I’m a big believer that in this market, whatever narrative you go looking for, you’ll find it. It’s very rare to find data that is always one-sided and not conflicting. And that’s the exact scenario that we are currently in – there’s a lot of data being released and processed, but also a lot of complexity to the data and the collection itself that can make even the most convicted investors a skeptic. At Aptus, we’ve preached patience and not allowing yourself to make knee-jerk reactions off of single data points. And today is no different.

Though it should be recognized that we’ve continued to witness an economy that doesn’t have as much momentum as it did one year ago, making it likely that we’ll (again) have to tap monetary policy as a life raft at some point in the future. This is not a message that is meant to scare investors, but a friendly reminder that the name of the game has very much changed since the inception of fiscal powers during the Great Financial Crisis.

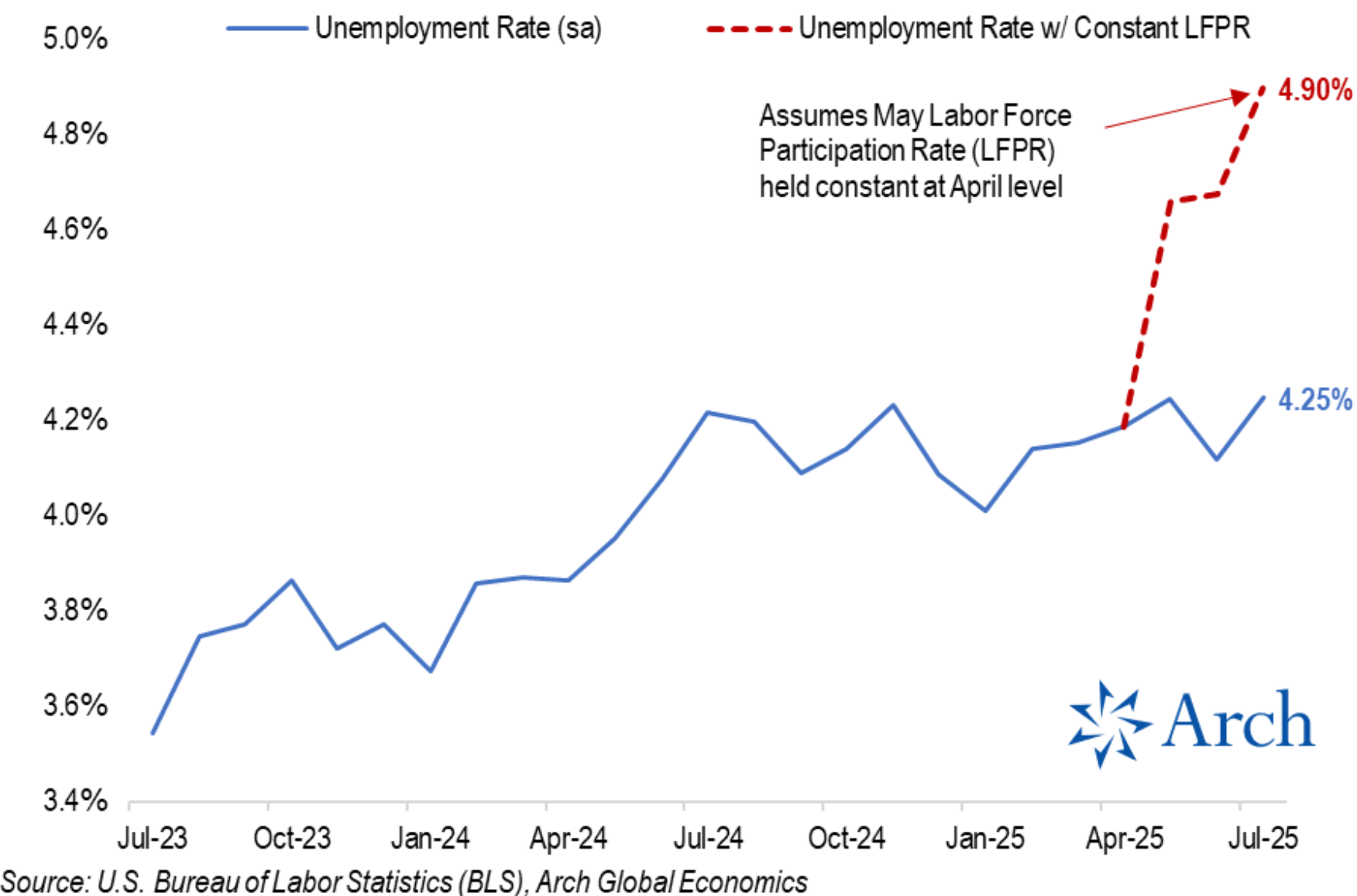

And we’re simply starting to see that in the data point this AM: the July jobs report was the weakest since the pandemic lockdowns. Forget the -31k miss between the 104k consensus and the 73k print. The two-month downward revision was a whopping -258k! The unemployment rate rose to 4.2% despite another drop in the labor force. There is pretty clearly a labor shortage in the US, but the ranks of the unemployed rose by 221k.

Brace for a Tweetstorm about Jay “Too-Late” Powell in reaction. But you won’t be hearing that from me.

Let’s take this in stride and look at everything that this market had to digest this week (without a whole lot of volatility might I add – until today): Thursday was an eventful day for macro, as markets digested Powell’s hawkish press conference the day prior, the Court of Appeals for the Federal Circuit heard oral arguments on IEEPA tariffs, Trump delivered the final letters on IEEPA reciprocal tariff rates, the White House issued new drug price control threats, incremental news flowed on secondary sanctions, QRA, and the liquidity drain continued…oh, and earnings season. And today’s data, just creates more increased complexity for the Fed.

The most important thing I can say, given the slew of client messages and emails this AM, we are not past the point of no return; we’re simply 2.5% off all-time market highs.

Lastly, if anyone would like thoughts on individual securities and their respective earnings report, please give me a holler.

