If someone looked up the Webster Dictionary definition of the Dave Chappelle Show, it would go something like this: It was rare sketch comedy that managed to be both outrageously inappropriate and socially brilliant at the same time. It felt like a college philosophy class taught by your single, unfiltered uncle at the Thanksgiving dinner table, but instead of books, there were skits about crackheads, race wars, and celebrity impressions that were way too accurate. The show’s genius was in making uncomfortable truths so hilarious you forgot you were supposed to be outraged.

While there are not many TV comedies as legendary, the show is likely difficult to discuss in polite company, let alone in an investment newsletter; but sometimes there’s a necessity to be a habitual line stepper like Rick James. Be like Rick, because when investing in the market and while everyone is adopting the same strategy, it ceases to work.

In just three short years, the show delivered a host of memorable – though often NSFW – quotes. Strangely enough, one of them feels like the perfect analogy for recent monetary policy and the market’s manic recovery over the past six months. As Rick James puts it in the classic “Charlie Murphy’s True Hollywood Stories” sketch, ‘{Insert Title of an Eric Clapton Song} is a hell of a drug.’ Likewise, when the FOMC re-kicked off its easing cycle with a ‘risk-management’ cut in September, it became clear that central bank policy can act as a boost for markets much like the infamous stimulant did for the Superfreak. All it took was Jerome Powell signaling that rates would be heading lower in the future.

Equities were not the only beneficiaries of this policy, as, contrary to the advice of Wu-Tang Financial, you did not need to diversify your bonds, as fixed income posted its third straight quarterly positive return. Even non-U.S. equities, which have been the subject of as much hate as Ice-T at the Playa Haters’ Ball, posted strong returns.

The S&P 500, a benchmark for risk assets, has rallied 35.1% off of the low print in April, as investors have purified themselves in the waters of Lake Minnetonka of tariff uncertainty, driving equities and sentiment back to nearly all-time highs.

If one were asked to explain this reversal in just one line, an investor would argue that it was driven by a durable economy, exceedingly easy financial conditions, and a boom in applied innovation. Or maybe the equation is even less complicated than that – for all that’s going on in the world, it could simply be due to governments, corporations, and households having remained on the gas pedal. All an investor has to do is look at the magnitude of U.S. fiscal spend, the capital expenditure intentions of the Magnificent Seven, or the U.S. household demand for risk assets.

Just because we’ve seen the 4th-best 5-month rally in equities ever, doesn’t mean that investors should stop partying like it’s 1999. The gas tank still has a lot of petroleum left, as there are three separate forms of economic stimuli hitting the economy and markets:

1. The Fed cut rates, but more importantly, signaled that a rate-cutting cycle has started. That matters because it means monetary stimulus is now occurring, which is positive for the economy and, peripherally, risk assets;

2. Fiscal stimulus is occurring via the passage of the One Big Beautiful Bill, which solidified and boosted tax cuts, as well as unleashed billions in Federal dollars across various industries; and

3. Private stimulus, meanwhile, is occurring through massive AI-linked capital expenditures from major tech companies such as META, MSFT, AMZN, ORCL and others.

As we all know, the market does not go up in a straight line, as pullbacks are healthy and should be welcomed. But a shift in policy easing has taken place and should provide some ‘insurance’ against the possibility that a sub-par US economy evolves into something worse, as it’s no secret that the labor market could be weakening. The more time passes; with the economy holding up despite a slower labor market, the more likely it is that the market will look further out into the future. Where most of the growth headwinds will likely be replaced by tailwinds from fiscal support and lower rates, which could create a continued path for upside in risk assets.

So, position yourself accordingly, and don’t be afraid to shoot the “j”.

