Bye weeks are huge. The Cincinnati Bengals had a bye week this past weekend; their defense needed it, our tailgate needed it, and I needed it. But, one of the biggest questions coming out of last week is simply if the Supreme Court is going to say “bye”, “bye”, “bye” (this is not an N ‘Sync reference) to the tariffs implemented under the International Emergency Economic Powers Act (IEEPA).

During oral hearings last Wednesday, many Supreme Court Justices expressed skepticism about the government’s broad interpretation of the IEEPA. Justices questioned whether “regulate importation” in IEEPA could authorize tariffs as taxes, emphasizing that revenue-raising powers belong to Congress. The government’s inability to cite precedent for such authority further weakened its case, and the tone of the hearing shifted consensus from a 50-50 outlook to a strong expectation of invalidation.

But, before we fully start, each week feels like its own market ecosystem, and last week was no different. The NASDAQ had registered its worst week since April; along that path, there was a sense of fatigue and a loss of momentum. It’s funny to me how quickly investors can become bearish off of a 2.5% move. But when the market is pricing in above-average growth and rate hikes, we shouldn’t be surprised if there is a little turbulence at cruising altitude. And, in the words of our Head Trader, Mark Callahan, keep your seat belt on by owning hedges, and don’t get off the plane at your connection in Chicago when you bought a ticket from New York to Los Angeles.

Let’s dig into the ramifications within the markets.

Furloughing the Tariffs

It hasn’t been a secret to market participants that there is a chance that many of the tariffs initiated earlier in the year will be nullified. The oral argument from last week made it a higher probability that the current administration is going to have to walk back and potentially return a lot of the recent tariff revenue. The basis of the Supreme Court’s argument stems from the Chevron deference. Basically, the new standard, emerging from the Supreme Court over the past year, requires Congress to write regulations and executive agencies to enforce them, as stipulated in the Constitution. The Supreme Court yesterday appeared to be leaning toward a similar take on tariffs.

