The TV show, South Park, is essentially a weekly fever dream where four foul-mouthed children serve as the only voice of reason in a universe populated by celebrity-obsessed morons and eldritch horrors. It’s the only place on Earth where you can watch a group of fourth graders who have survived more world-ending apocalypses than most market participants, followed immediately by a profound philosophical lecture on the First Amendment. It’s crude, it’s chaotic, and it’s consistently been “going too far” for nearly thirty years, proving that nothing is sacred, everyone is an idiot, and somehow, it’s all Canada’s fault.

The TV show, South Park, is essentially a weekly fever dream where four foul-mouthed children serve as the only voice of reason in a universe populated by celebrity-obsessed morons and eldritch horrors. It’s the only place on Earth where you can watch a group of fourth graders who have survived more world-ending apocalypses than most market participants, followed immediately by a profound philosophical lecture on the First Amendment. It’s crude, it’s chaotic, and it’s consistently been “going too far” for nearly thirty years, proving that nothing is sacred, everyone is an idiot, and somehow, it’s all Canada’s fault.

In the case of the market, the fault appears not to fall on the scapegoat of Canada, but with the U.S. and Iran, as investors feel like they’re living in an eldritch horror, given the constant barrage of volatile, politically driven war headlines. As many know, mixing markets and politics has a success rate about as high as Kenny McCormick surviving an episode. Thus, investors need to follow the north star of a newer character, PC (politically correct) Principal, as the voice of reason, to make sure we keep things between the political division lines.

PC Principal serves as the high-stakes day trader of social justice, functioning as a hyper-aggressive, Oakley-wearing embodiment of “woke” culture pushed to its extreme. Modeled after a stereotypical frat bro, this “social justice warrior” enforces political correctness with the same bone-crushing intensity and physical intimidation one might typically reserve for winning a championship football game.

Let’s heed the wisdom of PC Principal and follow his guide to navigating microaggressions in the market. When markets feel like it’s been crude, it’s been chaotic, and when emotions have “gone too far”, it always pays to get back to the basics – and the basics are simple:

Focus on Growth: The S&P 500 just posted its 5th straight quarter of double-digit EPS growth, which is a record.

Focus on Profitability: Both the Cap Weighted and Equal Weighted S&P 500 have witnessed expansion in their operating margin (profit). Remember, it’s difficult for the market to get into trouble when margins are increasing or remaining stable.

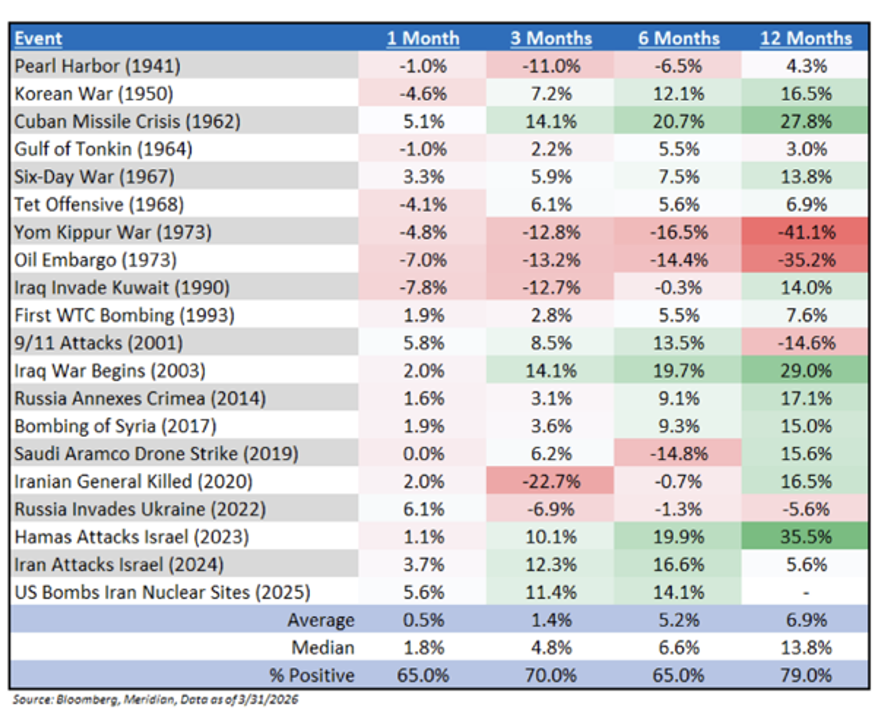

Markets look at geopolitical events solely through the lens of the impact of critical resources (i.e., oil), and unless the event is going to reduce the supply of oil (and make the price rise, slowing global growth), then markets will largely ignore the event. Yet, the current debacle has resulted in the “closing” of the Strait of Hormuz, a major global oil transit for 20% of the world’s oil, which will create a negative impact on markets as oil prices have risen sharply in response. What does that mean for markets?

