Our team looks at a lot of research throughout the day. Here are a handful of charts we think are good summations during one of the more complex backdrops in recent memory. From tariff uncertainty, shifting leadership, and macro crosscurrents that don’t fit neatly into a bull or bear narrative. As always, the goal is signal over noise.

Beckham: S&P 500 seasonality since 2009 shows April is typically a strong month for equities. If historical patterns hold, the current window provides a favorable backdrop before the summer lull.

Brad: For two years, S&P 500 earnings have consistently exceeded conservative estimates. With 2026 forecasts now calling for double-digit growth, the bar is finally set high. Execution is now the primary risk.

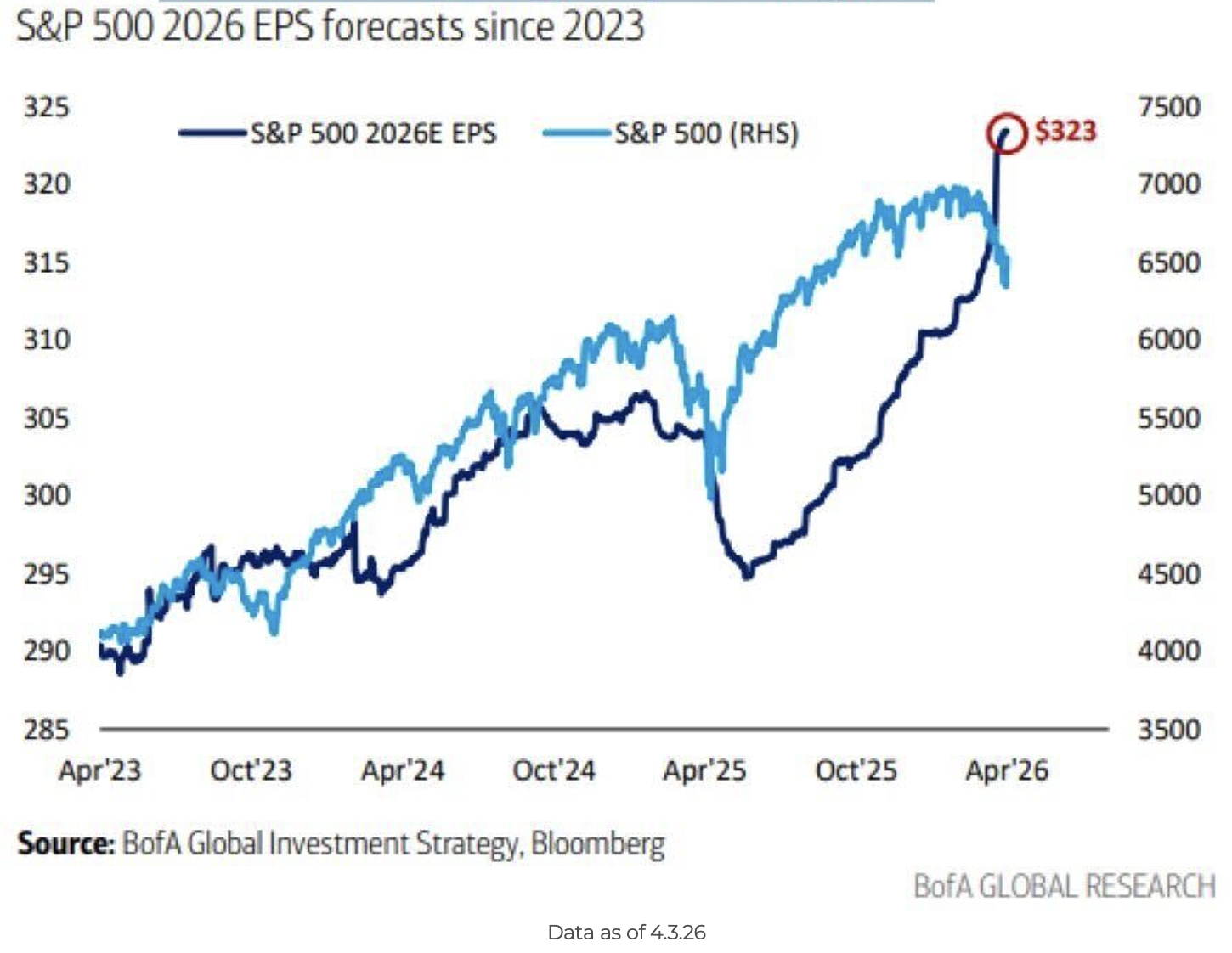

Joseph: Despite broader market volatility, 2026 EPS forecasts continue to move higher. The gap between price action and fundamental earnings power remains a critical tension point for bulls.

