The award-winning HBO series, Succession, is a razor-sharp corporate tragedy centered on the inevitable chaos of a changing of the guard, proving that transition is rarely a smooth or welcoming process. When the formidable patriarch of a global media empire, Logan Roy, faces a decline in health, his deeply flawed children scramble to prove their worthiness to claim the throne, while the patriarch himself stubbornly clings to control. The series brilliantly captures the toxic friction of organizational and generational change, showing how an institutional refusal to adapt turns a necessary evolution into a destructive war of attrition for a family unable to move forward.

The award-winning HBO series, Succession, is a razor-sharp corporate tragedy centered on the inevitable chaos of a changing of the guard, proving that transition is rarely a smooth or welcoming process. When the formidable patriarch of a global media empire, Logan Roy, faces a decline in health, his deeply flawed children scramble to prove their worthiness to claim the throne, while the patriarch himself stubbornly clings to control. The series brilliantly captures the toxic friction of organizational and generational change, showing how an institutional refusal to adapt turns a necessary evolution into a destructive war of attrition for a family unable to move forward.

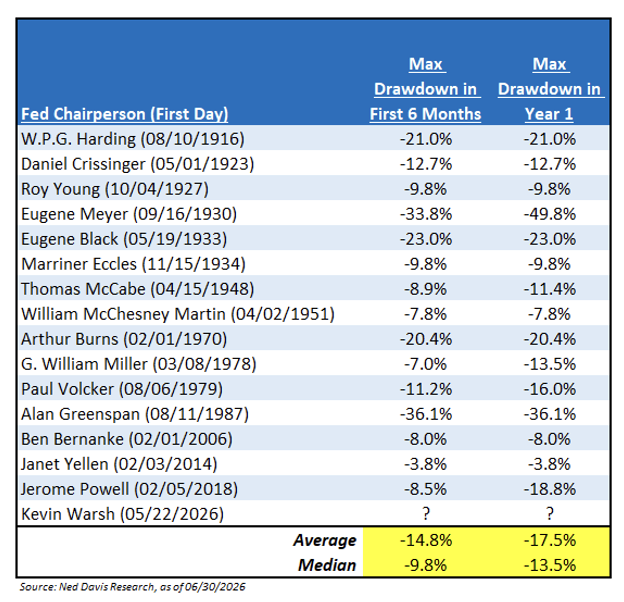

The market, specifically within the Federal Reserve, is currently undergoing a change of its own guard – Kevin Warsh took over for the previous Fed Chairman, Jerome Powell, in May. This transition will likely not be as sinister as the one surrounding the Roy family; it has been highly publicized that the new mentality of Kevin Warsh may create its own toxic friction of organizational change. While many investors view the upcoming changes as bad – and the market will likely challenge the new Fed quickly as it has always done – sometimes a refresh is healthy. In fact, the Fed has had many refreshes in its time, as it’s heeded the call to be pragmatic about evolving with the times – and maybe this time is no different. Below are the two topics of change for the Fed:

1. Warsh wants to rein in the Fed’s heavy hand and let markets play a bigger role in driving the economy, i.e., less balance sheet reliance; and

2. Warsh wants a Fed that lets markets do their own estimating – fewer press conferences, no dot plot handholding, and a central bank that acts rather than narrates.

Both changes ultimately reflect a level of anxiety from investors due to their preference for the predictability that comes with heavy central bank oversight. Said differently, people dislike change. Moving forward, the Fed is looking to move policy away from boosting asset prices via balance sheet expansion and toward productive capital, capex, and productivity.

The adage is Don’t Fight the Fed. Investors should expand that in the Warsh era: Don’t Fight the New Fed Either. The tools may be slightly different, and the communication style is dramatically different, but the underlying mandate of price stability in service of long-term economic growth will not change. And that mandate, executed with competence, has historically been bullish for risk assets.

