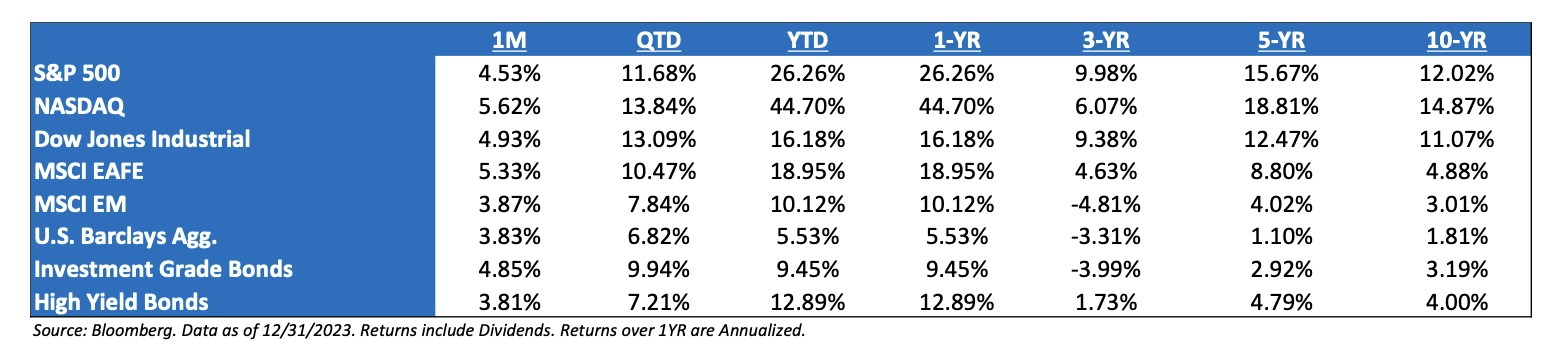

December ’23 Market Recap: Investors enjoyed broad-based relief in the fourth quarter. After rising sharply in Q2 and Q3, rates peaked in the fourth quarter fueled by Powell’s pivot at the December FOMC meeting. Similarly, oil prices peaked in late September and declined sharply throughout the fourth quarter as well. In Q4 investors bid on cyclicals, small caps and lower quality names, which lagged substantially in the first three quarters. With the change in rates, surprisingly, the 10-Year Treasury yield ended the year at the exact rate at which it began the year. The rally in rates led to the best 2-month rally in bonds in over 40 years!

Heading into 2024: A word of caution heading into 2024 is that the equity market seems as convinced about a soft landing today as it was convinced of a recession in 2022. In both cases, the short-term lesson is not to stand in the way of a market that wants to express an opinion, while the longer-term lesson is that the economy is a tortoise, and no matter the conviction level the equity market wants to have, the economy will take longer than most think to reveal its ultimate answer.

Q4 2023 Was a Reversal of Leadership in Q1, Q2, and Q3: For most of the year, leadership across size and style boxes was fairly linear, with larger and growthier stocks outpacing smaller and more value-oriented areas. In the fourth quarter, we saw a dramatic reversal and catch-up trade where small value clawed back some relative performance and narrowed the 2023 gap. In fact, the R2K went from a 52-week low to a high at a record pace.

Soft Landing Or Just Passing Through to a Recession?: The equity markets are happy to support a soft landing thesis for now as the bond market is just taking economic weakness as a reason to send yields lower. However, the mathematical truth is that it is impossible to know whether we are just passing through growth rates consistent with a soft landing before slowing into a recession or whether the economy will stay at growth rates similar to today.

Dippin’ Dots: The Fed delivered the dovish pivot that we expected at the December meeting. The bulk of the data flow since the Fed last met in November has been very favorable to their soft-landing outlook and has improved their confidence that inflation is on a downward trend. The shift in the Fed’s stance came through in the statement, updated projections, and the press conference. The statement made reference to growth in economic activity slowing “from its strong pace in the third quarter”, moderating job gains, and easing inflationary pressures over the past year. In terms of forward guidance, the statement now references what the committee will watch to determine “the extent of any additional policy firming that may be appropriate to return inflation to 2 percent over time.” the median FOMC participant now foresees a 4.6% funds rate in Q4 ‘24 and 3.6% in Q4 ‘25, down from 5.1% and 3.9% previously. The dots imply 75bp of cuts in 2024 and a cutting cycle that begins in June.

The Equity Volatility Tax: Since Nov 8, 2020 (Pfizer vax approval), every major benchmark average return is within basically 2% of each other. All the various style and size changes have just been giant reversions to the mean return. Don’t get whipsawed by the equity volatility tax. Since this date, the S&P 500 is up 11.06% annually, while the S&P 400 and S&P 600 are up 10.07% and 9.83%, respectively. Though, it may not feel like it after the return stream of 2023.

Next Year’s Earnings Profile: Although expectations for S&P 500 earnings in 2024 have moderated to a degree, the Street is still expecting nearly a 12% increase in profits after what is likely to be a flattish year in 2023. As it stands now, the expectations largely come down to the earnings power of the Technology and Communications sectors. EPS has been quite negative year-over-year in 2023 despite real GDP and the labor market being better than expected; the best evidence yet that nominal means much more to earnings than real. Nominal growth should continue to decelerate in 2024, as consensus EPS seem far too optimistic for that reality.

The Presidential Election Year: Since 1952, the S&P 500 has not declined in a year in which an incumbent president was running for re-election (avg. return of 10%). Stocks have declined in presidential election years, but in each of those cases, it was a year in which there was an open election with no incumbent running (1960, 2000, and 2008). This makes sense. Presidents want to be re-elected and will use whatever policy levers are needed to boost the US economy. In fact, every president who avoided a recession two years before their re-election went on to win the election. And every president who had a recession in the two years before their re-election went on to lose.

Earnings: ‘24 S&P 500 EPS = 246 (+11.5%). 2023 = $220 (+0.8%). 2022 = $219 (+7.4%). 2021 = $204. 2020 = $136. 2019 = $161. *

Valuations: S&P 500 Fwd. P/E (NTM): 19.7x, EAFE: 13.7x, EM: 11.9x, R1V: 15.4x, and R1G: 26.2x.*

*Source: Bloomberg and FactSet, Data as of 12/31/23

Disclosures

Aptus Capital Advisors, LLC is a Registered Investment Advisor (RIA) registered with the Securities and Exchange Commission and is headquartered in Fairhope, Alabama. Registration does not imply a certain level of skill or training. For more information about our firm, or to receive a copy of our disclosure Form ADV and Privacy Policy call (251) 517-7198 or contact us here. Information presented on this site is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy.

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 11.2 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 4.6 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security’s U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities.

The Dow Jones Industrial Average® (The Dow®), is a price-weighted measure of 30 U.S. blue-chip companies. The index covers all industries except transportation and utilities.

The MSCI EAFE Index is an equity index which captures large and mid-cap representation across 21 Developed Markets countries*around the world, excluding the US and Canada. With 902 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 Emerging Markets (EM) countries*. With 1,387 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Investment-grade Bond (or High-grade Bond) are believed to have a lower risk of default and receive higher ratings by the credit rating agencies. These bonds tend to be issued at lower yields than less creditworthy bonds.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. This includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities, and collateralized mortgage-backed securities. ACA-2401-4.