There’s noise… so much noise.

The headlines, data, and stuff that just don’t matter bombard investors. It’s our own dang fault. The noise only exists because there’s demand for it. Investors click on the bait and even make decisions off the emotions triggered by the bait.

Our aim at Aptus is to be informed with some noise, while targeting our focus towards the things that matter. Less noise, more substance. Substance being the stuff that moves investors closer to improving financial outcomes.

C.S. Lewis had a good quote in Mere Christianity about aiming for heaven. We want to aim for our north star, too…consistent in our focus and delivery of solutions that help solve things that matter. While we cover quite a few topics, the target today is a short reminder of the core investment belief that drives our business:

Asset allocation matters most, and within that, we want to own more stocks, less bonds, and blend hedges to protect against left tails.

Bondholders = Bagholders

In investing, a bagholder describes an investor who holds onto a declining asset. Many bagholders ignore the warning signs… of which there are plenty.

Our fiat system and the accompanying debt loads are not conducive to productivity gains translating to greater purchasing power of a dollar. We will spare you the soapbox, the point is simply that our system MUST dilute the dollar’s value over time.

Speaking of distractions, remember way back when (a couple of weeks ago), cost-cutting was the initiative? DOGE, fiscal restraint, trimming excess, etc. That was all the noise. We have quickly pivoted back towards a growth-centric philosophy, one that wants to run the economy hot to stimulate demand and growth beyond the pace of our debt expansion.

Good luck with that. As investors, what matters is the recognition of all this. Let’s just play the hand we are dealt through our asset allocation. It’s no surprise to any reader of ours that our opinion in both tails is risk assets up, and bond holders as bag holders. The likely outcome of good things (growth above expectations) is risk assets higher. The likely outcome of bad things (plunge protection team enters to supply more dollars) ultimately leads to risk assets higher.

Allocate accordingly.

Here Comes the Dollar Supply

This tweet from Charlie Bilello illustrates the increase in money supply over the last few years:

You could argue that this doesn’t matter. If that’s your stance, you probably think bonds are safe, too.

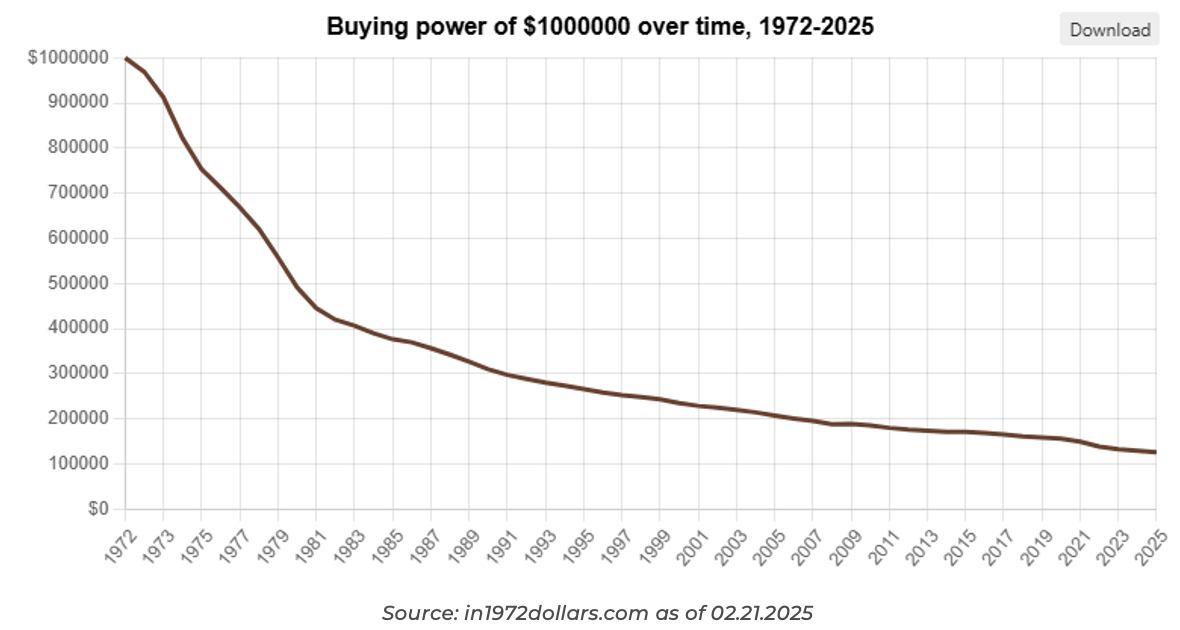

Here’s a reminder that when you hold something that can be created out of thin air, there’s a chance that thing might become worth less and less over time:

$1,000,000 today only has the purchasing power of $132,444 in 1972 dollars. Purchasing power of $1,000,000 has eroded by about 86.76% since 1972 due to inflation.

The cumulative price increase from 1972 to 2025 is 655.04%. This means that $1,000,000 in 1972 would buy the same amount of goods and services as $7,550,358.85 would buy today.

Let’s Run it Hot

We are hopeful that AI has productivity gains in store for us, to grow our way out of this debt issue. While hopeful, we will allocate dollars in a way to hedge that hope…via owning more risk assets.

We’d agree that a US default is unlikely, but the likelihood of bondholders being paid back with debased dollars is quite high. The current situation is roughly 97% public debt to GDP + 3.2% primary deficit + 3.4% effective interest rate. This means the US must grow nominal GDP at 6.6% to keep debt/GDP Stable.

The US has only grown nominal GDP at 6.6% or higher a handful of times:

-

- High Secular Inflation 1965-1985

-

- Dot-com Bubble (late 90s)

-

- Housing Bubble (mid-2000s)

-

- Everything Bubble (post-COVID)

Conclusion

Asset allocation is mission critical. If we get that right, we can get a lot of other stuff wrong and still be fine.

The backdrop is one where we are convinced that the need to own more stocks and less bonds will become increasingly apparent over time. We will continue to build solutions that help facilitate this shift and model portfolios that express this conviction.

We believe our allocations, which are a blend of risk assets with hedges, are positioned to be better in the tails. It’s the tails that carry the greatest impact towards compounding wealth through time.

If you have any questions at all, please reach out. We want to help cut through the noise. As always, thank you for your trust.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2506-18.