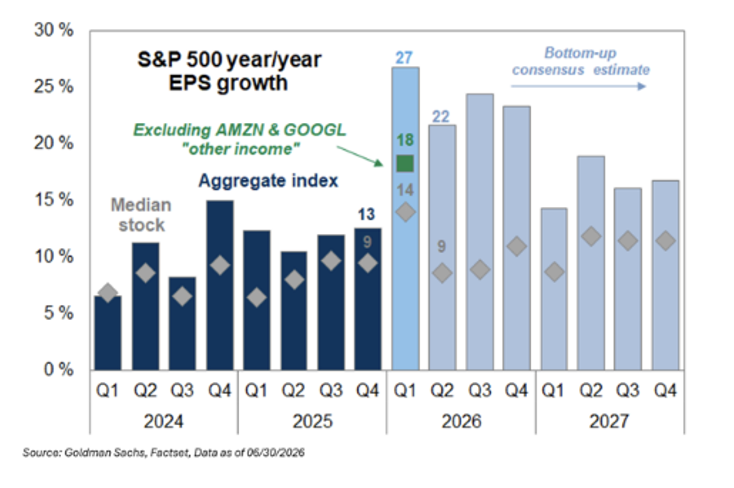

When the market feels overwhelmed with change, as many investors are witnessing today through revolutionary advancements in computing, a potential new Federal Reserve regime, and the rise of de-globalization, it always pays to focus on the basics. Many believe complex problems demand complex solutions, when in fact the opposite is true: the best answers are often the simplest ones. The market is no different. Beneath all the noise and change, the foundational drivers remain strong: (1) Growing economic earnings and (2) Increasing corporate profitability.

regime, and the rise of de-globalization, it always pays to focus on the basics. Many believe complex problems demand complex solutions, when in fact the opposite is true: the best answers are often the simplest ones. The market is no different. Beneath all the noise and change, the foundational drivers remain strong: (1) Growing economic earnings and (2) Increasing corporate profitability.

-

- Economic Growth (Right): Q1 ‘26 delivered one of the strongest earnings seasons ever. The S&P 500 grew earnings by nearly 27% – the results marked the sixth consecutive quarter of double-digit growth. What made this quarter particularly notable was the breadth – smaller companies flourished alongside their large-cap peers, signaling that the earnings recovery is expanding well beyond the technology sector.

-

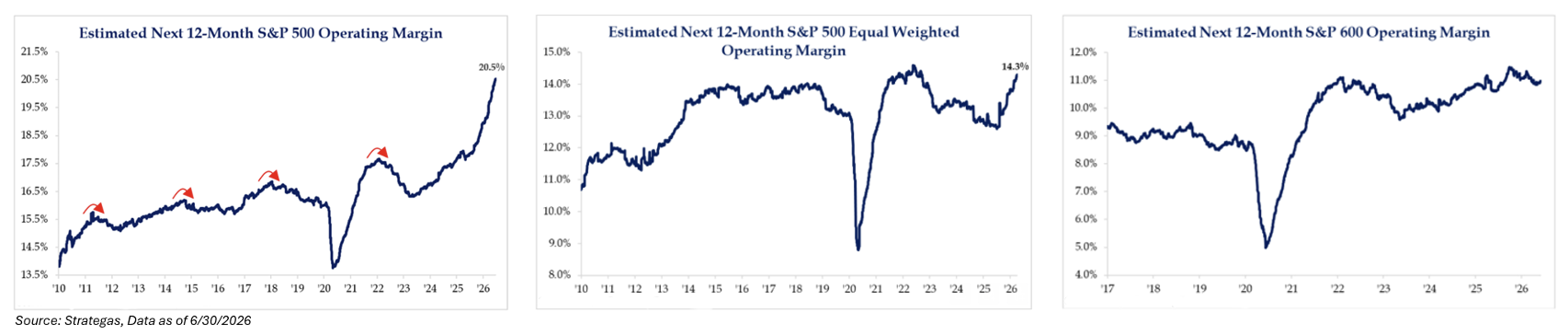

- Corporate Profitability (Below): The trend of increasing margins highlights how companies are successfully improving profitability, with technology playing an increasingly influential role across the index. Markets tend to remain stable when margins are expanding; it’s typically when this trend begins to reverse that risks become more pronounced. For now, despite recent geopolitical events, there appears to be little evidence of a downward shift.

The show Succession is basically a warning about refusing to change. The Roy family spent four seasons clinging to the same old patterns – chasing the patriarch’s approval & scheming instead of growing – while the media world shifts underneath them. None of them adapt, and that’s exactly what destroys them. Investing is no different.

Don’t be a Roy – embrace change – or at least give it a chance. Every business cycle is different, and the market will always decide who eats and who crawls – know which one you are. While the market’s rules of engagement will continue to change over time, the one constant should always remain focused on the simplistic basics: (1) Earnings, and (2) Profitability. Remember, it seems that throughout history, and even more so today, telling everyone the world is going to end is quite a lucrative career path. But it can only end once.

Stay Pragmatic. Stay Optimistic. Stay Resilient.

