The #1 question that I’ve been getting: Why is the S&P 500 Rallying?

As I’ve said, simply put, there’s a profitability boom.

-

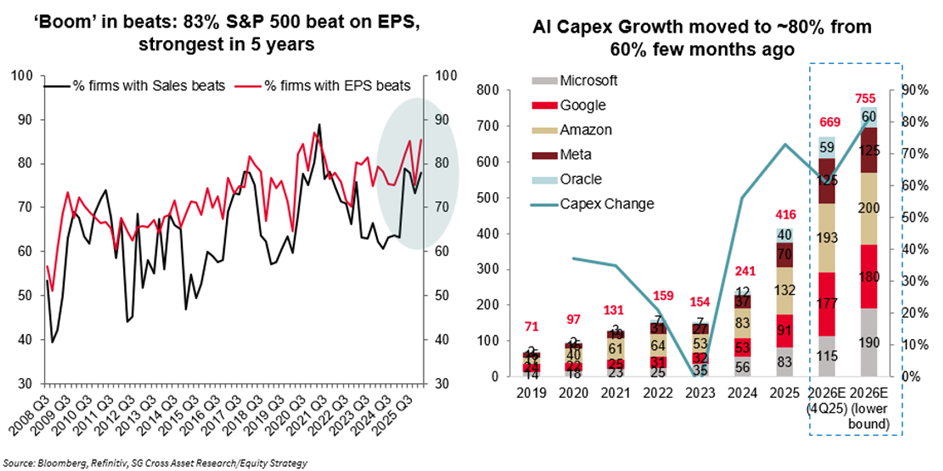

- “Boom” in EPS beats: 85% of S&P 500 firms beating EPS – the best hit rate in 5 years;

-

- “Boom” in Margins: 64% of sectors have seen margin expansion over the past three months;

-

- “Boom” in Growth: 73% of sectors are now expected to post double-digit EPS growth;

-

- “Boom” in Momentum: Forward EPS expectations are up by 8%, Revenues up by 4%;

-

- “Booming” AI demand: Hyperscalers saw EPS and revenue beats.

‘Nough said.

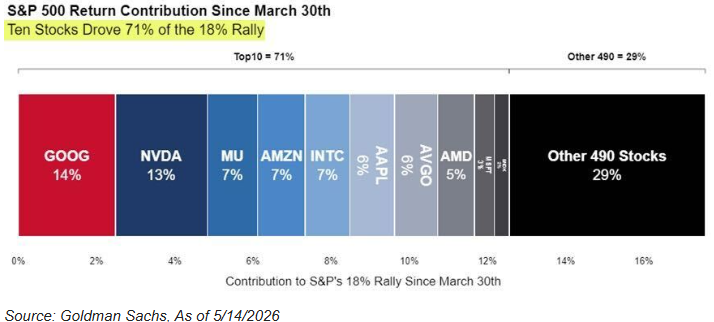

This is my favorite chart of the week:

Q1 2026 Earnings Recap

This past earnings season (hopefully) silenced the naysayers because growth was everywhere. It was the strongest earnings season since 2021 and the first time in four years that all 11 GICS sectors are showing positive revenue growth. Let’s start with a recap:

