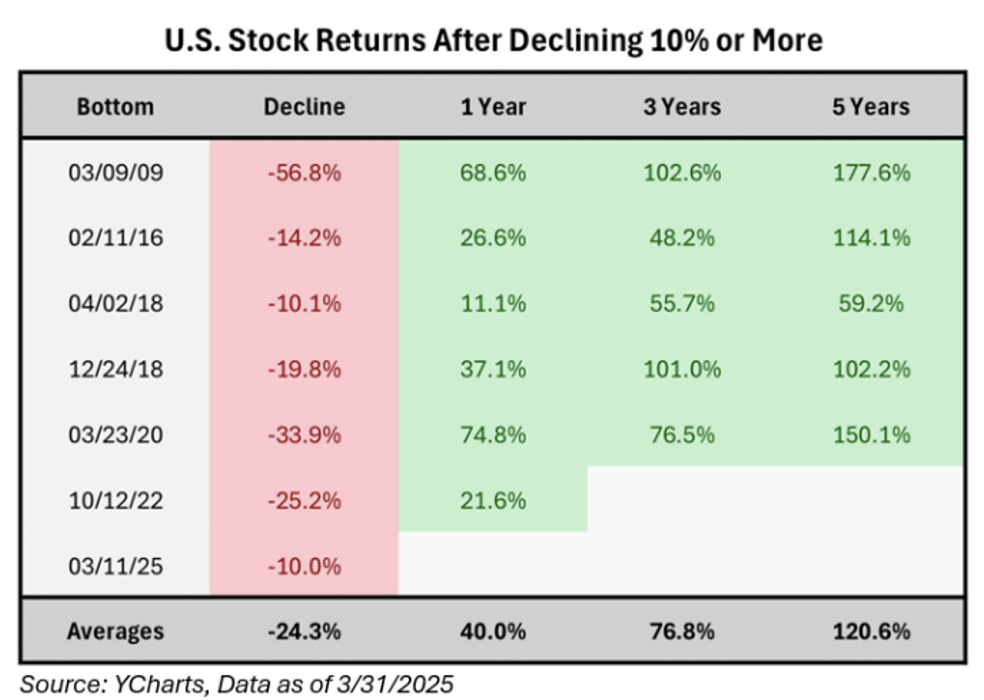

The volume of uncertainty has been turned up. The S&P 500 closed the quarter -4.28% after dropping 10% from the highs in mid-February. As Dave points out in our Q1 2025 newsletter, the most likely culprits are:

-

- Capital flows

- Expectations for slower growth

- Policy uncertainty

How should investors respond?

Own the risk and hedge the tail…that’s the foundation of our approach and in our opinion, the appropriate response. In the middle of uncertainty is a good time to talk through why that’s the case.

