rates, and both developed and emerging market currencies, suggests that the key driver is likely the momentum unwind. If tariffs were the primary catalyst, we’d expect heightened volatility in currency markets. If growth concerns were at the core, oil and interest rate volatility would be spiking. Instead, the broad lack of volatility confirms what this chart is signaling: a momentum unwind is the dominant force behind the recent market moves.

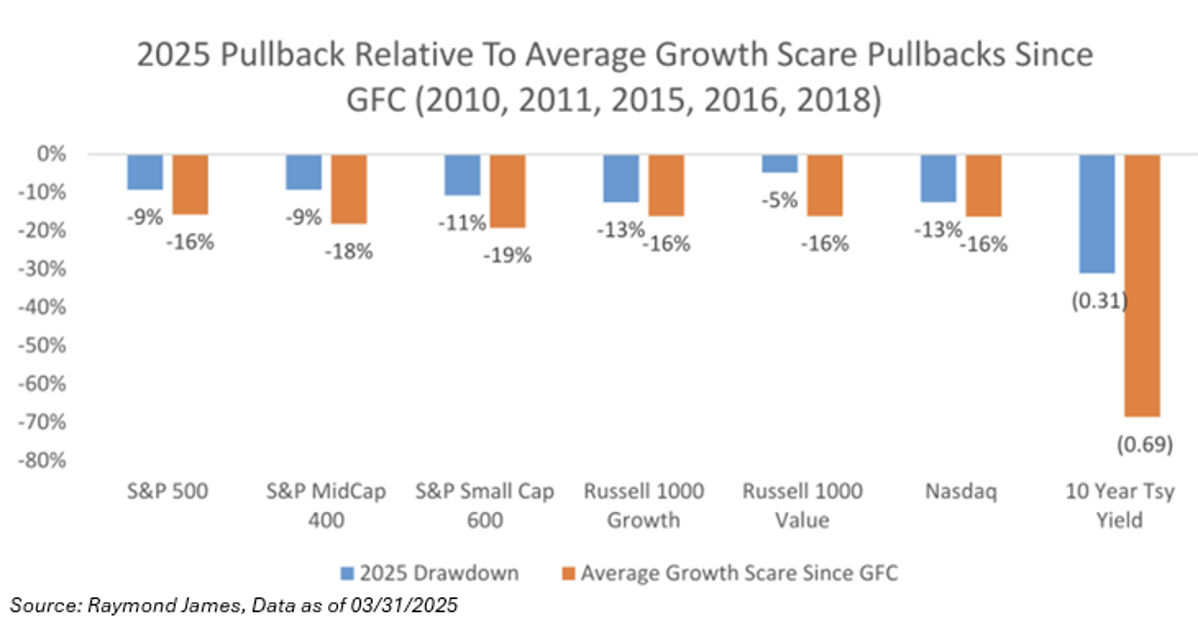

2. The Growth Slowdown: When comparing historical growth pullbacks, excluding COVID (plus, 2022 was rates-driven, not growth-driven), the drawdown that we are witnessing isn’t uncommon. These previous growth scares have resulted in a drawdown closer to -16.0%. While we aren’t necessarily down as much as average, we would say that the consumers and corporations remain much stronger today compared to these previous periods.

Another way of saying this is that the bond and credit markets don’t seem to be as concerned about as the equity market.

3. Policy Uncertainty: Investors still face two unknowns: 1) the extent and 2) the size of looming tariffs on major trading partners, including Canada, Mexico, the EU, and others. The unpredictable and spontaneous nature of the tariff threats has led investors to worry that even currently well-regarded trade partners aren’t safe from potential threats. Investors need a clear and consistent policy to have more conviction.