Historically, markets have proven surprisingly resilient in the face of global instability. As shown in the adjacent chart, selloffs triggered by oil shocks and geopolitical crises tend to be brief. Since 1941, data from twenty major events, including wars and military conflicts, reveal a trend that is far more encouraging than typical news cycles suggest. Despite the initial uncertainty these moments cause, the S&P 500 has been up 79% of the time one year later, boasting a median gain of +13.8%.

This performance actually exceeds the average annual return for a standard year. The takeaway is clear: historically, the market possesses a remarkable capacity to recover from and look past even the most distressing headlines.

It’s a great reminder that it pays more to be patient than clever. And that there are no participation medals in the stock market, as achieving higher potential returns typically requires the acceptance of greater volatility. Pullbacks are healthy and normal – political correctness be told – if an investor worries about a 10% pullback in the markets, maybe investing isn’t for you.

Look at the overall resiliency of the market over the past few years. Going back to early 2022, we’ve witnessed Russia’s invasion of Ukraine, 9% inflation, 550 basis points of U. S. Federal Reserve rate hikes, the second, third, and fourth biggest bank failures on record, historic increases in tariff rates, and a war in the Middle East. Yet over that period, stocks were up more than 50%. Equity resilience has been generated by strong earnings, AI capex, and addictive levels of fiscal stimulus. There are plenty of reasons to be optimistic.

While it’s understandable that investors likely need to check their privilege, after the recent string of above-average market performance, our highest conviction remains that patrons need to continue to own risk assets. Investors need to be “super cereal” about the threat to one’s portfolio right now, and it simply isn’t geopolitics; it’s ManBearPig – (1) half inflation, (2) half bond correlation and growth worries, and (3) half that the hurdle rate is likely higher than most believe. As Al Gore states: “It’s the single biggest threat to our planet portfolios.”

In general, it is not PC to criticize the market, and it certainly has not been profitable to bet against it. While the domestic political backdrop has generated some lack of enthusiasm, investors need to stay focused on the basics – growth and profitability. Remember, over longer periods of time, the market is stunning and brave.