Market Recap Q2 2026: The Market Had Its Boar on the Floor Moment

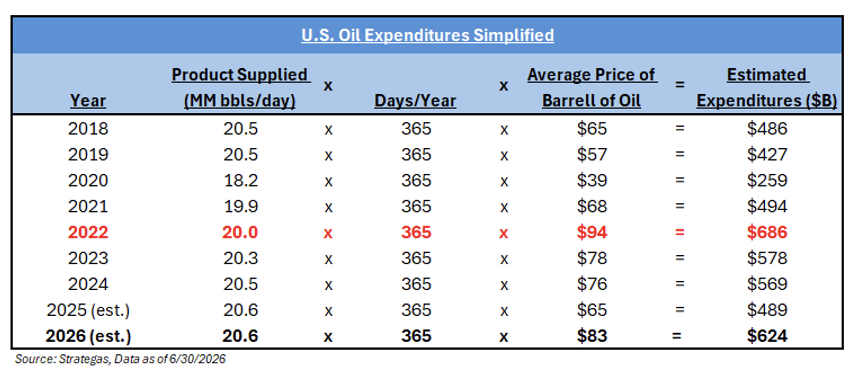

If Q1 2026 was the scene where the family patriarch, Logan Roy, locks everyone in the cabin and makes them fight for sausages, coined Boar on the Floor, Q2 was the episode where the camera pulls back, and you realize the ones who stayed calm and kept eating actually came out ahead. The market’s Boar on the Floor moment had passed. The Iran ceasefire arrived in late May. Oil retracted from its $100+ peak. The market did what the market almost always does after a geopolitical shock resolves: it recovered, quickly and aggressively, punishing everyone who sold the fear and rewarding everyone who sat on their hands.

If Q1 2026 was the scene where the family patriarch, Logan Roy, locks everyone in the cabin and makes them fight for sausages, coined Boar on the Floor, Q2 was the episode where the camera pulls back, and you realize the ones who stayed calm and kept eating actually came out ahead. The market’s Boar on the Floor moment had passed. The Iran ceasefire arrived in late May. Oil retracted from its $100+ peak. The market did what the market almost always does after a geopolitical shock resolves: it recovered, quickly and aggressively, punishing everyone who sold the fear and rewarding everyone who sat on their hands.

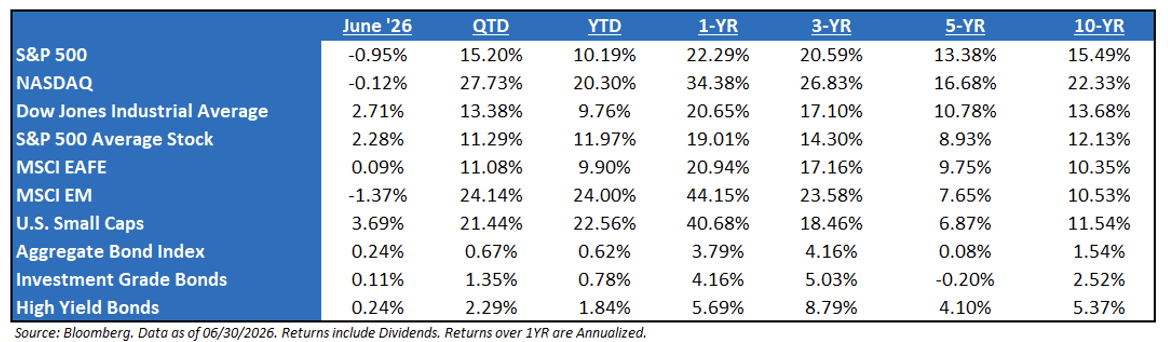

The S&P 500 gained 15.2% in Q2 2026 – it’s its 12th best quarter since 1950 – pushing the year-to-date (“YTD”) return into positive territory at roughly 10.2%. The growthier parts of the market led, with NASDAQ jumping 20.3%, powered by AI-linked earnings that continued to come in well above even the most optimistic expectations. The equal-weighted S&P 500 – a better proxy for the average stock – was also up over 12.1% YTD, a quiet confirmation that the market-broadening story that began in 2025 has continued its momentum.

The catalyst was straightforward, even if the anxiety leading up to it was not. The ceasefire agreement between the U.S. and Iran unlocked a cascade of positive repricing across equities, credit, and rate expectations. Brent crude oil – which had spiked above $113 per barrel at its March and April highs – pulled back sharply, taking with it the biggest near-term threat to inflation expectations and Fed policy.

equities, credit, and rate expectations. Brent crude oil – which had spiked above $113 per barrel at its March and April highs – pulled back sharply, taking with it the biggest near-term threat to inflation expectations and Fed policy.

Markets, as they always do, had already started pricing in the resolution before it was official.

