IPO investors are high-fiving right now with 2026 shaping up to be a record year for public offerings. We’ve fielded a lot of questions in regard to the SpaceX IPO, so I thought we’d write a Musing on it.

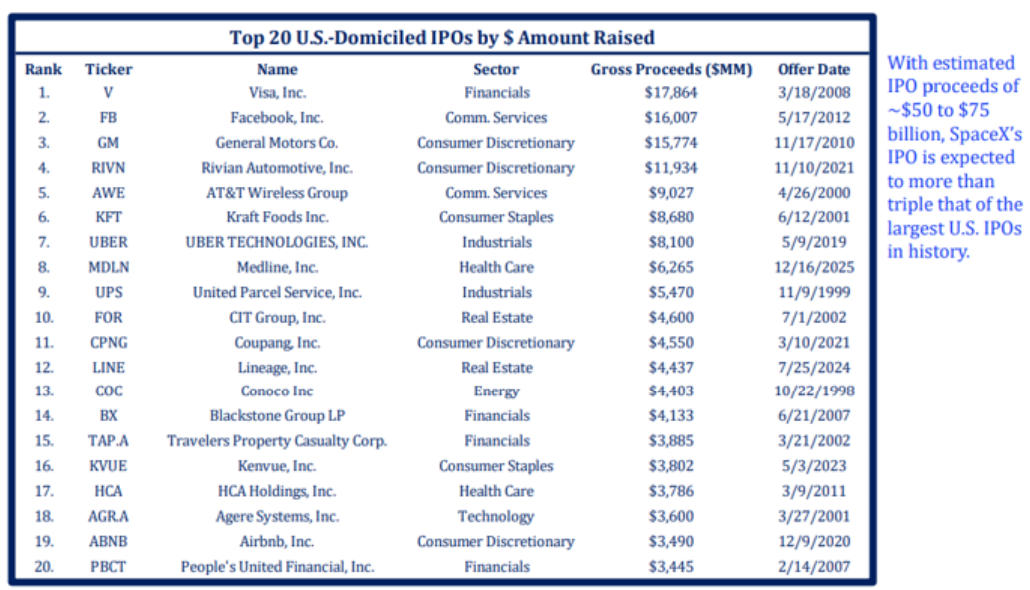

Source: Strategas as of 5.4.26

Source: Strategas as of 5.4.26

The SpaceX IPO

The 2026 IPO market is shaping up to be a historic year for “mega-listings,” driven by a massive backlog of high-valuation tech and aerospace companies finally testing the public waters. After a period of selective recovery in 2025, investor appetite is now anchored by giants in artificial intelligence and space exploration, with SpaceX and OpenAI leading the list of most-watched potential debuts. Industry analysts suggest that if these “juggernauts” proceed, total US IPO proceeds could surpass $140 billion, potentially setting a new record.