Underneath the Hood

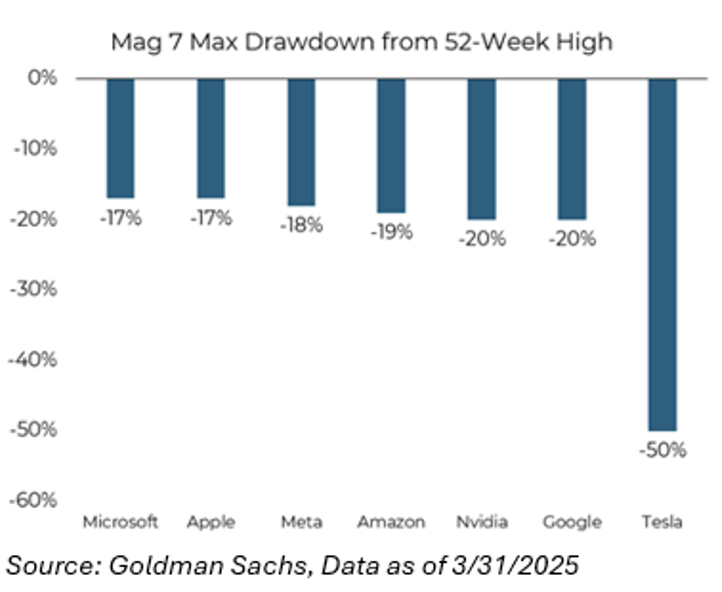

In 2024, the Mag 7 drove more than half of the S&P 500’s 25% total return. And, for the most part of the past two years, it has been the driving force behind all of the S&P 500’s earnings growth. But lately, the Mag 7 turned into the Lag 7, as investors began to reconsider stretched valuations and excessive positioning. In fact, almost every single Mag 7 stock either hit correction territory (>20%) or was within spitting distance of it. Historically, the cap-weighted index tends to experience 10% drawdowns in most years, similar to what we’ve seen recently. In contrast, the equal-weighted index, a proxy for the typical stock, has fallen only -7.3% during the recent bout of volatility and remains 8% below its all-time highs.

excessive positioning. In fact, almost every single Mag 7 stock either hit correction territory (>20%) or was within spitting distance of it. Historically, the cap-weighted index tends to experience 10% drawdowns in most years, similar to what we’ve seen recently. In contrast, the equal-weighted index, a proxy for the typical stock, has fallen only -7.3% during the recent bout of volatility and remains 8% below its all-time highs.

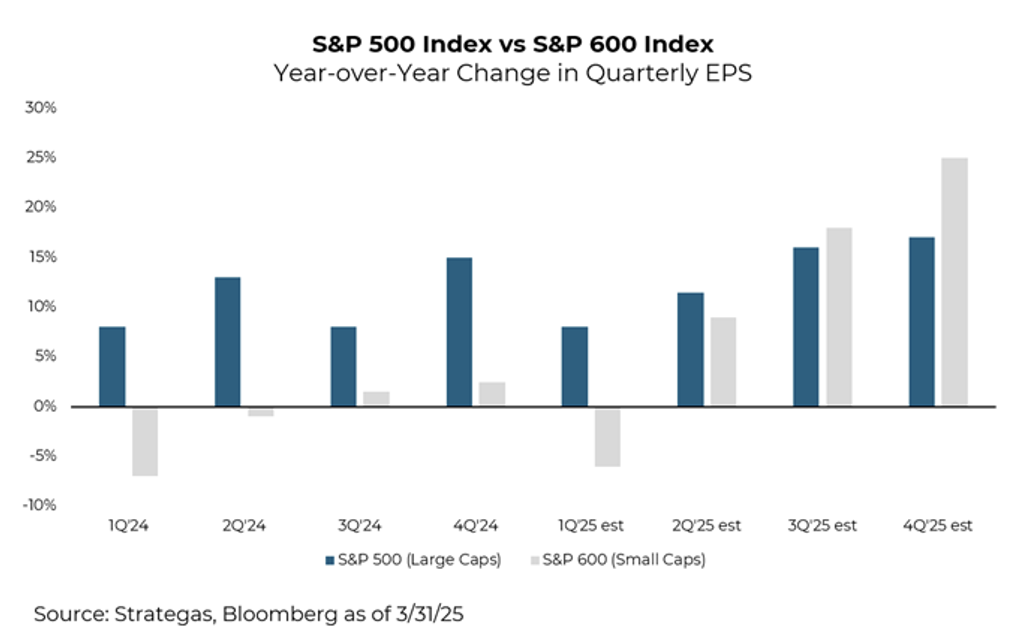

However, the increasing market breadth has completely eluded U.S. Small Caps, which are down -17.3% from peak-to-trough since its November 2024 highs. They’re off -9.5% year-to-date. Bluntly said, the “R” word, i.e., recession, is a very bad word for Small Caps. Whether it’s regional bank stress, meme stock volatility, or rising rates, something always seems to be holding back small caps over the past few years. With recession concerns resurfacing, small have taken a hit more than you’d typically see in the early stages of a slowdown.

