Here’s the big story in my mind: the S&P 500 EPS forecasts for 2026 and 2027 are climbing, but this optimistic trend might be a bit of a “smoke screen.” Most of those gains are concentrated in the Energy sector thanks to higher oil prices, which actually hides the growing pressure on other industries from an input cost perspective. While the energy giants are winning right now, the hidden costs for everyone else likely won’t hit the books until later, when some companies are forced to lower their future expectations – likely to occur during the next earnings season. We don’t have any way to measure what this damage could be, but just remember this: Growth is already kicking above its historical averages, allowing the market to take a slight hit to growth. So, this dynamic is not a reason to turn bearish.

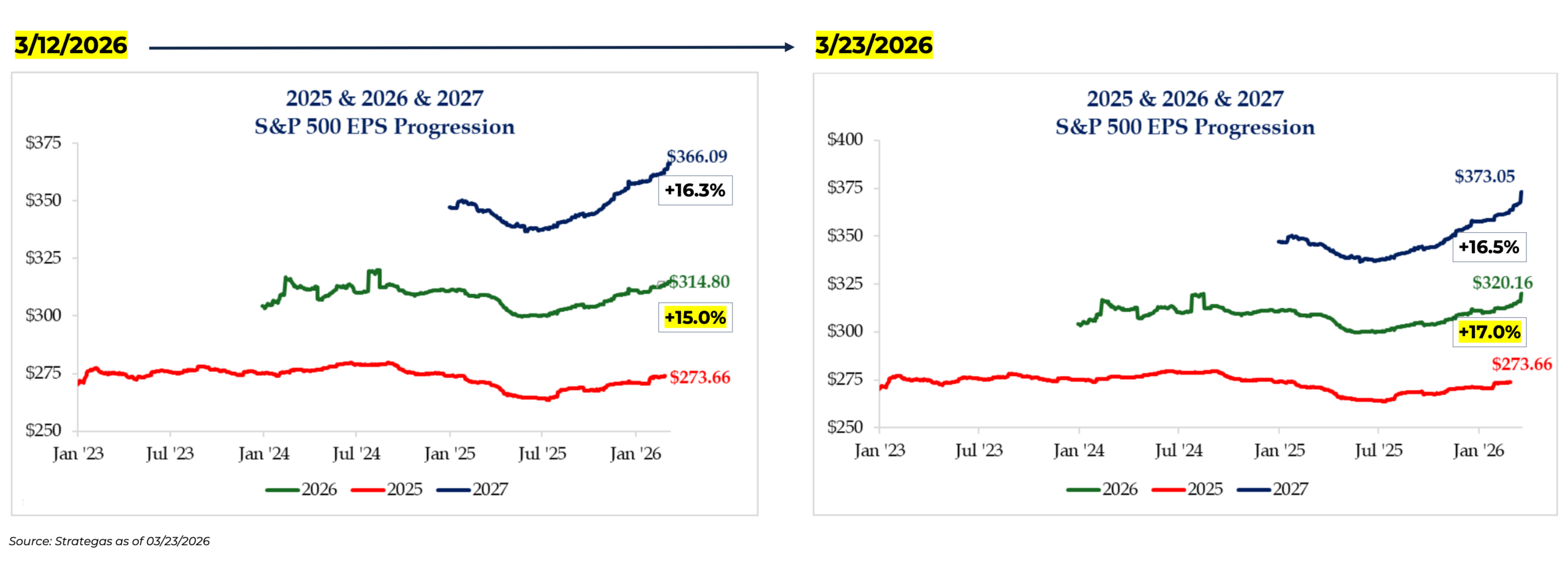

For example, earnings growth is expected to be 17.0% in 2026, up from 15.0% just 11 days ago:

Even if 15.0% is the correct number, a slight hit to growth isn’t going to cause this market to crater, in my opinion. Remember, the historical growth rate for the S&P 500 is ~+9%. Lest it be said, the clear-and-present danger for stocks in the very immediate timeframe is the ongoing impingement in the flow of oil and gas – but don’t let that fully change an optimistic approach to the market, as many longer-term themes remain healthy and intact.

