Investors love to talk about performance. Advisors love to show charts. But the number that matters most is the return clients actually capture, both pre-tax and after-tax, while still protecting against inflation and market drawdowns. Traditional portfolios often miss the mark on both counts. We did an August webinar on this.

For decades, the 60/40 portfolio has been the default. 60% equities for growth, 40% bonds for “safety.” On paper, it looks balanced. In practice, bonds have often been an anchor on returns, and their supposed safety disappears once you adjust for inflation and taxes.

The challenge for advisors today is not simply finding yield or chasing income. It is constructing portfolios that a) deliver higher pre-tax returns, b) compound more effectively after taxes, and c) protect clients from the risks that can derail long-term plans.

Why Bonds Struggle to Deliver

Bonds have historically been treated as the ballast of portfolios. They provided income and diversification when stocks fell. That framework made sense in a world of falling interest rates and lower inflation. But when you zoom out over longer horizons, the picture is far less flattering.

Looking at 100 years of U.S. Treasuries, the real return after taxes and inflation has been close to zero. Yes, there were short bursts of strong returns, but over the full century, compounding was flat. Add in the fact that bond coupons are taxed each year at ordinary income rates, and what investors often see is negative real compounding.

The problem is compounded by inflation. A 4% bond yield in a 3% inflation environment is not a real return at all after taxes. It is a slow loss of purchasing power disguised as income.

This reality makes bonds less of a “safe haven” and more of a drag on both pre-tax and after-tax growth.

A Better Framework for Asset Allocation

If bonds are not delivering real returns or meaningful diversification, the traditional model of more bonds for conservative clients and more stocks for aggressive ones breaks down. The better question is: how can we design allocations that maximize compounded growth while keeping drawdowns in check?

One answer is to reduce the reliance on bonds and increase equity exposure, while explicitly managing downside risk through hedges. Reallocating from a 60/40 portfolio to something closer to 80/20 can materially improve outcomes. Done right, this does not mean taking more risk. By using well-structured hedges, it is possible to raise expected pre-tax returns and lower drawdowns compared to the traditional mix.

Rethinking Risk Management

Risk management has too often been equated with holding bonds. The assumption was that bonds would rise when stocks fell. But recent years have shown that this correlation cannot be relied upon.

A more robust approach is to use explicit hedges that cost something upfront but can provide meaningful risk mitigation. Think of allocating 95% to equities and 5% to hedges. When markets rise, clients capture nearly all of the upside. When markets fall, the hedges do their job.

This approach reframes the conversation. Instead of relying on bonds as a blunt tool, advisors can be thoughtful about where growth comes from and how risk gets managed.