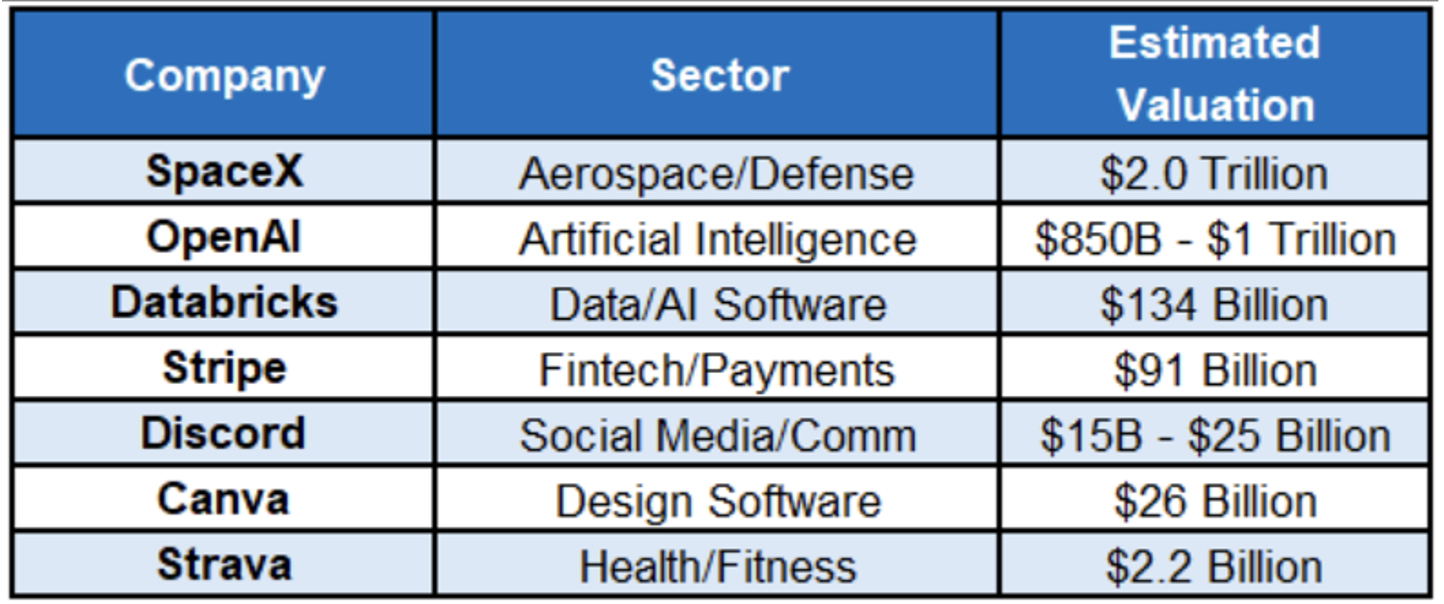

While the AI sector remains the dominant theme with names like Anthropic, Databricks, and Cohere in the pipeline, other long-awaited “unicorns” such as Discord, Stripe, Canva, and the fitness platform Strava are also eyeing 2026 windows. However, the market is likely to remain disciplined; investors will prioritize companies that demonstrate durable revenue models and clear paths to profitability over those fueled purely by hype, meaning the “window” stays widest for established leaders, not the speculative gambles.

Source: Bloomberg as of 5.4.26

Source: Bloomberg as of 5.4.26

It’s easier to discuss the SpaceX IPO in a Q&A format.

Question: Can my clients participate in the IPO?

Answer: Yes, it is historically quite tough for the average retail investor to get IPO shares at the offering price. While the landscape is shifting slightly in 2026, the “game” is still heavily weighted toward big players. Here is a breakdown of why it’s difficult and how the process actually works.

-

- The “Institutional First” Rule: In a traditional IPO, investment banks (underwriters) handle the share distribution. Their goal is to ensure a stable, successful launch, so they prioritize:

Institutional Investors: Hedge funds, pension funds, ETFs, and mutual funds. They buy in massive blocks and are seen as “stable hands.”

High-Net-Worth Clients: Brokerages often reserve their limited retail allocation for “Gold” or “Platinum” clients who have substantial assets.

-

- The Lottery System: Even if your broker offers IPO access (like Fidelity & Charles Schwab), they usually receive a tiny fraction of the total shares. If an IPO is “hot” (highly anticipated), it becomes a math problem:

Oversubscription: If 1 million retail investors want shares but the broker only has 50,000 to give, they use a lottery system or a pro-rata allocation.

The Result: You might request 100 shares and receive 5 or zero.

There is a famous saying in IPO investing: “If you can get it, you probably don’t want it.” Why?

Strong Demand: If an IPO is expected to “pop” 50% on day one, institutional investors will gobble up every share, leaving nothing for retail, or

Weak Demand: If big banks and hedge funds are passing on an IPO, underwriters will suddenly be very “generous” with retail allocations. If you find it remarkably easy to get a full allocation for an IPO, it might signal low professional interest.

With this, in IPO situations, we prefer to wait and see. The stock will likely see some early volatility, both positive and negative. Given there will be low float of shares, it could create some really strong demand, so we might see that IPO “pop” on the first day. I have seen that the share float trading will be just 5%. Given that the stock has been private for so long, you’d have to imagine you’ll see some insider selling when their lockup periods end due to the additional liquidity. One reason a company enters the IPO market is to bring liquidity to early investors.

At Aptus, we prefer to seek alpha through proper asset allocation structure (more stocks, less bonds, while remaining risk neutral at the allocation level), not striking it big on the IPO market.

Question: What are your thoughts on valuation?