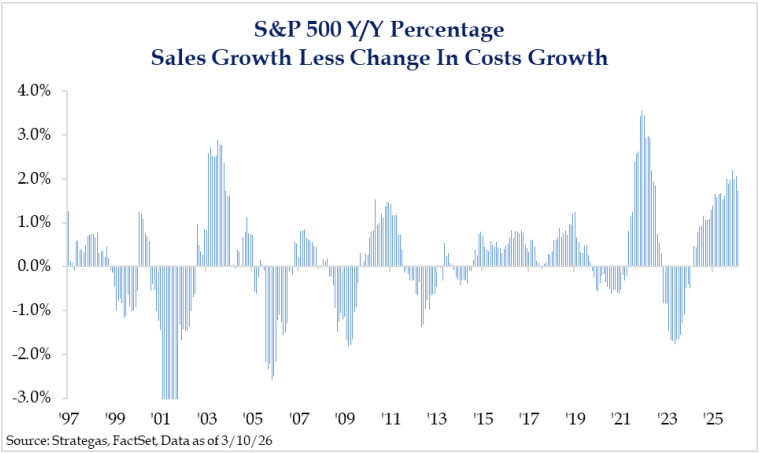

I think Strategas had a great chart that laid this narrative out perfectly. Sales growth still exceeds cost growth. This is important for margins. While the spread still stands at 1.7% today, it narrowed in February, even before the Iran war began. A spread this wide is more typically seen immediately following a recession, so its persistence mid-cycle is somewhat unusual. A further narrowing would not surprise us, but as long as the spread remains positive, it is difficult to become too negative on markets for an extended period of time.

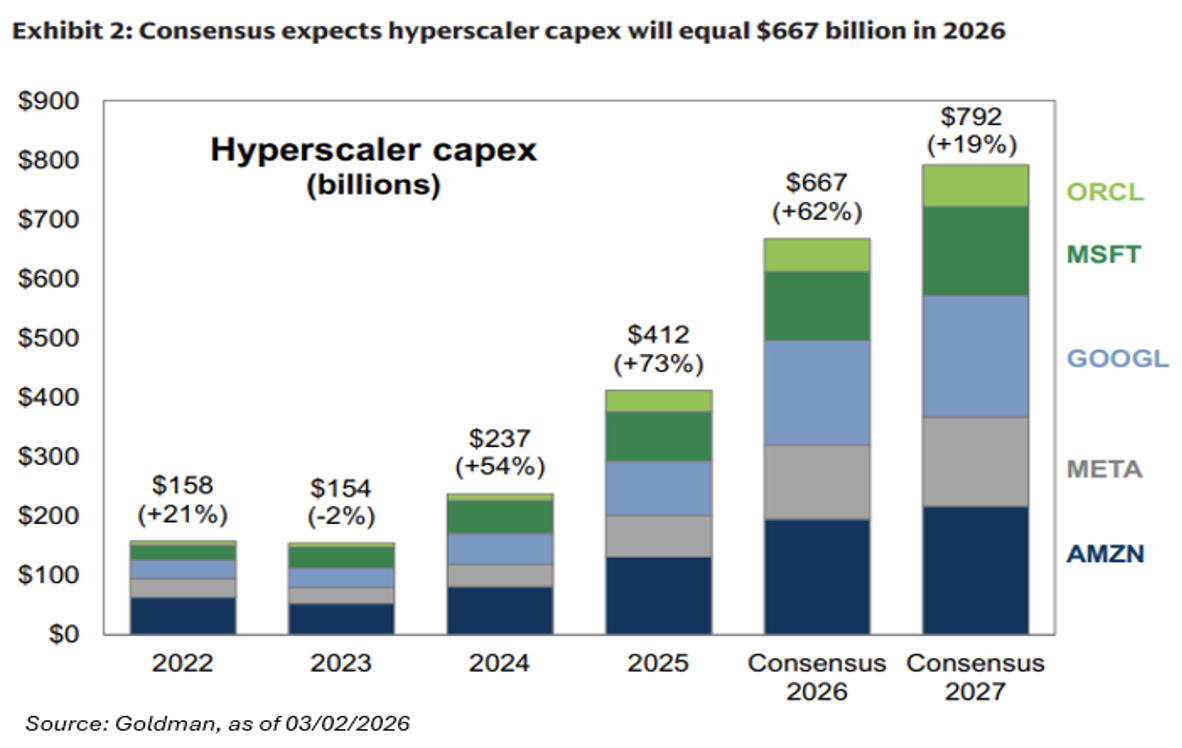

Unsurprisingly, growth expectations for the Magnificent Seven (“Mag7”) remain robust. The hyperscalers are still blowing the roof off capex estimates – something we’ve personally expected.

