We’re going to do a new style of the Aptus Musings today; it’s going to be a bit more educational. I had a conversation a few weeks ago with a friend and realized that I needed to know more about this topic: Stablecoins.

It has been a hot topic lately for people, as the stablecoin movement has really picked up some speed. Case in point, Bitwise CIO Matt Hougan recently stated that:

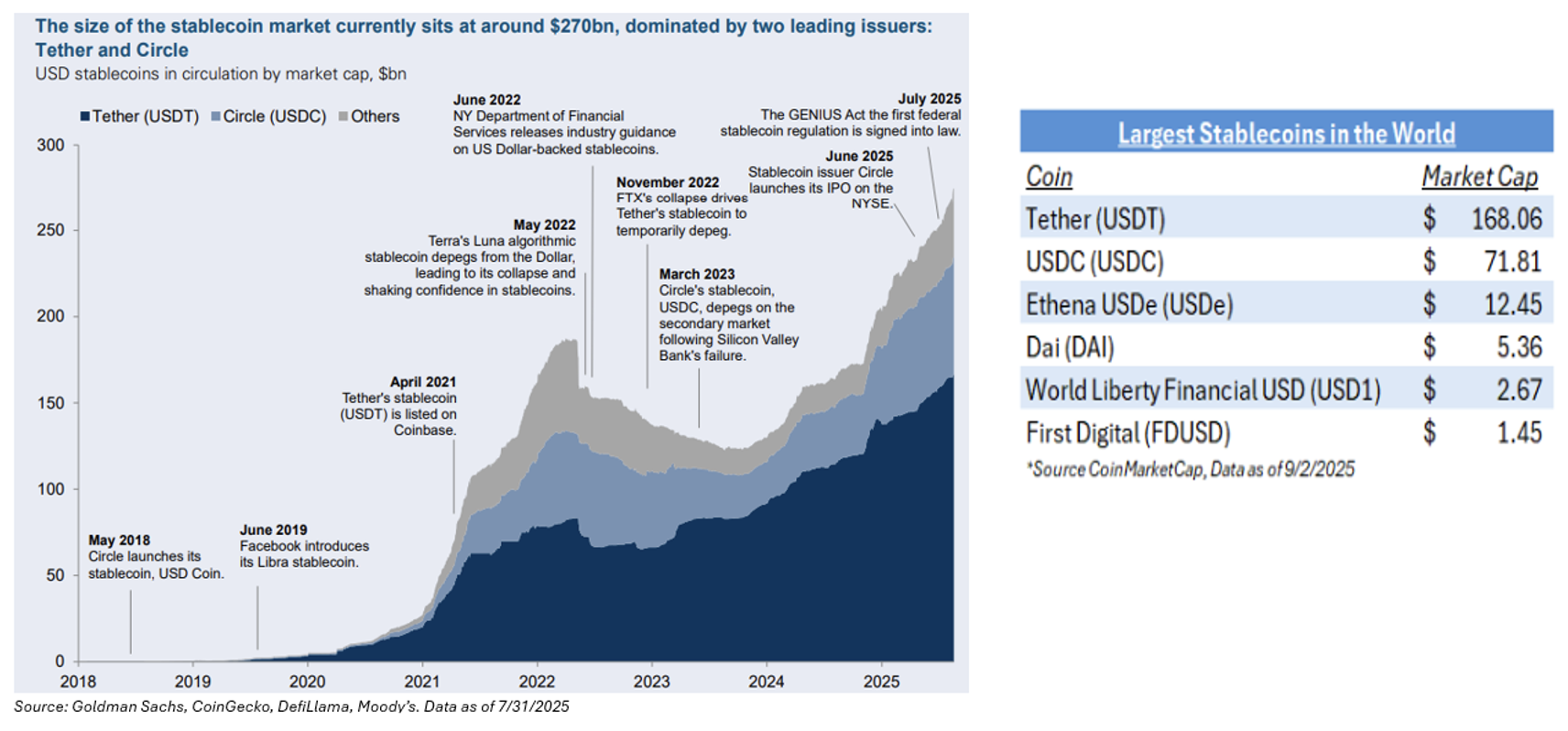

“Stablecoins have emerged as crypto’s second killer app, after Bitcoin. Over the past five years, stablecoin AUM has grown from just over $4 billion to $250 billion, and the U.S. Treasury Department projects they could top $2 trillion by 2030. It’s hard to find another industry where the government’s base case is 700% growth in the next five years.”

