Mitch Hedberg was an American stand-up comedian whose jokes felt like a stream of brilliant shower thoughts told through a haze of chill confusion. Known for his one-liners, offbeat delivery, and a stage presence that looked halfway between a rock star and a nap, Hedberg became a cult favorite. He turned everyday nonsense —like every book is a children’s book if the kid can read it — into an art form, leaving behind albums and fans who still quote him whenever something mildly inconvenient happens.

Mitch Hedberg was an American stand-up comedian whose jokes felt like a stream of brilliant shower thoughts told through a haze of chill confusion. Known for his one-liners, offbeat delivery, and a stage presence that looked halfway between a rock star and a nap, Hedberg became a cult favorite. He turned everyday nonsense —like every book is a children’s book if the kid can read it — into an art form, leaving behind albums and fans who still quote him whenever something mildly inconvenient happens.

And over the past year, the market started off very inconveniently, as many one-liners of headline information drove the market – i.e., Trump’s ‘Liberation Day’ shock tariffs ignite global trade war fears → China retaliates with counter-tariffs → Trump pauses tariff escalation after ‘queasy’ market reaction. While these headlines were likely less funny than Hedberg’s quick-witted jokes, they likely had lasting effects on investor sentiment on how to perceive the market over the short-term.

In one joke, Mitch states that Bigfoot is blurry; that’s the problem. It’s not the photographer’s fault. Bigfoot is blurry, and that’s extra scary; there’s a large, out-of-focus monster roaming the countryside. While the market may feel scary, it’s always going to be blurry in the moment. The market is a forward-looking mechanism, so it’s important to remember that if an investor is thinking about something problematic, it’s likely to already be known and priced into the market. And the recent market bottom on April 8th is another prime example of this. It pays more to be patient than clever.

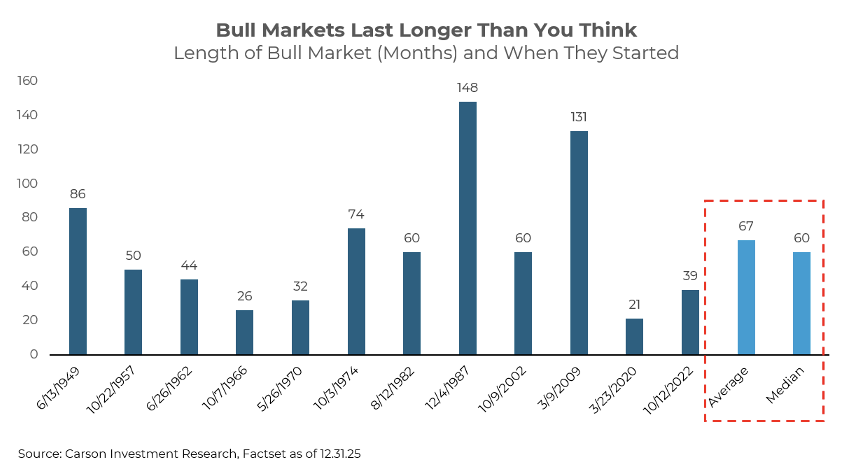

It’s likely too early to cleverly call a market top, stating that the bull market is over. In fact, looking at the 11 bull markets since World War II, the average one lasted more than five years. Not only that, the current bull market is up a very impressive 90% in just three years,which sounds like a lot, but in the context of historical rallies (the avg. bull market is +191%), perspective may state that the bull market is younger than many would think. Be patient.

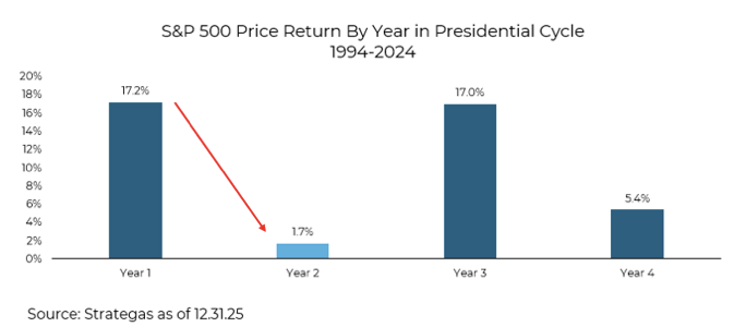

In 2026, a new variable may briefly enter the market landscape – mid-term elections. Investors need to remember, over longer periods, that the market isn’t political. Any short-term political movement or agenda that is viewed by the market as getting in the way of better earnings or growth will be viewed as negative and be a headwind on risk assets, and vice versa. Mid-term election years tend to be the most volatile year for stocks in the four-year presidential cycle. The average intra-year decline for the S&P 500 is 19%, compared to just 12% in the other three years (average of all four years is 16%). We would note that the S&P 500 has been positive in the following 12 months after the mid-term election during every instance since 1938.