Strip away the geopolitics, the Fed transition, the mid-term election noise that is already beginning to build, and what investors are left with is a deceptively simple picture: corporate America is making more money than anyone expected, at a pace that has now sustained for six consecutive quarters of double-digit EPS growth – a record. There has been an absolute boom in earnings:

-

- “Boom” in EPS beats: 85% of S&P 500 firms beating EPS – best hit rate in 5 years;

-

- “Boom” in Margins: 64% of sectors have seen margin expansion;

-

- “Boom” in Growth: 73% of sectors are posting double-digit EPS growth;

-

- “Boom” in Momentum: Forward EPS expectations are up by 8%;

-

- “Boom” in Revenues: Forward Revenue expectations are up by 4%; and

-

- “Booming” AI demand: Hyperscalers saw EPS and revenue beats.

With this, one of the more encouraging developments in financial markets has been the broadening of equity market participation beyond the narrow band of mega-cap technology names that dominated returns in ‘23, ‘24, and parts of ‘25. Recently, smaller stocks and international equities joined the party and began contributing more meaningfully to overall market performance. This broadening is underpinned by an equally important development on the earnings side – corporate profit growth is no longer the exclusive domain of big tech, with more sectors now reporting solid revenue and margin expansion.

market performance. This broadening is underpinned by an equally important development on the earnings side – corporate profit growth is no longer the exclusive domain of big tech, with more sectors now reporting solid revenue and margin expansion.

When earnings breadth improves, it tends to make a bull market more durable and less vulnerable to a sharp reversal triggered by disappointment in just a few stocks.

International markets have quietly benefited from the same AI theme as US stocks, just through a different lens. Non-US stocks outperformed the US by about 14% last year and kept climbing in 2026. Much of that has come through Emerging Markets’ exposure to AI infrastructure – EM stocks are up 44% over the past 12 months, with Latin America benefiting from copper demand and South Korea standing out on strong earnings momentum – plus a broader rotation into Europe on policy reform and dollar weakness. The open question is whether this is a real regime shift toward diversification or a temporary reversion that’s already lost some steam after this year’s energy shock.

Moving forward, domestically speaking, the three key tenets of this market remain intact: fiscal policy is stimulative, monetary policy is transitioning under new leadership, yet remains supportive, and private capital spending on AI continues to accelerate. As long as earnings are growing – and they are at a historically exceptional pace – the burden of proof remains with the bears. We are still in a bull market. Don’t fight it.

Equity Fireside Chat: The Toms & the Roys of the Russell 3000

Equity and bond markets look like they’re disagreeing, but they may not actually be. Stocks are grinding higher on genuine conviction in AI-driven productivity gains, and that conviction may be well-founded. Then, the US 10YR Treasury’s stickiness in the mid-4% range isn’t bonds calling that growth story into question – it’s a separate, fiscal signal, reflecting deficits, heavy issuance, and a term premium that won’t budge while the debt trajectory looks unanchored. So, bonds aren’t pricing weaker growth; they’re pricing a messier balance sheet. Read that way, equities are the market engaging with the growth question, and that’s where investor attention should be focused.

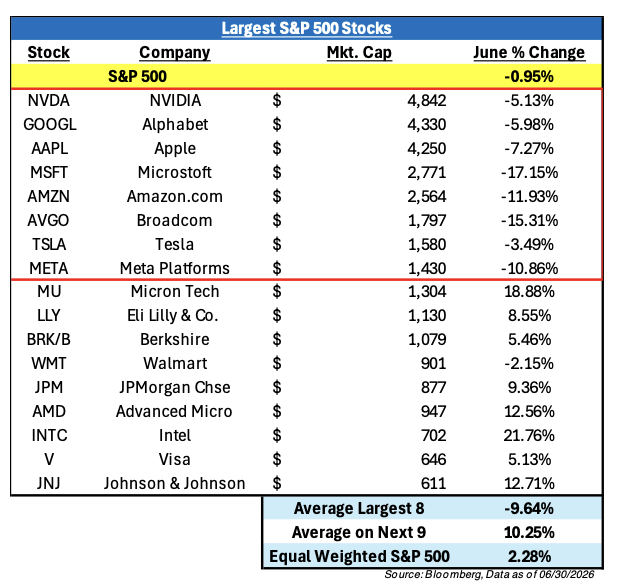

Beneath a calm-looking index, dispersion has been unusually high this year. The average rolling 3-month correlation among S&P 500 stocks has been at just 13%, which is lower than 98% of the time since 2022. This simply means that stocks are moving far less in lockstep together than usual – that there have been a few very large winners and a lot of stocks that have underperformed. While this may seem bearish, it’s not.

than 98% of the time since 2022. This simply means that stocks are moving far less in lockstep together than usual – that there have been a few very large winners and a lot of stocks that have underperformed. While this may seem bearish, it’s not.