Even U.S. Treasury Secretary Scott Bessent projects stablecoins could reach an $8 trillion market. Alongside Circle’s IPO fueling the fire of interest, Washington D.C. passed a few landmark bills in the “crypto” space, and the first has been signed by the President, but others are awaiting Senate approval:

The GENIUS Act: Establishes a unified standard for stablecoin issuance and reserves.

The CLARITY Act: Defines SEC and CFTC oversight for digital assets and allows for a migration path from SEC to CFTC jurisdiction.

The Anti-CBDC Surveillance State Act: Prohibits the Fed from issuing a centralized digital dollar without Congressional approval, promoting decentralized solutions.

To be candid, personally, I don’t find it to be a coincidence that the government is pushing stablecoin legislation right now, mandating that it is backed by U.S. Treasuries and pegged to the U.S. Dollar, during a time where there is a need for more Treasury demand and reliance on the U.S. Dollar. More on that later.

Fun Fact: Tether, which didn’t exist before 2014, recently disclosed that it’s in the top 20 of Treasury debt holders globally.

Let’s get educated. But remember, just because we are educated about a topic or talking about a topic, it does not mean that it’s always a viable investment. I’m a taker of thoughts and opinions.

Summer of Stablecoins

Let’s start with the basics.

What is Stablecoin?

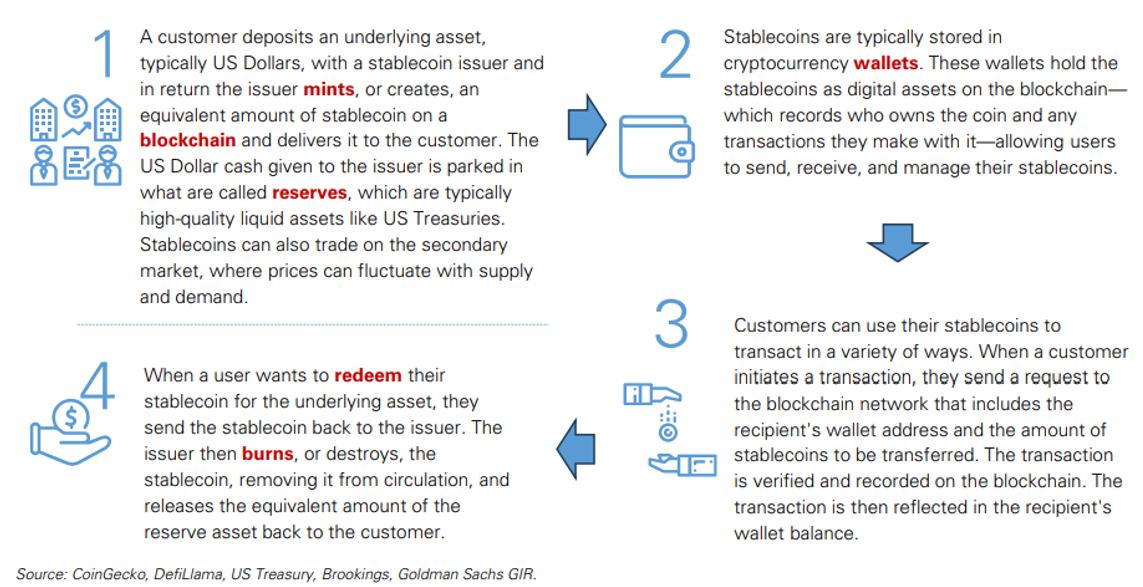

A stablecoin is a kind of digital money that is designed to have no value change. Imagine you have a digital dollar on your phone, and it always equals one real dollar. While most cryptocurrencies like Bitcoin can jump up and down in price, a stablecoin tries to act more like regular money (such as the dollar) by staying the same value. This is usually done by keeping real money in a bank to back up each digital coin. So, it’s a way to use fast, digital money without having to worry about it being worth much less or much more tomorrow than it is today.

To achieve this stability, stablecoin issuers usually keep reserves of the asset they’re linked to, such as holding $1 in the bank for every 1 stablecoin, or by using algorithms that adjust how many coins are available. If the price starts drifting away from the peg, mechanisms kick in to bring it back. For example, if demand for the stablecoin rises and its price goes above $1, new coins may be created; if it falls below $1, coins can be bought back or destroyed to raise the price again. So, while regular cryptocurrencies are mainly driven by market speculation, which can create huge price swings, stablecoins are built specifically to minimize these ups and downs by anchoring their value to something much more reliable.

