Our team reviews a massive amount of institutional research throughout the week to isolate the signals that matter most. This week’s selection steps back to appreciate the unbridled engine of American innovation, the undeniable fundamental strength of corporate margins, the physical requirements of the AI build-out, and shifting mechanics in the credit and rate markets.

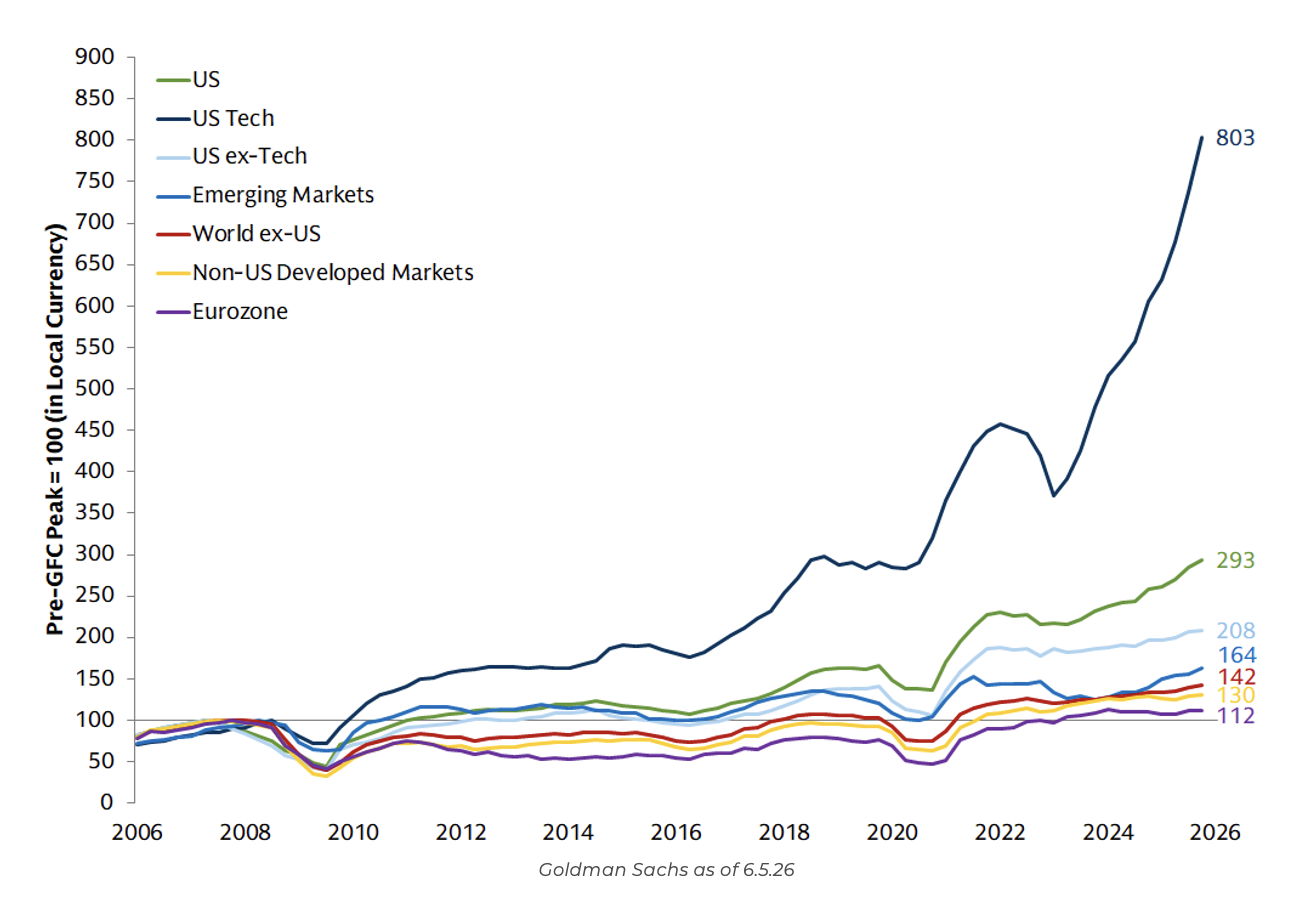

John: When looking back at the core story of the capital markets in the first half of 2026, so much of what we are analyzing is simply the residue of unbridled American innovation, ingenuity, and risk-taking. The parallels to the shale revolution are clear, but the magnitude of what is playing out in the technology sector today is on another level.