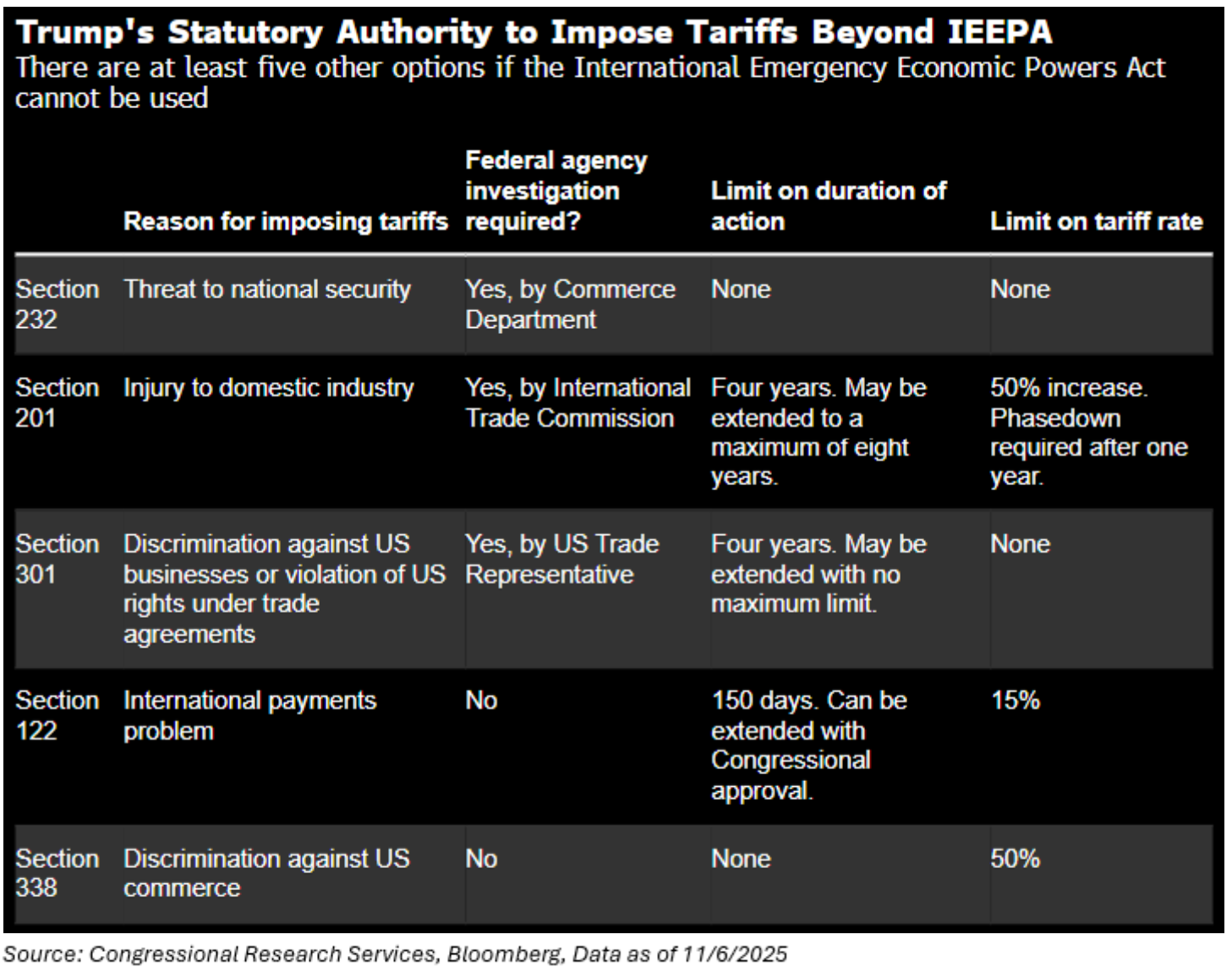

Tariffs won’t end right away, even if the court overturns them, or more accurately, upholds the lower court ruling against them, because the White House can use other laws to justify them. The White House is currently relying on the 1977 International Emergency Economic Powers Act, but there are plenty of other laws on the books allowing the President to impose tariffs, including the never used Section 338 rule passed in 1930, which allows tariffs on countries discriminating against US commerce, which is pretty much the root of President Trump’s decision to impose tariffs in the first place.

Another solution, though unlikely, would be for Congress to incorporate these tariffs into the budget. However, this is not possible during a government shutdown (this part may be stale by the time you’re reading this), and it would need to be included in a budget omnibus bill, as there is no realistic chance that 60 senators would vote to permanently enact the President’s signature policy. Still, it remains an option.

But let’s talk about what is more important: The implications of the market, because I’m not a court nerd.

The likely market reaction to the Supreme Court overturning the tariffs is this: A short-term positive, but a longer-term term could be viewed as more mixed. The removal of tariffs is positive for corporate profits, so we should see a knee-jerk rally in stocks; however, we don’t see the removal of the IEEPA tariffs as a complete bullish game-changer. Why?

-

- Uncertainty Will Continue: Markets are in love with certainty. This entire process may need to start all over. Even if the tariffs get shot down, the administration will utilize other methods to enact tariffs (sections 232 and 338), though this direction will be more onerous. Yet, these methods will also likely be challenged by the lower courts (again). Markets crave certainty, and this will unlikely provide any relief, as it may be a mild headwind on many U.S. corporations that will have to operate in a perennially uncertain trade environment, and over time, it is reasonable that this uncertainty does restrain investment decisions by those companies, possibly hurting profits and overall economic activity.

-

- From a Treasury Perspective: The “One, Big, Beautiful Bill” (OBBB) relied on tariff revenue to keep the deficit under control. If that tariff revenue is substantially reduced, it will cause a deterioration in the U.S. fiscal situation that could put more sustainable upward pressure on Treasury yields. The debt bears have been reasonably silenced this year with the additional $200B+ in tariff revenues. This could change that.