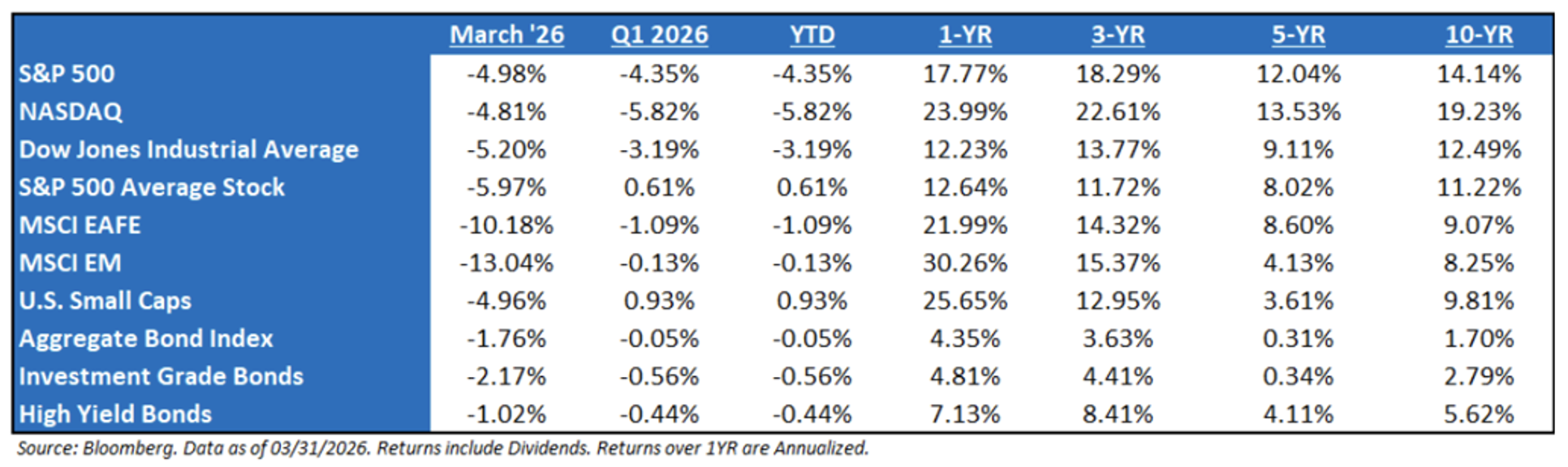

Market Recap: Q1 2026

Domestic and International markets were not a “safe space” for the risk-averse investors in Q1 2026. The quarter was defined by a sharp shift from early optimism to pronounced volatility, as geopolitical shocks and macro uncertainty rattled global equities. Markets entered the year supported by solid earnings expectations, AI-driven growth themes, and hopes for easier monetary policy, but sentiment deteriorated quickly after a January selloff tied to renewed tariff tensions and escalating conflict in the Middle East. By March, major U.S. indices had fallen into correction territory, with the S&P 500 down notably from its peak and the Nasdaq off more than 10%. Rising oil prices, inflation fears, and shifting rate expectations compounded the risk-off tone, even as corporate fundamentals remained relatively strong, with S&P 500 earnings still projected to grow in the low double-digits.

earnings expectations, AI-driven growth themes, and hopes for easier monetary policy, but sentiment deteriorated quickly after a January selloff tied to renewed tariff tensions and escalating conflict in the Middle East. By March, major U.S. indices had fallen into correction territory, with the S&P 500 down notably from its peak and the Nasdaq off more than 10%. Rising oil prices, inflation fears, and shifting rate expectations compounded the risk-off tone, even as corporate fundamentals remained relatively strong, with S&P 500 earnings still projected to grow in the low double-digits.

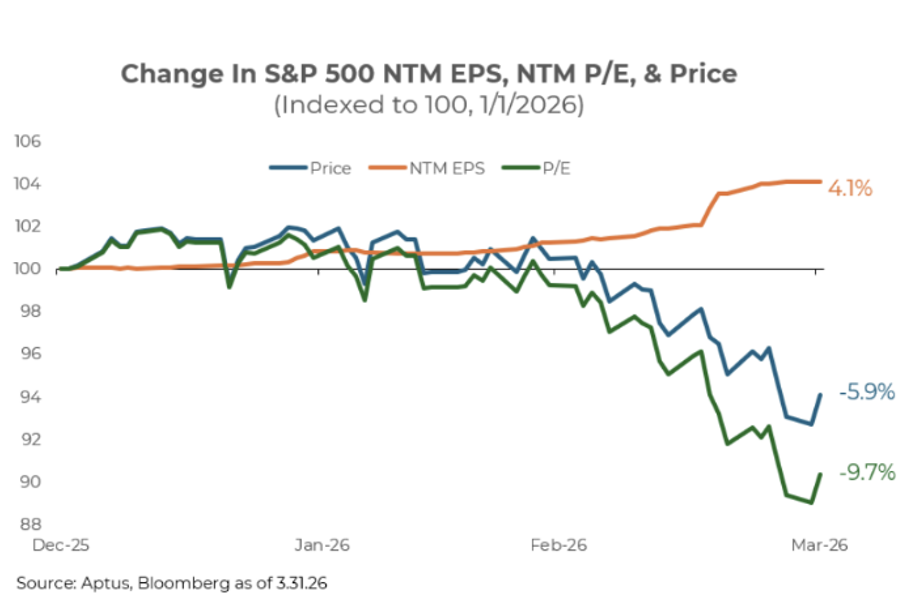

Total return comes from three (3) different sources: (1) Yield, (2) Earnings Growth, and (3) Valuation Changes. While Yield tends to be somewhat static, always slightly benefiting returns, the latter two tend to be more dynamic. Earnings Growth is a measure of economic mobility, and changes in valuation signal the investment crowd’s sentiment about the current market.

Earnings: Earnings grew above expectations that were set at the beginning of the year. In fact, 2026 expected earnings growth was originally expected to be 12.9%, but after a strong Q1 earnings season, expectations rose to 17.0%, an accretive move for markets of +4.1%.

Valuation: Given geopolitics and skepticism about artificial intelligence (“AI”), the market’s sentiment gauge turned bearish in the quarter, as valuation detracted from performance by -8.4%, falling below 20x.