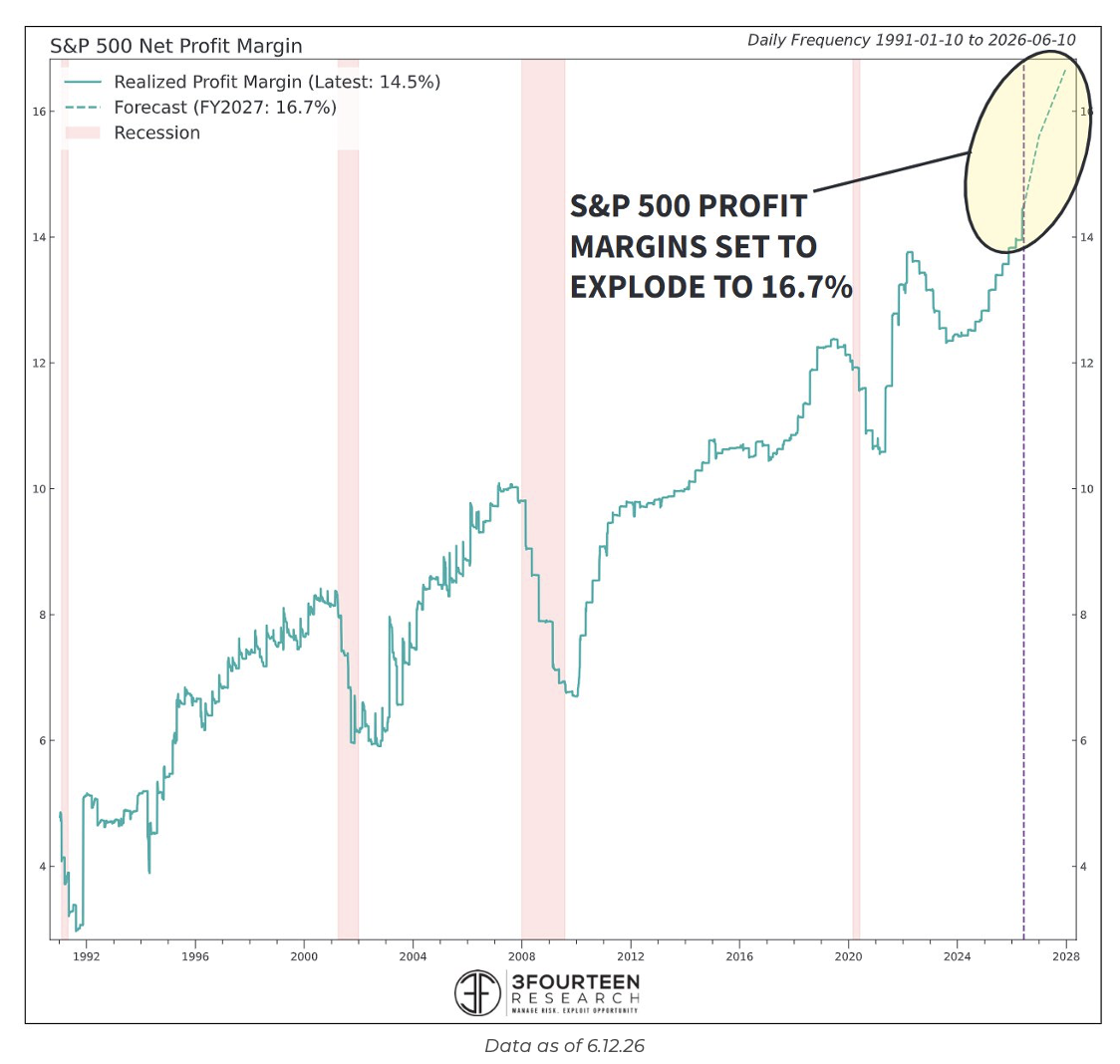

Jake: S&P 500 profit margins continue to hit new records, with forecasts projecting a climb to 16.7%. This incredible profitability is driving the fundamental reality of these companies and mathematically justifying current market valuations.