Said simply, while there may be a short-term rally in stocks off the Supreme Court ruling, the decision may inject uncertainty back into global trade, and prolonged uncertainty is the enemy of long-term economic growth.

Personally, I think that the ramifications will be greater on the rates side of the picture frame than equities, given the deficit scenario. Overturning the tariffs would end the pricing pressures associated with them, but would also mean a loss of trillions in revenue over the next decade. This significantly increases the Treasury issuances, especially as the OBBB depended on these revenues.

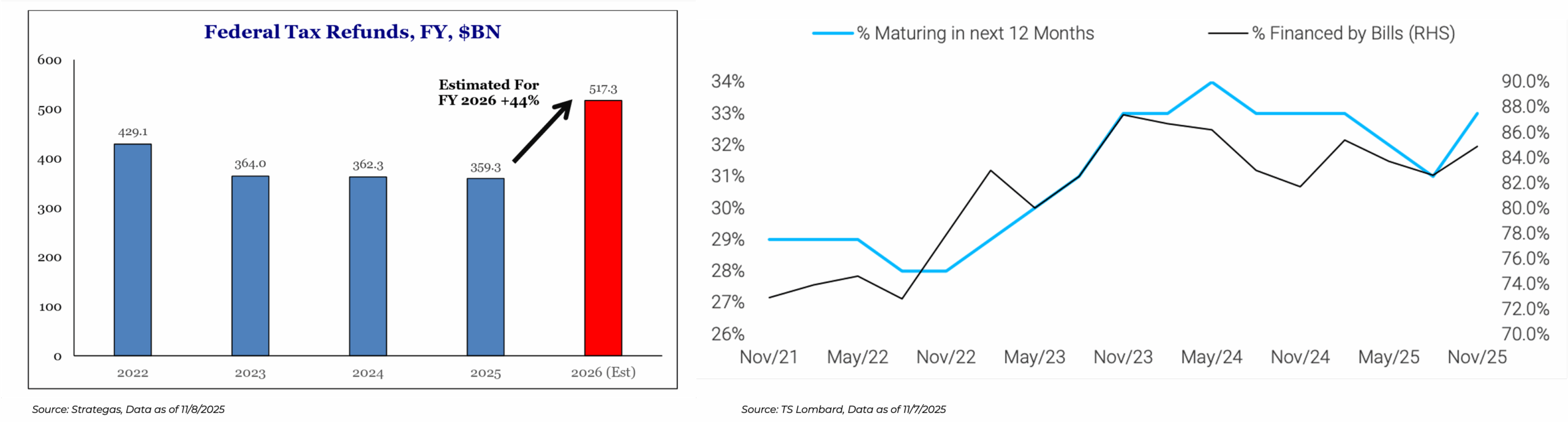

Looking at the chart below, the one on the left shows the increase that consumers will be receiving from a Federal level perspective in 2026. No surprise; there’s a substantial jump given the OBBB tax benefits. In the meantime, the Treasury will be using the Fed’s bill-buying policy to continue to rely on bills to finance the deficit (chart on the right). Nearly 85% of the Q4 financing will come from bills, up from 82.6% in Q3. This also jumps the percentage of Treasury debt maturing in the next 12 months to 33% from 31% in Q3.

Conclusion

Major decisions argued in the fall rarely conclude in December. At the same time, the parties have requested the Court to move quickly, which could accelerate the process into early next year. It looks more and more likely that these tariffs will get contested, and the market is going to have to digest uncertainty. Though I do feel comfortable saying that it likely won’t create the same level of equity volatility witnessed earlier in the year. I think the main takeaway should be that this could be another prime case study where investors may need to think differently about fixed income moving forward. If the deficit continues to increase, the only way to fund the gap is through treasury issuances, i.e., a likelihood of higher rates.