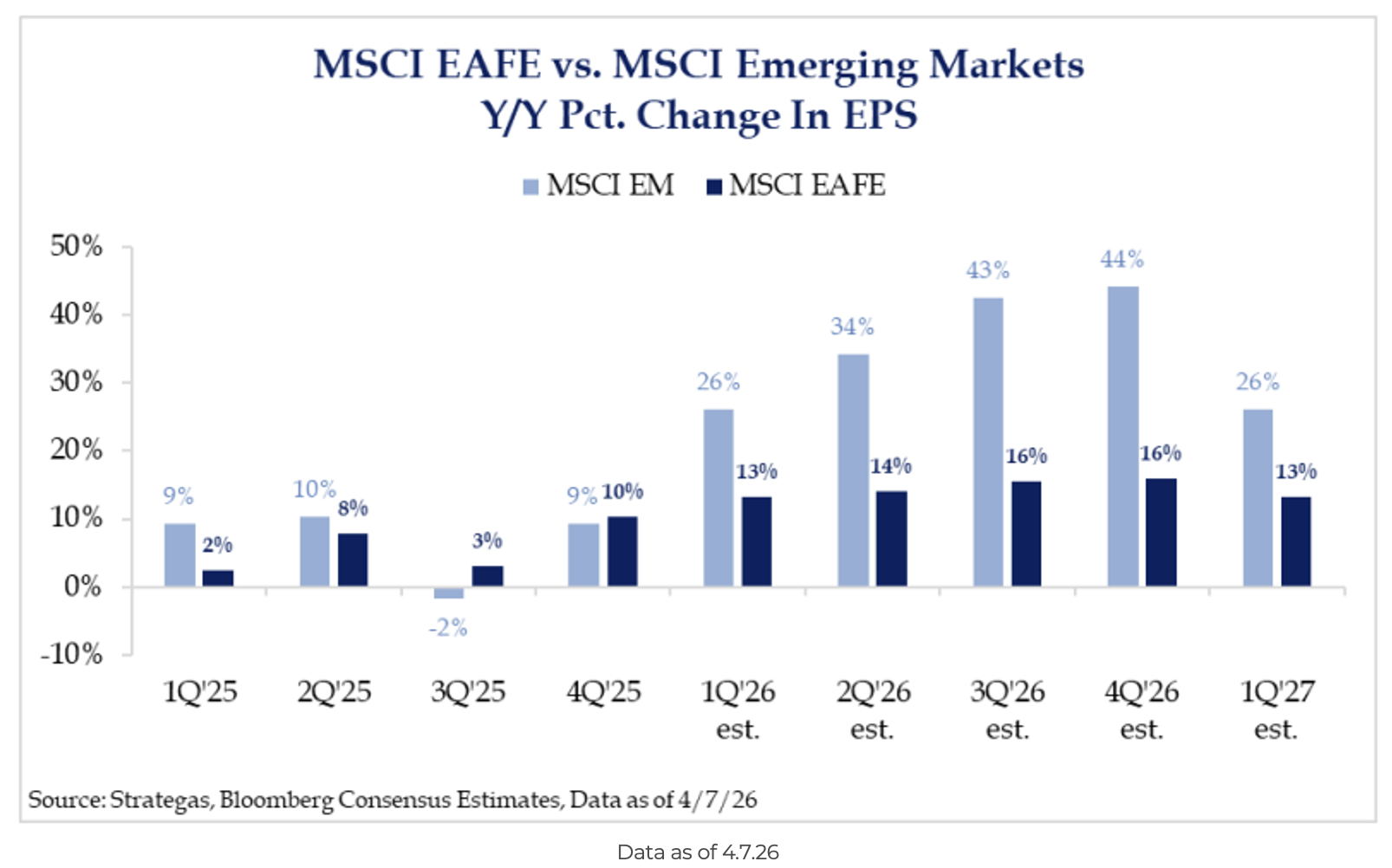

John: It’s not just the United States. Emerging Markets may be the earnings growth story of 2026. While energy concerns in Asia persist, they aren’t reflected in estimates yet. EM resilience may be overlooked.