Let’s begin.

A Musing of Musings

If you’ve been on one of our quarterly calls in the past month, many of you know that I’m a rational optimist and believe that it’s hard not to own risk assets right now. Said differently, I’d be a buyer of pullbacks. But, as stated above, let’s talk through the increased complexities in this market, because we’re getting it from multiple angles – hence, why this is a musing of musings.

Fed Jargon & GDP

Many will likely question my graphic for this segment, but hear me out: It’s all about growth. Growth, not inflation, matters more. If growth falters, the pass-through of tariffs becomes a moot point. If growth continues, so will wage growth and consumer spending. Powell recognizes this but is not convinced that growth is going to falter, stating that market performance and excess liquidity in the system (created by both monetary and fiscal policy) are driving the overall economy.

The dissents (Bowman and Waller), alongside Bessent and Trump, believe that growth has already started to falter and could be troublesome if the Federal Funds Target Rate stays where it is. Perhaps unspoken is that tariffs are a tax that slows the economy, and Washington, D.C., needs Fed policy on its side, or there could be some short-term damage.

Personally, I do believe that growth has started to falter, but from a high starting ground, and is likely being insulated by the amount of capex spend in the arms race of AI, specifically on the margin side of the equation. More on this below.

But this is why Jerome Powell and the FOMC’s job is so difficult right now. Which side of the argument is correct?

-

- If the Dissents + Bessent + Trump are correct on the direction of the economy and waiting for employment to falter likely means that the Fed is too late because tariffs without a rate cut will slow overall growth; or

- If Powell + Overall FOMC are correct, and growth rebounds in the second half of this year, as it did in 2023 and 2024, Powell goes into the Fed’s Hall of Fame (though, I think, will likely still be remembered standing next to President Trump in a hard hat – h/t Brad Rapking).

There is a LOT of noise in the recent data – whether it’s a data collection problem or a revision problem, which makes the data-dependent Fed’s job nearly impossible to be perfect on timing – it’s likely that the Fed will always be late if they are data dependent. Just look at GDP and Jobs as prime examples.