The Trump administration’s push to make the U.S. the “crypto capital of the world” is progressing with stablecoins as a large contributor. Essentially, stablecoins have become the first crypto product with mainstream utility and institutional clarity, and legitimacy. Not only that, but the GENIUS Act drives adoption across banks, fintechs, Fortune 500 companies, and beyond. The competition is intensifying as firms rush to secure a share of the stablecoin market. There have been several major players, including Amazon and Apple, that have revealed plans to either develop their own stablecoins or begin accepting them as payment methods.

What Are the Use Cases?

Dollar savings products are available outside the US. In countries where access to dollar bank accounts is limited, both savers and institutional investors use stablecoins as an alternative, which increases global demand for the dollar and helps stabilize prices in economies experiencing volatility or inflation. Argentina is a well-known example, where many people choose Circle’s USD Coin (“USDC”) over holding pesos. This trend has inspired numerous businesses across Latin America and Africa, with many start-ups in BRICS nations now offering retail users the ability to hold dollar equivalents through stablecoins.

Currency translation is another major use case, given that stablecoins are digital representations of currencies that can be transferred across borders. If stablecoins did nothing else but save consumers from having to pay a cross-border money transfer fee, that in itself would be enormously valuable, given that such fees average around 7%.

What Are the Cases Against Stablecoin?

-

- Many economists point to the Free Banking Era (1830s – Pre-Civil War) where individual banks could issue proprietary bank notes. In principle, these banks would be obliged to redeem a $1 banknote for a dollar’s worth of gold. But, in practice, some banks would not have enough collateral to redeem their notes, leading to different banknotes to trade at different values – ultimately leading to a rush to get assets, i.e., a bank run.

-

- Even during the banking problem of March 2023, some of the big stablecoin issuers held reserves as deposits at SVB, which holders feared were uninsured, leading to sharp declines in the value of their coins. That could happen again. And even if stablecoin issuers don’t fail to redeem their coins, chaos could still ensue if doubts arise. For example, Circle had $3B of deposits at Silicon Valley Bank (SVB), which led to the USDC to briefly de-peg.

-

- For the vast majority of the US population, existing banking and payment systems are already fairly efficient and reliable, offering few incentives to switch to stablecoins. Only 4% of the U.S. is considered “un-banked”. And while stablecoins could lower the cost of transactions by eliminating credit card interchange fees and freeing consumers from having to accept artificially low bank interest rates, credit card companies and banks provide consumers with a package of services.

Card companies provide fraud protection and deferred payment options, and bank deposits up to a sizable amount are insured, none of which will be the case with a stablecoin. So, any potential savings will likely be outweighed by the loss of these valuable protections and services.

-

- The Fed could tighten monetary policy, which would constrain the money supply, causing the stablecoin gold rush to end before it ever really began. Most major stablecoins like USDC and USDT are pegged to the US dollar and backed by reserves held mainly in interest-bearing assets such as US Treasury bills and cash equivalents. When interest rates are high, those reserves generate significant income, which supports the stablecoin’s operating model, security, and sometimes even ecosystem growth incentives. To put into context, 99% Circle’s revenue was dependent on interest income.

The Commercial Opportunity:

Stablecoin issuers earn revenue by generating more return on their reserves than they spend on partners and operations. This interest, or “reserve income,” cannot be paid directly to coin holders under the GENIUS Act, since stablecoins are classified as payment tools rather than interest-bearing assets. Instead, issuers often share reserve income with partners, who may pass along rewards to users. For instance, Circle pays Coinbase, which then offers USDC rewards on its platform. Models differ: Paxos’ USDG distributes nearly all reserve income to partners (minus a small fee), USDT keeps all of it, and USDC falls in between, sharing about 60% in 2024.

There have been some questions on the commercial bank side of things. Some banks feel threatened by stablecoins, while others feel empowered. Community banks worry that stablecoins could siphon low-cost deposits away from the banking system, which is partly why they supported the GENIUS Act’s provision that prohibits stablecoin issuers from paying interest to coin holders. But mid-sized banks and neo-banks view stablecoins as both a deposit-gathering and customer stickiness tool that could enable other business lines, such as a crypto trading business. So, banks’ fortunes could diverge as stablecoins proliferate. Or is this really a line of business that will have materiality to earnings over longer periods of time if there is a slow adoption? Only time will tell.

Our Thoughts:

Overall, the success of stablecoins likely comes down to fungibility, meaning that every stablecoin must be accepted at full value everywhere. So, the question is: Is there staying power?

This is the direct factor that could lead to an increased speed of adoption, which has so far been limited. Stablecoin usage remains largely confined to crypto-asset trading, with minimal uptake in consumer payments. While adoption may grow with regulatory and technological maturity, the outlook remains highly uncertain. For any significant migration, it would require stablecoins to offer either better economics than traditional deposits or lower payment frictions – neither of which seems likely anytime soon. That doesn’t mean that we shouldn’t be educated on the topic. Knowledge is power.