-

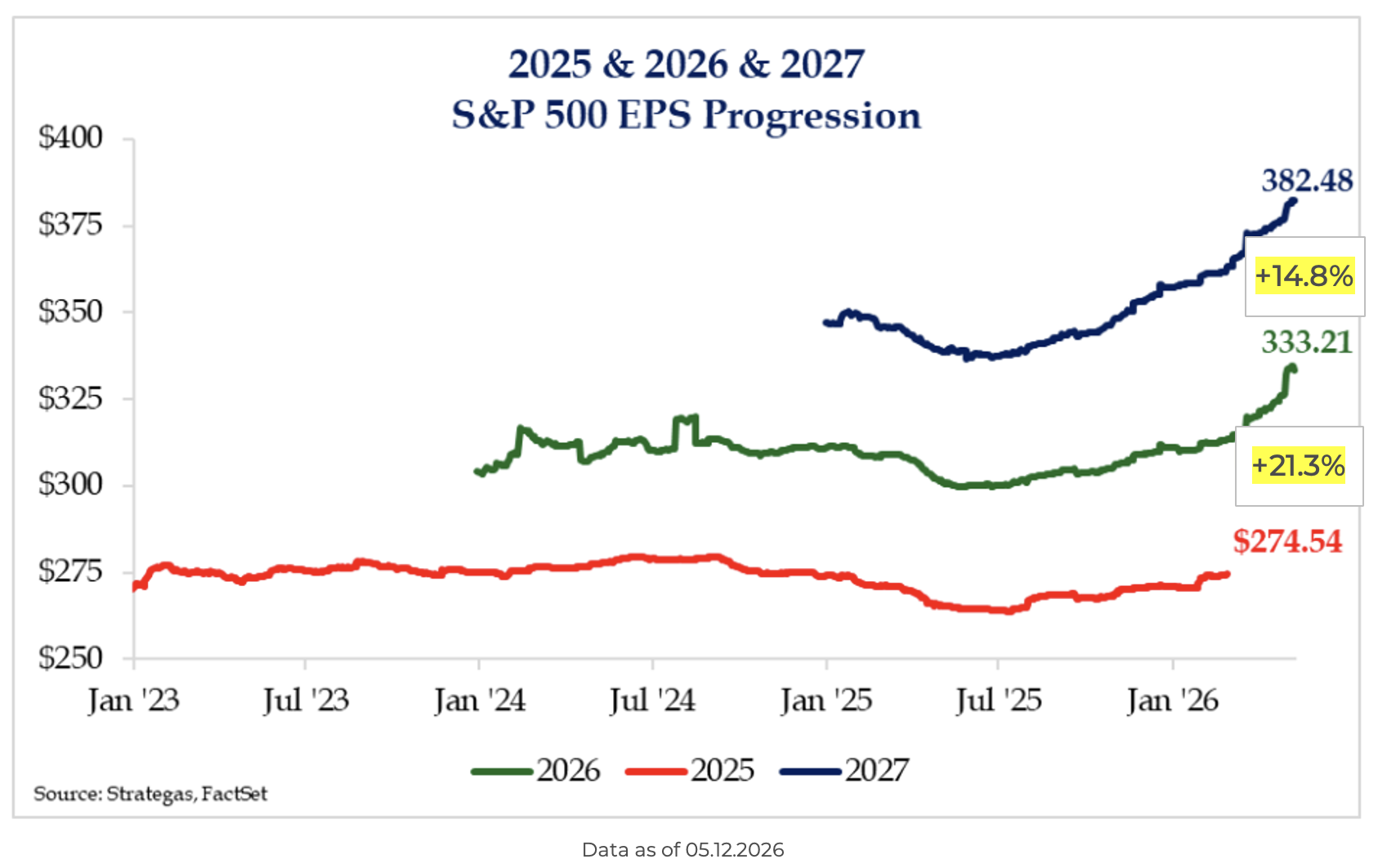

- Corporate earnings estimates are performing significantly better than the historical norm. While analysts typically cut expectations by 1% to 3% each quarter, the current season has seen the S&P 500 estimates rise by nearly 4%, with MidCaps up 1% and Small Caps holding steady.

-

- Nearly every sector has had positive earnings revisions since April 1 (beginning of earnings season), with only utilities and staples slightly lower. Although driven by energy and tech, the breadth of better-than-typical earnings revisions is noteworthy.

-

- The breadth of positive EPS revisions over the past three months has been mostly positive since July 2025, an exceptionally broad positive trend, which highlights the increasing broad economic impact of AI spending, the OBBBA, and likely the recovery of cyclical industries.

