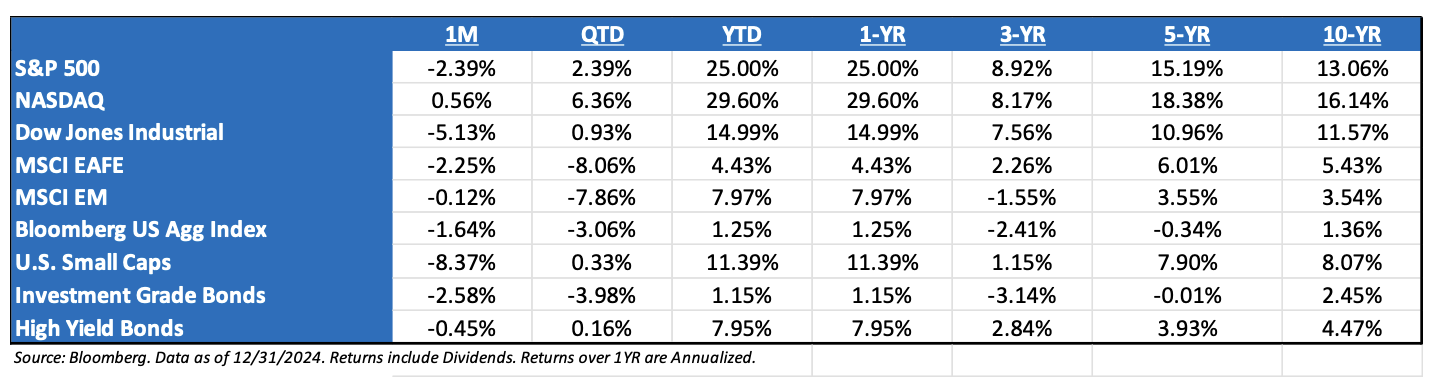

Market Recap – December 2024: The rally in stocks in 2023 was driven, mostly, by hope of market friendly events: The end of rate hikes and start of rate cuts, the economy slowing to a soft, not hard, landing, AI profit explosions and positive geopolitical resolutions. The rally this year has been driven by the partial realization of those hopes: Growth did slow but didn’t contract (soft landing), the Fed did aggressively cut interest rates, AI demand and excitement didn’t waver and geopolitical crises didn’t get worse (although they didn’t get better). As we enter 2025, the question for markets is whether the positive events realized in 2024 can last. Does the soft-landing stay in place or does it deteriorate? Does the Fed keep cutting rates or do they pause? Does inflation fall to 2% or rebound? Do pro-growth policy hopes get realized?

Fed Update: At the beginning of the year, the terminal rate was expected to be ~3.0%, but with the inflation proving to be stickier, and the potential remaining for a re-acceleration, the bar has shifted to a level closer to ~3.8%. Put differently, while fewer-than-expected rate cuts are a disappointment in the near term compared to market expectations, the facts tell me that the rate-cutting cycle is still in place, and, as a result, Fed policy remains supportive for stocks – maybe just less than before.

The Burden of Proof Remains with the Bears: Put simply, while the economy is slowing, the news has not been bad enough yet to cause a sustainable decline in stocks. The Fed’s easing cycle, coupled with “OK” macroeconomic data, has kept earnings forecasts steady.

-

- What Bears are Saying: Rising unemployment, weak ISM Manufacturing PMI, and negative earnings guidance hint at challenges ahead. Concerns also include political uncertainty (domestic and global) and geopolitical risks (Russia/Ukraine, Israel/Palestine).

- What Bulls are Saying: 1) Still “ok” economic data—slowing, but not alarmingly so, 2) The initial market rally due to anticipated Fed rate cuts, 3) Earnings growth, still strong at over 10% year-over-year, and 4) Optimism around AI advancements.

First Year of a New Presidential Cycle: Until recently, it was a decent bet that the second half of a President’s term would be better for market performance than the first. Generally speaking, Presidents would make the hard decisions when their political capital was at its highest and then let it rip as they sought re-election. All that seemed to change with the election of President Obama, the introduction of QE and the budget deficits that accompanied it. Since 2005, the best year for market returns has been the first year of a Presidential term – and it’s by an enormous margin.

Politics and Markets: The market is not political. It doesn’t care about draining swamps, political retribution, woke or anti-woke campaigns or DEI initiatives. The market only cares about policies that:

-

- Increase (or decrease) earnings, and

- Support growth (or hinder it).

Any political movement or agenda that is viewed by the market as getting in the way of better earnings and growth will be viewed as negative and be a headwind on risk assets, regardless of whether those policies are from Republicans or Democrats. This is the way we must view political coverage over the next year (and likely four years) and this will help us cut through the noise and stay focused on the policies that will impact markets.

Everyone Wants to Talk About Tariffs: We believe that Trump will likely try to push tariffs in the Tax Bill.

-

- China: The market is telling us that it believes that China tariffs are likely. The new administration can easily reopen an investigation and add a 10% tariff rate to the existing tariffs to get the tariff process started. Trump is trying to raise the cost of business in China and migrate the supply chains.

- Europe: Tariffs on Europe are more difficult than China. For example, we do not believe that Trump has the legal authority to impose a universal tariff. As such, we expect this to be more of a threat to “escalate to de-escalate,” with the goal of better market access for US products in the EU.

- Mexico and Canada: Raising tariffs on our largest trading partners is a violation of the USMCA, which was passed into law by Congress. As such, Trump’s ability to enact these tariffs is more difficult relative to the China tariffs, but not entirely out of the realm of possibilities. The process just takes longer and is fraught with legal hurdles. Trump’s team knows this. We get a feeling that these tariffs are more about immigration than trade.

- Universal Tariffs: As stated above, we believe that Trump does not have the legal authority to impose a universal tariff.

S&P 500 EPS: ’25 (Exp.) EPS = $275. ‘24 EPS = $239 (+15.1%). 2023 = $220 (+8.6%). 2022 = $219 (+0.5%). 2021 = $204.*

Valuations: S&P 500 Fwd. P/E (NTM): 21.7x, EAFE: 14.0x, EM: 11.8x, R1V: 16.6x, and R1G: 28.6x. *

*Source: Bloomberg and FactSet, Data as of 12/31/24

Disclosures

Aptus Capital Advisors, LLC is a Registered Investment Advisor (RIA) registered with the Securities and Exchange Commission and is headquartered in Fairhope, Alabama. Registration does not imply a certain level of skill or training. For more information about our firm, or to receive a copy of our disclosure Form ADV and Privacy Policy call (251) 517-7198 or contact us here. Information presented on this site is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy.

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 11.2 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 4.6 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security’s U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities.

The Dow Jones Industrial Average® (The Dow®), is a price-weighted measure of 30 U.S. blue-chip companies. The index covers all industries except transportation and utilities.

The MSCI EAFE Index is an equity index which captures large and mid-cap representation across 21 Developed Markets countries*around the world, excluding the US and Canada. With 902 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 Emerging Markets (EM) countries*. With 1,387 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Investment-grade Bond (or High-grade Bond) are believed to have a lower risk of default and receive higher ratings by the credit rating agencies. These bonds tend to be issued at lower yields than less creditworthy bonds.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

Nasdaq-100® includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. This includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities, and collateralized mortgage-backed securities. ACA-2501-2.