-

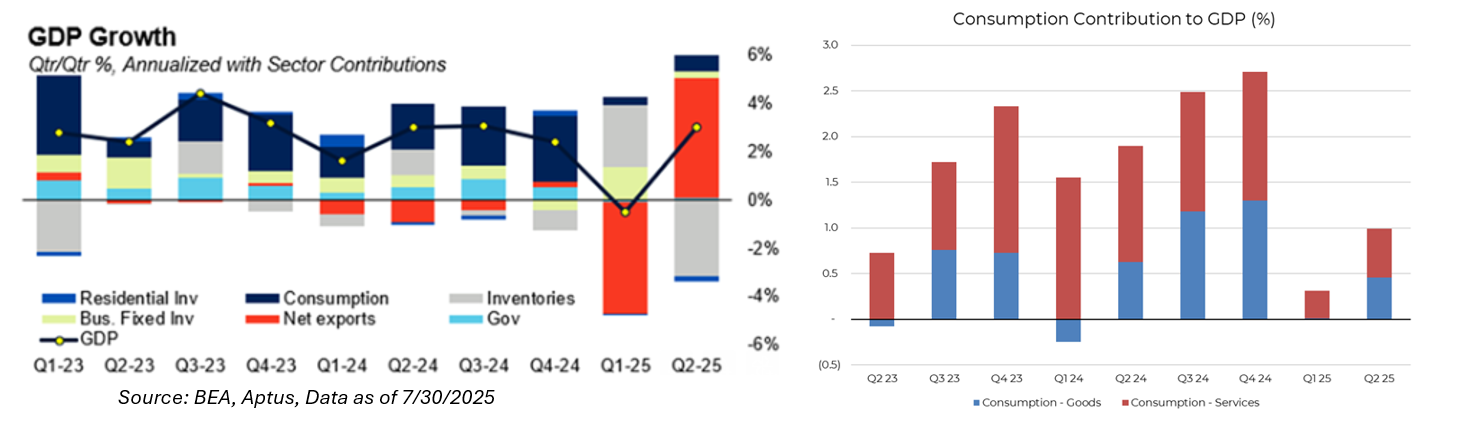

- GDP: Real GDP grew at a 3.0% rate in the second quarter after falling 0.5% in Q1. Domestic demand growth was little changed between Q1 and Q2. Real domestic final sales grew at a disappointing 1.1% rate following the disappointing 1.5% rate in the first quarter, underscoring the point that the volatility in top-line GDP reflects a measurement problem rather than true production strength or weakness. In other words, GDP did not really fall in Q1, but by the same token, it did not really jump in Q2 either. The first half average real GDP growth rate — a better way of thinking about the data, given the volatility in trade and inventories unleashed by President Trump’s tariff policies — was 1.25%.

- Jobs Report: Simply said, how can the data be trusted if, every single month, there are large revisions to the jobs data? Granted, it’s not uncommon to have revisions – though these are large. The only thing that investors can count on is that what we are seeing today will likely change.

This is an interesting chart:

Data as of 07.31.2025

Data as of 07.31.2025

When you can create your own personal narrative and when there are complexities in the data, it creates a differing of opinions at the Fed, i.e., dissents. For those that are enjoying the Summer (I’m jealous), this was the first time since 1993 that the Fed had two dissents in one meeting. History has shown that two dissents is a good leading indicator that the Fed’s next move follows the dissent, sooner than later.

This is also a great reminder that when there are periods of data, market, and emotional volatility, we believe it’s best to stick to a tried-and-true asset allocation structure where timing the market isn’t necessary. In a world where everyone wants to overtrade, in our opinion, having a proper structure like ours that takes out the necessity of proper timing–which is a feature, not a bug to our philosophy–is paramount. If you’re making investment decisions based off of the next Fed move, please let me take the other sides of your trades.

FYI, here are Bowman’s and Waller’s Dissent Rationale: Bowman’s is here, and Waller’s is here.

Earnings Season

It would be an understatement to say that this earnings season has seen a significant amount of dispersion. Let’s look at the facts: About 66% of the S&P 500 have reported earnings this quarter. So far, 74% beat on EPS, 77% beat on Sales, 61% beat on BOTH.