The negative returns seen in Q1 were driven entirely by a decline in multiples. While many investors have long anticipated this “multiple contraction” – arguing that stocks were overvalued – the shift finally materialized this quarter as valuations reset lower. Despite this pullback, we maintain that current multiples are justified; the market’s underlying composition has evolved so significantly over the last several decades that historical comparisons from 10 or 40 years ago no longer serve as accurate benchmarks.

The negative returns seen in Q1 were driven entirely by a decline in multiples. While many investors have long anticipated this “multiple contraction” – arguing that stocks were overvalued – the shift finally materialized this quarter as valuations reset lower. Despite this pullback, we maintain that current multiples are justified; the market’s underlying composition has evolved so significantly over the last several decades that historical comparisons from 10 or 40 years ago no longer serve as accurate benchmarks.

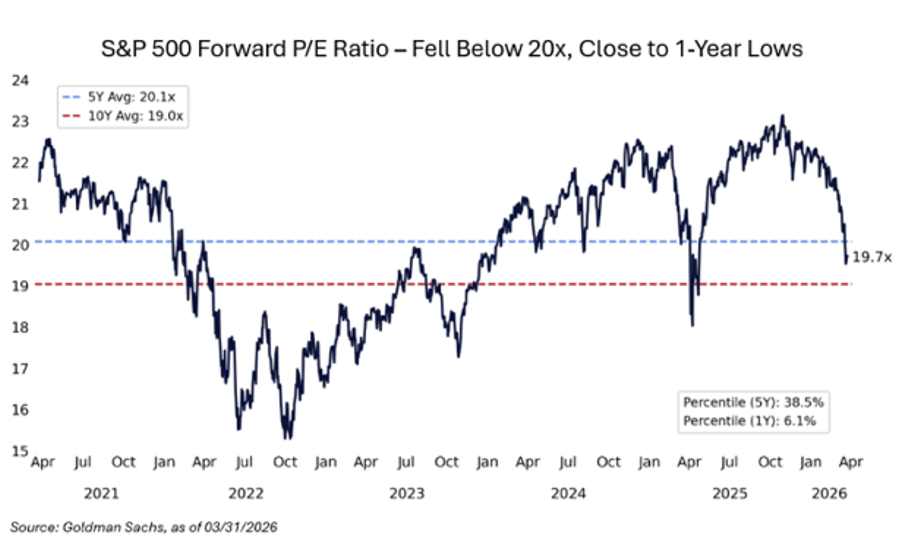

Regarding valuation, whether an investor looks at P/E (price-to-earnings) or EBITDA (2026 Edition – Earnings Before Iran, Tariffs, and Donald Announcements), the market’s valuation is much more palatable than where it stood a year ago. SPX forward P/E is sitting ~19.7x, below its 5-year average of ~20.1x, and now in the 6th percentile of its 1-year range (lowest since April’s Liberation Day). Historically, when the S&P 500 forward P/E falls below 20x, forward returns have been favorable.

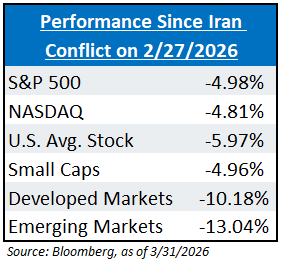

After a year of skepticism, domestic markets and the US dollar continued to show that they are the “safe space” for global assets when crisis struck, debunking a lot of the de-dollarization and a change in world order narratives. Furthermore, when growth is expected to weaken, capital flocks to areas of the market that are expected to witness growth, and that happens to be in the United States. While International markets may still be leading the year relative to domestic markets, markets favored dollar-denominated aspects when volatility struck after the Iranian War began in late February.

debunking a lot of the de-dollarization and a change in world order narratives. Furthermore, when growth is expected to weaken, capital flocks to areas of the market that are expected to witness growth, and that happens to be in the United States. While International markets may still be leading the year relative to domestic markets, markets favored dollar-denominated aspects when volatility struck after the Iranian War began in late February.

All-in-all, the S&P’s modest 4.35% dip in the quarter suggests a surprising level of resilience. When a primary asset holds its ground despite negative headlines, it shows that sometimes it’s hard to keep a good market down.