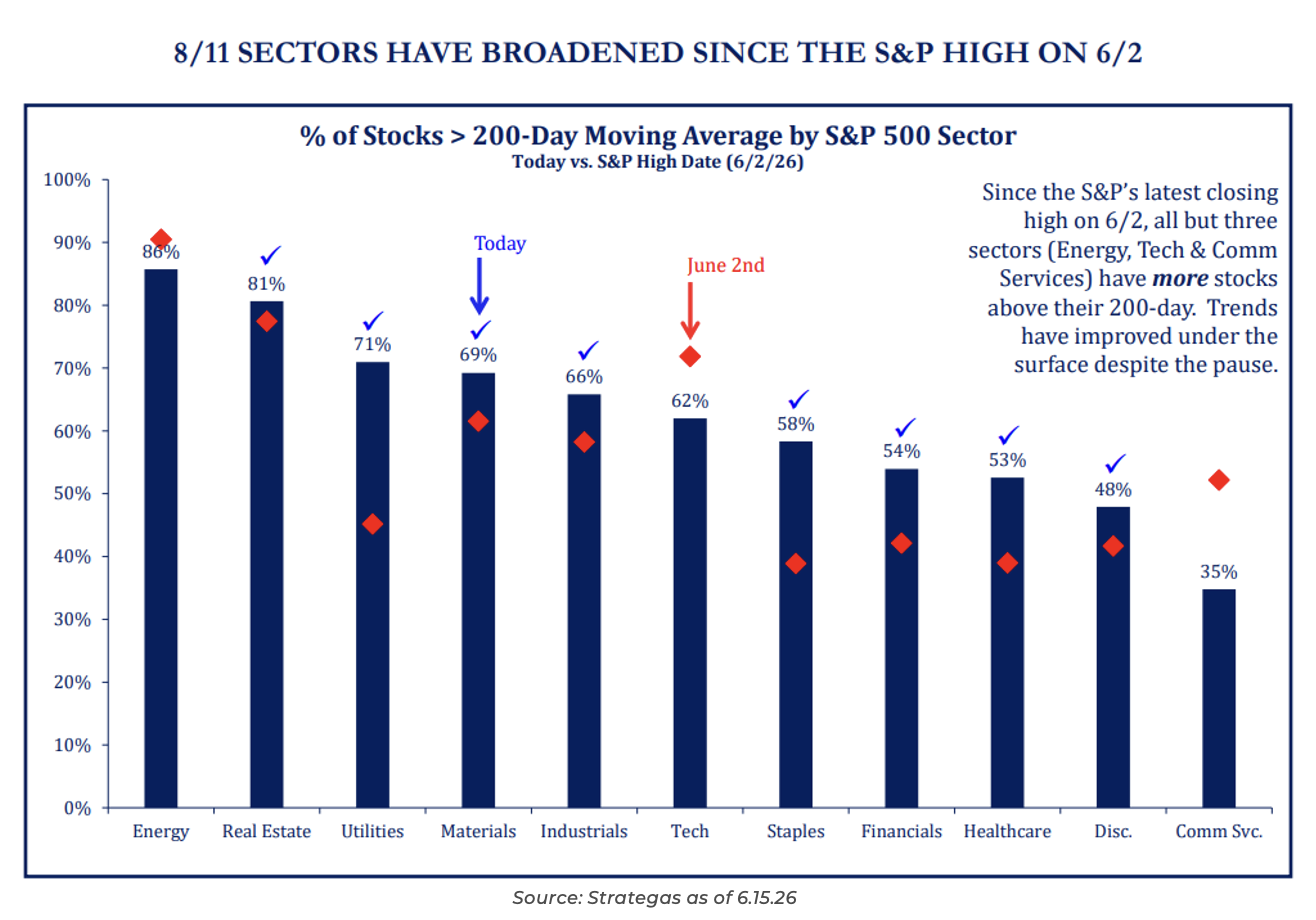

JG: While heavy concentration in Big Tech has been the defining narrative of this rally, we are finally seeing the market broaden out since hitting its recent highs. Rather than a fragile, top-heavy market, capital is starting to rotate into lagging sectors.