Fundamentally, it’s also been a tough stretch. As of Q1 2025, small cap earnings growth is projected to outpace large caps in the second half of the  year. But unless growth reaccelerates meaningfully, that potential leadership shift may never materialize.

year. But unless growth reaccelerates meaningfully, that potential leadership shift may never materialize.

One reason investors are eyeing small caps is valuation. They remain historically cheap, trading roughly one standard deviation below large caps for three straight years, making them look attractive if the macro picture improves.

But, if there’s a discussion about increasing market breadth, then investors can’t leave International stocks out of the conversation.

Fire Side Chat: The Great International Debate

In a knee-jerk reaction, it seems that Donald Trump has started to make international equities great again. The theme of US exceptionalism has been as powerful as any – whether an investor starts the clock in 2009 or 2020, the US has been the best game in town. Flash forward to today, some investors are wondering if this narrative has changed, as U.S. underperformed the rest of the world by the largest amount in 23 years during the first quarter.

Nonetheless, the first leg of this rally seems to be more of a capital flows story, as international was substantially under-owned heading into the year. The way this looks in our US equity market is “rotation” or “broadening”, as the global asset managers that we believe have been funding much of the “US exceptionalism” of Mega-caps and winners of the last 2 years are likely rejiggering global weightings at the beginning of this year. This doesn’t hurt the entire US equity market, but the parts of the equity market that those global assets have moved into the last several years (i.e., mega cap tech). For those that don’t know, capital flows can really move the markets, especially if the money flows from something that has been “over-owned” to something that has been substantially “under-owned”.

To be specific, U.S. equities have underperformed International due to the following reasons:

-

- Europe is still lowering rates, even with inflation above 2%, while the US is clearly done until the economy weakens. European economies are very sensitive to the short end of the curve, so economic improvement should be evident very soon;

-

- Germany is likely to start allowing EU countries to expand fiscal stimulus in order to increase defense budgets, and start the process of taking the US training wheels off of the European experiment of the last 80 years;

-

- At the same time, the U.S. will be cutting the deficit (we’ll see, just a narrative right now), which will create an economic headwind in the US at the same time Europe is expanding. And after 6-7 years of compounded overweighting of US equities, global managers appear to be talking themselves into rotating back into the rest of the world;

-

- On top of this, year-over-year (“YoY”) growth is broadening out. For the last 2 years, most equity indexes around the world including the US had modestly down YoY earnings, at the exact same time the Magnificent 7 was putting up 40%+ EPS growth.

-

- In essence, the valuation spread between “winners” the last 2 years, and “losers” the last 2 years had gotten very extreme, with the same sectors, styles, factors outperforming and underperforming almost every month for 2 years. This phenomenon is highly unusual. At some point you get some reversion to the mean and it feels that we reached that point at the start of the year.