Market Recap: Q3 2025

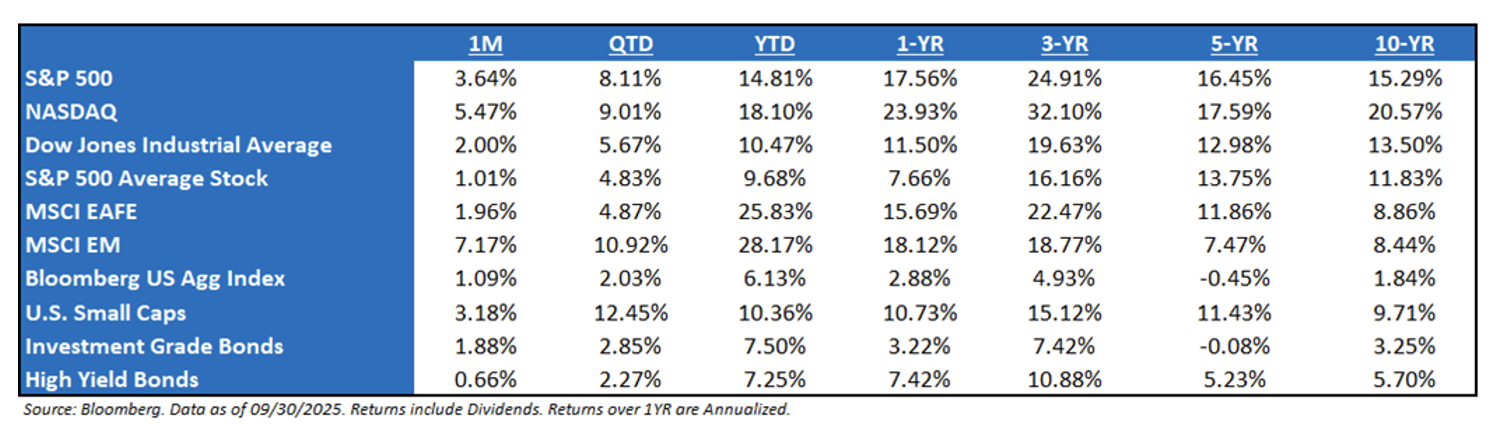

Stocks have bounced back from the tariff-tantrum pullback like a Prince crossover; quickly, reaching new highs on 28 different occasions this year – the S&P 500 returned 8.11% during the quarter. Even through all the noise during the quarter and year, the stock market game has produced three different winners: Q1 Winner: European Markets, Q2 Winner: U.S. Markets, and Q3 Winner: Asian Markets.

Even with the recent Federal Reserve rate cut trumping the liquidity drain during the quarter, the benefits didn’t fully materialize into a full broadening out in the market like many hoped for. In fact, the quarter witnessed some of the highest dispersion amongst stocks in recent memory – only ~38% of the members in the S&P 500 outperformed the overall index in Q3.The biggest driver of performance continued to be the thematic plays, as it was the artificial intelligence (“AI”) areas of the market that called, “Game, Blouses”.

But it was a weird quarter for overall performance, as there were two different narratives in play. Usually, when Small Caps outperform Large Caps, the “S&P 500 Average Stock” performs well. That was not the case during the quarter. Performance can be transcribed into two things: (1) continued leadership from the mega-caps, as capex spending continues to lead drive revisions and revenue, and (2) expectations of lower interest rates drove the smallest of the small.

Small Cap stocks finally joined the equity party, as the asset class hit new all-time highs for the first time since 2021 – a total of 966 days, which is the second-longest streak ever. For some time, within small caps, investors have been focused on elevated interest expense and persistent profitability challenges. However, as companies have adapted to the higher rate environment, it’s notable that the growth outlook for small caps in 2026 has shifted meaningfully. While part of this improvement can be attributed to easier year-over-year comparisons, it’s also the first time we have seen a sustained and meaningful growth trajectory for small caps surpassing their large-cap peers. Hence, the bid to the asset class.

caps, investors have been focused on elevated interest expense and persistent profitability challenges. However, as companies have adapted to the higher rate environment, it’s notable that the growth outlook for small caps in 2026 has shifted meaningfully. While part of this improvement can be attributed to easier year-over-year comparisons, it’s also the first time we have seen a sustained and meaningful growth trajectory for small caps surpassing their large-cap peers. Hence, the bid to the asset class.

As long as earnings are growing, which they are, and as long as both monetary and fiscal policy are on the market’s side, the burden of proof will remain with the bears. Where all this leads is that we are still in a bull market – don’t fight it – but that doesn’t mean chase it. It appears that the market is entering a period where it can see a moderation of the hard economic data, but not enough to warrant a recession. If markets price in deeper rate cuts off the back of this, then this will only serve to ease financial conditions further. Meanwhile, the forward-looking sentiment data should continue to improve with economic tail risks diminishing and expansionary fiscal policy on the horizon. This, combined with continued AI-driven investment and innovation should continue to support risk assets once we move beyond the current geopolitical tensions.

Stay nimble; don’t be too bearish, don’t be too bullish.

Equity Fireside Chat: Is it a Boom or Bubble for the AI-Centric Stocks?

The best line to describe the new age of Mega-Cap stocks is simple and clear: company size used to be the enemy of growth; now, it’s the engine.