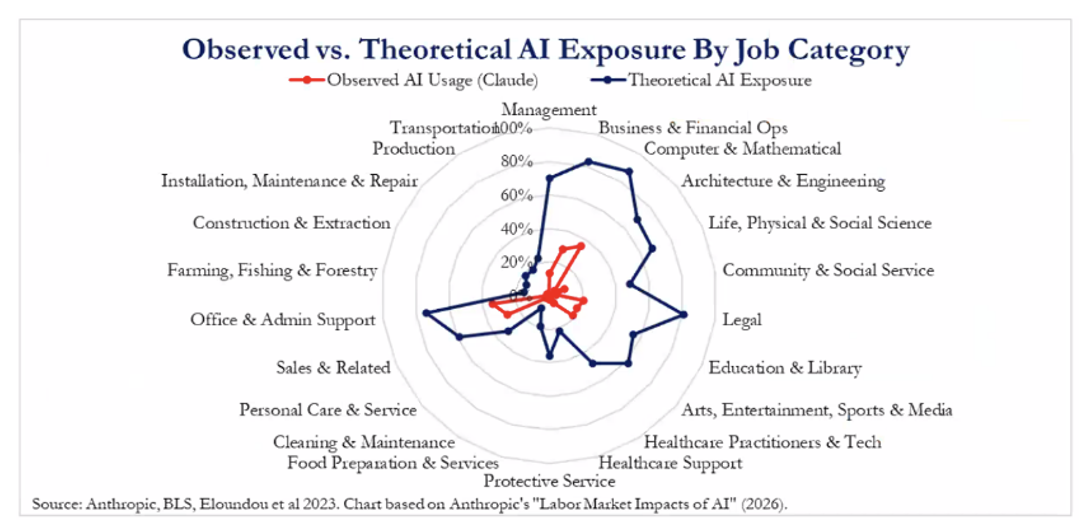

U.S. Labor Market Fireside Chat: AI Took Our Jobs!

The valuation reset witnessed in Q1 is derived and mirrors the “They took our jobs!” anxiety of South Park’s Amazon storyline, where automation fundamentally devalued the traditional labor force. Just as the South Park townspeople struggled to find their worth in a world of sorting robots, investors are recalculating the market’s “multiple” to account for an AI-driven economy, a technology that is considered revolutionary, not evolutionary. This shift isn’t just about valuation; it’s a recognition that the market’s composition has changed – shifting from human-centric productivity to an automated reality where historical benchmarks are as obsolete as a roadside mall.

fundamentally devalued the traditional labor force. Just as the South Park townspeople struggled to find their worth in a world of sorting robots, investors are recalculating the market’s “multiple” to account for an AI-driven economy, a technology that is considered revolutionary, not evolutionary. This shift isn’t just about valuation; it’s a recognition that the market’s composition has changed – shifting from human-centric productivity to an automated reality where historical benchmarks are as obsolete as a roadside mall.

Markets have been accustomed to rewarding AI winners, but in Q1, the market faced an existential question of deciding who would be AI losers, and it relentlessly punished them. What scared the market most was that many of the jobs targeted by AI disintermediation are considered “white” collar jobs, unlike the jobs that were displaced in South Park, CO. There’s no example better to point to than Software stocks to provide an example of AI disintermediation – these companies were down 24%+ in Q1, yet earnings expectations continued to climb, meaning that a lot of the damage is due to valuation compression. But this begs for a bigger question: What will the labor force look like in an advanced computing, agentic world?

Unlike the South Park episode, the market isn’t likely to be visited by the ghost of Karl Marx, but similarities to his 1848 novel, the Communist Manifesto, are definitely haunting “AI Doomers”. Karl Marx argued that Capitalism would negatively impact the workforce. Marx’s take may have sounded very logical at the time, but it was also catastrophically very wrong. Here are Marx’s main thoughts:

-

- The Drive for Efficiency: To maximize margins, business owners are forced to relentlessly optimize labor, typically by replacing human effort with more efficient technological solutions.

- The Shift to Automation: Intense market competition compels capitalists to pivot their investment away from human workers and toward “constant capital”, i.e., machinery and automated systems.

- The Labor Surplus: By automating roles, the system maintains an “industrial reserve army” of the unemployed. This surplus of workers keeps demand for jobs high and wages perpetually suppressed.

- Wealth Concentration: As production becomes increasingly automated, wealth flows upward, concentrating in the hands of the few who own the technology and means of production.

- The Consumption Gap: Eventually, the system faces a paradox: as wages are squeezed to boost profits, the working class loses the purchasing power necessary to buy the very goods being mass-produced.