Tax Efficiency as Daily Alpha

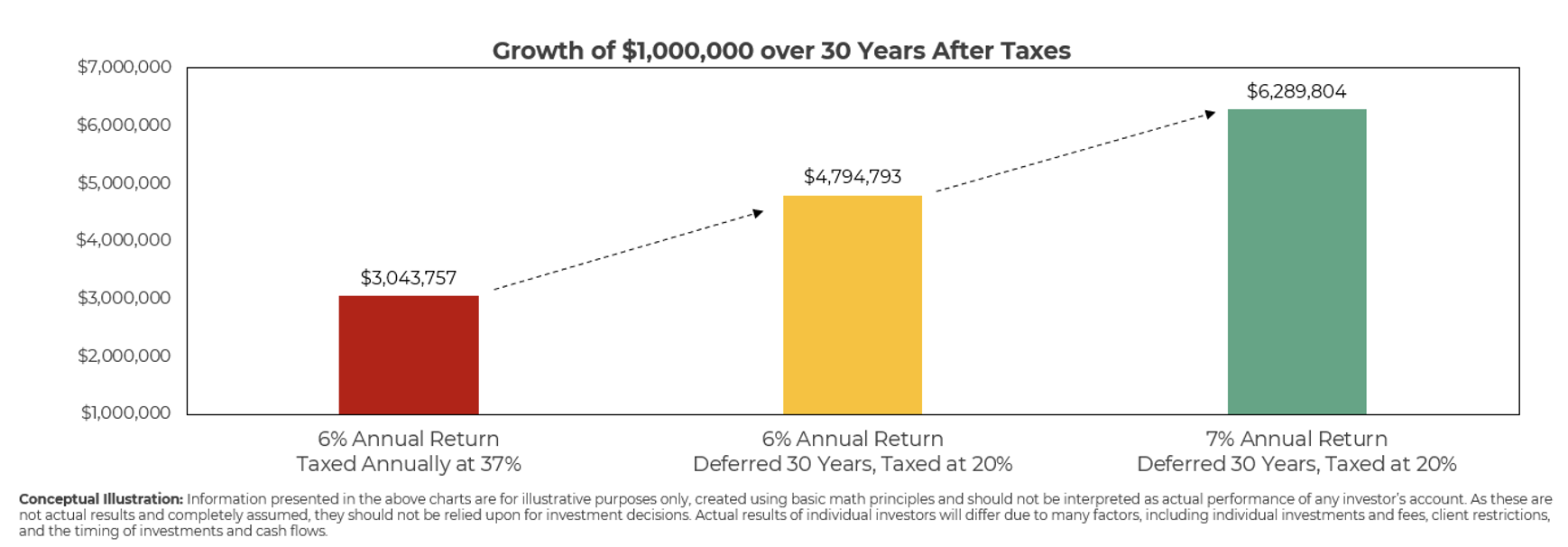

Even the best allocation decisions can be undermined if portfolios are not tax efficient in a non-qualified plan. Taxes matter not just at the end of the year, but every single day that compounding is at work. The difference between annual taxation and deferred taxation is staggering.

Consider a 6% annual return. If taxed each year at high short-term rates, $1 million compounds to roughly $3 million over 30 years. Simply deferring taxes until the end, paying long-term capital gains instead, results in nearly $5 million. That is a more than 50 percent improvement without any change to the investment return.

The lesson is clear: tax efficiency is alpha. It is incremental value that accrues to clients no matter what markets do.

Three Ways to Improve Tax Efficiency

Advisors can improve after-tax returns by rethinking both the vehicles and the strategies they use:

1. Favor equities over bonds. Equity gains are often taxed at lower long-term rates, while bond coupons are taxed annually as ordinary income.

2. Use ETFs. The ETF structure allows for in-kind creation and redemption, reducing taxable events often paid out through mutual funds and separately managed accounts.

3. Explore innovative ETF alternatives. New strategies that are designed to replicate fixed income exposure without taxable distributions, deferring income until realization.

As a whole, this transition aims to capture more of the right tail when markets are strong, protect capital in the left tail when markets fall, and simply track markets in between. Over time, that path can drive higher compounded growth for clients, with higher after-tax capture.

The Bigger Picture for Advisors

Advisors are not just portfolio managers; they are stewards of client wealth. Every decision about allocation and taxes has ripple effects that determine whether clients meet their goals, fund their legacies, and secure their financial independence.

The good news is that advisors do not need to outsmart the market with brilliant stock picks to deliver value. By improving asset allocation and focusing relentlessly on both pre-tax and after-tax compounding, advisors can generate tangible, lasting benefits.

This is not about chasing benchmarks. It is about building portfolios that truly serve clients, compounding more effectively over time, and creating better outcomes that clients can feel in their retirement, in their charitable giving, and in the wealth they pass on.

Key Takeaways for Advisors

-

- Rethink bond allocations on both pre-tax and after-tax bases.

- Use “equity plus hedge” framework to raise expected returns without increasing drawdowns.

- Maximize tax efficiency through ETFs and deferred income structures.

- Focus conversations on what matters most: terminal wealth, returns that clients keep, and purchasing power.

The path to higher returns is not complicated. It is about more directly targeting improvements in allocation, risk management, and vehicles. We think advisors who embrace this approach can not only deliver more value to clients but also strengthen their own practices.

Disclosures

Past performance is not indicative of future results. This material is not financial or tax advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed and all calculations may change due to changes in facts and circumstances.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2508-27.