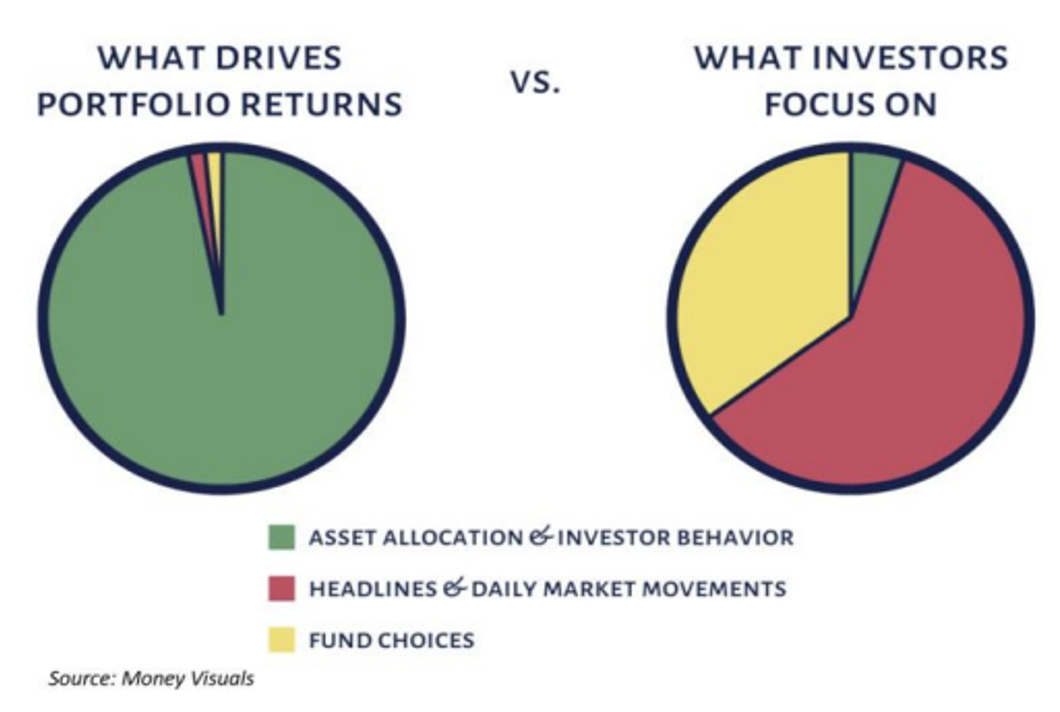

Asset Allocation Matters Most

If you break investment choices into 2 broad categories …

-

- Risk Assets – Think stocks

- ‘Safe’ Assets – Think bonds and cash. If you’ve read anything of ours, you understand why we put the term ‘safe’ in quotations

Your ability to compound (grow) your wealth is dependent on your asset allocation.

Read that last sentence one more time. Worry less about which stock you own or which fund manager you have. Worry more about being allocated properly.

The Goal is Compounded Returns

Financial plans work better with higher compounded returns. Higher compounded returns lead to higher ending terminal wealth.

Your assets grow through a multiplicative process where this period’s return is multiplied by the next etc. For example, if you earn 10% on your money one year and then another 10% the next year, your cumulative return over those two years is (1.10 x 1.10) – 1 = 21%.

Compounding being multiplicative simply means the returns build on themselves – each period’s return is stacked on the previous one.

This matters because:

Volatility Tax. We discuss this frequently. The difference in compounded vs. simple returns is a drag on returns that we want to minimize

Negative returns have more impact than positive returns. In other words, we need to avoid large losses

Don’t think linearly (simple returns)…that’s not how wealth compounds.

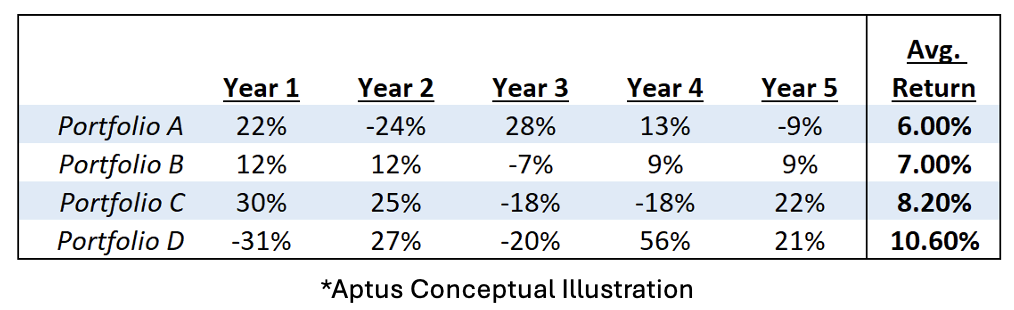

Here’s a visual using 4 hypothetical portfolios:

Most people think Portfolio D would be the best because its average (simple) is the highest.