Consider this: At the start of January, consensus was for $540B of spending in 2026; now it’s already up to $667B (and the goal posts for 2027 have moved from $630B to $792B).

Despite generally lower stock prices across the AI sector (the only Mag7 + AVGO that is beating the S&P 500 this year is GOOGL, outperforming the S&P 500 by only ~1%), it’s not easy to disassociate the capex storyline from the absence of EPS upgrades, but the acceleration of spend continues to invite hard questions on returns and efficacy. But remember, in a winner-take-most construct, it’s not obvious whether these companies have much of a choice but to spend. This level of spending equals 2.2% of GDP.

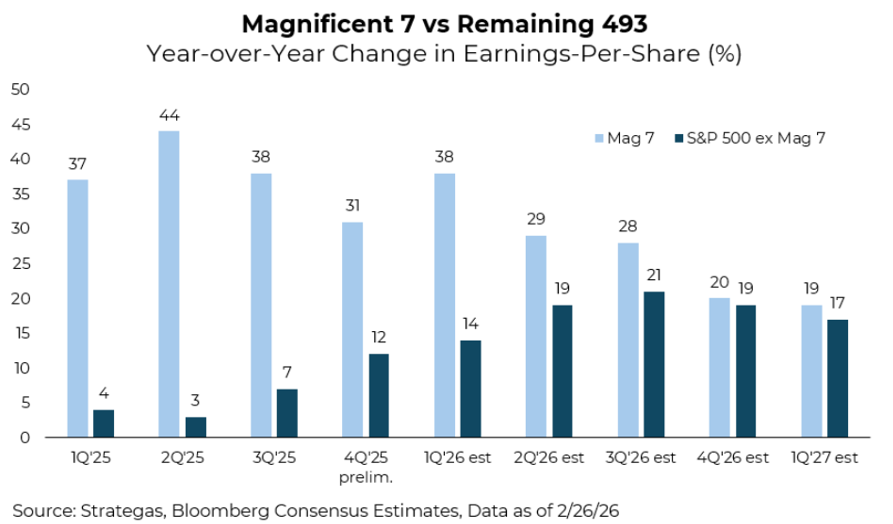

Seven AI-exposed stocks accounted for half of S&P 500 EPS growth in 2025 and should contribute a similarly large share in 2026. While the median S&P 500 company grew earnings by a healthy +9% in 2025, the seven stocks (AMZN, AVGO, GOOGL, META, MSFT, MU, NVDA) collectively grew earnings by 32% last year. Consensus estimates suggest NVDA alone will account for 24% of S&P 500 EPS growth in 2026. I know many readers will consider this a bearish signal, but this has been the story of the last few years… and has it been bearish for markets? No. As I just said, the median S&P 500 company grew EPS at 9%, which is right in line with historical averages.