For context, that trio of historical averages dating back to 2000, respectively, is 65%, 59% and 46%. In its simplest form, this has been a GREAT earnings season that is besting expectations to a point where EPS growth on a year-over-year basis is now 7% (originally expected to be 4.8%). And that is why we have seen earnings beats being rewarded, rising +160bps relative to the market (that’s “normal” versus history). Misses are getting absolutely crushed, falling -810bps, on average, post-print.

My highlight has been the continued strength in the capex narrative amongst hyperscalers.

I’ve been searching for a chart like this for months now. It’s quite remarkable. And will likely continue to change in the upcoming weeks.

If I were to grade this earnings season, I’d give it a 7.9/10.0.

As always, I’ll put out a full Q2 2025 earnings recap in the next few weeks – likely after the consumer names report because… well, tariffs.

The Wildcard

The markets could see some whipsaw if the IEEPA strikes down President Trump’s tariffs. Note that this is not a problem with tariffs exactly, as Congress has indeed delegated trade authority to the executive branch over the past century, just not through IEEPA. So, the money that has been collected may need to be refunded (to US Corporations). These refunds would occur even if the US tariffs were reinstated through other legitimate avenues – such as Section 232, Section 301, the 1930s Tariff Act, etc. Food for thought – imagine that by Q4 2025 that there is ~$100B+ of cumulative tariffs refunded to US companies + monetary easing + deregulation. Investors may go from talking about the US consumer struggling to an overheating economy very quickly.

Tails Occur More Often Than Investors Think

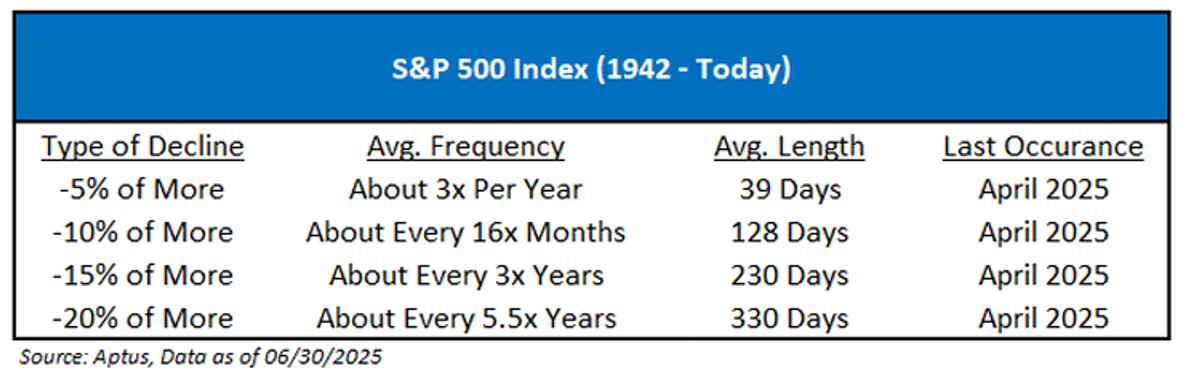

It should be reminded, that in this “new age” of the market, we are firm believers that tails will occur more often – that’s not a pessimistic sign, as right tails are positive tails – investors just need to evolve with the market to make sure that they are prepared for the continued complexities in data and environments moving forward. History tells us that 20% or greater pullbacks happen every 5.5 years on average.

Well, we are 5.5 years into the 2020s, and we’ve already witnessed three > 20% pullbacks.

-

- February19, 2020 to March 23, 2020: -33.79%;

- January 22, 2022 to October 12, 2022: -24.02%; and

- February 19, 2025 to April 8th, 2025: -21.35%

Remember, there has always been a leptokurtic distribution in returns. Moving forward, we believe that the frequency and magnitude will increase, and those who depend on a proper allocation structure instead of market timing will come out with the best and smoothest CAGRs.

We believe that our structure, more stocks, less bonds, while remaining risk neutral, is one of the few asset allocations that allows you not only to perform better in the left tail (bad), but also the right tail (good), taking out the aspect of trying to time the markets.

Remember, when it comes to an allocation, it’s Team over Players. Feel free to reach out with any questions.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2508-2.