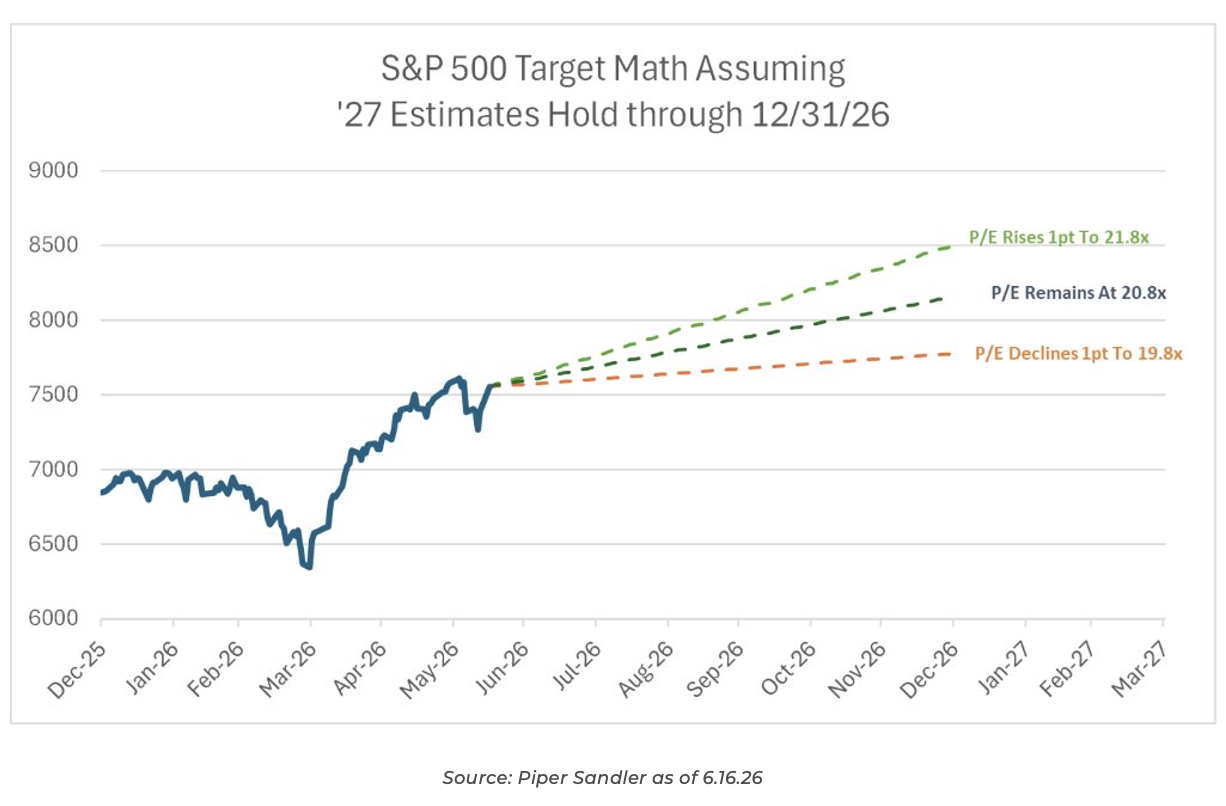

Dave: Ultimately, attempting to predict where the S&P 500 is heading requires solving a two-variable equation: forecasting earnings, and forecasting the multiple applied to those earnings. Right now, forward earnings look exceptionally strong, providing structural support to the market regardless of near-term multiple fluctuations.