Personally, when it boils down to it, as mentioned in the intro, this is one of the government’s ways to strengthen the reliance on the dollar. If the Genius Act mandates that high-quality reserves must be used, i.e., Treasuries, then that’s a straight increase to the bid, driving demand. Given the need for increased Treasury demand in the market, I don’t believe it to be coincidence that the Government is pro-stablecoin regulation right now. This is straight from the horse’s mouth:

As investors, we may not need to take a side on whether there are merits to stablecoin investments or not – it’s not necessarily a black and white issue. Because at the end of the day, inflows into stablecoin are likely just going to increase the amount of capital that can be spent by consumers (specifically international adoption), which is a positive, as much of the money will be taken out of money-markets or deposits, but still backed by USD or US Treasuries (i.e., increase demand for USD). While interesting, I think that it pays more to be knowledgeable on the subject, than invested.

As for Client Portfolios – FAQ

1. How are we invested? I.e., the introduction of the Purchasing Power Protection Sleeve:

There is an obvious difference between stablecoins and cryptocurrency – one is pegged, one is not. While we may own a few companies in our Aptus ETFs that would benefit from the tailwinds in stablecoins, we think our messaging is best expressed through the recently launched Aptus Purchasing Power Protection Sleeve (“PPP”) – It’s a mixture of Bitcoin and Gold.

Email us for more details.

In the words of our CIO, JD Gardner, CFA, “The only crypto worth talking about is Bitcoin, as it has different characteristics than other cryptos and other cryptos don’t have the network of Bitcoin and never will.”

We would prefer something that is not pegged to Treasuries or the USD, as it does not address one of the biggest problems facing advisors today – protecting the value of your assets. We think the Aptus PPP can do this more efficiently. Because if investors are substituting bitcoin for stablecoin, which is backed by the UST, we think they may fall back into the trap of injecting longevity risk – again, stablecoin is backed by UST and pegged to the dollar. One could maybe say…Stablecoins are also guaranteed loss coins.

2. Is Visa (V), which is owned in the Aptus Compounders Sleeve, at risk?

Another narrative impacting the portfolio is blockchain and the rise of stablecoins, which potentially impacts the payments industry as a faster, cheaper, and more global alternative. While the technology behind stablecoins is promising, we see them as part of the current ecosystem, not a replacement. A stablecoin functions more like a currency than a payment rail, equivalent to digital cash (often backed by a U.S. asset), transacting on a blockchain. For most day-to-day uses, the stablecoin must be converted back to fiat currency.

Quite simply, the overall cost of stablecoin does not account for the full end-to-end use costs, which include on and off-ramp foreign exchange, regulatory compliance, settlement, and fraud protection. This is why we believe stablecoin platforms will and have already partnered with trustworthy and well-capitalized networks such as Mastercard and Visa, similarly to what we experienced previously with other FinTech companies and their threatened disruption. Therefore, we will continue to monitor, but we are less worried about this narrative, and the payment names remain important investments in our portfolio.

For a complete list of holdings for the Aptus Compounders Sleeve, see disclosures below.

Please reach out if you have any questions or would like to talk through this.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

Aptus Compounders Holdings as of 06/30/2025: American Tower Corp. (AMT), Amazon.com, Inc (AMZN), Broadridge Financial Solutions, Inc (BR), Chemed Corp. (CHE), Copart Inc (CPRT), Diamondback Energy, Inc (FANG), JPMorgan Chase & Co (JPM), Microsoft Corp. (MSFT), ServiceNow Inc (NOW), NVIDIA Corp. (NVDA), Progressive Corp. (PGR), Quanta Services, Inc (PWR), Roper Technologies Inc (ROP), Visa Inc (V), and Walmart Inc (WMT).

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

When a page is marked “Advisor Use Only” or “For Institutional Use”, the content is only intended for financial advisors, consultants, or existing and prospective institutional investors of Aptus. These materials have not been written or approved for a retail audience or use in mind and should not be distributed to retail investors. Any distribution to retail investors by a registered investment adviser may violate the new Marketing Rule under the Investment Advisers Act. If you choose to utilize or cite material we recommend the citation, be presented in context, with similar footnotes in the material, and appropriate sourcing to Aptus and/or any other author or source references. This is notwithstanding any considerations or customizations with regards to your operations, based on your own compliance process, and compliance review with the marketing rule effective November 4, 2022.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2509-8.