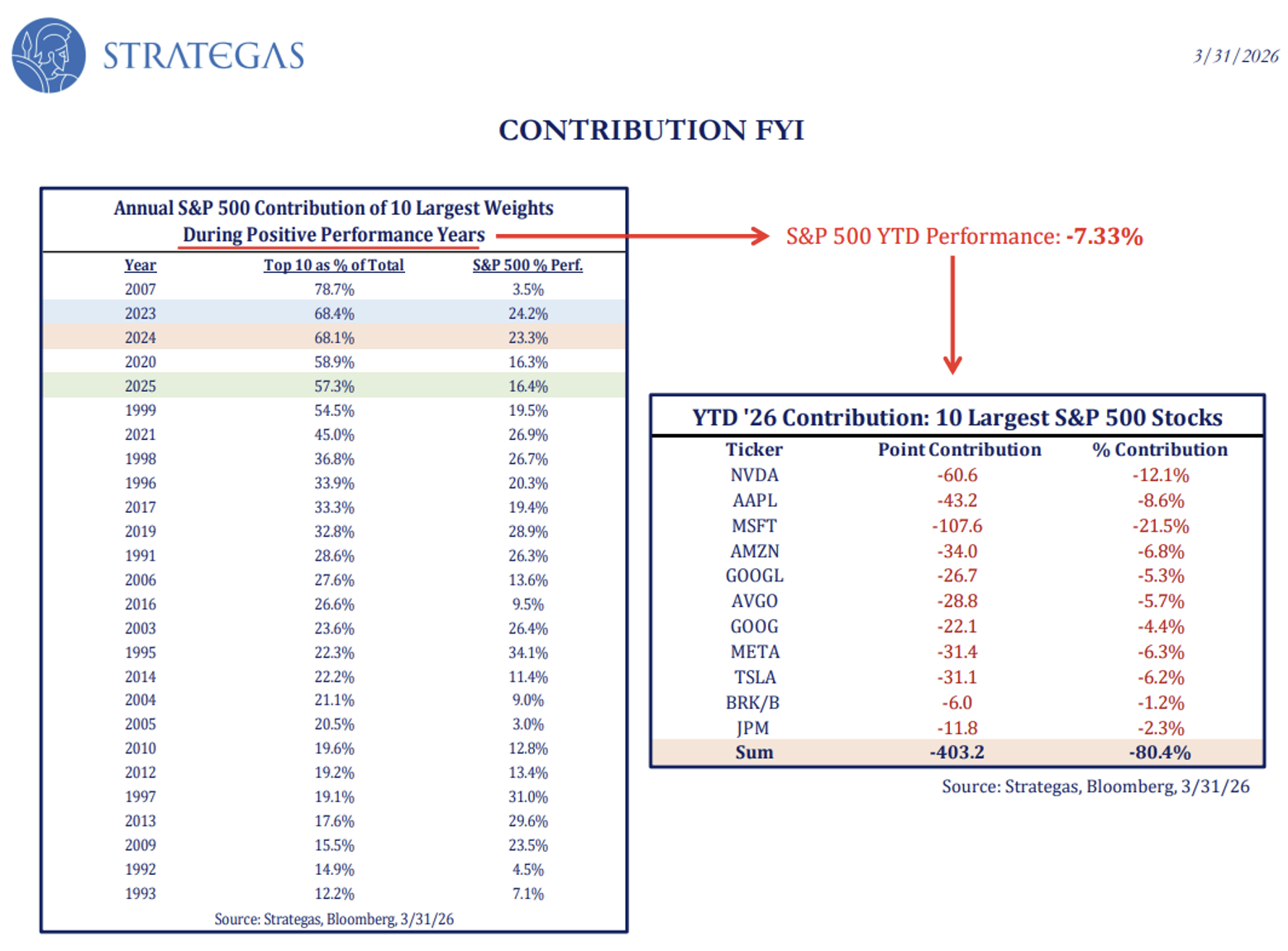

Mark: While the S&P 500 index has been resilient given ongoing geopolitics, a look under the hood reveals the S&P 500’s top 12 constituents were broadly deeply negative through the end of March, signaling a massive shift in market leadership.