-

- Large, mid, and small cap indices are on pace now for 15%+ year-over-year (“YoY”) earnings growth, which is generally typical only in early stages of economic recoveries; however, in this case, we believe it is consistent with a Fed willing to let the nominal economy “run hot” so far.

Data as of 05.14.2026

Data as of 05.14.2026

So why was earnings season so strong?

Growth is being propelled by a mix of structural and cyclical tailwinds: tax perks, a tightening labor market, and AI finally hitting the bottom line. We’re also seeing a boost from 2025’s delayed capital projects, a shift toward rebuilding inventories, and a six-year streak of aggressive spending by high-income earners despite rising commodity costs.

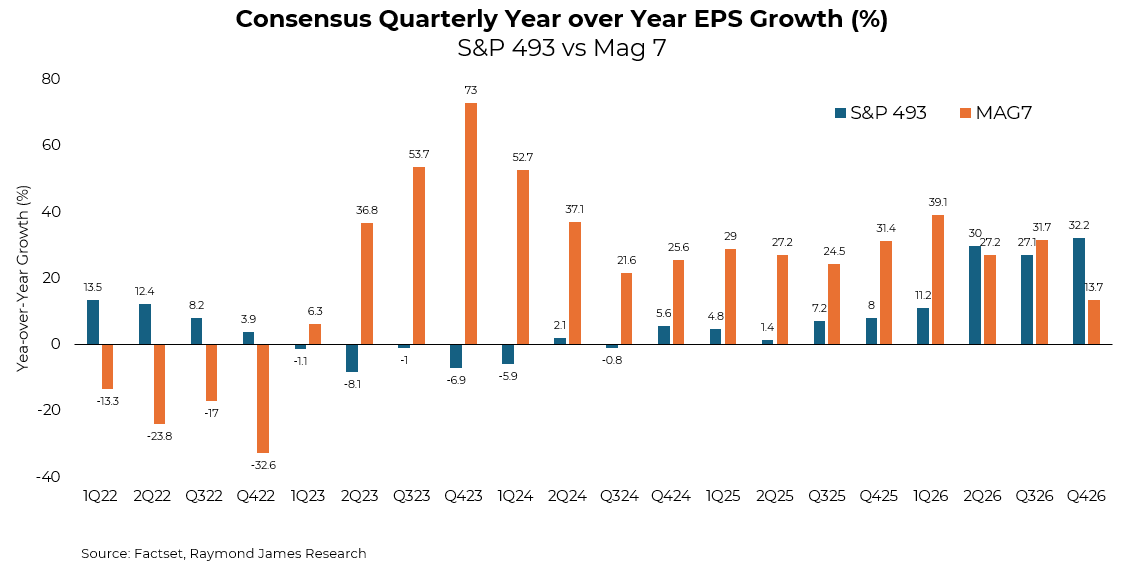

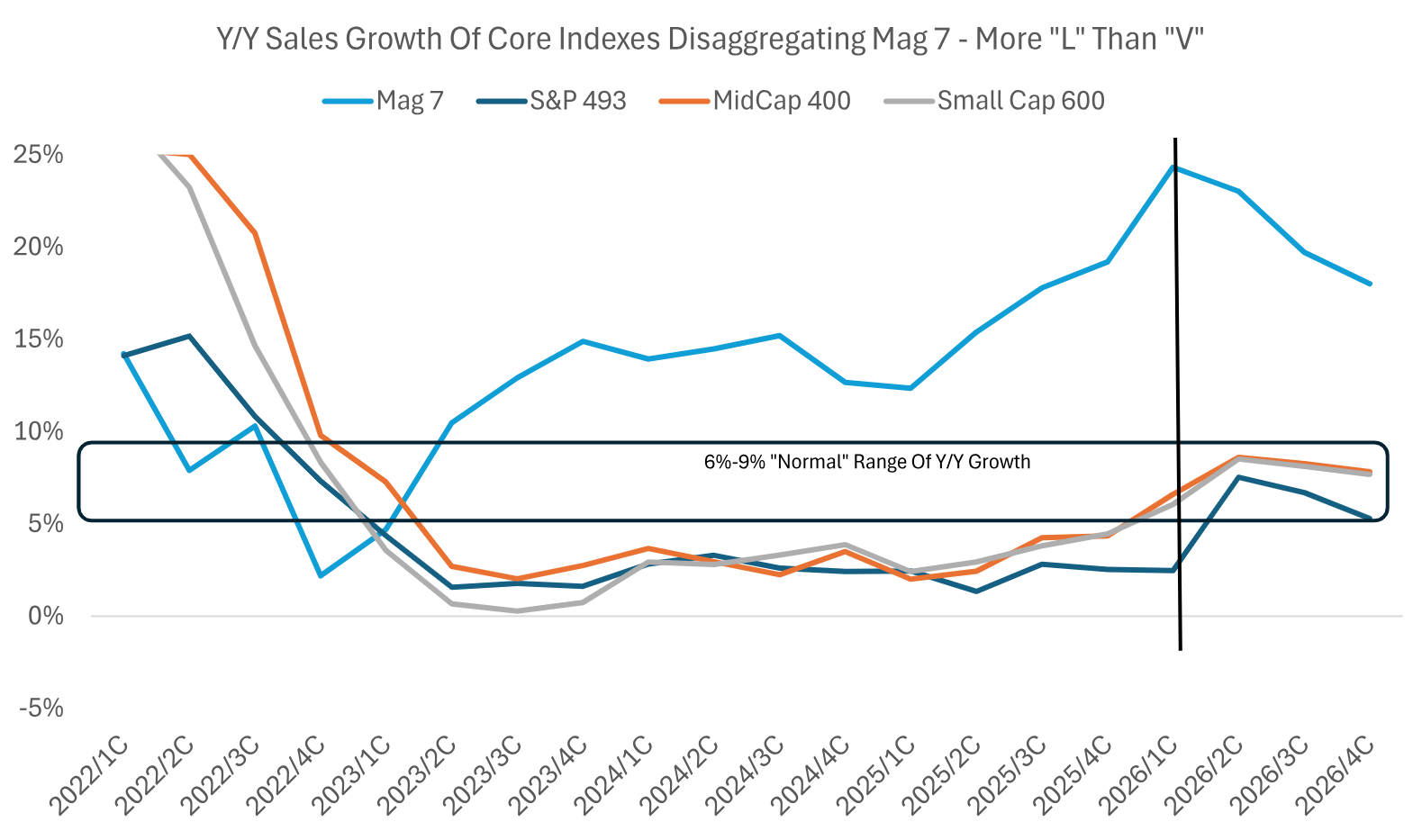

The Magnificent 7 (“Mag 7”) is currently outperforming expectations with accelerating sales, though a deceleration is projected for late 2026. Meanwhile, for the first time in four years, the rest of the market has stabilized, returning to the high-single-digit revenue growth typical of the pre-2022 era.

Source: Raymond James as of 05.14.2026

Source: Raymond James as of 05.14.2026

AI investment is shifting corporate strategy from share buybacks to aggressive capex. Hyperscalers are now funneling 100% of their cash flow into infrastructure, with Mag 7 group buybacks already down 64%. We forecast this trend to continue through 2026, with S&P 500 capex growth (+33%) significantly overshadowing buybacks (+3%) before growth likely begins to decelerate in 2027. We wonder what the ramifications will be for EPS.

Data as of 05.14.2026

Data as of 05.14.2026

While many of our clients fear we’re reliving the 2000 dot-com bubble, the data tells a different story. Unlike a true bubble driven by hype, today’s price growth is supported by a 13% increase in earnings, while the NTM P/E has actually contracted by 5% this year.

Essentially, the market is rising because companies are more profitable, not because valuations are getting stretched. Between these fundamentals and the geopolitical caution surrounding the Iran War, the market appears disciplined rather than overextended.

As always, please reach out if you would like any commentary on any company’s earnings report.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2605-16.