Last week was supposed to be a quiet, short week; it was anything but. Cue Friday, February 20th:

1) SCOTUS Tariff decision (deemed illegal),

2) Core PCE (higher than expected), and

3) First look at Q4 GDP (lower than expected).

But, before we dive in, below is one of my favorite paragraphs that I’ve read over the past few weeks. Many long-term readers know that I don’t like (or enjoy) talking about the fancy terminology that colleges and professors utilize – things like Neo-liberalism, Bayesian, or Keynesian economics. I simply go by the David-esian economics of follow what the market is telling us, because, in my opinion, the market is what the market is and that’s all there is to it.

“Wall Street’s Keynesian Blindness to Trump’s Supply‑Side Revolution. Wall Street has the story wrong. The US is growing at 4%, powered by a capex boom and an explicit attempt to rebuild the country’s productive base. Yet the dominant narrative still treats this as a tired, late-cycle surge destined to end in recession and a weaker dollar. That’s why money is rushing into utilities and staples at 50x earnings, while AI and software are being dumped indiscriminately. What investors have missed is the Trump–Bessent project: to use productive capital, bank deregulation, and supply-side economics to deliver strong, non-inflationary growth. This is not another sugar‑high stimulus. It is an effort to raise potential output and shift the structure of the economy.

Look at positioning, and the verdict is obvious. The rush into gold, the historic underweight in the dollar, the wholesale rejection of AI-linked equities – all express the same view: Trump and Bessent will fail. Markets are behaving as if the only possible outcomes are inflation, crisis, or both. This is what happens when an industry dominated intellectually by Keynesians keeps reaching for the same demand‑side playbook. AI hype and Trumpian turbulence have undoubtedly exhausted investors. But fatigue is not a framework. The real question now is whether Wall Street can abandon its reflexive Keynesianism long enough to see that this may be the beginning of a new supply‑side era, not the classic late-cycle trade.” – James Thorne

These tariffs, whether one agrees with them or not, have been another great case study for following what the market is telling you. If investors had done that, they would have navigated last year’s tariff tantrum quite well. Below, we’ll try to help navigate what the market is telling us, now that SCOTUS has ruled against IEEPA and Trump has announced his alternative plan.

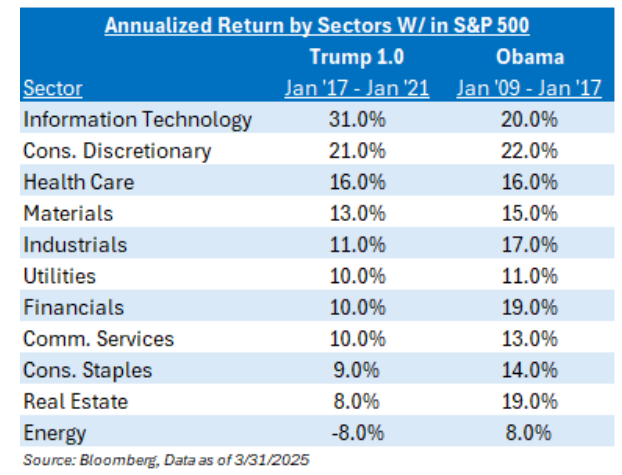

But remember one of my favorite charts from last year: Old macro wisdom states that economics (and earnings) supersede politics (and geopolitics). It always has and always will. It’s likely fair to say that Presidents Obama and Trump don’t have much overlap in their Venn diagram, yet the same parts of the market worked well under both of them, and vice versa.

Luckily, Friday’s market reaction has been quite muted; something that could not be said on April 2nd of last year.

The Nightman Cometh? Trumped by SCOTUS

It’s Always Sunny in Philadelphia is one of my favorite TV shows ever, specifically The Nightman Cometh episode that is about Charlie staging a bizarre, original rock opera where “the gang” portrays characters in a surreal battle between the Dayman and the Nightman.

In a political landscape that feels like a high-energy production of The Nightman Cometh, the administration’s tariff strategy has reimagined global trade as the ultimate “troll toll.” Much like Frank Reynolds’ iconic (and confusing) gatekeeper, these tariffs serve as a firm price of admission for any foreign goods looking to enter the American market. As the Nightman of international imports approaches the border, he’s met with a demand for payment – a bold, protectionist barrier designed to ensure that if you want to play in this market’s “soul”, you’ve got to pay the price. But, economists did not view this policy as a “Master of Karate and Friendship” for domestic manufacturing, aiming to chase away the darkness of trade deficits and usher in a “Dayman” era of American-made prosperity.

While SCOTUS did not give an opinion on that aspect (nor should they), they did rule on the legality of how the “troll toll” was collected: illegally. But, as you’ll see below, it may not all be Dayman in the future, as the Nightman has alternative ways to collect future tolls to get into this country’s “soul”.