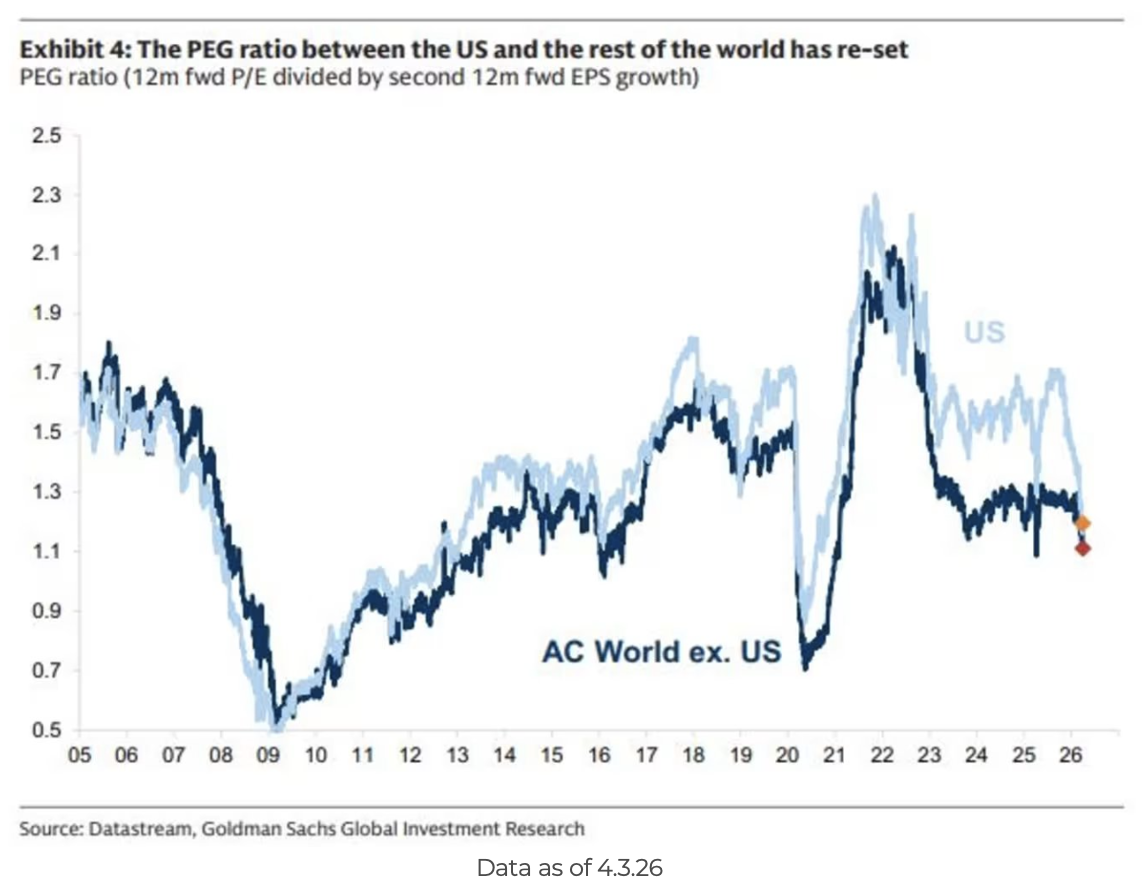

Derek: Given earnings have remained resilient, and valuations among these large companies have reset, the PEG ratio for the US versus the rest of the world has compressed, making these large cap companies increasingly attractive on a relative and growth-adjusted basis.