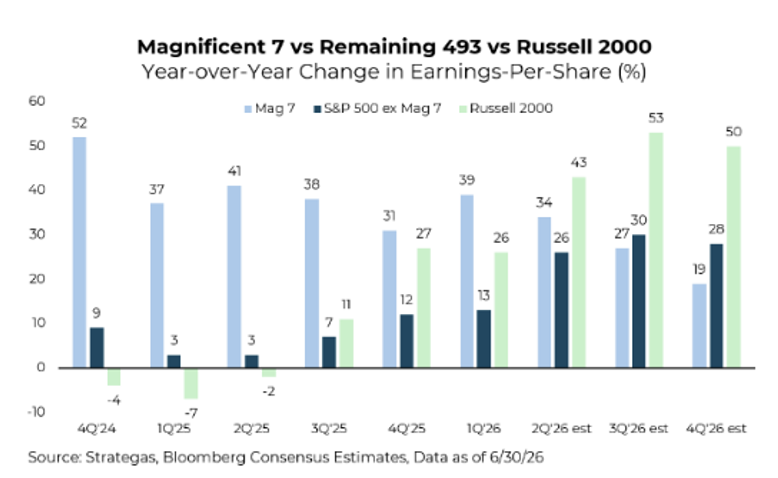

Yet, this fixation on concentration remains top of mind for investors, even if it is one of the weakest arguments that one can make on the market. While the premise sounds intuitive – if a handful of stocks are driving returns, future returns must be fragile. The data says otherwise. Since 1990, there have been 5 years in which fewer than 35% of the S&P 500 stocks outperformed the index. In those years, the S&P 500 returned an average of 22%, more than double its long-run annual average of 10%. This is how innovation has always worked. Technology revolutions aren’t distributed evenly across thousands of companies. Regardless of how the AI era ultimately unfolds, the decisive advances are being driven by a small number of firms.

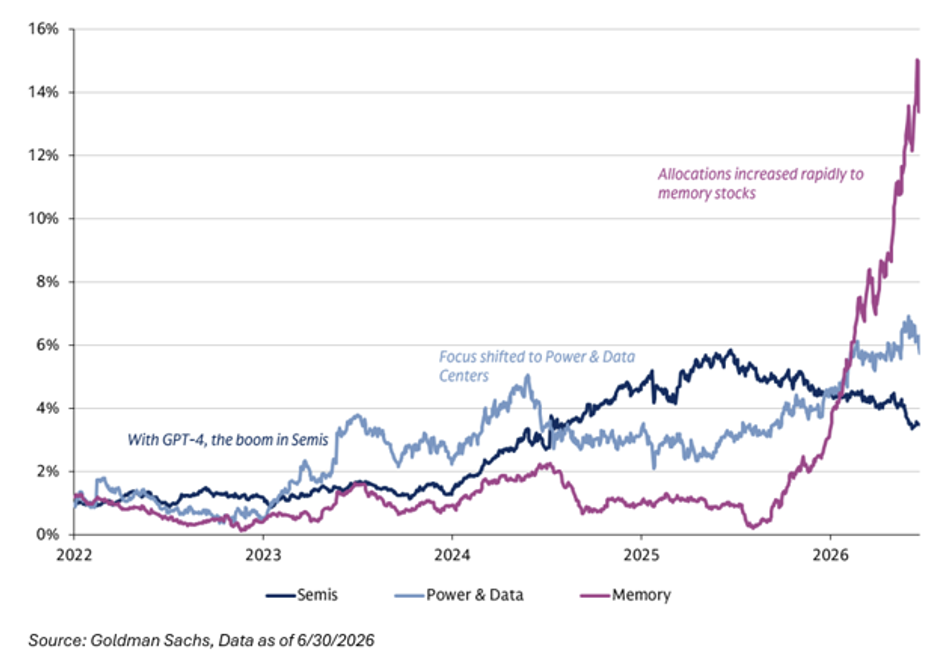

Even the AI trade is not in lockstep. The trade has rotated through distinct phases: (1) The semis boom, led by GPU and compute exposure; (2) Then a shift into power and hyperscalers; and (3) Most recently, a run in memory names.

And right now, the old Animal Farm adage is correct: All Tech stocks are created equal, but some Tech stocks are more equal.