While there may be a bit more volatility moving forward into a mid-term election year, investors need to remember all the liquidity being pumped into the economy. Over long periods of time, the stock market is like an escalator – it can never break; it can only temporarily become stairs. Sorry for the convenience. While the market has acted as an escalator over the past three years, annualizing at a rate of return of 22.94%, it may act more like stairs for the time being, i.e., it may take a little bit longer, and a little more effort for the market returns to climb higher.

While there may be a bit more volatility moving forward into a mid-term election year, investors need to remember all the liquidity being pumped into the economy. Over long periods of time, the stock market is like an escalator – it can never break; it can only temporarily become stairs. Sorry for the convenience. While the market has acted as an escalator over the past three years, annualizing at a rate of return of 22.94%, it may act more like stairs for the time being, i.e., it may take a little bit longer, and a little more effort for the market returns to climb higher.

In the near term, investors may not know who the real hero of the market is going to be – Fiscal policy, Monetary policy, or private spend? It’s like a belt. Belts hold up a pair of pants, but pants have belt loops that hold up the belt – who is the real hero? But the market will likely have a lot of heroes in the near-term. For example, the growth trajectory on fiscal, Fed dovishness, combined with AI and broader capex, should continue to drive returns. Historically, the index does not de-rate when rate cuts occur against a non-recessionary backdrop; however, the scope for re-rating will hinge on the magnitude and pace of Fed adjustments and fiscal spend. For now, we believe the base case is that earnings growth will continue to dictate the direction of the market, a dynamic that should remain robust.

When it comes to betting on risk assets, you need economic growth, and there’s no better place to find growth than the U.S. – it’s a reason to remain optimistic. Remember, at the end of the day, the government used to use an exorbitant amount of fiscal policy; they still do, but they used to too. Fiscal exuberance is something that has always been present in the economy, and it’s likely something that will not slow down and will come at larger scales in the future, as it’s difficult to put toothpaste back in its tube once released.

This type of economic engineering mandates that investors need to follow what the tape is telling them. The old adage, Don’t Fight the Fed, should be expanded to also include Washington, D.C. policy. Focus on what you can control, prepare for what you cannot.

Market Recap – Q4 2025

The stock market right now feels like it’s performing stand‑up: the audience is laughing, nobody fully gets the joke, and somehow everyone still walks out richer. During the quarter and 2025 as a whole, the S&P 500 kept hitting new highs, making “all‑time” sound more like a recurring appointment than an event.

For most investors, 2025 reinforced a few lessons: staying diversified across regions, sizes, and styles mattered more than precise rate calls; maintaining exposure to structural themes like AI and productivity paid off, albeit with periodic air pockets; and trying to trade each macro headline risked missing the powerful rebounds that turned a volatile year into a broadly positive one for balanced portfolios.

Not only that, but against common belief, the market did start to broaden out in 2025. Yes, the AI-centric narrative continued to dominate conversations and work well from a performance standpoint, but look at all the other parts of the global market that also did well – Developed Markets jumped +32 while Emerging Markets also posted a +34% return. This is something that caught a lot of investors offside during the year, but it should be noted that a large part of the contribution of these returns came from currency translation (i.e., weak U.S. dollar) and valuation expansion. If an investor believes that international trade will continue to work, it is likely that earnings growth will need to be present in the future.

U.S. and global equities posted solid full-year gains in 2025, but the ride was much choppier than the headline returns suggest, with multiple 5–10% pullbacks clustered around policy and geopolitical shocks. Large-cap U.S. growth and tech again set the tone, as AI, cloud, and semiconductor names drove a disproportionate share of index performance, while more defensive and rate-sensitive sectors like utilities and parts of real estate lagged despite easing yields. Don’t fight this market. This doesn’t mean that the market won’t have a pullback, as they are necessary and healthy, but research shows that the best time to own the market is when it is hitting new all-time highs.