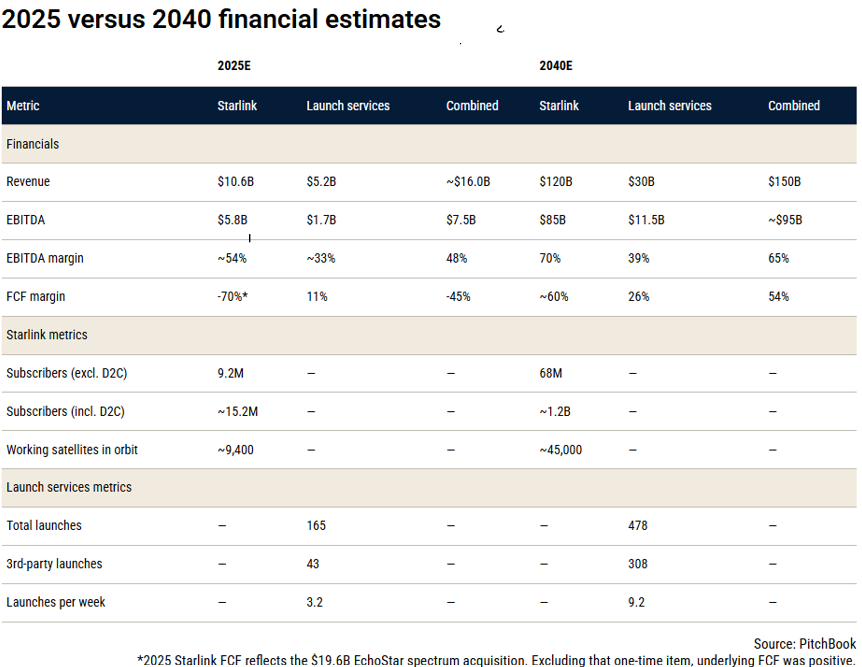

Answer: It’s expensive. This is why we are somewhat “toned down” on the stock. The valuation isn’t really supported by the fundamentals. Here is a breakdown of its 2040 estimates:

Data as of May 2026

Data as of May 2026

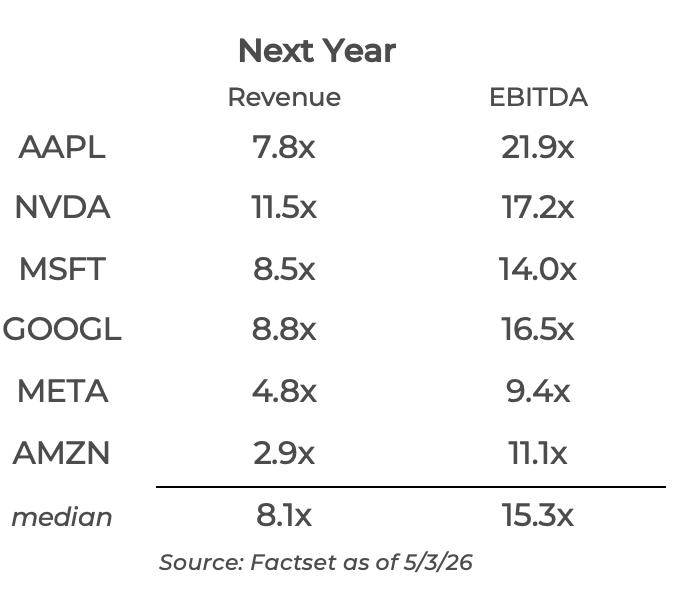

$150B revenue in 2040! At a $2T IPO valuation, that’s 13x 2040 revenue and 21x 2040 EBITDA. For context, here are some comparisons:

In other words, even after baking in 14 years of growth, SpaceX is vastly more expensive than the top 6 most valuable US public companies are today! We struggle to get on board with that, no matter the potential behind a company.

Question: Will it be included in the Indices?

Answer: I’m looking at how each index will modify its rules-based inclusion system to allow these new, mega-cap IPO stocks into the benchmark. This feels more like a court case that sets future precedent, if anything. Here’s an example: The NASDAQ changed the rules for index inclusion, effectively solidifying that the stock would trade on the NASDAQ, not the NYSE.

The New “Fast Entry” Rule: Effective May 1, 2026, Nasdaq updated its inclusion methodology to create a “Fast Track” for massive companies. This change is significant for several reasons:

-

-

- Timeline: Previously, new listings typically had to wait 3 to 12 months (often waiting for the annual December rebalance) to be considered. Under the new rules, a mega-cap IPO -defined as ranking within the top 40 by market capitalization – can be eligible for inclusion after just 15 trading days;

-

-

-

- Notice Period: Nasdaq now requires only five days of market notice before adding these qualifying companies to the index; and

-

-

-

- Float Requirements: The exchange has eliminated the strict 10% minimum free-float requirement for these mega-caps, allowing companies that list only a small percentage of their total shares to still qualify for the index. They also changed rules to allow 3x float.