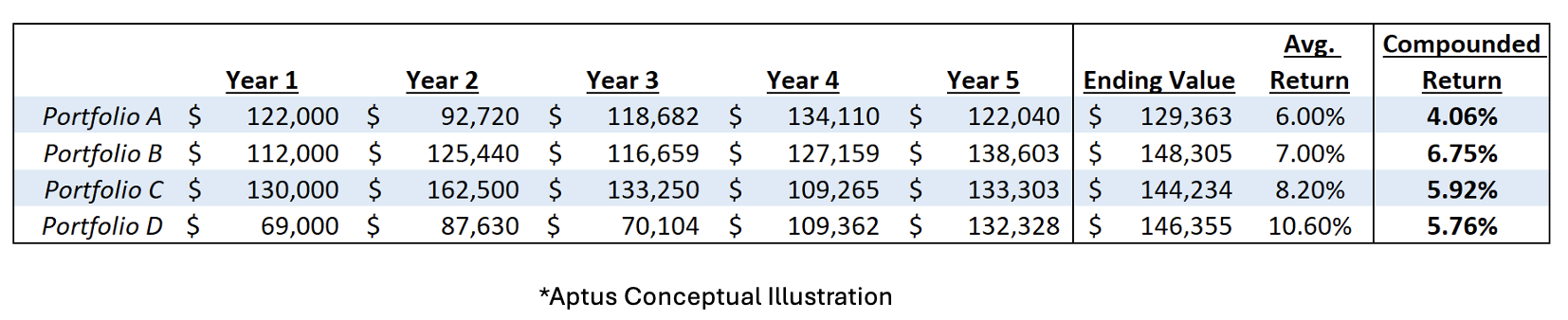

But, when you apply this path of returns to a capital base of $100,000, you can see the difference in terminal wealth each path creates.

The Takeaway: The best portfolio was Portfolio B. Despite having a lower simple average, it had the highest compounded return, which translates to the highest terminal wealth.

*Notice the volatility tax (simple average – compounded). Portfolio B’s is almost non-existent. Why? Because it avoided large drawdowns.

Fear Sells

While most people probably don’t think in terms of a volatility tax, it’s the inherent awareness that makes market crash predictions effective clickbait.

The negative impact to a long-term CAGR (compounded annual growth rate) of large losses is easily quantified. The behavioral impact is tougher to quantify. Based on my experience (and my kids point out I have gray hair now, so I feel more qualified to say that), the behavioral reactions by investors to uncertainty are the main culprit of lower CAGRs.

We could load you up with similar graphics as the one above that should instill confidence, but people still want to try and time asset allocation decisions based on the emotions they are feeling.

Remember, it’s our belief that the illusion of ‘safe’ returns is the greatest contributor to longevity risk investors face. And longevity risk should be the main concern.

Disappearing Return is a great summary that walks through why taxes and inflation are destroying the traditional definition of ‘safe’.

If a 10% drawdown turning into a 50% drawdown in equities is the fear, then hedge that risk away; don’t re-allocate towards the illusion of safety.

It’s the Tails That Matter

The chart above shows monthly outcomes for US equities for 100+ years. We’ve overlaid a normal distribution bell curve to the actual returns observed. Keep this in mind:

Frequency: The bell curve focuses on how often returns happen

Magnitude: This focuses on the impact of returns

Tail returns are the returns to the extreme left and extreme right of the distribution plot. They occur less frequently; they are the outliers. As the chart illustrates, while the tails occur less frequently, their combined contribution to long-term returns is 67.30%. Notice that of that total, the left tail carries the highest contribution. That jives with the multiplicative math – negative returns have more impact than positive returns.

When our focus is on generating the highest compounded returns possible while minimizing large drawdowns, we must recognize that magnitude is more relevant than frequency.

Think about the multiplicative process above.

The tails matter most as they impact long-term returns. Said another way, large losses should be avoided while positioning to capture as much of the upside as possible.

We want to be better in the tails.

Your Portfolios

Our entire approach is designed to own risk assets as we believe they are the stronger engine to drive returns. We want to hold hedges to protect against the extreme left tails that inevitably occur. The hedges are the brakes, and they’re negatively correlated to the engine.

This is different than a traditional approach that allocates away from risk assets in favor of things that have what we believe to be inferior engines for returns, all in the name of dampening volatility.