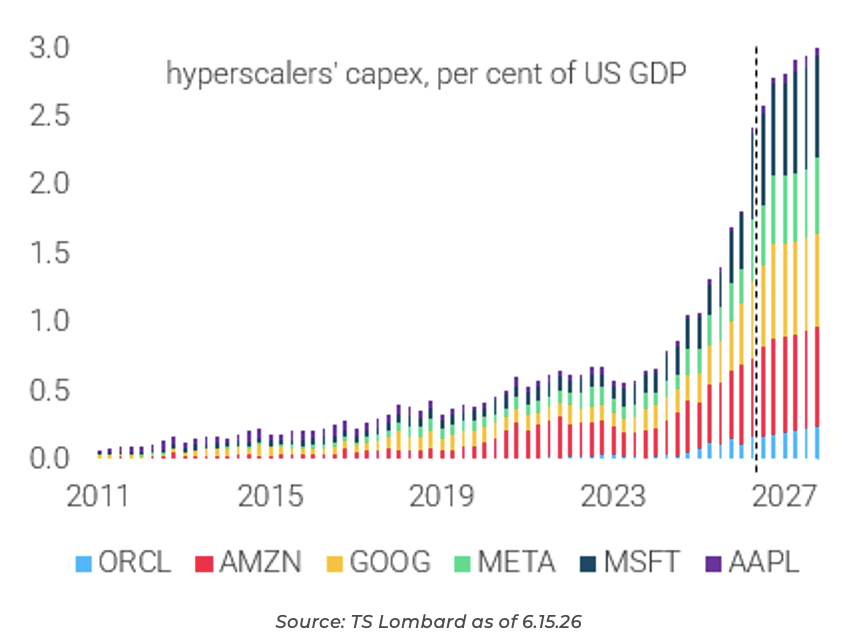

Beckham: The scale of technology investment has transcended sector boundaries to become a macroeconomic pillar. Hyperscaler capital expenditure continues to drive aggregate economic growth and now makes up approximately 3% of U.S. GDP.

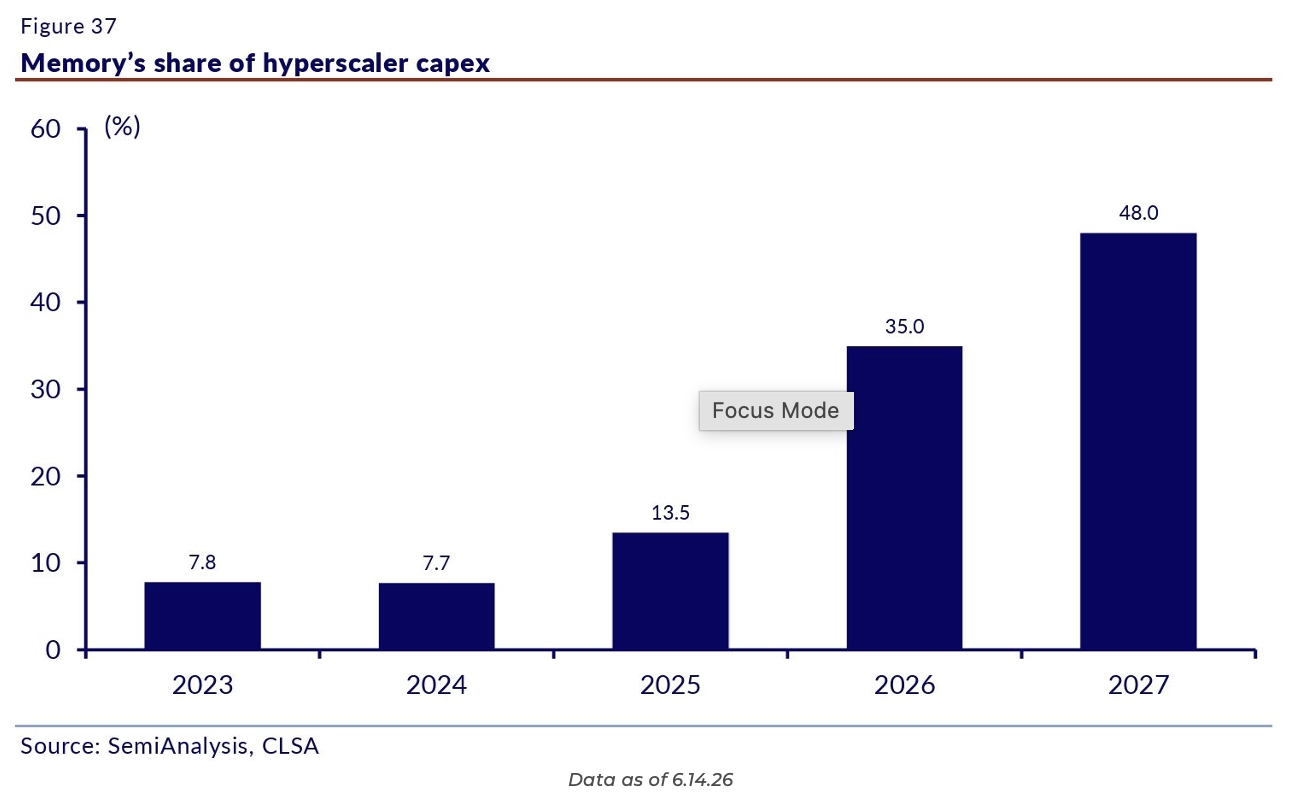

Ten: That massive hyperscaler spend has direct downstream beneficiaries. The ongoing data center build-out requires a massive, structural increase in physical memory, which is capturing a rapidly growing share of total hyperscaler capex budgets.