-

This could place it on a timeline for a QQQ inclusion by July. At a $2.0T valuation, if SpaceX only floats 4.3%, its “standard” inclusion weight would be negligible. Applying the 3x multiplier treats SpaceX as having a $225 billion “index market cap” for weighting purposes. For context, a $260B effective market cap would put SpaceX’s weight roughly on par with companies like Palantir or Netflix (depending on their current prices), but significantly below the “Magnificent Seven” giants like Apple or Microsoft. The result will likely be a position of ~1.1% to 1.3%.

The S&P is also working through similar changes. We guess S&P 500-type funds will include it in their year-end reconstitution, with a chance of it happening sooner (they rebalance around the last Opex day of each quarter). However, we would feel comfortable saying that this inclusion will likely take longer than QQQ.

Lastly, we wouldn’t rule out some sort of “float” squeeze with active managers trying to front-run that trade before index flows hit, but that is currently a tough world to predict.

For portfolio consideration, given that many of our equity baskets need to correlate to the S&P 500 – allowing our hedging profiles to dictate performance – we are closely monitoring SpaceX’s inclusion date and overall weight.

Question: Can I get indirect exposure to SpaceX?

Answer: Yes. Here are a few ways, though we don’t suggest them:

1. GOOGL (Alphabet) – Alphabet owns 6.11% of the company

2. SATS (EchoStar) – As of early 2026, EchoStar owns approximately 2%-3% of SpaceX. While that percentage might sound small, the context of the deal has made EchoStar one of the most talked-about “backdoor” ways for retail investors to gain exposure to SpaceX before its rumored mid-2026 IPO.

3. TSLA – Many would assume Tesla owns some shares, but it has no direct ownership. Elon Musk running both companies likely means there will be some ties between them.

4. A few funds state that they own some of the private shares; contact us if you’d like to know which ones. However, this route has pros and cons because I’ve had concerns about private assets held in a daily liquid vehicle. What I dislike is the pricing of the SpaceX positions (my understanding is that the price is re-marked every time there is a secondary offering).Since we are closer to the IPO than ever, I feel a bit better; ultimately, the listed market dictates the price. My fears before real IPO traction were a weak secondary offering, the SpaceX position being marked down, and seeing the fund down 20% or something based on that. Less likely now, but this doesn’t eliminate the SpaceX risk until the IPO

Advantages:

-

- This is one of the last true ways to get exposure to SpaceX; most private vehicles have closed off access.

- Daily liquidity allows clients to access their capital without any lockup periods.

- Some diversification as the funds tend to hold other positions (even if they are looking for just SpaceX position); and

- Should seamlessly transition to owning SpaceX shares directly.

Disadvantages:

-

- Investors are at the mercy of whatever else they own (another diversification benefit is that the index the fund follows might not perform well).

- Pricing transparency – this kind of disappears post-IPO, but I have never loved Special Purpose Vehicles (SPVs) as it isn’t entirely clear how they value the SpaceX position. For example, there is no listed price, and while the weighting may say a weight, the market value could be higher or lower.

- Costs – the SPV must be fairly expensive; many of these funds state all-in costs of nearly 2%, even though the management fee is less than 1%. That is 1% or more in additional expenses that can/will drag fund performance. I would assume a lot of this gets marked down post-IPO as they should just be long the shares, but we’ll have to see then.

- What is the next private company they hold? Many of these funds’ biggest selling points are owning private investments as a significant portion of the fund. Some have owned Klarna in the past, and one currently owns Anduril. I’d be interested to see what they own next and/or if it gets anywhere close to the size/weight SpaceX is now (given the rapid price appreciation in SpaceX, I would assume not). There is risk in the future of backfilling companies that graduate to the public markets.

The IPO market was the “OG” casino gambling game in the market, given the potential to “get rich quick”. But now that there are other forms to gamble on in the market (S/O Brain Jacobs, CFA’s recent piece on Polymarket), it feels like the gambling addiction in the market is insatiable right now – so we’d assume that it’s highly likely that many of you will be asked the SpaceX question in the upcoming weeks.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama.

ACA-2605-9.