I thought the old saying was: “Markets fall like an elevator, but rise like an escalator“, but I guess it’s the opposite as of late.

- In 2026, the market had its fastest recovery to all-time-highs (“ATH”) following an 8% drop. The market reclaimed its highs in just 11 trading days.

- In 2025, the market had its fastest recovery to ATH following a 15% drop; it only took 55 days to reclaim the highs.

This is just another reminder that the market is smarter than all of us and is a forward-looking mechanism.

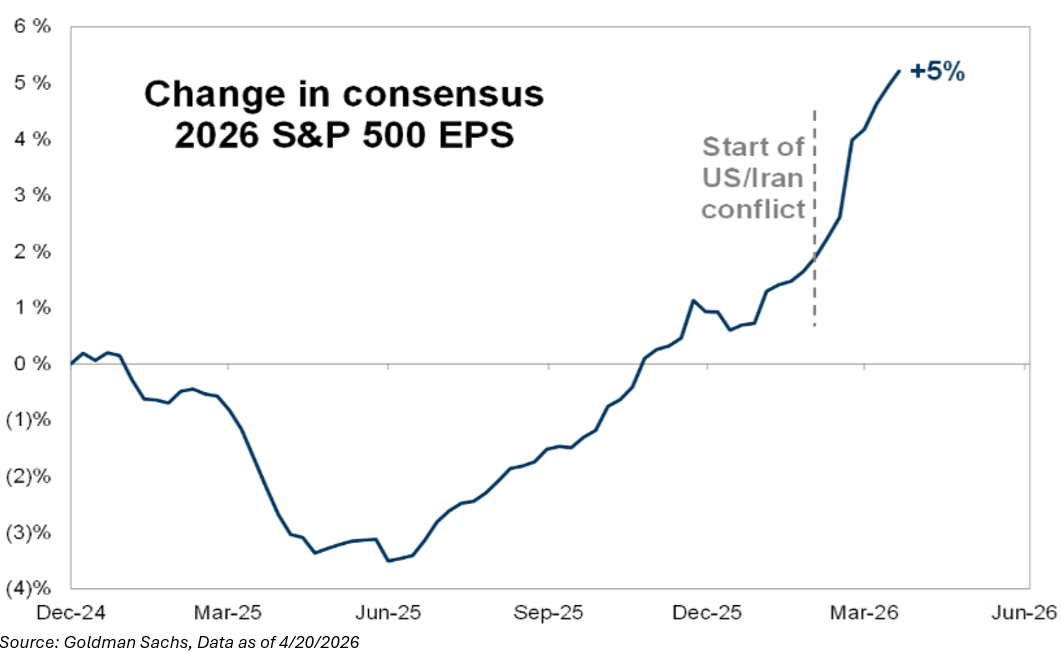

But many would have thought a rebound would mean a broadening market; that wasn’t quite the reality. The market is narrowing again in the recovery from the post-March lows, even more narrowly than the post-Liberation day rally. It seems like Technology and AI infrastructure are sucking the oxygen out of the room for essentially all other sectors. But, looking back one final time, it appears to me that the market sniffed out the trail three weeks ago; the conflict would result in a short-term inflation pinch, not a lasting growth shock.

In that context, consider this: S&P earnings estimates have been marked higher every single week since the conflict began. Looking forward, this now becomes a show-me story; the ceasefire must hold, the US economy must prove it didn’t buckle, and US mega-cap tech names must deliver.

So, let’s get our hands dirty and see what the market needs to deliver from an earnings standpoint because, just this AM, I watched Bloomberg TV for the first time in years and kept hearing the talking heads call it, “Earn-mageddon”. Come on, y’all.