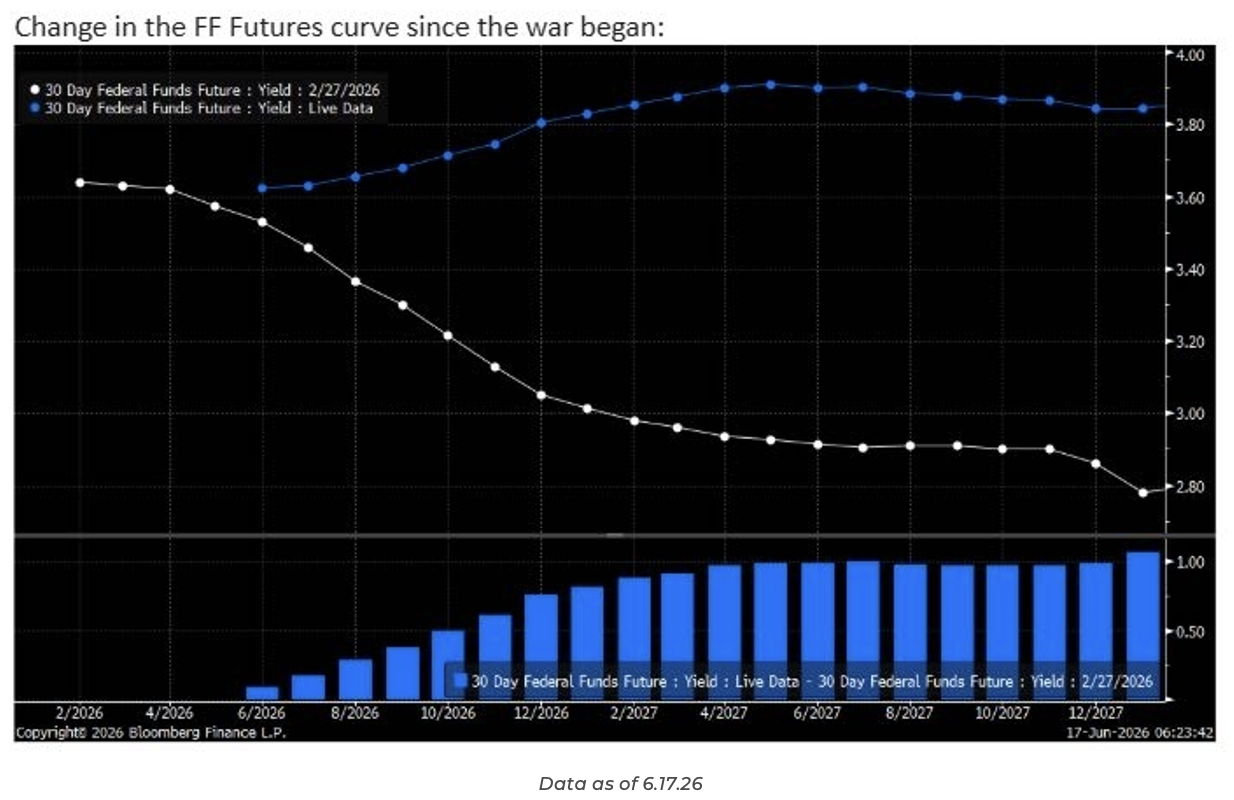

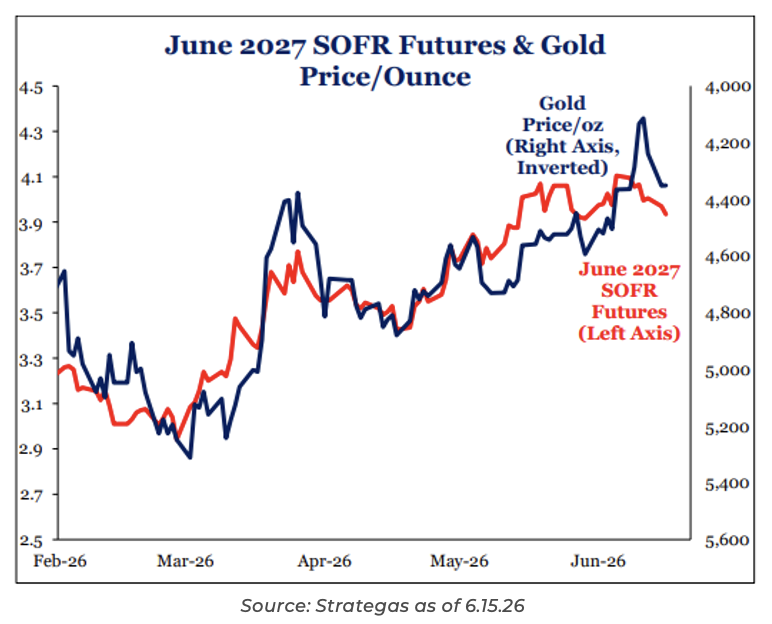

JD: Geopolitics continue to reprice the curve. One of the most significant secondary impacts of the Iranian War has been the dramatic shift in not only inflation estimates, but broader interest rate expectations, as reflected in the shifting Federal Funds Futures curve since the conflict began.