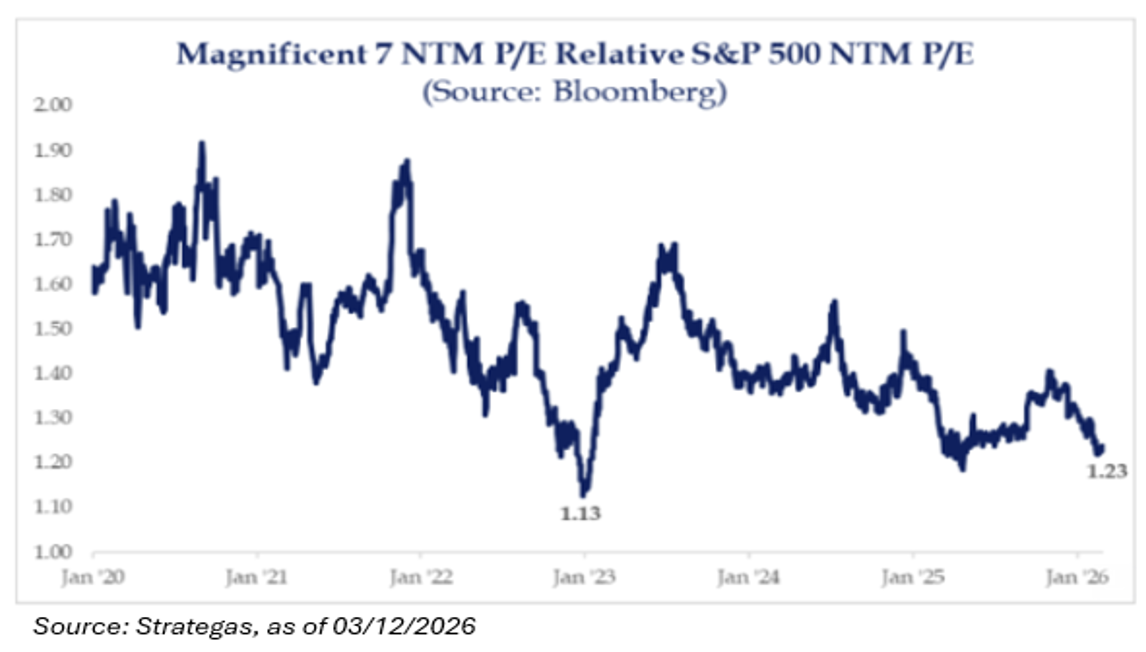

As the chart above shows, these mega-cap companies are expected to continue outperforming the broader index in terms of growth. The broadening trade depends on a meaningful improvement in fundamentals across the remaining 493 companies. Yet, these mega-cap companies are trading at the most attractive levels since 2020, but investors remain cautious here. The primary concern appears to be the scale of capital expenditures, particularly now that some is finally being funded through debt.

Moving forward, I believe the focus should be entirely on AI productivity gains. The share of firms quantifying productivity gains from AI has been limited so far, but should increase in 2026. Investors are searching for long-term “winners” that will use AI to become more productive, but very few companies have quantified the impact on earnings. We expect more companies to quantify productivity gains in the coming quarters. However, translating productivity gains to sustainable earnings tailwinds will depend on a company’s ability to retain incremental profits rather than pass them on via lower prices and higher wages.

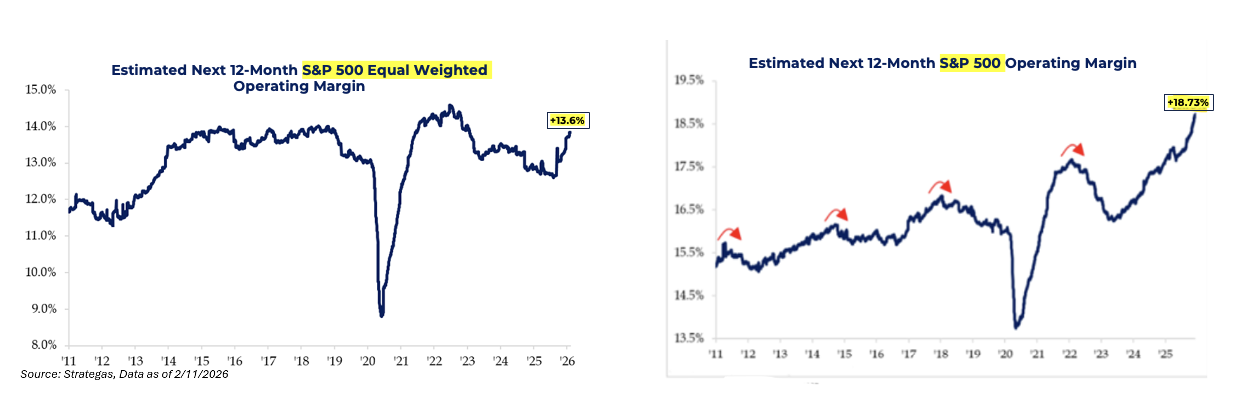

I haven’t seen an updated version of this chart lately, but market operating margins likely remain true:

All-in-all, the S&P’s modest 4% dip suggests a surprising level of resilience. When a primary asset holds its ground despite negative headlines, it prompts a few theories: the market might be complacent, betting on a short-lived conflict, or signaling that the US economy can actually weather $100+ oil. It might even be pricing in a more stable long-term geopolitical landscape.

While I won’t claim to have a crystal ball for geopolitics, a few things are clear:

The Bull Trend: The primary upward trend is still holding, but the stakes rise every day.

The Energy Factor: The longer supply remains tight, the more the growth-versus-inflation trade-off deteriorates.

Global Impact: If this pressure continues, the US will feel the squeeze – but other developed markets and their central banks face a much steeper uphill battle.

Reach out if you’d like any of our internally created individual stock earnings reports.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2603-21.