With earnings season beginning this morning, I decided to write our Q3 2025 Earnings Preview on a flight to Omaha. And while heading to this special investment city, it’s hard to not be reminded of Warren Buffett, but many of you know my thoughts on The Oracle of Omaha. I respect the hell out of the man, but have always been annoyed by the Twitter charlatans who worship his every word in an effort to clone his ability.

Below is an excerpt from our Aptus Compounders Philosophy (email us if you’d like to view the full piece) that I think is perfectly fitting.

“Each Investor’s strategy is and likely should be different from the next person – it’s good to be different. We believe that too many investors focus on cloning others like Warren Buffett, when it’s a mistake. It’s not who they really are. There are 10,000 Elvis impersonators, and their combined income is far less than the original. Instead of cloning someone, we want to take the valuable lessons and nuggets that we obtained from studying the greats, and apply it to our own process, experiences and personality.”

Remember, it’s OK to be different; It’s OK to be yourself. No one does Warren Buffett better than Warren, and no one does you better than yourself.

To touch more on a topic recently discussed in the Aptus Quarterly Newsletter, given the recent news of Circularity regarding OpenAI and (NVDA, ORCL, AMD, AVGO, etc.), I read something that mimics my overall thoughts on this topic.

But simply said, there’s more of a bubble of people calling for a bubble… than an actual bubbles (H/T Brad Rapking for that comment).

Is AI a Bubble?

-

- Yes; prices have increased at a pace that many don’t believe are sustainable and there are likely some aspects of speculative excess in the market. Just look at the “Style” of stocks that have outperformed from the recent April low. But, zooming out, since the low in March 2020, the Nasdaq is up about 200%. In contrast, during the tech bubble of the early 2000s, the index rose closer to 400%.

- Yes; the market is more concentrated today than ever before. Technology is at its ATH of weighting at 35%. The top 10 stocks are >40% of the index. But, as you’ll see on slide 17 in our Quarterly Update Deck, there’s a lot of business diversification at these Mega-Cap Companies.

-

- One of my favorite quotes from the quarter is that Mega-Cap stock’s size is no longer the enemy of growth; it is their engine. In fact, there have been many periods of high concentration in the past that have NOT ended with a bubble bursting.

-

- Yes; the history of bubbles is the aggregate value of the companies involved in a newfound innovation exceeds the future cash flows. However, price appreciation to this point has been principally driven by sustained, superior earnings growth.

-

- Furthermore, the dominant companies of today have particularly strong balance sheets in which the AI investments are financed by free-cash-flow.

- Valuation; Current levels are not yet at levels that are typically seen at the height of past bubbles. The average P/E value of the Mag. 7 (Ex. TSLA) is ~30x forward. In 2022, these valuations were closer to 40x; and 50x during the Dot.Com bubble.

All in all, I’m not saying that we are not heading towards a bubble. We’re likely to have some type of air pocket in the future, but that’s not a bubble. And I’m not saying that all the above makes me fully comfortable with the market; that’s why we efficiently own hedges that protect against this exact worry. The above is a very reasonable framework of rationality.

The bottom line is that we don’t know the hour or the day the market peak will occur, but having a plan to prepare for what you can’t control makes sense.

But hey, that rational narrative doesn’t sell clicks or views.

Onward.

Q3 2025 Earnings Season Preview

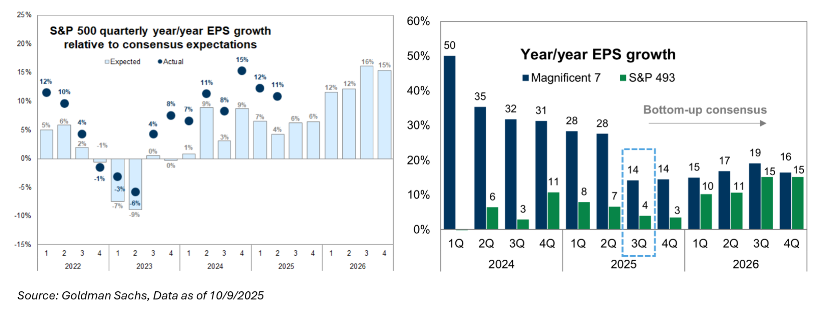

The market has become accustomed to beating analysts’ earnings expectations over the past few quarters, and that’s a narrative that will likely persist in Q3, as the bar appears to continue to be artificially low.

Let’s look at the numbers:

-

- Consensus year-over-year (“YoY”) expectations for EPS growth at the index level (S&P 500) currently sits at 6%. For reference, last quarter witnessed revenue growth of 6%;

- Then, the market is pricing in YoY revenue growth of 4%, which is somewhat difficult for me to reconcile with nominal GDP growing 4.6% and 4.7% (expected) in Q2 and Q3, respectively, and;

- Lastly, the consensus Magnificent 7 EPS growth rate of 14% in Q3 represents a slowdown to half the pace of realized earnings growth in Q1 and Q2. Anecdotally, I have only witnessed the momentum for AI Capex increase in the past quarter.

All of these seem a bit low, right? Personally, I think the market continues to not realize the impact that operating leverage has on earnings, and it’s one of the main reasons that we continue to beat very pessimistic expectations, handily, I may add. That being said, I do need to recognize that EPS growth should indeed decelerate modestly relative to last quarter due to a smaller FX tailwind and higher tariff payments.

Maybe we’re set up for another beat-and-raise type of quarter, or maybe the market has started to price in this recurring theme, given the recent positive move in markets.

One thing that has surprised me this quarter – which is very atypical – is that the market has witnessed intra-quarter positive EPS revisions.

-

- S&P 500 earnings have been revised higher by 2%;

- S&P 493 estimates have been revised higher by 1%.

This contrasts with the typical historical pattern of modest downward revisions to year-ahead EPS estimates. This is only the fifth time since 2003 that Q3 has seen this phenomenon; usually, Q3 sees EPS expectations decline by ~3% intra-quarter. With little recent change to the outlook for tariffs or the economy, we expect much more modest revisions this quarter.

Things That I’m Looking at During This Quarter’s Earnings Season

Earnings Revisions and How the Market Rewards Them: While earnings results this quarter should broadly beat consensus estimates, I would not be surprised if there’s not a slew of widespread upward estimate revisions that characterized last quarter’s earnings season. The upward revisions during the Q2 season largely reflected corporate guidance and analyst estimates moving from the elevated tariff rates that had been announced just ahead of the Q2 reporting season, and the associated economic uncertainty, to the lower rates and improved growth outlook in place this summer.

AI Capex Trends: AI-related capex spending has been a key topic of client conversations in recent weeks. Hyperscaler commentary this quarter regarding AI demand and capex spending will be critical to the durability of the AI trade. Consensus estimates imply hyperscaler capex growth will remain robust this quarter at 75% YoY but slow sharply to 42% in Q4 and to roughly 20% in 2026. However, AI capex spending has consistently exceeded bottom-up estimates during the last several quarters.

Lastly, if you’ve had a quarterly investment call with us in October, one thing that I’ve pointed out is that Small Caps are now expected to eclipse Large Cap EPS growth in Q4 of this year. At the same time, the average stock isn’t expected to hit this crossroads in 2026. The expectation of lower yields is likely the largest contributing factor to this, but also one of the likely reasons why Small Caps outperformed large caps in Q3, while the average stock trailed the larger brethren.

Disclosures

Past performance is not indicative of future results. This material is not financial or tax advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed and all calculations may change due to changes in facts and circumstances.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2510-17.