But the magnitude of performance has scared some investors, alongside major investment news outlets stating that the AI-centric names are in a bubble that is ready to burst. We’re not buying that narrative right now. Yes, performance has been great for this narrative. Following a 32% rally in 2024, AI-exposed equities have rallied by an additional 19.2% YTD. AI-Driven stocks have driven:

-

- 75% of the S&P 500 returns since ChatGPT’s launch in November 2022;

-

- 80% of the earnings growth during the same period; and

-

- 90% of capital spending growth.

One can argue the companies at the top of the index today are significantly more profitable – and far less overvalued – than they were back then. The valuation point bodes this question: the NASDAQ has rallied in 16 of the past 17 years – how much of that has been the multiple? Answer: Since the start of 2009, the total return of NDX is +2,306%. The breakdown: (1) 74% is thanks to earnings growth; (2) 16% is dividends; and (3) just 10% is valuation expansion. That sounds like merit-based performance.

Among the largest stocks, valuations are also still below the levels reached during the 2000 and 2021 peaks. The five largest stocks in the index (NVDA, MSFT, AAPL, GOOGL, AMZN) trade at P/E multiple of 30x, compared with 40x at the peak in 2021 and 50x at the peak in 2000.

The reason for the heightened optimism is that hundreds of billions of dollars in AI capex investment have continued to support AI infrastructure stocks. In particular, the public US AI hyperscalers (AMZN, GOOGL, META, MSFT, ORCL) have made $346B in capex investments during the past four quarters. Capex growth among these stocks also accelerated sequentially in Q2 (from 69% year-over-year in Q1 to 78% in Q2). The earnings and returns of firms involved in the build-out of this infrastructure – i.e., semiconductors, electrical equipment companies, technology hardware firms, power suppliers – have benefited from these sizable capex investments.

While the inevitable slowdown in capex growth poses a risk to the valuation of AI infrastructure stocks, as of right now, it doesn’t seem like this will occur in the near future. Overall Capex has a lot of tailwinds:

1) Full instant depreciation, 2) Falling interest rates, 3) Tariff incentives, 4) Deregulation, 5) and an AI gold rush.

Given the continued fodder around the AI bubble, this will be a debate that will continue well into the future. But for now, it’s their friends versus the revolution. And we’re choosing the revolution.

Fixed Income Fireside Chat: The Most Hated at the Playa Haters’ Ball

Jerome Powell isn’t just a shoo-in for the most hated at the Playa Haters’ Ball this year; he’s likely been the winner since he became Fed Chairman in 2018.

Given this, investors shouldn’t be surprised that President Trump called him Jerome “too late” Powell. It’s a layup because it neatly describes a central part of the

Fed’s way of acting. As Chris Waller described in a speech last year, the FOMC intentionally waits longer to act than markets would like – by focusing on quarterly rather than monthly data, for instance – to avoid acting prematurely. As a result, the Fed is always late to move, but usually not too late to avert disaster.

