Personally, I feel like tariffs have already started to take a back seat to: 1) Q2 2025 S&P 500 Earnings (i.e., resiliency of corporate America), and 2) Labor Markets / Non-Farm Payrolls (i.e., when labor markets are strong, so is consumer spending). I believe this because the market is starting to recognize the playing field for tariffs. It was the U.K. and Vietnam (ex. China) who had the lowest and highest tariff rates, respectively, on Liberation Day (April 2nd). Some of the first few trade deals announced were … the U.K. and Vietnam. The rates were 10% and 40% (with Transshipments), respectively. These will likely be the bookends for any potential trade policy.

P.S. Moving into summer, if there was a top-of-mind item that I’m currently worried about for the market (to the downside), it would be that liquidity is being drained from the market at the same time when there is fodder for increased tariffs. We saw how the Treasury General Account (“TGA”) affected rates to start the year; we’d expect the same on the other side. As always, please reach out if you have any questions on this topic.

Let’s dive in.

Q2 2025 Earnings Season Preview

Ultimately, fundamentals drive share prices, and despite the noise coming out of Washington, D.C. and concerns over potential earnings per share (“EPS”) estimate deterioration, there has been little sign of a meaningful weakening so far. With tariffs in place for nearly the entire quarter, this reporting season should offer greater visibility into their impact – this is going to be the real test for the market. However, the recent extension of the trade negotiation deadline is likely to prolong corporate uncertainty and delay decision making. That said, the passing of the tax legislation has at least removed one layer of uncertainty for businesses. I would hope that the market has the ability to beat this “lowered” bar, which could set up for increased optimism in risk assets.

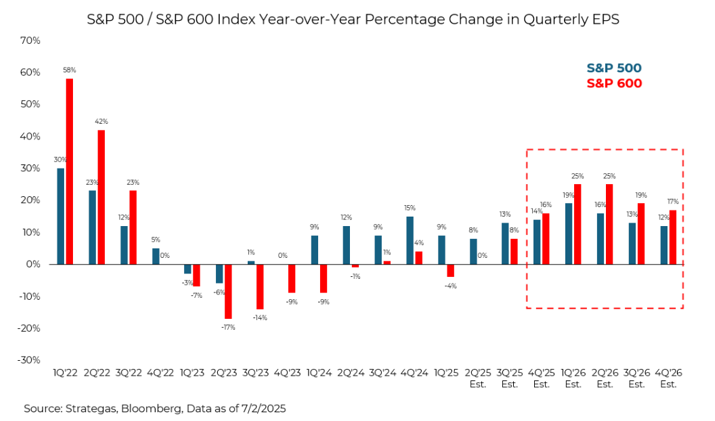

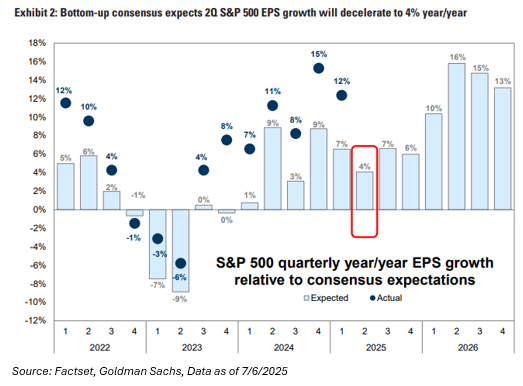

As of now, the market is expecting EPS growth of 5.8% for the quarter. This follows back-to-back quarters of EPS growth greater than 14%. From a revenue perspective, the market is expected to grow by 3.7%, remaining broadly in line with nominal GDP. Heading into Q2, these figures were much higher. For example, sales were expected to grow closer to 5%, and EPS of 11%. The largest contributor to the decline in EPS expectations is from margin compression, i.e., more companies not passing on increased tariff costs to consumers just yet.

From their peak, EPS expectations are lower by: 2025: -5.55% and 2026: -6.13%

In my opinion, this should not worry investors. It’s very normal for EPS expectations to decline as a year progresses.

Now, in my very rudimentary way of thinking, since I went to University of Kentucky, it doesn’t make sense to me that at the start of the year, revenue was supposed to grow +5% and EPS +15%. With inherent operating leverage in the index, this is a 3:1 payout. Now, we’re expecting revenue growth of 3.7% and EPS growth of 5.8%. That’s a ratio of 1.6x. This means that a substantial amount of operating margin has been priced out of the benchmark, and it doesn’t appear that it will be due to slowing Technology growth. Said another way, a lot of pricing degradation is being priced in from the remaining, more cyclical parts of the S&P 500, which means that: 1) the market is likely pricing in a very low bar for earnings (good), or 2) tariffs are widespread and corporations are eating the cost (bad).

This bodes a large question – What have we learned about tariff pass-through on the Consumer? Tariff costs can be absorbed by 3 participants: (1) U.S. Consumers, (2) US Businesses and (3) Foreign Exporters. I’ve read that many economists assumed that consumers would absorb 70% of tariffs. Let’s look at the data and see what it’s telling us.

-

- For the consumer, this hasn’t shown up in recent inflation reports.

- And for foreign exporters, investors would see this occurring by exporters lowering their export prices to the U.S., which would show up as lower import prices, which hasn’t happened either.

So, as of now, it feels like companies have been forced to swallow the cost of tariffs, which would likely represent downside risk to operating margins. Unless corporate America did a great job front-running the tariffs via inventory. This can only last so long. It’s important to understand that it can take a long time for tariff costs to show up in official data, hence why the Fed minutes this week continued to show some worry on this topic.

Let’s talk about margins. As we’ve always said, the market typically avoids significant trouble as long as operating margins remain solid. And, as of last quarter, operating margins resumed their upward trend and while they’re off their highs at 17.8%, the overall trajectory remains quite stable. If this stability remains, it would support the case for risk assets.

Here’s What I’m Focusing on in Q2 Earnings Season

Outside of profit margins for the S&P 500, I’m focusing on the resiliency of earnings within the Magnificent Seven (“Mag 7”). In more detail, the top 10 stocks account for almost 40% of the index; thus, if these stocks continue their consistent earnings stream, it may be difficult to see deterioration of index EPS relative to historical standards. And a lot of this thesis has to do with the current capital expenditure cycle (“capex”), of which there has been no sign of capex letting up just yet. One of the biggest outstanding questions for the broader technology sector is whether the mega scalers will continue to spend heavily on capex. At this point, we believe the answer is yes. The “circular capex” story at the top of the market remains intact, with large tech firms investing in AI infrastructure driving demand for semis, software, and services. We’d assume that this boom will continue in the near term. I believe that this is one of the main reasons that the S&P 500 will best the lowered bar for Q2 2025 EPS expectations, but keep an eye on it to try to recognize the duration of the capex boom.

Lastly, we’ve said this for a long time now, but when global growth becomes scarce, investors naturally seek out areas where growth remains, and the U.S. seems to be the only game in town right now. We don’t believe that U.S. exceptionalism is over by any stretch of the imagination.

Disclosures

Past performance is not indicative of future results. This material is not financial or tax advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed and all calculations may change due to changes in facts and circumstances.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2507-14.