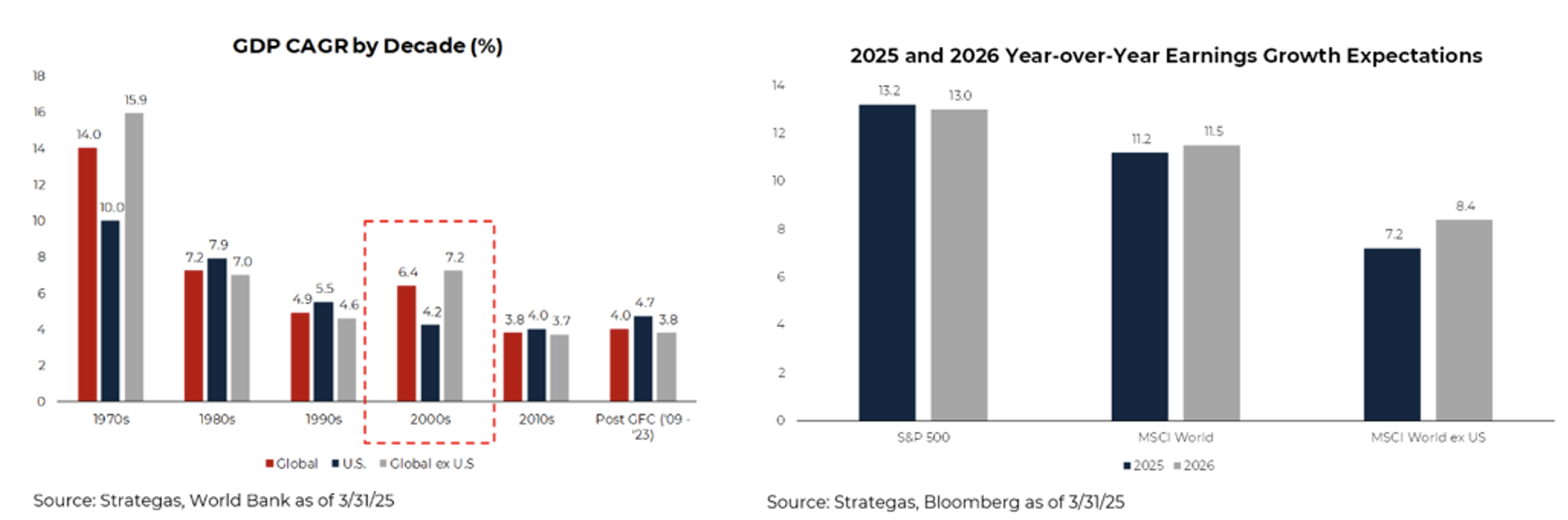

As fiscal spending shifts from the U.S. to abroad, investors are becoming increasingly excited about the potential for a pick-up in growth. However, in the near term, global market outperformance is likely driven by a re-rating of multiples, fueled by a historically steep discount. Looking back to the last time the international discount relative to the U.S. shrank, we find ourselves in the early to mid-2000s, when China entered the WTO. European companies gained access to a new market, and global ex-U.S. growth outpaced U.S. growth by 3%. Today, however, there is no obvious catalyst that would drive an extended period of outsized growth abroad. While President Trump’s policies are causing some countries to rethink their investment strategies, we suspect the negative headlines will fade over time.

Final Thoughts

We all know that the market experiences three 5%+ pullbacks per year on average. These corrections are healthy and should not be alarming. The data below shows that these pullbacks are common rather than extraordinary. Since 1928, the largest annual drawdown averages -16.0%, yet year-end returns typically remain positive.

The message here is clear: it pays to stay patient, not clever by trying to time the market. Plus, as you see on the right chart, volatility breeds opportunity.

It’s been said that most of the time markets behave quite normally. In fact, this accounts for 85% of the time. During these periods, investing tends to be “easier”. These periods will have little significance to compounding returns over longer periods of time. It’s the other 15% that matters – the periods could be in either direction – elation or terror. How an investor handles these times of euphoria and panic are most important to portfolios. If we are on the precipice of one of these 15% periods, remain calm. As investors, our behavior right now is the most important thing to focus on, as staying invested tends to be one of the most beneficial (in)actions one can do.

Remember, it’s all about perspective. The market was at an all-time high only a few weeks ago and is only off -4.3% year-to-date.

Stay Nimble; Remain Patient.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

The content and/or when a page is marked “Advisor Use Only” or “For Institutional Use”, the content is only intended for financial advisors, consultants, or existing and prospective institutional investors of Aptus. These materials have not been written or approved for a retail audience or use in mind and should not be distributed to retail investors. Any distribution to retail investors by a registered investment adviser may violate the new Marketing Rule under the Investment Advisers Act. If you choose to utilize or cite material, we recommend the citation be presented in context, with similar footnotes in the material and appropriate sourcing to Aptus and/or any other author or source references. This is notwithstanding any considerations or customizations with regards to your operations, based on your own compliance process, and compliance review with the marketing rule effective November 4, 2022.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2504-1.