Obviously, this did not work out in practice because people underestimate the power of Capitalism; Capitalism always finds a way.

Technological displacement on farms enabled the creation of higher-paying modern industries; historically, innovation destroys old roles only to birth unimagined new ones. Despite past fears – like those during the 1990s internet boom – employment and real wages have remained stable as the economy adapted. While “AI Doomers” predict a permanent underclass, mimicking Marx’s ideology, they ignore 175 years of evidence showing that technology consistently replaces lost jobs with better opportunities.

Again, why would investors believe that this time is different? While there may be an emotional disconnect between the non-linear advancement of technology, we believe that there will be a more nuanced approach to adoption. For AI to truly trigger a permanent economic downturn, several extreme conditions would have to be met at once: adoption would need to skyrocket, machines would have to replace humans almost entirely, and the government would have to stand by without intervening – unlikely. Not to mention the massive amount of computing power to scale without limits, while new investments fail to create new jobs. Of which, the global infrastructure does not have the ability to power this, given current bottlenecks.

History suggests productivity gains do not automatically translate into labor withdrawal or demand collapse because they alter the composition of demand, expand real incomes, and generate new industries. Economists underestimated the elasticity of human wants.

demand, expand real incomes, and generate new industries. Economists underestimated the elasticity of human wants.

While revolutionary technology, such as AI, can seem overwhelming, just remember, the stock market is still all about stocks, which are all about underlying businesses.

Businesses adapt; they always have and always will. While AI may seem scary, it remains a reason to be optimistic, as investors currently may not be able to comprehend the labor ecosystem of the future, much like it was difficult to imagine a world with the internet in the late 1990s and the new jobs that were created from it.

While no one can promise that AI won’t “take our jobs,” the productivity and evolution of the future job market is something to look forward to, especially for those who own risk assets.

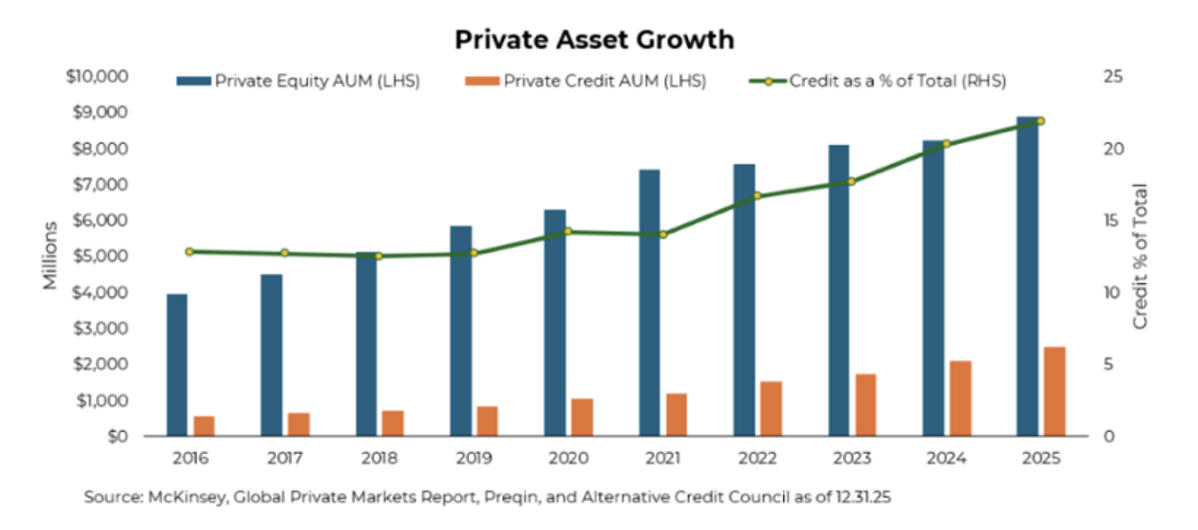

Alternative Asset Fireside Chat: Respect the Marginalized Assets

Eric Cartman might just be the world’s most unlikely critic of private equity. When he dons his badge and nightstick, he transforms into the ultimate (yet self-appointed) enforcer, demanding absolute “authoritah” from a world that rarely takes him seriously.

Eric Cartman might just be the world’s most unlikely critic of private equity. When he dons his badge and nightstick, he transforms into the ultimate (yet self-appointed) enforcer, demanding absolute “authoritah” from a world that rarely takes him seriously.