The bond market in 2025 delivered its strongest year since 2020, as falling yields and a Federal Reserve that cut policy rates by 0.75% sparked a broad rally across fixed income. Core U.S. bond benchmark, the Bloomberg U.S. Aggregate Bond Index, posted a return of roughly 7.3%, aided by both price gains and attractive starting yields. Riskier segments outperformed: U.S. high-yield bonds returned more than 8%, and leveraged loans also produced solid mid‑single‑digit to high‑single‑digit gains, supported by resilient economic growth and low default rates. The year also marked a normalization of the yield curve as term premia re-emerged, with long-term yields settling in a roughly 4–5% range.

As mentioned earlier, the key tenets of this market remain – fiscal, monetary, and private spend. All of which should boost economic growth. As long as earnings are growing, which they are, and as long as both monetary and fiscal policy are on the market’s side, the burden of proof will remain with the bears. We are still in a bull market – don’t fight it – but that doesn’t mean chase it. It appears that the market is entering a period where it can see a moderation of hard economic data, but not enough to warrant a recession. If markets price in deeper rate cuts off the back of this, then this will only serve to ease financial conditions further. Meanwhile, the forward-looking sentiment data should continue to improve with economic tail risks diminishing and expansionary fiscal policy on the horizon. In our view, this, combined with continued AI-driven investment and innovation, should continue to support risk assets once we move beyond the current geopolitical tensions. We may be headed into a Goldilocks period with both bond and equity markets performing well.

Equity Fireside Chat: Is it a Boom or Bubble for the AI-Centric Stocks?

“I had a stick of Carefree gum, but it didn’t work. I felt pretty good while I was blowing that bubble, but as soon as the gum lost its flavor, I was back to pondering my mortality”.

In the past quarter, it has felt like the Artificial Intelligence (“AI”) trade has forgotten its carefree exuberance, as the narrative has started to lose its flavor. In our opinion, one of the biggest near-term risks to the market is some type of slowdown in the AI narrative. While this seems to be a consensus opinion, we believe that market pundits have difficulty seeing the forest through the trees on this topic because fear sells, and the benefits of this technology need to be viewed through a longer-term perspective.

Fear of asset bubbles has been ingrained in investor behavior since the Dutch Tulip-Mania of the 1630s. Then, more recently, as the market had to digest the commentary from Michael Burry, who correctly called the mortgage-backed security crisis in 2007, about AI-exuberance. Not all booms lead to busts. In fact, we don’t think that all booms are created equally. The worst kind of bubble is one that is unproductive and financed by banking institutions, e.g., tulips, gold, and housing. The best kind of bubble, relatively speaking, is one that doesn’t hurt growth too badly, but adds an element of future productivity. The best example of the latter is the dot.com bubble of the late 1990s.

While lots of money was both made and lost during the tech bubble, investors at the time could have had no idea of the long-term benefits that the internet would bring to the global economy. For example, the bubble occurred four years before Facebook was created, seven years before the first iPhone, and nine years before Uber. While there was some short-term capital pain for those who didn’t remain patient, the entire world population continues to benefit from the addition of the internet to their day-to-day lives.

We believe that advanced computing will be no different, though it is nearly impossible to fully understand the long-term benefits and how the market evolves to this technology through the lens of today. Much like the internet, no investor or economist could understand how the labor market would evolve after the internet frenzy. For example, the gig-economy was born and facilitated by digital platforms (like Uber, DoorDash, YouTube Influencers, etc.). Though we may not like it, these “new” occupations have added to the wealth of the consumer.