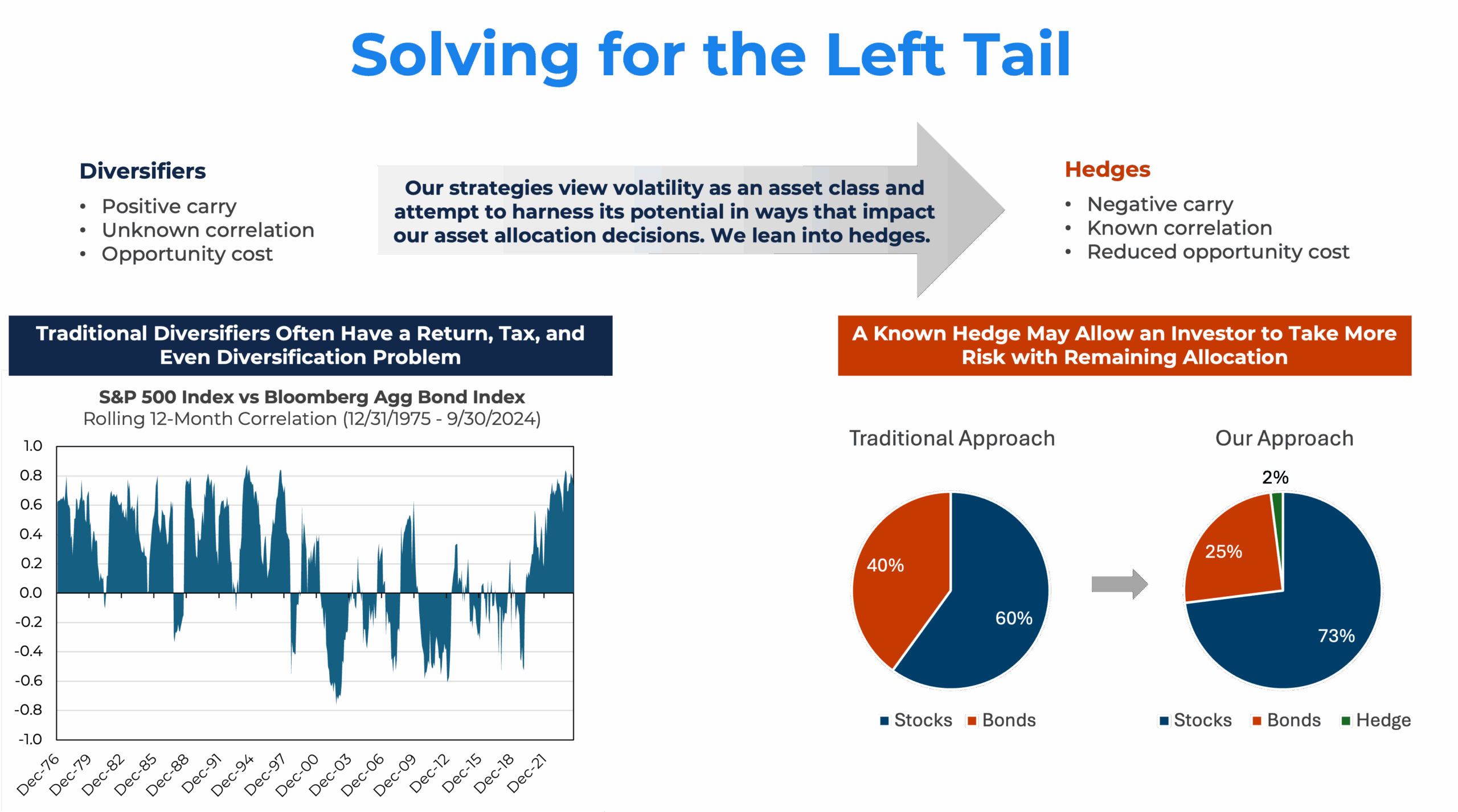

Given investor focus on downside protection, I think we need to review the diversifiers versus hedges argument (h/t JD). Read here.

Source: Aptus as of 11.11.2025

Source: Aptus as of 11.11.2025

Please reach out if you have any questions on this topic.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2511-12.