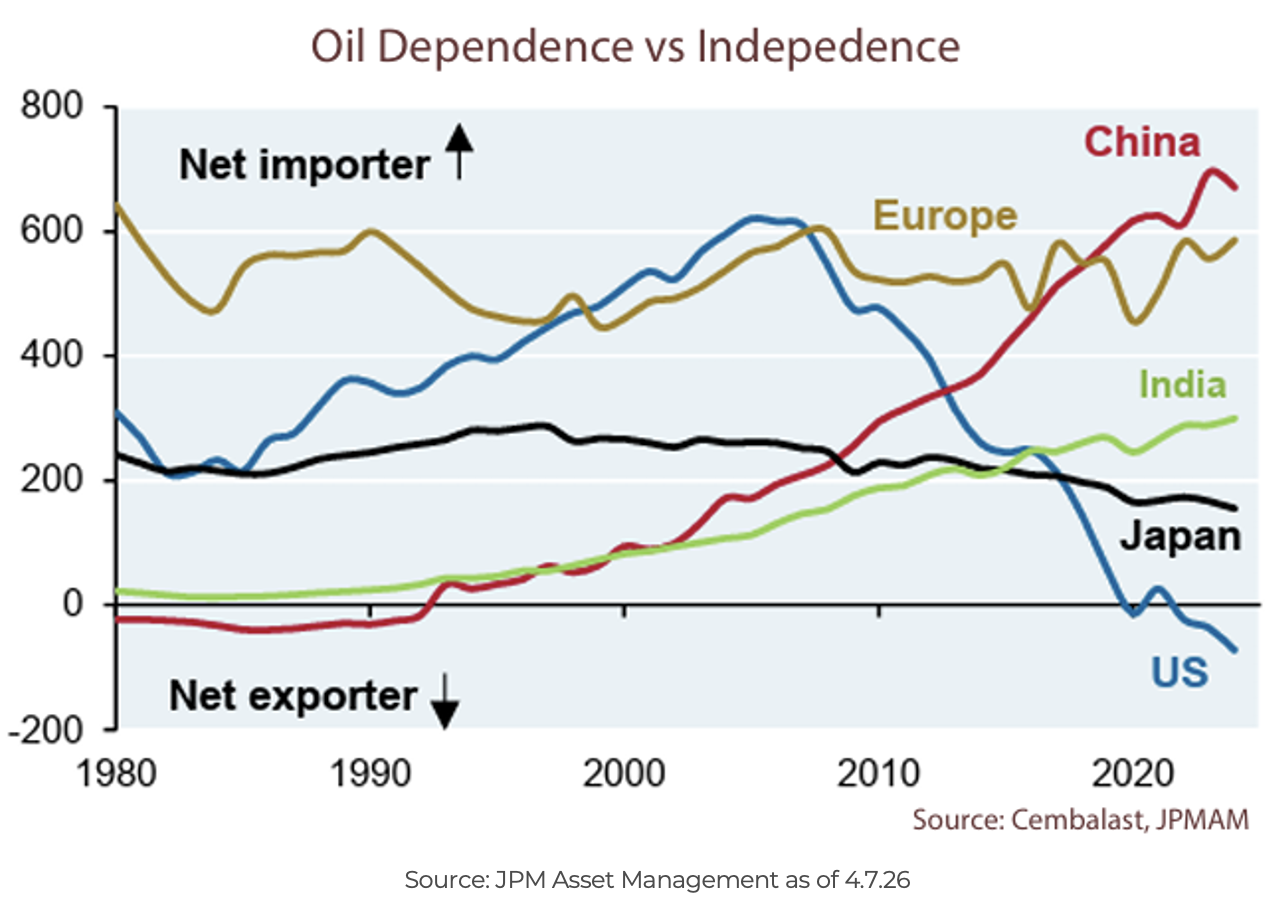

Brett: The case for the United States is further supported by an energy profile that has fundamentally changed. As a net exporter, the domestic economy is far better shielded from global oil shocks than in previous decades.