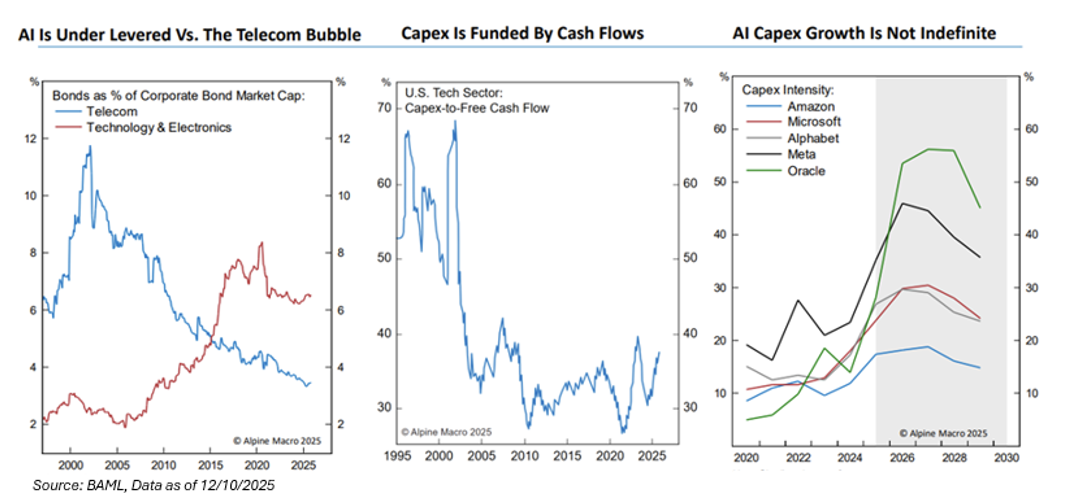

Unlike past episodes of speculative excess, today’s AI cycle is being largely financed by profitable, cash-rich firms and underpinned by robust demand. The Tech sector’s free-cash-flow margin, near 20%, is more than double its late 1990s levels, underscoring both robust profitability and capacity to self-fund AI investment. Price appreciation to this point has been primarily driven by sustained, superior earnings growth, and the dominant companies of today have particularly strong balance sheets in which the AI investments are financed by free-cash-flow. Not to mention their valuations are much lower than what we’ve witnessed in the past.

Still, markets are struggling to price a technology that is advancing at an exponential rate. While markets appear undeterred, even with solid fundamentals, they can have a correction. We believe there is a difference between a bubble and an air pocket. While we don’t believe that we are currently in the former, the latter is a possibility. The boom in tech stocks and AI spending could lose its luster, even if temporarily. While few doubt the potential transformative impact of AI, a shift in momentum could be triggered by a range of factors (i.e., a miss on mega cap earnings, a supply crunch on power or critical materials, or an external liquidity shock). Given the significance of AI investment, such a slowdown could cause a swift pullback in the overall market, or at a minimum, pressure the AI-linked wealth gains that have lifted consumption.

Understanding the overall AI risk doesn’t mean that an investor should be underweight in the market or afraid to invest. Simply said, we believe the best way to approach AI is not to try to pick the winners and avoid the losers, but to address it at the asset allocation level by owning more stocks.

We believe that it is a very rational and conventional framework to not fade this new technology but embrace it with the safety of utilizing hedges on the exact thing that investors want to protect against – a pullback in the S&P 500 – which has a concentrated exposure to advanced computing. If one can do this, without chasing the more speculative areas within this AI theme, we think it’s one of the most efficient ways to play the productivity narrative that could continue to push the market into witnessing right tail environments.

Macroeconomics Fireside Chat: What About the Dufrenes?

“When you go to a restaurant on the weekends and it’s busy so they start a waiting list, they say, “Dufrene, party of two, table ready for Dufrene, party of two.”

And if no one answers they’ll say the name again: “Dufrene, party of two.”

But then if no one answers, they’ll move on to the next name. “Bush, party of three.”

Yeah, but what happened to the Dufrenes? No one seems to care. Who can eat at a time like this? People are missing. You people are selfish. The Dufrenes are in someone’s trunk right now, with duct tape over their mouths. And they’re hungry.

They should say, “Bush, search party of 3; you can eat when you find the Dufrenes.”

But the U.S. consumer isn’t missing. Actually, consumer spending is the opposite of missing right now. If the Dufrenes really were lost, one would likely find them at a restaurant that is one step above where the Bush family is currently eating. The U.S. consumer remains very healthy, and it’s likely that they’ll be even healthier after the bazooka of liquidity entering the market in the first half of 2026, given consumer-based tax cuts. As seen below, the consumer has a household net wealth almost double what it was 10 years ago.