-

- More Equal: Markets are drawing a sharp line between those cashing the checks and those writing them. To a degree, this is both fair and rational – hyperscalers are deploying close to 100% of operating cash flow back into capex, and investors are right to ask hard questions. That said, investors should argue this scrutiny is a healthy sign: it reflects a level of capital discipline that was conspicuously absent in the late 1990s. It’s just those receiving the checks from the hyperscalers that are winning.

-

- Less Equal: In 1H 2026, the market took more of a shoot first, ask questions later type of approach. In previous years, the market rewarded stocks that it considered to be “AI winners”. This year, the market tried to sniff out who it believed to be “AI losers” and punished them considerably. There’s no better place to point to than Software stocks to provide an example.

Remember that when the biggest names or those that have performed the best stumble, the rest don’t have to follow. Historically, when mega-cap stocks have sold off, the instinct is to brace for a broader market collapse – but this theory has been challenged lately. As the largest technology and AI names pulled back sharply in June, the equal-weight S&P 500 outperformed its cap-weighted counterpart.

Concentration cuts both ways: the same dynamic that makes a handful of stocks look like “the market” on the way up means their stumble doesn’t have to take everyone else down with them. Said differently, the market narrows on the way up, and broadens on the way down.

Throughout school, people teach investors that intelligence is about finding patterns. This is wrong, as in a complex world, intelligence should consist of ignoring things that are irrelevant and avoiding false patterns. This is why the equity markets are likely on the correct path of performance right now, as their focus remains on earnings and profitability.

Macro Economics Fireside Chat: You Can’t Make a Tomlette Without Breaking Some Greggs

There’s a moment in Succession where Tom Wambsgans, an executive at Waystar Royco, is testifying before Congress about the cruise scandal. He offers up the now-famous line that you can’t make a Tomlette without breaking some Greggs. It’s brutal, it’s funny, and underneath the joke is a more universal bit of organizational logic: any real shake-up means somebody’s old way of doing things gets cracked open, even if nobody sets out to target them specifically.

There’s a moment in Succession where Tom Wambsgans, an executive at Waystar Royco, is testifying before Congress about the cruise scandal. He offers up the now-famous line that you can’t make a Tomlette without breaking some Greggs. It’s brutal, it’s funny, and underneath the joke is a more universal bit of organizational logic: any real shake-up means somebody’s old way of doing things gets cracked open, even if nobody sets out to target them specifically.

Kevin Warsh, the new chair of the Federal Reserve, seems to be operating from a similar instinct – minus the boardroom backstabbing, plus a few less profane press conferences. In fact, there won’t be any profane press conferences, and unlike Cousin Greg in the same Congressional hearing, Kevin Warsh won’t be speaking in an affirmative fashion to markets anytime soon. Warsh has boiled his advice to the Fed: “Stop talking so much. More thinking, less talking.”

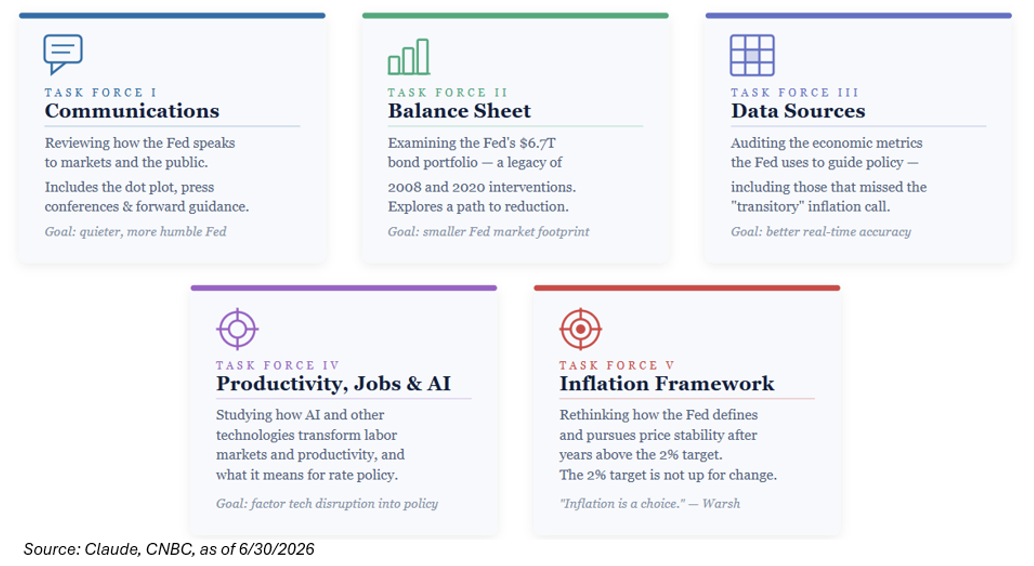

But less communication isn’t the only shakeup at the Fed moving forward – there are a few other changes:

-

- Unlike most transitions, this one came with an unusual wrinkle: Previous Fed Chairman Jerome Powell didn’t fully exit stage left. He chose to stay on the Fed’s Board of Governors, meaning the new chair inherited an active, recently departed predecessor still holding a vote in the room – something like Logan Roy staying on the company board after “stepping back,” still glowering from the corner of every meeting;

-

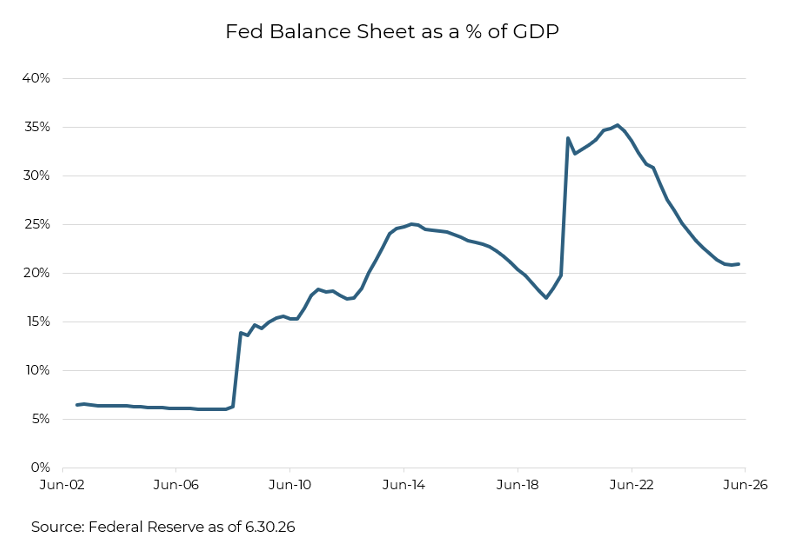

- The shrinking of the Fed’s balance sheet; and

-

- Kevin Warsh also announced the creation of five task forces – working groups designed to study how the Fed communicates, how it gathers economic data, whether AI is reshaping productivity, and a handful of other structural questions.

Here’s the good news for anyone nervous about an institution like the Fed being treated like a family business: none of Logan Roy’s kids ended up chairing those five task forces. There’s no Kendall trying to leverage a data-modernization group into a power play, no Roman undermining the communications task force with a poorly timed joke in front of reporters, no Shiv trying to use the AI-productivity panel to settle a personal score. Instead, Warsh will bring in ideas from the economics and business community, from inside and outside the Fed.

While this feels like a lot of change, investors should welcome an overall reset, as this is just one man, Kevin Warsh, who is asking tough questions, but ultimately deferring to the FOMC and the institution it represents to yield the answers. Again, Kevin Warsh is not going at this alone, and the entire Federal Open Market Committee (“FOMC”) agrees the Fed can and should do better at achieving its mandates: (1) pricing stability, and (2) full employment.

All of these “changes” ultimately reflect an anxiety among investors about free markets and a preference for the predictability that comes with heavy central oversight. But that kind of aggressive intervention, which the market has become accustomed to, is no silver bullet. Since the Bernanke era, the Fed has repeatedly over-promised and under-delivered, relying ever more heavily on market intervention to make good on its commitments – a pattern that has consistently generated costly and unforeseen side effects. Said differently, Fed independence looks to shift investor focus from Fed captivity to a refocus on economic supply-driven fundamentals.

It’s worth remembering the Fed has done this changing dance before. Volcker was the stoic, cigar-chomping, no-nonsense inflation hawk. Greenspan’s deliberately opaque, minimalist statements were themselves a style choice that later chairs deliberately reversed in favor of more transparency and detailed forward guidance. Bernanke pushed the Fed toward explicit inflation targets and far more communication during the financial crisis.

minimalist statements were themselves a style choice that later chairs deliberately reversed in favor of more transparency and detailed forward guidance. Bernanke pushed the Fed toward explicit inflation targets and far more communication during the financial crisis.

Yellen and Powell expanded forward guidance even further, walking the market through their thinking meeting by meeting. Each one of those shifts was, in its moment, treated as a structural change to how the most powerful central bank in the world does business – and each time, the institution absorbed it, adjusted, and kept properly functioning.