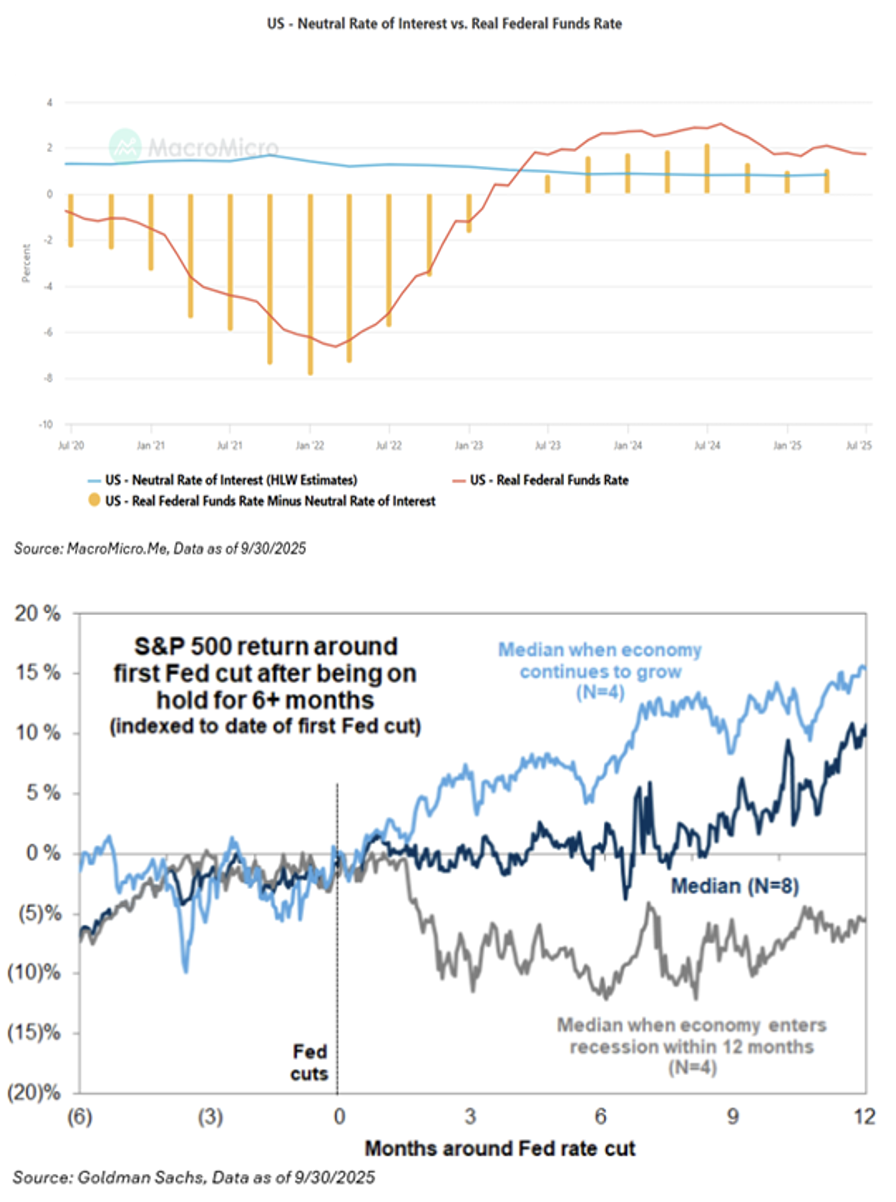

At the end of the day, the biggest question for the Fed is Where is the Neutral Rate? It’s no secret that the balance of risk is moving towards equality, which suggests that the Fed should be moving rates towards equilibrium.

In simple English, policy should be closer to neutral, which the majority of FOMC voters believe means a fed funds range of 3.0%-3.25% – when risks to the two sides of the Fed mandate are in balance. Right now, the Fed still believes inflation risks outweigh employment risks. Since the last meeting, however, employment risks have increased, and inflation risks have decreased. But the Fed believes inflation risks will remain dominant through 2027, while the market is comfortable that risks will return to balance next year.

Taking this in context of stocks, the market typically rises when the Fed resumes cutting alongside a growing economy. With the economy seamlessly moving through the tariff impacts, the market is pricing in a re-acceleration of growth in 2026, and continued Fed cuts will support further gains for US equities.

As of quarter end, the market expects two more 25 bp cuts to the policy rate this year, continuing in October, followed by additional cuts in 2026. Furthermore, while real GDP growth will remain below-trend for the remainder of this year, though higher-than-expected, many believe the US economy will avoid a recession. And that’s the important question for the market – will we enter a growth slowdown or a recession? During the last 40 years, the S&P 500 has typically generated positive returns following the resumption of Fed cutting cycles during which the economy continued to grow.

Conclusion

This year has been a great case study for investors, reminding them that they need to leave emotions out of their investment portfolio. Back in April, the market was showing signs of bearish sentiment rivaling that of the COVID and Great Financial Crisis lows, of which the market weakness never came to fruition. It’s one’s time in the market, not timing the market. We continue to have a few differentiated convictions in the current market:

1. The Necessity to Own Risk Assets – Participate and Protect – as the Government’s fiscal agenda will unlikely slow down, leading to increased money supply (i.e., printing money) and currency debasement. We believe that bonds are certificates of confiscation, and one’s ability to own less fixed income and more risk assets, while keeping risk in check is the key.

2. Tails Will Occur More Often – Both good tails (right) and bad tails (left) will be more commonplace in the market moving forward. Even though the frequency is less, understanding that the tails contribute more to one’s success on compounding capital over long periods of time.

We believe that if you attack the aforementioned problems, investors will be opening their investment statements with the same smile as Calvin looking at his first WacArnold’s paycheck.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

The content and/or when a page is marked “Advisor Use Only” or “For Institutional Use”, the content is only intended for financial advisors, consultants, or existing and prospective institutional investors of Aptus. These materials have not been written or approved for a retail audience or use in mind and should not be distributed to retail investors. Any distribution to retail investors by a registered investment adviser may violate the new Marketing Rule under the Investment Advisers Act. If you choose to utilize or cite material, we recommend the citation be presented in context, with similar footnotes in the material and appropriate sourcing to Aptus and/or any other author or source references. This is notwithstanding any considerations or customizations with regards to your operations, based on your own compliance process, and compliance review with the marketing rule effective November 4, 2022.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2510-2.