This same aggressive assertion of power is currently playing out in the private credit market. Often dubbed “shadow banking,” this sector sees non-bank lenders and private equity firms bypassing traditional financial institutions to lend directly to companies. In this unregulated frontier where the old rules don’t always apply, Cartman would see a chaotic landscape in desperate need of his brand of discipline. To him, it’s a personal affront to the “authoritah” he believes is necessary to keep the gears of the economy – and South Park – grinding along.

What do we mean when we say that private equity firms bypass traditional institutions? One big difference between what happened during the banking fiasco of 2023 and what is happening to private credit now is that banks are not only supervised by the Fed, but they also have the Fed, the FHLB, and others as a liquidity backstop to prevent bank runs. There is no such backstop for private credit. The other big difference is that banks cannot restrict withdrawals from regular accounts. Private credit can and has. Those restrictions may prevent a run, but they also make it more difficult to raise new funds, which will be a problem for industries, like tech, reliant on private debt for growth.

fiasco of 2023 and what is happening to private credit now is that banks are not only supervised by the Fed, but they also have the Fed, the FHLB, and others as a liquidity backstop to prevent bank runs. There is no such backstop for private credit. The other big difference is that banks cannot restrict withdrawals from regular accounts. Private credit can and has. Those restrictions may prevent a run, but they also make it more difficult to raise new funds, which will be a problem for industries, like tech, reliant on private debt for growth.

This is why following the flows of private credit and capping withdrawals is important.

So, what’s happening? The problem starts with “marks.” Public markets reprice in real-time. As investor sentiment toward less-liquid, higher-risk loans has soured, publicly traded prices drop instantly. Private credit, however, moves slowly, and only “marks” the price of their investments every so often. Some investors call this volatility laundering.

When private marks remain elevated while public equivalents are cheaper, a perceived arbitrage opportunity emerges. Investors realize that their “private” dollar is worth $1.00 inside the fund, but the “equivalent” assets in the public market are trading at $0.92. The rational move? Get out at par while you still can. But most private equity funds have a redemption cap, such as 5% or 7% of net asset value. These withdrawals can cause a “theatre fire” scenario: The building isn’t necessarily burning, but because there is only one small exit, people may prefer to leave before a potential stampede.

This gives managers two options: (1) close the fund, refusing to honor redemptions beyond the cap, and (2) sell the “crown jewel” assets at a discount. In a way, the “illiquidity premium” that investors loved on the way up has become an “illiquidity penalty” on the way down.

But, in our opinion, this isn’t something to completely worry about right now, and it likely won’t create a systemic financial problem. It’s easy to sell fear when a black box holds illiquid assets. Systemic financial collapses aren’t triggered by risky borrowers, but by over-leveraged lenders. While popular opinion blames high-risk loans, history shows that panics – like the 2008 Global Financial Crisis or the 1998 LTCM collapse – occur only when the lenders themselves lack the liquidity to cover their own massive leverage. Goldman says that these loans average 40% loan-to-value (“LTV”) with interest coverage ratios of 2x, thus not heavily levered.

While concerns about private credit-led market disruption are rising, high default rates – even in double digits – are unlikely to cause a Financial Crisis type of snowball effect. The real danger lies not with the borrowers, but with the lenders. If the institutional backers of private credit, such as pension funds and insurers, face their own liquidity crunches or lose access to cheap capital, they may be forced to sell assets. This “forced selling” is what triggers a systemic doom loop and a full-scale financial panic.

But these types of investors (more institutional) tend to have rationality and time on their side. The recent growth in the asset class has mostly come from the retail crowd that doesn’t have the same investment horizon as institutions – it’s much shorter. It’s estimated that 90% of the $2.5T asset remains owned by institutional investors, and the remaining 10% is with the more emotional retail crowd. Even if analysts call for 8% – 12% default rates, which are correct, in the grand scheme of things, it’s not a career-ending injury, only equating to $200M – $300M in losses. At the end of the day, credit is credit, and coverage ratios are healthy. But their valuation could be wrong – which is an equity problem, not a private credit problem.

We don’t necessarily recommend investing in this asset class – since more efficient and liquid alternatives exist – but we currently see no evidence of a systemic threat. No matter what, anything is better than following South Park Bank’s investing advice – and it’s gone…

Conclusion: The Case of Skeptical Optimism

In the markets, cynicism is expensive. We believe in skeptical optimism: the idea that while you should watch your back, you should always bet on growth. Pessimists might get lucky occasionally, but they rarely build lasting wealth.