Q1 2026 Earnings Preview

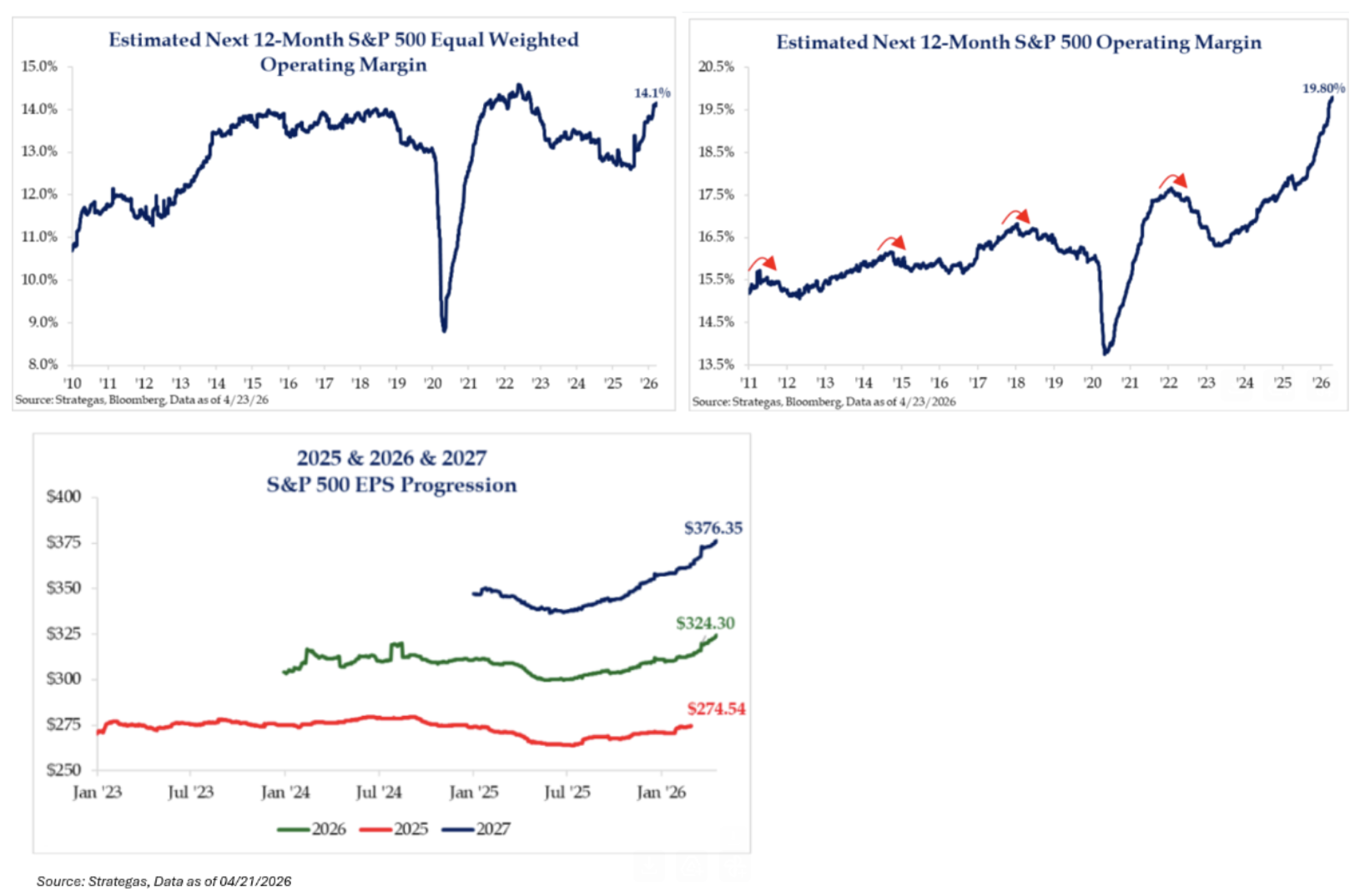

If anyone has listened to our commentary over the last few weeks, they know that now is not the time to panic because two simple market basics remain very strong: earnings growth and profitability. In fact, earnings growth for the S&P 500 is now expected to grow 18% in 2026. Is that good?

As I stated above, EPS expectations have increased every week since 2/27.

Let’s start with some spice. Some may call this a “Hot Take“, I’d call it rational. The EPS growth story is not going to be derailed due to higher input costs (via oil). It’s no secret that the energy sector has driven a lot of the increase in EPS expectations since the beginning of March. But many will question the legitimacy of this, as it’s likely to be negated due to higher input costs. So, when I say that EPS is expected to grow 18% in 2026, some naysayers will say that estimates are not updated because they’re not factoring in prices and potential economic slowdown due to the Iran war.

