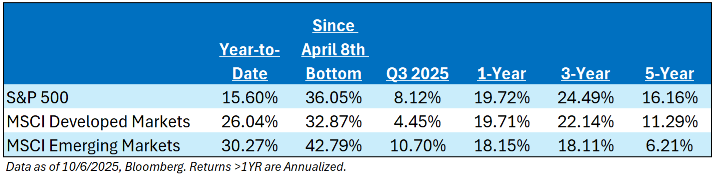

Before I start, I’ve continued to receive a lot of questions regarding the U.S. v. International debate. One of the main rules of Wall Street is that attitude follows performance… and performance abroad has been quite good lately.

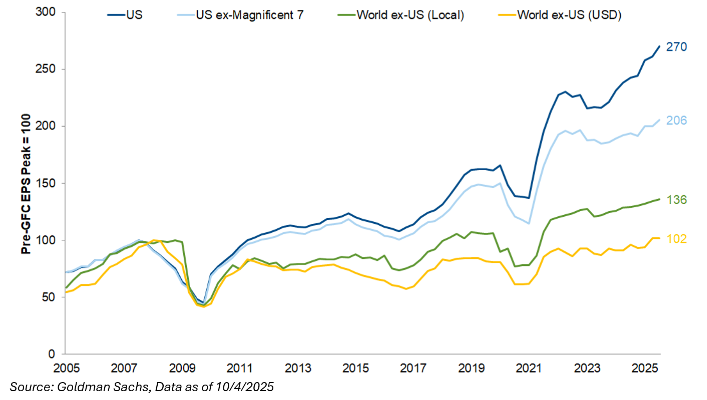

Our team has heard comments that if you strip out the Magnificent Seven, International stocks have likely grown just as fast as Domestic stocks – Wrong. In fact, earnings growth of the S&P 493 has been better, considerably better, than the rest of the world (irrespective of currency and virtually irrespective of sector). Obviously, horse races can be very sensitive to starting points, but the punch line wouldn’t change if we started the clock say, five or ten years ago.

Let’s begin.

The Government Shutdown and the Implications for the Market

If you don’t want to read any more today, just read the following line: “Keep the Government Shutdown Out of Your Portfolio”. The Government is like an 8th-grade student writing a book report; it will be completed at 11:59 PM the day it is due, or it will be completed shortly thereafter with a parental note. Either way, it’s going to get done.

Here is the most impactful point that we can make: Yes, the government shut down for the first time since 2018 but the composition of what drove this shutdown is completely different. There are two kinds of government shutdowns:

1. It can be triggered by the debt ceiling, in which case the government cannot borrow to fund operations.

2. It can be triggered by a failure to pass appropriations, in which case the non-essential parts of government without appropriations are shut.

Thankfully, this shutdown was not triggered by the debt ceiling, which means we don’t think default is a threat. That’s a huge positive for the market. Think 2013 shutdown (h/t PH). The War Department, Homeland Security, and the Treasury have been funded and will remain open and operational. In addition, parts of the government taking in revenue can remain open as long as the revenue is sufficient to cover operating costs.

From a market standpoint, the biggest impact will come from delayed economic data. Important Federal agencies such as the Bureau of Labor Statistics will not produce economic data (i.e., last Friday’s NFP Report was delayed) and while this isn’t a disruption in the short term, it could be in the weeks ahead. I say that because while the Fed dots showed two more rate cuts in 2025, that remains an uncertain proposition. That means important labor market data, which is the Fed’s primary concern on the economy, will be delayed.

If the shutdown were to continue until the Fed’s Oct. 29 meeting (unlikely but not impossible), the central bank would have to decide whether to cut rates without access to large portions of economic data. Once the government reopens and that data becomes available, it could reveal a labor market far weaker or stronger than anticipated, adding complexity to the Fed’s judgment and, more importantly for markets, to investor expectations about its next moves.

Why can’t the Senate easily pass a continuing resolution? Congressional Democrats watched President Trump steamroll policy for the last eight months and had little leverage to stop him. But government funding is one area where the Democrats have leverage. This is because Government funding requires 60 votes in the Senate, and Republicans hold just 53 seats. Democrats are going to use those votes as leverage, which is what I think ultimately led the US government into a shutdown. It’s really all come down to the enhanced tax credits for the Affordable Care Act (ACA) that expire at the end of 2025, and Democrats are willing to shut down the government to get those credits extended. In my opinion, it’s unlikely to happen.

Government Shutdowns Don’t Materially Impact the Market or the Economy

An analysis of previous shutdowns shows that, on average, markets continue to perform during government shutdowns, with S&P 500, MidCap 400, and Small Cap 600 all historically generating performance of >3% during these time periods.

Note that there have only been 5 instances of shutdowns, and performance is heavily skewed by the late 2018/early 2019 funding gap, which coincided with a meaningful Fed pivot from hawkish to dovish and subsequent equity rally. Overall equity index performance has been positive in most funding gaps, suggesting little evidence that a funding gap is a rational risk to equity performance (at least historically!)

Onward and upward.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2510-12.