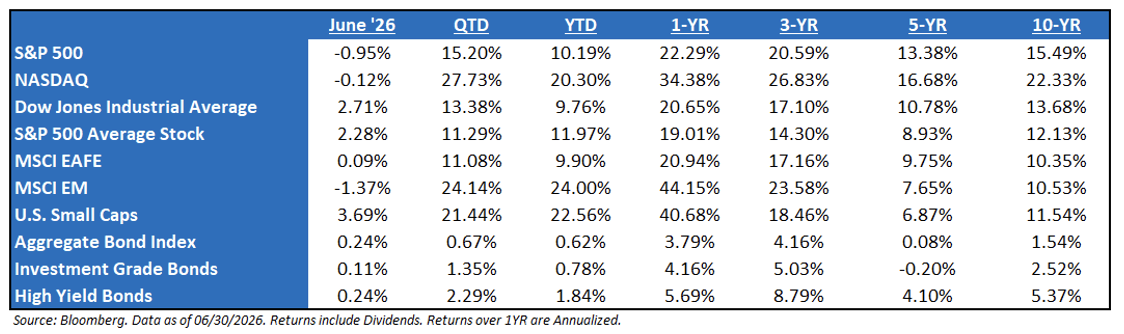

Equity Recap – The First Half of 2026 Has Been a Lesson in Resilience, But Not Stability: S&P 500 Has Best Quarter Since 2020, and NASDAQ Has Second Best Since 2001: Markets have absorbed a remarkable sequence of shocks: the Iran war, renewed energy security concerns, sticky inflation, volatile policy expectations, and the continued reordering of global supply chains. Yet risk assets have held up better than many feared, supported by strong U.S. growth, strong corporate earnings, and relentless artificial intelligence (“AI”)‑related investment. Many of the themes we identified at the start of the year have broadly played out. Fiscal expansion and AI investment have underpinned stronger‑than‑expected U.S. growth. Equity leadership has begun to broaden beyond mega‑cap technology, even as AI remains a dominant force.

Bond Recap: Bond Market Recap → Bear Flattening of the Yield Curve: During Q2 and 1H 2026, global bond markets navigated a “higher-for-longer” environment as sticky inflation – exacerbated by geopolitical tensions and energy price shocks – prompted a patient Federal Reserve to pause aggressive rate easing. While a sharp economic downturn was avoided, the reduction in anticipated rate cuts forced a material repricing that pressured duration-sensitive assets and kept the 10-year U.S. Treasury yield anchored in an elevated 4.0% to 4.5% range. Because the market aggressively priced out near-term rate cuts, short-term yields rose at a faster clip than longer-dated maturities, ultimately driving a distinct flattening of the Treasury yield curve over the course of the quarter.

Aptus’ Phrase of the Year – Get Back to the Market Basics: When markets feel like they’re chaotic, focus on the basics, which are very simple:

-

- Earnings Growth Continues to Trend Higher: With Q1 earnings season in the rearview, the fundamental backdrop for equities remains supportive. As of the end of June, the ‘26 earnings growth stands at 23.6%. If there’s one area of fundamental risk, it’s the continued concentration within the index – it can drive markets higher or lower. For now, though, growth remains robust due to the strong operating leverage from those exact mega-caps.

-

- Profit Growth Remains Strong: Simply said, when economic profitability is increasing or staying stagnant, historically it’s been difficult for the market to get into trouble. Not only is the market-cap weight index, the S&P 500, witnessing operating margin expansion, but the average stock has also seen growth.

When the Biggest Names Stumble, the Rest Don’t Have to Follow: Historically, when mega-cap stocks have sold off, the instinct is to brace for a broader market collapse – but 2026 has challenged that assumption. As the largest technology and AI names pulled back sharply in June, Health Care, Industrials, and Financials held their ground, and the equal-weight S&P 500 continued to outperform its cap-weighted counterpart. Concentration cuts both ways: the same dynamic that makes a handful of stocks look like “the market” on the way up means their stumble doesn’t have to take everyone else down with them.

Why Has the Market Remained So Resilient? Three separate forms of economic stimuli are hitting the economy and markets. Combining these factors increases expectations for economic growth and corporate earnings sustainability.

Monetary stimulus: In September, the Fed cut rates, but more importantly, signaled that a rate-cutting cycle had started. That matters because it means monetary stimulus is now occurring, which is positive for the economy and, peripherally, risk assets. It tends to take 12 to 16 months for rate cuts to flow into the economy.