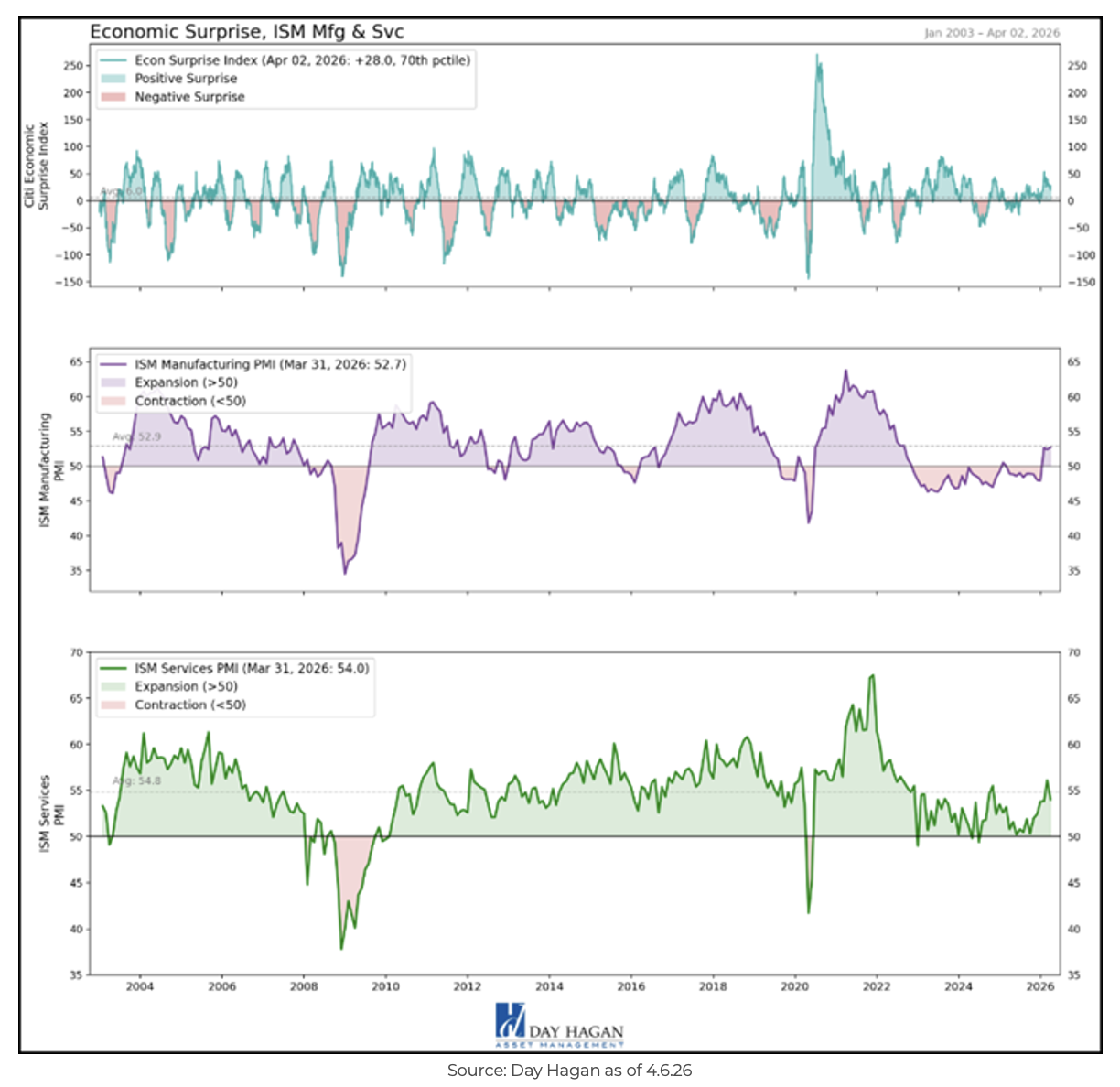

JD Gardner: Economic data remains resilient but nuanced. While the Surprise Index is positive and Manufacturing is expanding, the slight cooling in Services suggests growth is supportive but losing some peak momentum.