Ultimately, as investors come to grips with the shifts underway at the Fed, the real question is whether these changes will redefine how markets operate. The tools at the Fed’s disposal may differ somewhat, and its communication style marks a sharp departure – but the core mission of maintaining price stability to support sustained economic growth remains unchanged. And when that mission is carried out competently, it has tended to favor risk assets over time.

None of this is to say change at the Fed is risk-free, or that “breaking a few Greggs” along the way is automatically worth it. Reasonable people disagree about whether less forward guidance helps markets plan or just adds confusion, whether shrinking the balance sheet faster risks tightening financial conditions at the wrong moment, and whether a chair operating alongside his still-present predecessor can really set a new tone without friction. But the institutional structure – five task forces, a twelve-member voting committee, governors who need actual majority support to do anything – means no single person, however ambitious, gets to run the place like a family fiefdom.

You can’t make a Kevin Warsh scramble without cracking some Powells.

Conclusions: Succession Brings Change; And That’s OK

At the center of this entire newsletter is the recognition that things change over time – Technology, the Fed, etc. And that’s OK.

The worst personality trait of an investment professional is to resist this change. Markets are constantly evolving, and the investors who fail to adapt are the ones who get left behind. Stubbornly clinging to outdated frameworks, familiar names, or comfortable narratives is not a sign of discipline – it is a blind spot. The greatest opportunities in markets have almost always emerged from change, and the greatest losses have often come from those who refused to see it coming. An open mind is not optional in this profession; it is the job.

And this wisdom is even more apparent today, as it feels like everything in this market is changing – quickly.

Likely the first thing to come to mind is the revolutionary technology that has the phrase “bubble” attached to it. In potential bubble scenarios, the most enthusiastic bulls dismiss skeptics as unimaginative or blind to the promise of new technology. Meanwhile, bears get caught up searching for the perfect historical parallel or waiting for a clear catalyst – which, when it finally arrives, often looks surprisingly ordinary, like a quiet reduction in capex guidance. The hard truth is that calling the top of a bubble is nearly impossible. Markets can defy logic and continue climbing for far longer than anyone expects before reality sets in.

This is why it’s important to avoid these mistakes:

-

- “AI is clearly a bubble” – No one can possibly know that. It’s a waste of time mulling it over too much.

- “AI is going to be a wonderful business”. You can’t possibly know that. It’s a waste of time mulling it over too much.

The most sensible approach is a balanced one. And that’s why we believe the Aptus Asset allocation is prepared for any outcome regarding artificial intelligence. It overweights stocks to reap the profitability and growth benefits, but always aims to keep the guardrails intact through hedging, in case there is an air pocket. Investors should always focus on what they can control; Prepare for what they cannot.

And as the market continues to evolve, there are always some core principles that should be the foundation of one’s mental game:

1. At the end of the day, the pursuit of perfection is an ultimate, pressurized failure mindset – it’s one that will eat every investor alive if they continue to chase it. Everybody wants to be the hero because they care and they want to win really badly. But success(ion) doesn’t live in that realm.

2. Neither does comparison. Comparison is the thief of joy. If one continues to compare themselves, they’ll remain joyless.

It’s fitting: Succession’s real lesson isn’t about succession at all; it’s about adaptation.

The heirs apparent spent four seasons fighting to inherit a company exactly as it was built, chasing approval for a playbook that no longer applied, desperate to be the hero in a story that had already ended, and one by one, they lost. The person who ultimately won wasn’t the smartest or most ambitious in the room; they simply paid attention to where things were going instead of where they’d been. Markets don’t reward loyalty to the old regime any more than the company in the show did. The investors who survive aren’t the ones clinging hardest to yesterday’s framework or chasing the perfect call; they’re the ones flexible enough to recognize the moment they’re actually in.

Succession brings change. And that’s okay – so long as you’re not still waiting for Logan to tell you what to do.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

The content and/or when a page is marked “Advisor Use Only” or “For Institutional Use”, the content is only intended for financial advisors, consultants, or existing and prospective institutional investors of Aptus. These materials have not been written or approved for a retail audience or use in mind and should not be distributed to retail investors. Any distribution to retail investors by a registered investment adviser may violate the new Marketing Rule under the Investment Advisers Act. If you choose to utilize or cite material, we recommend the citation be presented in context, with similar footnotes in the material and appropriate sourcing to Aptus and/or any other author or source references. This is notwithstanding any considerations or customizations with regards to your operations, based on your own compliance process, and compliance review with the marketing rule effective November 4, 2022.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2607-2.