While I recognize that this tariff strike-down story will likely be cast in a political light, in my opinion, it’s a bigger corporate earnings story. Companies will ask for (or demand) refunds, which, if they happen, will likely be done via the tax code. And also like COVID-related price spikes, it’s unlikely companies will cut their prices. It could simply just increase corporate margins. This could basically be a big win for corporate America and market participants, as both love to witness increasing margins.

I’m not surprised by the market’s muted reaction on Friday. Why? First, it fully expected this decision.

Second, the ruling doesn’t address some of the uncertainty that remains in the future. But here is what I believe are the two important things to focus on moving forward:

- Will there be refunds?

- What are the procedures for tariffs moving forward?

Let’s walk through both.

What Will Happen With the Refunds?

Friday’s decision made no reference to any tariff refunds, which may create future uncertainty in the market. In fact, Supreme Court Justice Kavanaugh was the only one to bring up refunds in his dissent. In my opinion, SCOTUS should have at least addressed the process moving forward on refunds, but it seems like they kicked the can back down to the lower courts.

As of right now, there are over 1,000 court cases at the Court of International Trade. For reference, in 2024, there were only 264 cases opened. In 2025, given the tariff debacle, this number jumped to over 1000 cases. And already this year, approximately 950 cases have been opened at the Court of International Trade. It’s quite an extensive list of companies that have filed a motion, making it clear that these companies want to create a paper trail of receipts and records to potentially have a better shot at getting a future refund.

From Trump’s perspective, it appears that he has no appetite for paying anything back. No surprise there.

Ultimately, we have no clue how long this process will take to resolve. I’ve read 6-9 months, but how does anyone have a clue? This will likely be tied up in the courts for quite some time and may ultimately get kicked back up to SCOTUS.

What are the Procedures for Tariffs Moving Forward?