The preferred measure of economic growth is through Gross Domestic Product (“GDP”), which is the total market value of the goods and services produced within the United States in a year. The largest component of GDP tends to be contributed by consumer spending, totaling ~70% of the calculation. Said another way, as the U.S. consumer goes, so goes the U.S. economy – or vice versa.

There is a wide range of ramifications dependent on spending habits. Specifically, slowing GDP can create structural problems in the economy, as it is marked by lower real income, higher unemployment, lower levels of industrial production, and a decline in retail sales. All of which will influence the S&P 500’s earnings per share, which tends to be one of the most reliable factors when determining the market’s price direction.

This is exactly why we believe the market will be fixated on the consumer moving forward, even after the dust settles from tariff ramifications. If spending remains resilient, then earnings growth will likely drive the market and support a higher valuation multiple. But if the consumer shrugs due to 1) the potential for a slowdown, 2) a weakening labor environment, and 3) the ramifications of almost five years of compounded inflation lowering their purchasing power, it could derail the economy.

But GDP growth has been stellar for quite some time.

Much like the S&P 500 performance can be supported by the “average stock” if the Magnificent Seven falters, GDP can be supported by the remaining 1/3rd: investment spending. Infrastructure spending and productivity could make a serious recession unlikely, as the government continues its focus on fiscal spending, from helping consumers to helping companies spur investments.

But, as always, it comes down to the consumer’s propensity to spend. And in this period of time where inflation is continually above the Fed’s 2% target (the average inflation rate in the United States has been 3.6% since 1950), investors have started to recognize thatinflation needs to be viewed from a cumulative standpoint over a client’s investment horizon, instead of through the lens of an annualized economic figure.

Dufrene, party of two. Dufrene, party of two. Like the Dufrene, concerns related to inflation and lost purchasing power have gone missing. So, a big question heading into 2026 is whether persistently high inflation will finally slow spending, not just on the lower end of the income cohort, but also the upper end.

Conclusions

Market participants who skew bearish tend to sound the smartest, but it’s the bulls that are the ones who tend to make money over longer periods of time. Recently, there has been a lot of focus on economic data (and lack thereof, given the government shutdown), specifically single data points, and depending on one’s thesis, any narrative can be written to prove or disprove a bullish thought, and vice versa. That’s why it’s important to remember that only during periods of a recession and a recovery does economic data tend to portray the same message. Remember, if there isn’t a recession during the year, the S&P 500 is higher 85% of the time.

This means that investors need to continue to remain balanced – don’t get too bearish or too bullish. Don’t get too growthy or too deep value. Don’t get too defensive or too cyclical. Increase the horsepower of your allocation’s engine by owning more stocks, while remaining risk neutral through ownership of volatility. We are firm believers that a proper allocation structure and maintaining a process that executes on that structure will outperform over longer periods of time, specifically during periods of slowing growth and economic uncertainty.

Long-term wealth isn’t created overnight. If it were, it would be like going fishing and hoping to catch a fish stick – that would be too convenient. As always, it’s time in the market, not timing the market. Over the last 100 years, if an investor missed out on the 50 best days, their return would be cut almost in half if they were invested full-time. But the best days occur when pessimism is at its peak – 38 of the 50 best days over the past 100 years occurred during 2022, COVID, The Great Financial Crisis, The Dot.com Bubble, and … The Great Depression.

At the market’s top, everyone’s time horizon extends to infinity. At the bottom, it collapses into ‘today.’ Expand your time horizon for better results, as trying to always correctly time the market is like playing tennis against a wall. No matter how good you get, you’ll never be as good as a wall.

The moral of the story is to always remain invested.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

The content and/or when a page is marked “Advisor Use Only” or “For Institutional Use”, the content is only intended for financial advisors, consultants, or existing and prospective institutional investors of Aptus. These materials have not been written or approved for a retail audience or use in mind and should not be distributed to retail investors. Any distribution to retail investors by a registered investment adviser may violate the new Marketing Rule under the Investment Advisers Act. If you choose to utilize or cite material, we recommend the citation be presented in context, with similar footnotes in the material and appropriate sourcing to Aptus and/or any other author or source references. This is notwithstanding any considerations or customizations with regards to your operations, based on your own compliance process, and compliance review with the marketing rule effective November 4, 2022.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2512-31.