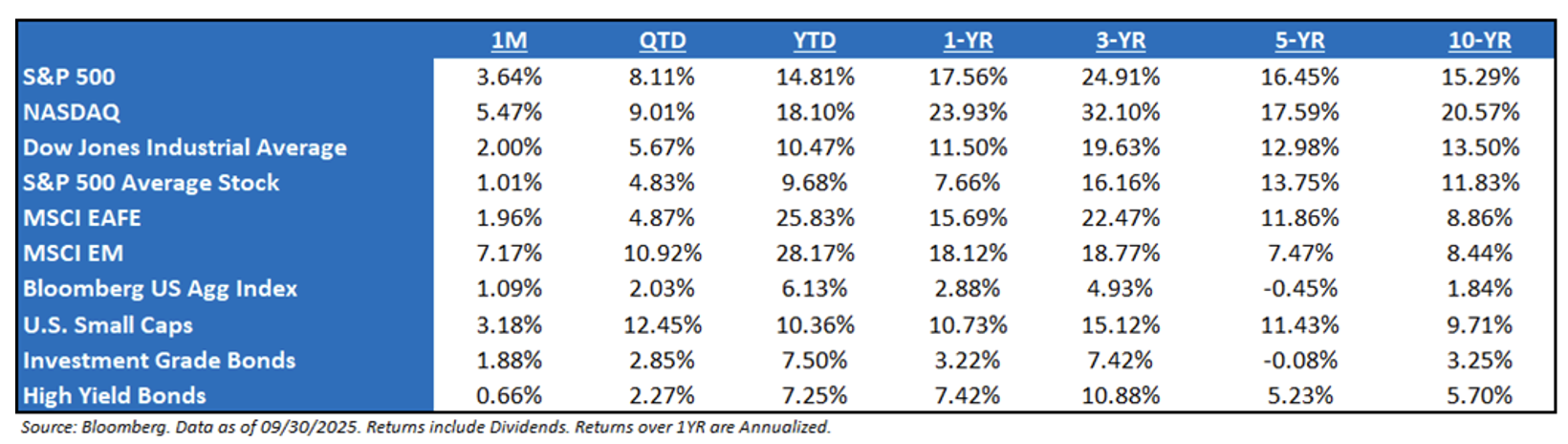

Market Recap September 2025 – Life Certainly Looks Like Easy Street in the Equity Markets: It’s always easier when the markets are going up. Equities have continued to press to all-time highs, and long rates have continued lower. We find it difficult to poke too many holes in the bull case, though we’re not divorced from reality either. The market has had to endure some weakening macro reports, i.e., stickier inflation and a slowing jobs market. While the market appears to have shaken off this concern, on the heels of continued strength in the A.I. narrative. Don’t fight this market. This doesn’t mean that the market won’t have a pullback, as they are necessary and healthy, but research shows that the best time to own the market is when it is hitting new all-time highs.

Federal Reserve Meeting Update: The Federal Reserve cut interest rates by 25 basis points to the 4.00% – 4.25% range, marking a 125bp reduction since rates began coming down last September, but the first cut since December – i.e., 9 months in between cuts. The long pause was in response to fears of inflation stemming from the tariffs imposed in February and April this year. Fed’s dot plot indicated two more rate cuts were possible before year-end. This trajectory may have allowed today’s decision to proceed without additional dissents. The next two meetings are Oct. and Dec., though Fed Chair Powell noted that cuts then were not done deals. He called today’s move a “risk management cut.” With the re-engagement of their rate cut cycle, the goal should be to get policy rates from restrictive to neutral. A key question remains: how low is the fed funds rate going to go (where is neutral?). We still believe a ~1% real (inflation-adjusted) rate should be a good longer-term target.

Earnings Season Recap: Despite the lower expectations, Q2 exceeded even the pre-liberation day growth expectations with growth coming in at more than double initial expectations – ending around +12.9%. Revenue growth came in at a whopping 6.3%, outpacing the previous four quarters, even before tariffs were introduced. Concerns over stalling sales have not materialized. Looking ahead, full-year 2025 EPS estimates are once again approaching $270, while growth projections for 2026 remain strong at around 13%! The Mag 7 was driving most/all of the earnings growth in 2023/2024, while the rest of the index was in a modest earnings recession. This trend was expected to reverse in 2025, but the line keeps getting pushed out to the right. Mag 7 EPS continues to outperform (+26% in Q2 ’25), while EPS continues to underwhelm everywhere else with small, mid, S&P 493, and Europe essentially with flat EPS YoY. The lines are now expected to cross in Q4 ‘25/ FY26, which would be consistent with broadening performance in the equity market, but at this point, we would expect more delay to this much anticipated event.

