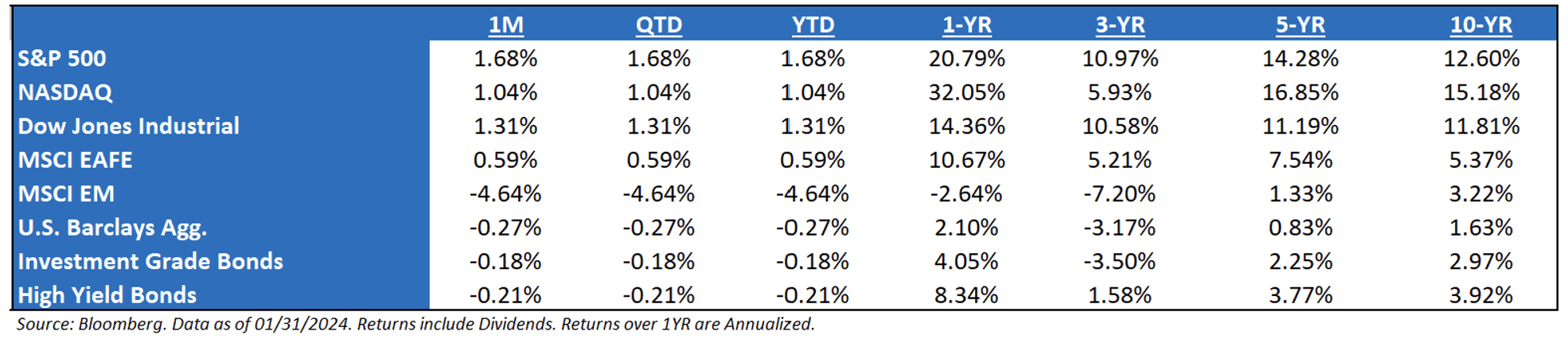

January ‘24 Market Recap → Good Start, Bad Breadth: Despite the S&P 500 rally, the equal-weighted S&P 500 fell 0.7% as breadth narrowed to just 34% (% of stocks ahead of S&P 500), a bottom 3rd percentile in history. The “Nifty 50” gained 3.0%, the “Not-So-Nifty 450” down 0.2%. But this is entirely consistent with earnings revisions so far this year, where consensus 2024 earnings expectations for the top 50 stocks remained intact vs. the 1% cut to the remaining 450. While not as extreme as it was during the Tech Bubble the Nifty 50’s index weight started to outpace its earnings weight, which suggests that a lot of good news has been priced into the mega caps.

Heading into 2024: A word of caution heading into 2024 is that the equity market seems as convinced about a soft landing today as it was convinced of a recession in 2022. In both cases, the short-term lesson is to not stand in the way of a market that wants to express an opinion, while the longer-term lesson is that the economy is a tortoise, and no matter the conviction level the equity market wants to have, the economy will take longer than most think to reveal its ultimate answer.

January Fed Meetings → The Flight has Been Delayed: The Fed held interest rates at 5.25%-5.5%. The decision was unanimous, but the FOMC’s language changed considerably (likely reflecting a wide range of individual committee member views). The next move is likely a rate cut, but the precise timing is still debatable. Chair Powell noted in his press conference that there has been progress on the dual mandate. The labor market is coming into better balance, though labor demand still exceeds labor supply. Powell noted that “greater confidence” would come from a continued string of U.S. inflation data about where it is now. He said that it’s unlikely FOMC confidence will increase enough by March to cut rates (i.e., the FOMC likely needs more time).

The Need for Monetary Policy Equilibrium: a monetary policy equilibrium can be generally defined as 1) the Fed behaving the way the market expects as well as 2) the market behaving the way the Fed expects. A better monetary policy equilibrium will occur when the Fed’s “dot” forecasts and market expectations converge. This equilibrium may only be cemented after the first Fed rate cut in 2024 since there are two major monetary policy questions now: 1) when does the return to a more neutral rate start; and 2) how low is the Fed funds rate going to go (where is neutral?).

Soft Landing Or Just Passing Through to a Recession? The equity markets are happy to support a soft landing thesis for now as the bond market is just taking economic weakness as a reason to send yields lower. However, the mathematical truth is that it is impossible to know whether we are just passing through growth rates consistent with a soft landing before slowing into a recession, or whether the economy will stay at growth rates similar to today.

Economic Data: Economically, nominal GDP, nominal consumer spending, nominal prices, essentially everything nominal, is decelerating, and although this process is slow in the U.S. It’s happening much more severely outside the U.S. This is unlikely to stop in 2024, and yet nominal corporate EPS are projected to re-accelerate through the year to ~20% y/y growth by Q4 ‘24.

Earnings Season Has Begun: To start the month (pre-Megacap results), 124 S&P 500 companies (30% of index earnings) are in. While consensus 4Q EPS (actuals + estimates) is tracking a ‘meet’ vs. expectations at the start of January, reported EPS has come in 5% above consensus, led by Financials (+10%) and Industrials (+7%). Reported sales beat by 0.7%. 73%/65%/51% of reporters beat on EPS/sales/both, better than the historical average of 63%/59%/44% and last quarter’s 65%/59%/48%. Reactions to beats (+80bps) have been more muted vs. the historical average (+150bps).

The Presidential Election Year: Since 1952, the S&P 500 has not declined in a year in which an incumbent president was running for re-election (avg. return of 10%). Stocks have declined in presidential election years, but in each of those cases, it was a year in which there was an open election with no incumbent running (1960, 2000, and 2008). This makes sense. presidents want to be re-elected and will use whatever policy levers are needed to boost the US economy. In fact, every President who avoided a recession two years before their re-election went on to win election. And every President who had a recession in the two years before their re-election went on to lose.

Earnings: ‘24 S&P 500 EPS = 243 (+11.8%). 2023 = $218 (-0.5%). 2022 = $219 (+7.4%). 2021 = $204. 2020 = $136. 2019 = $161. *

Valuations: S&P 500 Fwd. P/E (NTM): 20.0x, EAFE: 14.1x, EM: 11.3x, R1V: 15.4x, and R1G: 26.4x.*

*Source: Bloomberg and FactSet, Data as of 01/31/24

Disclosures

Aptus Capital Advisors, LLC is a Registered Investment Advisor (RIA) registered with the Securities and Exchange Commission and is headquartered in Fairhope, Alabama. Registration does not imply a certain level of skill or training. For more information about our firm, or to receive a copy of our disclosure Form ADV and Privacy Policy call (251) 517-7198 or contact us here. Information presented on this site is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy.

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 11.2 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 4.6 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security’s U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004, and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities.

The Dow Jones Industrial Average® (The Dow®), is a price-weighted measure of 30 U.S. blue-chip companies. The index covers all industries except transportation and utilities.

The MSCI EAFE Index is an equity index which captures large and mid-cap representation across 21 Developed Markets countries*around the world, excluding the US and Canada. With 902 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 Emerging Markets (EM) countries*. With 1,387 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Investment-grade Bond (or High-grade Bond) are believed to have a lower risk of default and receive higher ratings by the credit rating agencies. These bonds tend to be issued at lower yields than less creditworthy bonds.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

Nasdaq-100® includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. This includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities, and collateralized mortgage-backed securities. ACA-2402-2.