We want volatility. Specifically, upside volatility. We want to avoid massive drawdowns, or the left tails. We do that through owning hedges. Return / Volatility is not the risk metric that concerns us. We want Return / Drawdown to be as attractive as possible.

The presence of our hedges and the convexity in their payoff in a left tail allows us to own the risk confidently.

Own the Risk, Hedge the Tail

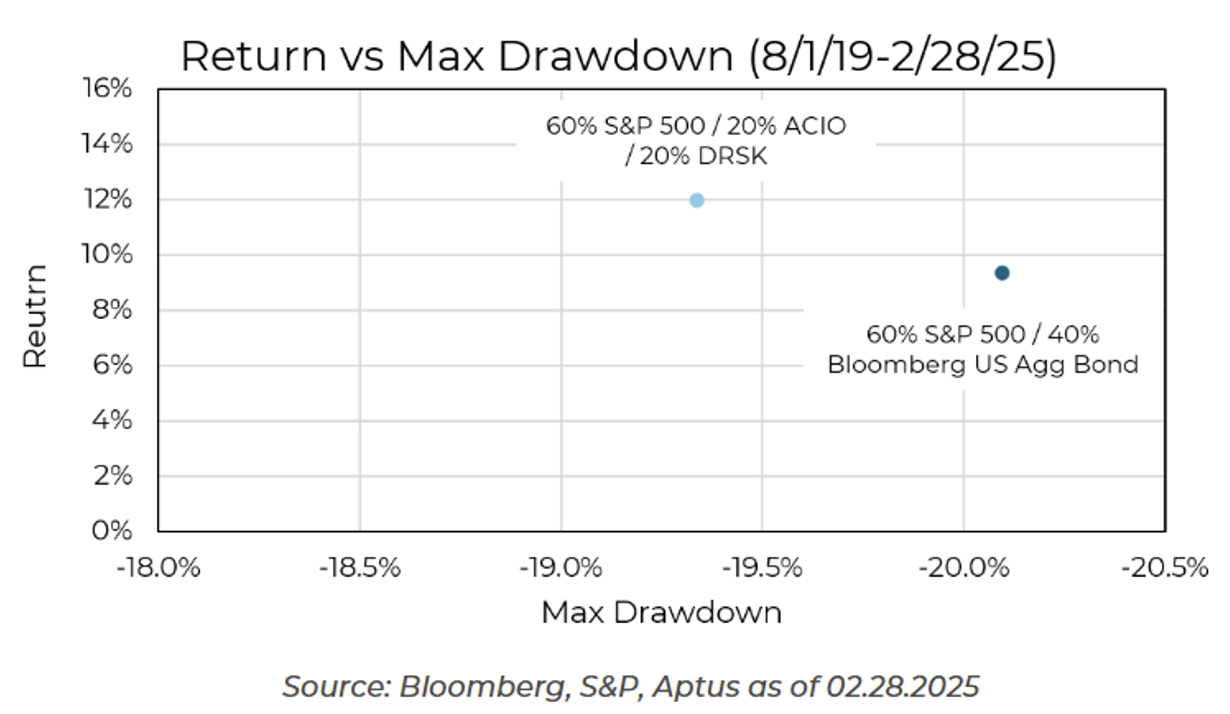

The team put together a write-up that, in my opinion, is a must read: A Modern Approach to 60:40

It illustrates how using our two flagship funds can impact portfolios and free an investor of the emotional distractions that come with investing.

Here’s a teaser:

There will be bumps along the way, without a doubt. We will experience negative returns from time to time. The ever-present risk in the market is why there is potential for return.

We are confident that if we can improve allocations to perform better in the tails, better outcomes are ahead.

We are working daily to continue to earn your trust. We appreciate you. Please don’t hesitate to reach out with any questions.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

*Conceptual Illustration: Information presented in the above charts are for illustrative purposes only and should not be interpreted as actual performance of any investor’s account. As these are not actual results and completely assumed, they should not be relied upon for investment decisions. Actual results of individual investors will differ due to many factors, including individual investments and fees, client restrictions, and the timing of investments and cash flows.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2504-4.