Tariffs Deemed Illegal → What Does This Mean? The US Court of Appeals for the Federal Circuit (“CAFC”) rejected Trump’s tariffs enacted through the International Emergency Economic Powers Act (“IEEPA”). The Court’s decision was largely expected. It’s likely that President Trump has a backup plan through Balance of Payments and Section 301 to resurrect tariffs even if the Supreme Court strikes down the tariffs in early 2026. With respect to refunds of tariffs already paid, CAFC remanded the case back to the Court of International Trade to decide if a universal injunction requiring all previously collected tariffs to be refunded is consistent with the Supreme Court’s disfavoring universal injunctions. For now, the tariffs remain in place and will continue to be collected. We expect the Supreme Court to take the case in October and a decision sometime next year.

Who’s Footing the Tariff Bill? Per Goldman, they expected the consumer to bear ~70% of the tariff cost. That has not been the case so far, as they now estimate that corporations have footed the majority of the bill so far, estimated to be ~64% as they work their way through pre-tariff inventories. Consumers, estimated by Goldman, have only eaten 22%, while foreign exporters have about 14%. This makes sense, as we have not seen inflation materially jump, nor the 3- and 5-YR breakevens – the latter being the important part. But some of this data should be seen in the S&P 500 operating margin. Although it is decreasing, it seems like the operating leverage of the Magnificent Seven has more than insulated this margin degradation.

The Market Moving Forward: As long as earnings are growing, which they are, and as long as both monetary and fiscal policy are on the market’s side, the burden of proof will remain with the bears. Where all this leads it that we are still in a bull market – don’t fight it – but that doesn’t mean chase it. It appears that the market is entering a period where it can see a moderation of hard economic data, but not enough to warrant a recession. If markets price in deeper rate cuts off the back of this, then this will only serve to ease financial conditions further. Meanwhile, the forward-looking sentiment data should continue to improve with economic tail risks diminishing and expansionary fiscal policy on the horizon. This, combined with continued AI-driven investment and innovation, should continue to support risk assets once we move beyond the current geopolitical tensions. We may be headed into a goldilocks end to the year with both bond and equity markets performing well.

Politics and Markets – The Government Shutdown: In my opinion, the market is not political. It doesn’t care about draining swamps, political retribution, woke or anti-woke campaigns, or DEI initiatives. The market only cares about policies that:

-

- Increase (or decrease) earnings, and

- Support growth (or hinder it).

Any political movement or agenda that is viewed by the market as getting in the way of better earnings and growth will be viewed as negative and be a headwind on risk assets, regardless of whether those policies are from Republicans or Democrats. This is the way we must view political coverage over the next year (and likely four years), and this will help us cut through the noise and stay focused on the policies that will impact markets.

S&P 500 EPS: ’26 (Exp.) EPS = $296.33 (+11.4%). ’25 (Exp.) EPS = $266.00 (+8.5%). ‘24 EPS = $245.16 (+11.5%). 2023 = $220 (+8.6%). 2022 = $219 (+0.5%).

Valuations: S&P 500 Fwd. P/E (NTM): 22.8x, EAFE: 15.5x, EM: 13.8x, R1V: 17.8x, and R1G: 30.2x. *

*Source: Bloomberg and FactSet, Data as of 09/30/2025

Disclosures

Aptus Capital Advisors, LLC is a Registered Investment Advisor (RIA) registered with the Securities and Exchange Commission and is headquartered in Fairhope, Alabama. Registration does not imply a certain level of skill or training. For more information about our firm, or to receive a copy of our disclosure Form ADV and Privacy Policy call (251) 517-7198 or contact us here. Information presented on this site is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy.

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 11.2 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 4.6 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization.

The Nasdaq Composite Index measures all Nasdaq domestic and international-based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security’s U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security types not included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities.

The Dow Jones Industrial Average® (The Dow®), is a price-weighted measure of 30 U.S. blue-chip companies. The index covers all industries except transportation and utilities.

The MSCI EAFE Index is an equity index which captures large and mid-cap representation across 21 Developed Markets countries*around the world, excluding the US and Canada. With 902 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 Emerging Markets (EM) countries*. With 1,387 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Investment-grade Bond (or High-grade Bond) are believed to have a lower risk of default and receive higher ratings by the credit rating agencies. These bonds tend to be issued at lower yields than less creditworthy bonds.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

Nasdaq-100® includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. This includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities, and collateralized mortgage-backed securities. ACA-2510-6.