Fiscal stimulus is occurring via the passage of the “One Big Beautiful Bill”, which solidified and boosted tax cuts, as well as unleashed billions in Federal dollars across various industries.

Private stimulus, meanwhile, is occurring through massive AI-linked capital expenditures from major tech companies such as META, MSFT, AMZN, ORCL, and others (remember, these mega-cap tech firms could spend more than $750 billion on AI infrastructure in 2027).

The Fed Meeting June 2026: The Federal Reserve left the Fed Funds rate unchanged in a 3.50%-3.75% range at the most recent meeting, as expected. The dot-plot median forecast increased by 1/8 of a point this year and by 1/4 of a point in both ’27 and ’28. The longer-run median declined from 3.125% to 3.063%. Notably, there are only 18 dots (historically have been 19) in the dot plot, except for 2028, which has just 17, suggesting someone had no 2028 estimate and Kevin Warsh declined to submit any estimates at all. What stood out to markets was that 9 of the 18 officials who submitted a forecast now see a rate hike in the remaining six months of the year, whereas 8 officials anticipate no change.

Bull Markets Last Longer than Investors Think: It’s likely too early to cleverly call a market top, stating that the bull market is over. In fact, looking at the 11 bull markets since World War II, the average one lasts more than five years. Not only that, the current bull market is up a very impressive 120% since October ‘22 – which sounds like a lot – but in the context of historical rallies (the avg. bull market is +191%), perspective may state that the bull market is younger than many would think.

The Fed Under Kevin Warsh: The adage is Don’t Fight the Fed. Investors should expand that in the Warsh era: Don’t Fight the New Fed Either. The tools may be slightly different, and the communication style is dramatically different, but the underlying mandate of price stability in service of long-term economic growth will not change. And that mandate, executed with competence, has historically been bullish for risk assets.

Moving Forward, Investors Need to Remain Optimistic: As long as earnings are growing, which they are, and as long as both monetary and fiscal policy are on the market’s side, the burden of proof will remain with the bears. We are still in a bull market – don’t fight it – but that doesn’t mean chase it or sell if there is weakness. It appears that the market is entering a period where it can see a moderation of the hard economic data, but not enough to warrant a recession. Meanwhile, forward-looking sentiment data should continue to improve as economic tail risks diminish and expansionary fiscal policy is on the horizon. This, combined with ongoing AI-driven investment and innovation, should continue to support risk assets once we move beyond the current geopolitical tensions.

A Different Ending: As the market continues to evolve, there are always some core principles that should be the foundation of one’s mental game:

-

- At the end of the day, the pursuit of perfection is an ultimate, pressurized failure mindset – it’s one that will eat every investor alive if they continue to chase it. Everybody wants to be the hero because they care and they want to win. But success doesn’t live in that realm.

-

- Neither does comparison. Comparison is the thief of joy. If one continues to compare oneself, they’ll remain joyless.

S&P 500 EPS: ’27 (Exp.) EPS = $392.99 (+15.8%). ’26 (Exp.) EPS = $339.29 (+23.6%). ’25 (Exp.) EPS = $274.54 (+12.0%). ‘24 EPS = $245.16 (+11.5%).

Valuations: S&P 500 Fwd. P/E (NTM): 20.6x, NASDAQ: 23.5x, EAFE: 15.9x, EM: 11.3x, R1V: 17.6x, and R1G: 24.4x. *

*Source: Bloomberg and FactSet, Data as of 06/30/26

Disclosures

Aptus Capital Advisors, LLC is a Registered Investment Advisor (RIA) registered with the Securities and Exchange Commission and is headquartered in Fairhope, Alabama. Registration does not imply a certain level of skill or training. For more information about our firm, or to receive a copy of our disclosure Form ADV and Privacy Policy call (251) 517-7198 or contact us here. Information presented on this site is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy.

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 11.2 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 4.6 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security’s U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities.

The Dow Jones Industrial Average® (The Dow®), is a price-weighted measure of 30 U.S. blue-chip companies. The index covers all industries except transportation and utilities.

The MSCI EAFE Index is an equity index which captures large and mid-cap representation across 21 Developed Markets countries*around the world, excluding the US and Canada. With 902 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 Emerging Markets (EM) countries*. With 1,387 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Investment-grade Bond (or High-grade Bond) are believed to have a lower risk of default and receive higher ratings by the credit rating agencies. These bonds tend to be issued at lower yields than less creditworthy bonds.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

Nasdaq-100® includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. This includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities, and collateralized mortgage-backed securities. ACA-2607-8.