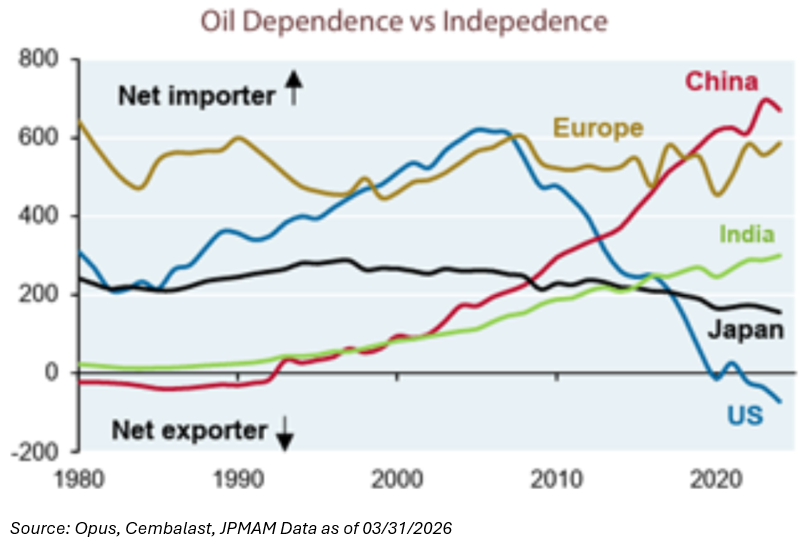

Personally, I do not think that the Iran war has anything real to do with most equities besides Energy companies. It’s a distraction from the real key variable – growth. The doomers (or “Panicans” as John Luke would put it) would say that many barrels of oil will never reach the market (that’s probably correct), driving oil higher. But those higher energy prices may only affect things for 12-18 months, so as long-term investors, who really cares? Investors should be smart enough to see through this.

We’ve read that if oil averages $90/barrel in 2026, it could be a 4%-5% headwind to earnings. And I bet that figure is conservative. Because we are not the energy-dependent country that we used to be in the 1970s and 2000s.

Moving on, corporate and consumer resiliency have been consistently underestimated. And after multiple shocks since COVID, companies are better positioned to navigate disruptions. Plus, operating margins are expanding, the second core tenet explaining the market’s resilience.

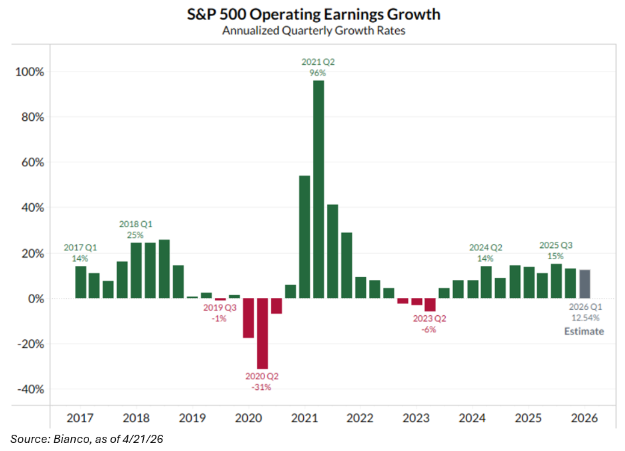

Although we’ve discussed CY 2026 earnings extensively, the Q1 2026 year-over-year (“YoY”) earnings are expected to be 12.5%. This suggests even greater YoY growth is likely for Q2, Q3, and Q4.

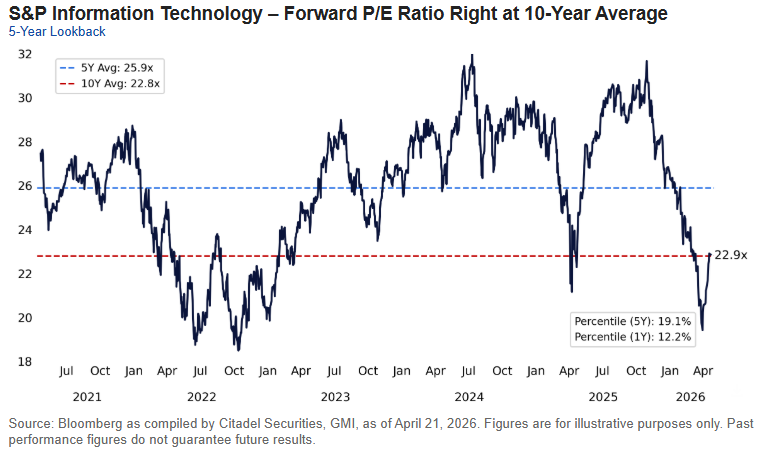

With valuations looking quite appealing, even on the Technology side of the ledger:

After the recent rally, there’s likely some increased optimism about this earnings season, so the bar may be higher than it was four weeks ago. Since companies are unlikely to change their annual guidance significantly in Q1, our focus will remain on AI capital expenditure (“CapEx”) spend, as AI is driving most of the recent earnings growth.

Given the skepticism about AI profitability and the recent market run, there will be significant stock dispersion beneath the market’s surface. Please reach out if you have any individual questions about any stocks, or if you’d like to see our Q1 2026 material.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2604-25.