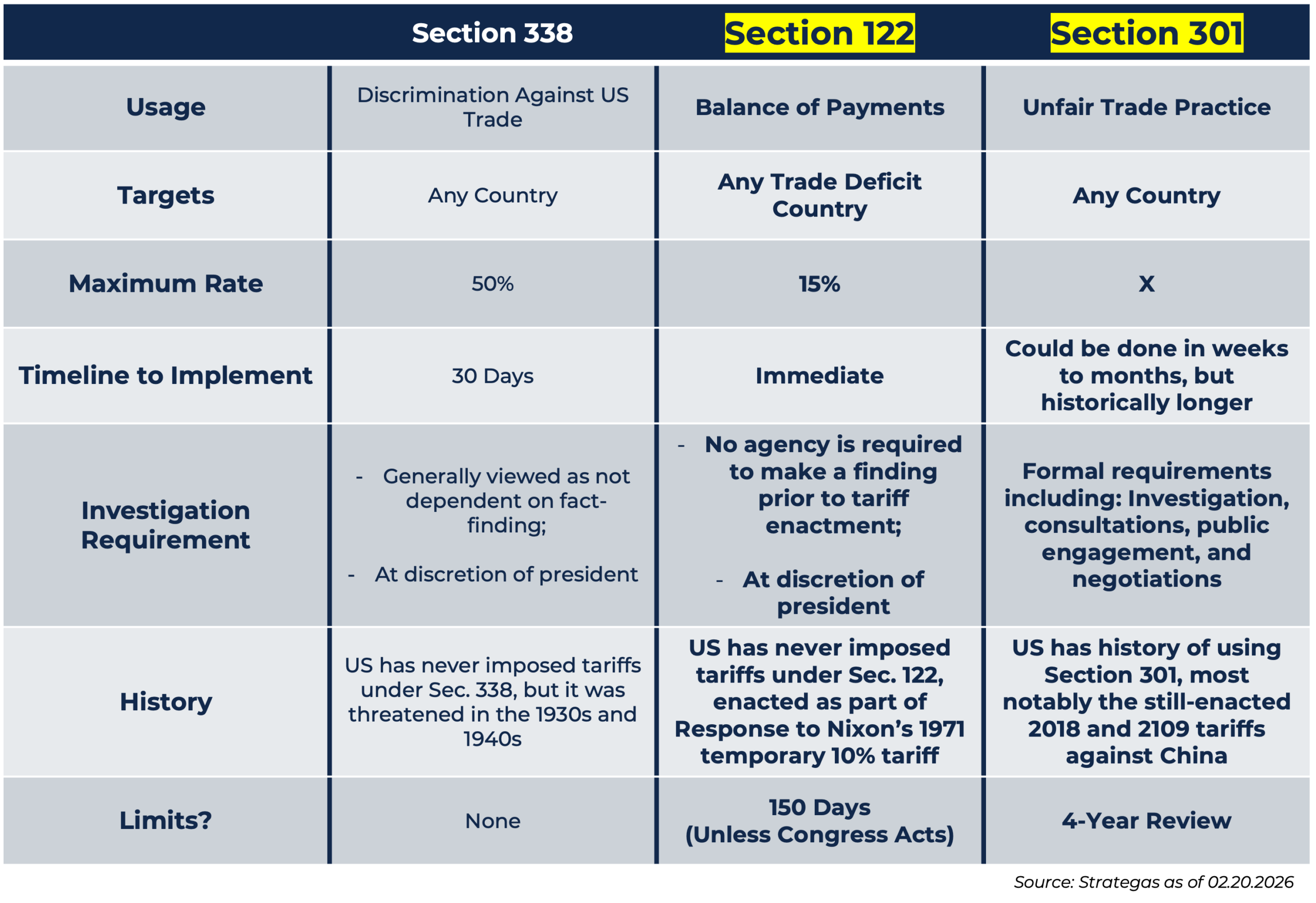

Trump telegraphed the plans for the future during his press conference on Friday. While these alternative authorities that he had to choose from come with various procedural, timing, and rate-related constraints, bringing some potential variability to rates in the interim. However, long-term, tariffs are here to stay. Potential permutations include:

Section 122 + Section 301: Use of Section 122 to impose immediate tariffs of up to 15% on trading partners with whom the U.S. maintains a trade deficit. During the 150-day time limit, the administration conducts Section 301 (country-specific) investigations; at the conclusion, the Section 301 tariffs go into effect. Section 301 does not have time limits or rate caps. This avenue would likely be more legally durable, but more procedurally complex.

Section 338: Use of a largely unused 1930s statute that allows the president to unilaterally declare tariffs to respond to “unreasonable” policies that discriminate against the commerce of the U.S., up to a maximum rate of 50%. Given the lack of precedent, it is unclear to what extent a formal investigation is required. This approach is viewed as more legally shaky/unprecedented, but would likely allow the president to move more quickly.’

So What Did Trump Do?

Not only did Trump come out nearly 2 hours after the decision, but he came out with a replacement plan, one that feels quite bullish for the market. Like the market, I believe Trump likely knew the negative outcome was imminent from SCOTUS, and he wanted to get a plan in place for the future so he could keep his negotiation leverage with many countries.

Here is what we expect to happen in the future:

Happening Now: Bring on Section 122. The U.S. will place a 10% tariff rate on all countries through Section 122, replacing the IEEPA tariffs. These tariffs can only last for 5 months.

-

-

- This means there is no 30-day waiting period, and the tariffs are immediate.

- This is below what the market expected, as Trump had the ability to go up to a 15% rate. This is significant because there are many countries that have a rate greater than 10%. For example, the EU, Japan, and India have a rate at 15%. More emerging market economies, like Vietnam, have a rate closer to 19%. It’s likely that he settled on the 10% rate for two reasons: 1) This is what Trump campaigned on, and 2) There could be some legality problems if there are variable rates amongst different countries under Section 122 (For example, the UK and Australia are at 10%, which would have been below the 15% rate creating a potential legal problem).

- This is a bullish rate because a lot of countries have a rate greater than 10%. So, it’s great for companies doing business in Europe, Asia, Japan, etc. –> It’s almost half of what many countries currently pay.

-

Happening In the Future: Bring on Section 301. While those above tariffs (Section 122) are in place, D.C. will start the Section 301 process to get greater power on tariffs. It will be a race against time, as the government performs all the research and due diligence on each individual country under Section 301. Basically, can they complete all of the paperwork for the tariff continuation before Section 122’s 5-month window expires? This will be a heavy task, but not impossible. This could become a significant market issue because it injects uncertainty regarding the direction of tariffs in the near future. It will be clunky and complicated, but will the market work through all of this?

Also (Possibly) in the Future: Trump can use Section 338 to bridge the gap if some countries take longer to complete the Section 301 diligence over the next 5 months.

What Does this Mean for China? This means nothing for China, as the U.S. already has Section 301 authority over China. This decision doesn’t impact them at all. Obviously, Trump and PM Xi will be meeting with each other in early April, and both parties have had a tendency to increase tariff rates beforehand as a show of power – this time will likely be no different.

Overall, I think the market will likely view this positively because there will be some level of tariff reduction in the short term. This 10% announcement was likely the only surprise to come out of today’s SCOTUS and Trump’s announcements.

I’ll leave you with one thing: The hardest way to get new ideas into one’s head is to get the old ideas out.

Change is not bad; it is just different. When economic regimes change, so must the assumptions that govern our thinking of the state of the economy. There’s lots of change in our economy right now: 1) Supply side economics, 2) Jobs & remote work, 3) Sticky inflation, 4) Higher LT Rates, and 5) Immigration.

Don’t deny change because it’s difficult to understand. Embrace it and see if there’s an alternative way of thinking.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2602-19.