Pessimism about the long-term does not align in any way with a historic worldview. Investors can choose to believe that right now is the beginning of the end, but that is a bet against all of human history and against human nature itself. As has always been the case, progress occurs against an inevitable backdrop of catastrophe. Always has, always will. Invariably, you can always find what you go looking for, and your investment results will probably mimic that worldview.

end, but that is a bet against all of human history and against human nature itself. As has always been the case, progress occurs against an inevitable backdrop of catastrophe. Always has, always will. Invariably, you can always find what you go looking for, and your investment results will probably mimic that worldview.

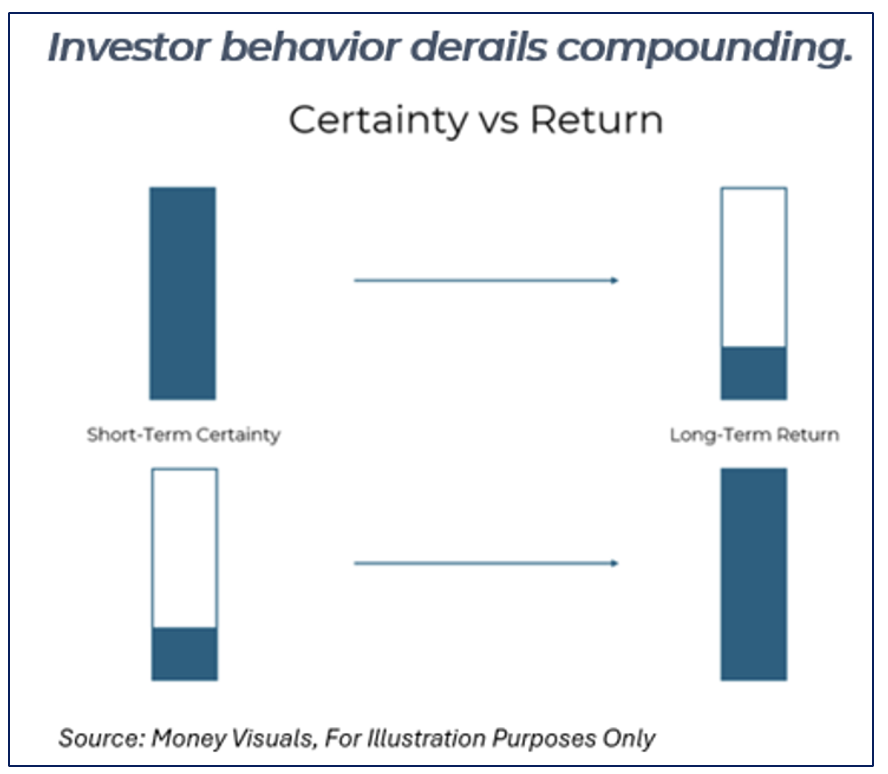

It’s also important to avoid emotional investing. Investors often make poor decisions when emotions drive actions. The more certainty you seek from your portfolio in the short term, the lower your long-term returns will be, and the lower your long-term returns are, the probability of achieving your investment goals will decrease in lockstep.

Just $1 invested in the S&P 500 in 1922 would be worth nearly $14,000 today, so where are all the historical could-have-been billionaires? The missed opportunities are not because of wars, recessions, or crises, but because of emotional and volatile investor behavior. It is not adverse market conditions that derail compounding; it’s investors’ reaction to them. At the end of the day, it’s about how your portfolio performs when you are wrong, not when you are right, that will make all the difference.

We believe that following a tried-and-true asset allocation structure – such as more stocks, less bonds, while remaining risk neutral – will provide a true “safe space” that would even make PC Principal jealous.

Happy Livin’,

The Aptus Investment Committee

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

The content and/or when a page is marked “Advisor Use Only” or “For Institutional Use”, the content is only intended for financial advisors, consultants, or existing and prospective institutional investors of Aptus. These materials have not been written or approved for a retail audience or use in mind and should not be distributed to retail investors. Any distribution to retail investors by a registered investment adviser may violate the new Marketing Rule under the Investment Advisers Act. If you choose to utilize or cite material, we recommend the citation be presented in context, with similar footnotes in the material and appropriate sourcing to Aptus and/or any other author or source references. This is notwithstanding any considerations or customizations with regards to your operations, based on your own compliance process, and compliance review with the marketing rule effective November 4, 2022.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2510-2.