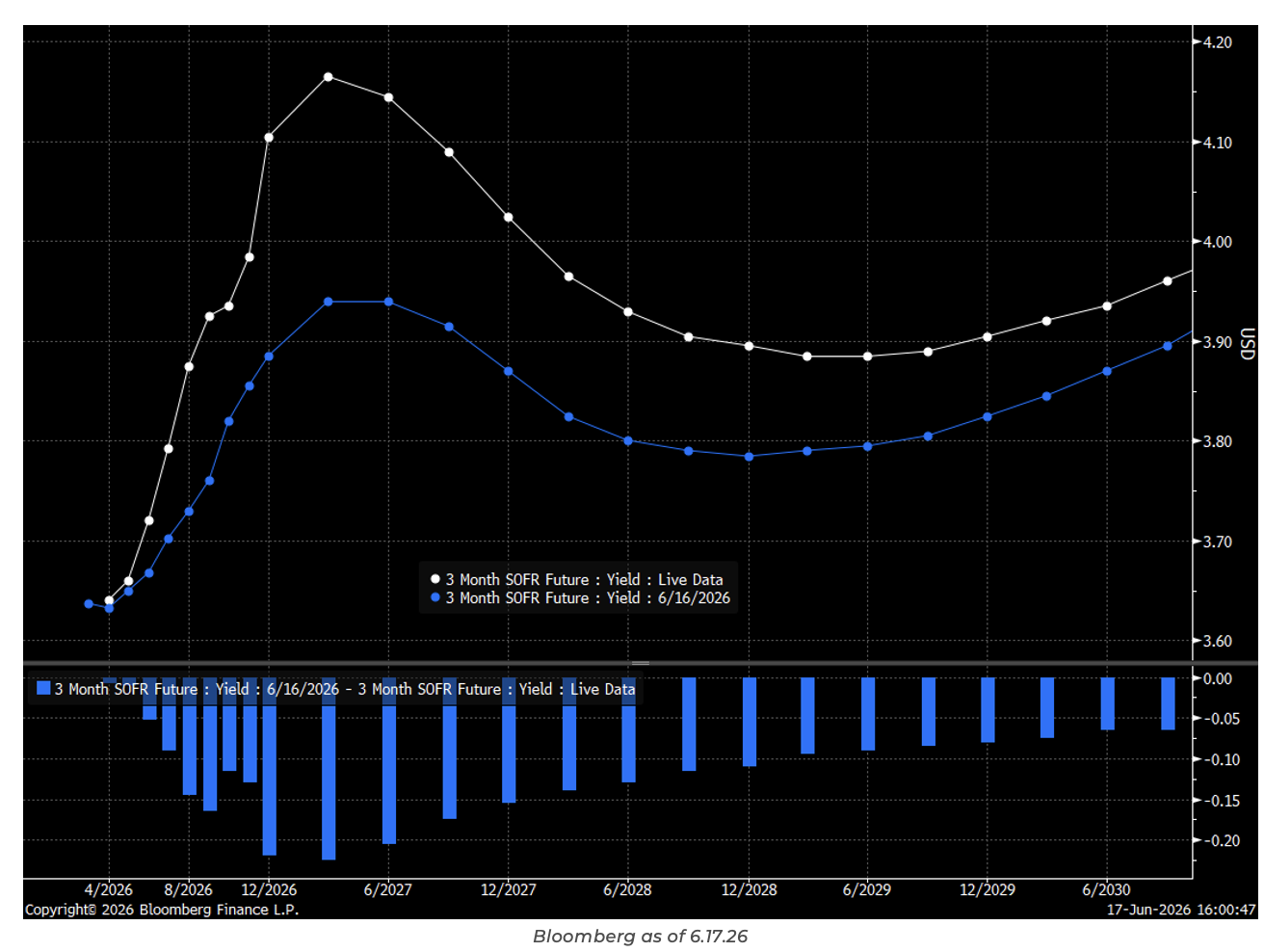

Joseph: Chairman Kevin Warsh’s debut FOMC meeting sent rate expectations higher. While the Fed kept rates steady for now, the hawkish shift removed anticipation of near-term cuts and instead signaled an active rate hike by year end as policymakers battle sticky energy inflation.

Brett: The traditional macro is that gold and real interest rates share a negative correlation, but that relationship has been broken. Despite real yields remaining elevated as