Aptus Compounder Update

The Aptus Compounder Stock Sleeve is designed to provide equity exposure to a carefully selected group of individual stocks that offer, what we consider to be, attractive prospects through a combination of yield, growth, quality, and reasonable valuations relative to large-cap peers.

Strategic Context

From a construction perspective, this trade shores up some of the strategy’s underweight to both the Technology sector and the Semiconductor industry. Recently, the team has recognized that the strategy’s ethos may be off due to the following reasons:

1. Even with many of the holdings within the Compounders portfolio having some sort of AI-exposure (i.e., PWR, APH, NVDA, etc.), the strategy continued to feel like it is underweight the benchmark to the narrative around advanced computing, and

2. It’s no secret that high-quality stocks have been underperforming low-quality stocks for over two years now. That said, the team has also identified that there may be an overweight to stocks that have a market-driven AI dis-intermediation narrative surrounding them, whether correct or not.

We believe that this trade helps bolster the overall portfolio, attacking the aforementioned risks. And that sometimes, the sale is more important than the buy. Lastly, even though we are increasing the portfolio’s exposure to the AI-narrative, we don’t believe that this sacrifices the strategy’s stellar downside protection. Overall, this will increase our risk-adjusted beta in a well-diversified company that we believe has a long runway for growth.

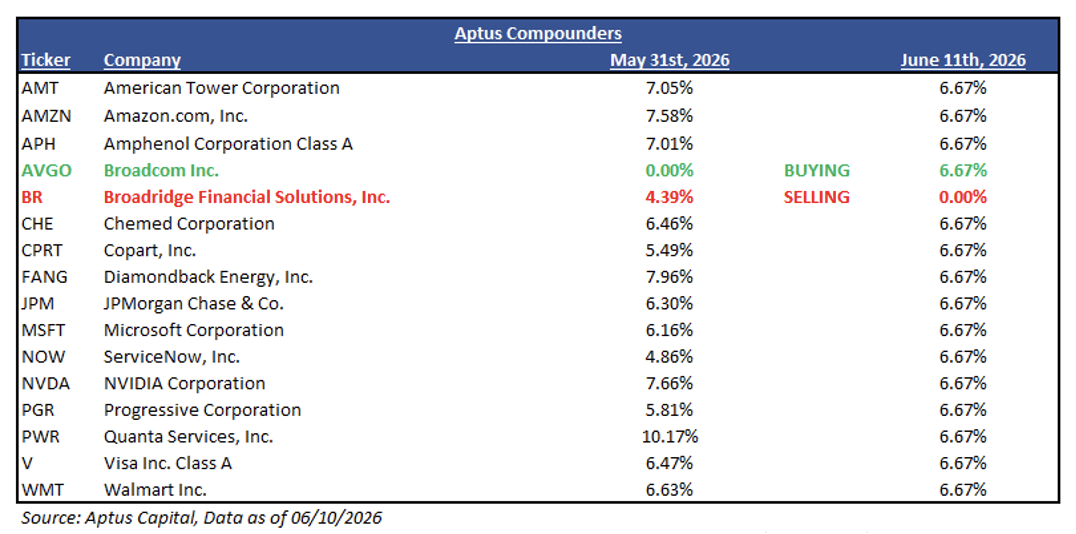

*This Trade includes a full rebalance of the Compounders Portfolio*, as Quanta Services Inc. (PWR) has become oversized in the allocation.

Sale: Broadridge Financial Solutions (BR)

The Aptus Compounders portfolio is selling Broadridge Financial Solutions (BR). The Equity Team continues to believe in the company long-term, as they believe that fundamentals remain quite strong, but have recognized that fighting the near-term narrative around AI-disintermediation is a losing battle.

The disintermediation narrative suggests tokenized securities can settle atomically on the chain (delivery vs. payment in real time), eliminating the multi-day settlement cycle (T+2/T+1) that requires Broadridge’s reconciliation, clearing, and processing services. If settlement is instantaneous and automated via smart contracts, the infrastructure layer Broadridge occupies shrinks dramatically. While investors have not seen any of this in the business’s execution, the market is adamant about seeing this threat through. However, the team continues to think the bear case around tokenization is overstated and appreciates that Broadridge is rapidly working to roll out client solutions in this area, as it’s likely that it will likely add complexity but operate via a broker-facilitated world, leaving Broadridge well positioned to help both issuers and brokers.

As the Equity Team always says, investors need to follow what the market is telling them, and right now, the market is telling them that it’s not proper to continue holding in the Compounders strategy.

Purchase: Broadcom Inc. (AVGO)

The Equity Team believes that Broadcom Inc. (AVGO) makes an exceptional stock investment because it acts as a diversified, highly profitable tollbooth on the global technology highway. While companies like Nvidia dominate generic AI processors, Broadcom dominates the lucrative niche of custom AI chips and essential high-speed networking hardware, resulting in explosive, triple-digit growth in its AI segment. What truly sets Broadcom apart from its hyper-cyclical chip peers is its defensive “moat”: its massive infrastructure software portfolio (powered by VMWare) brings in predictable, multi-billion-dollar recurring subscription revenue. Managed by an aggressive, efficiency-focused leadership team, this unique hardware-software hybrid generates a massive 40%+ free cash flow margin, allowing the company to aggressively reward investors through reliable dividend growth and massive stock buybacks

The Team does recognize that shares may be on pause for a short while – and that’s okay. But the story gets even more interesting once it enters 2027. And at the end of the day, the team will own a company growing revenues and EPS >50%, with gross/operating margins in the 70s/60s, and potentially trading at a teens forward P/E valuation in an environment that is only getting stronger for them. If investors have to wait a quarter or two for that story to re-emerge that’s OK – the team will gladly wait for it.

Thank you for your continued trust.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

Information presented in this commentary is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Information specific to the underlying securities making up the portfolios can be found in the Funds’ prospectuses. Please carefully read the prospectus before making an investment decision. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy.

The company identified above is an example of a holding and is subject to change without notice. The company has been selected to help illustrate the investment process described herein. A complete list of holdings is available upon request. This information should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any of the holdings listed have been or will be profitable, or that investment recommendations or decisions we make in the future will be profitable.

The S&P 500® Index is the Standard & Poor’s Composite Index and is widely regarded as a single gauge of large cap U.S. equities. It is market cap weighted and includes 500 leading companies, capturing approximately 80% coverage of available market capitalization.

The content and/or when a page is marked “Advisor Use Only” or “For Institutional Use”, the content is only intended for financial advisors, consultants, or existing and prospective institutional investors of Aptus. These materials have not been written or approved for a retail audience or use in mind and should not be distributed to retail investors. Any distribution to retail investors by a registered investment adviser may violate the new Marketing Rule under the Investment Advisers Act. If you choose to utilize or cite material, we recommend the citation be presented in context, with similar footnotes in the material and appropriate sourcing to Aptus and/or any other author or source references. This is notwithstanding any considerations or customizations with regards to your operations, based on your own compliance process, and compliance review with the marketing rule effective November 4, 2022.

Aptus Capital Advisors, LLC is a Registered Investment Advisor (RIA) registered with the Securities and Exchange Commission and is headquartered in Fairhope, Alabama. Registration does not imply a certain level of skill or training. For more information about our firm, or to receive a copy of our disclosure Form ADV and Privacy Policy call (251) 517-7198. ACA-2606-10.