rate-cut expectations are pushed out, gold has continually powered to new highs.

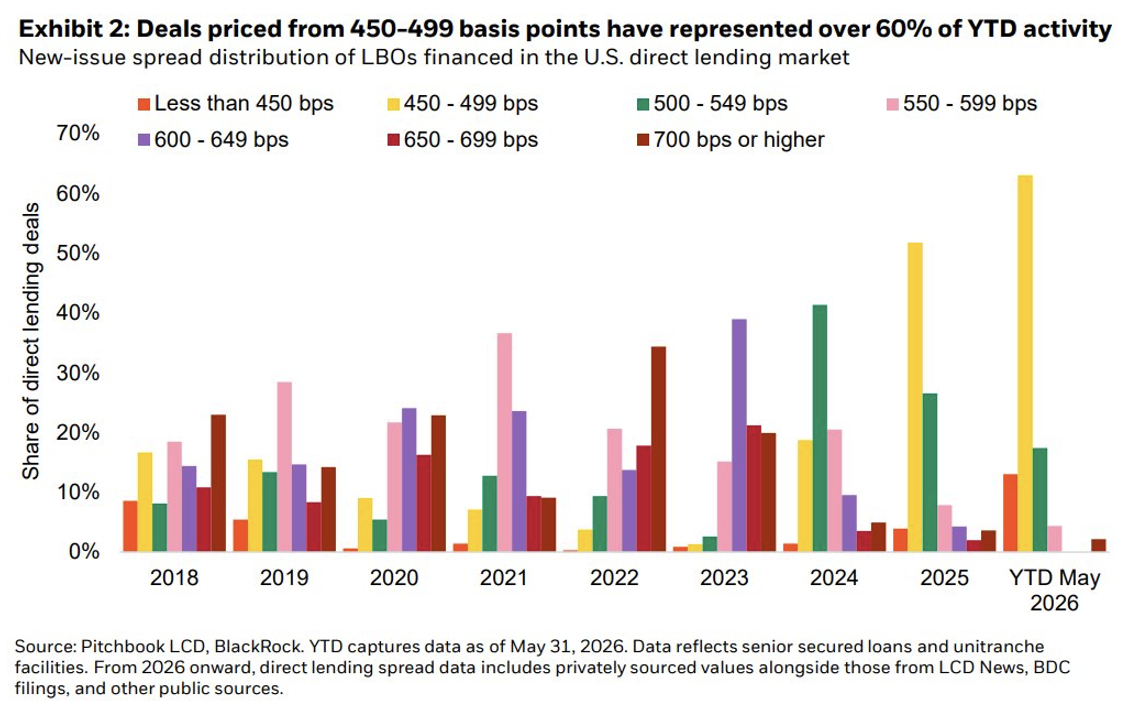

Brad: In the credit markets, over 60% of this year’s direct lending LBOs have priced in a highly concentrated band: 450 to 499 basis points. It wasn’t too long ago that this pricing tier was strictly the domain of Broadly Syndicated Loans (BSLs), highlighting the continued evolution and maturation of private credit.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2606-16.