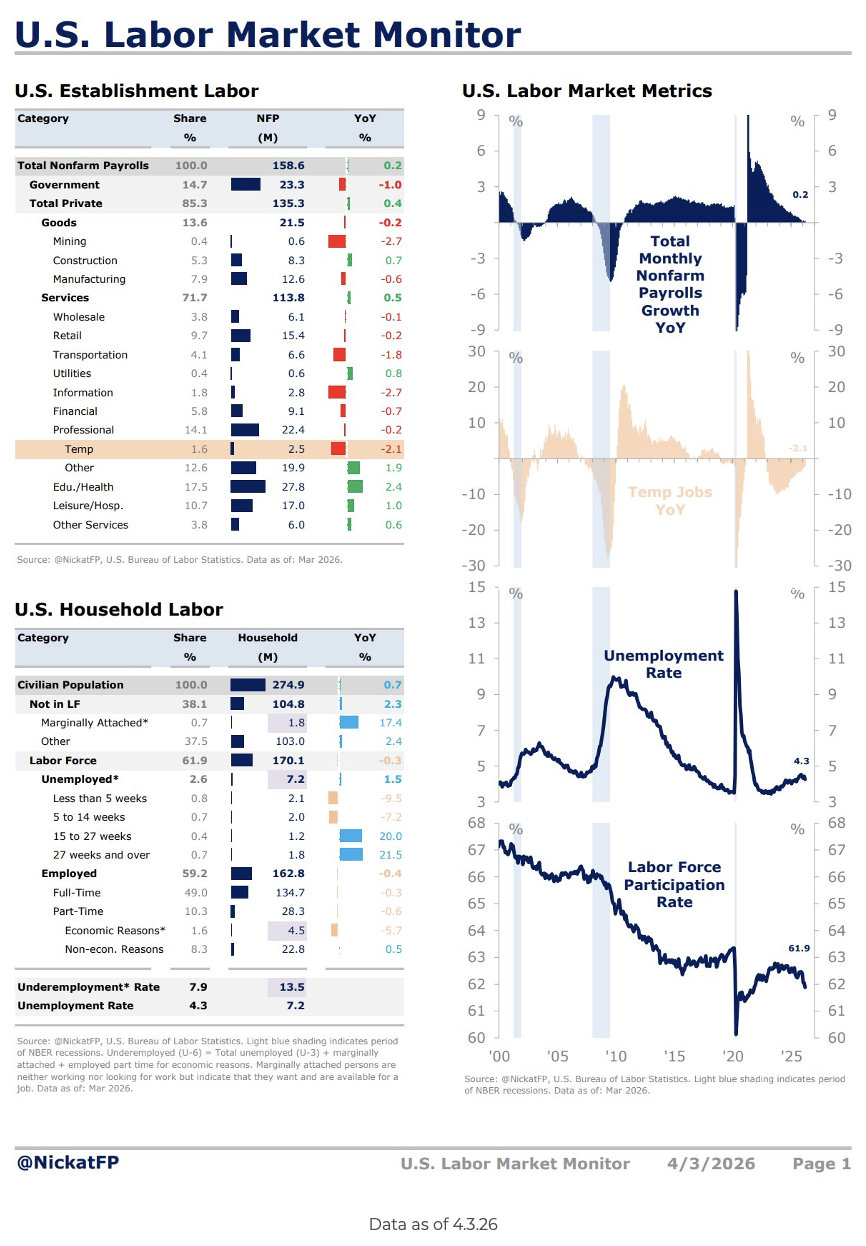

Brian: The labor market also remains a riddle. Payroll growth is flat, and participation is shrinking, yet unemployment stays low. Whether this is AI-driven downsizing or a productivity miracle remains the key debate for 2026.

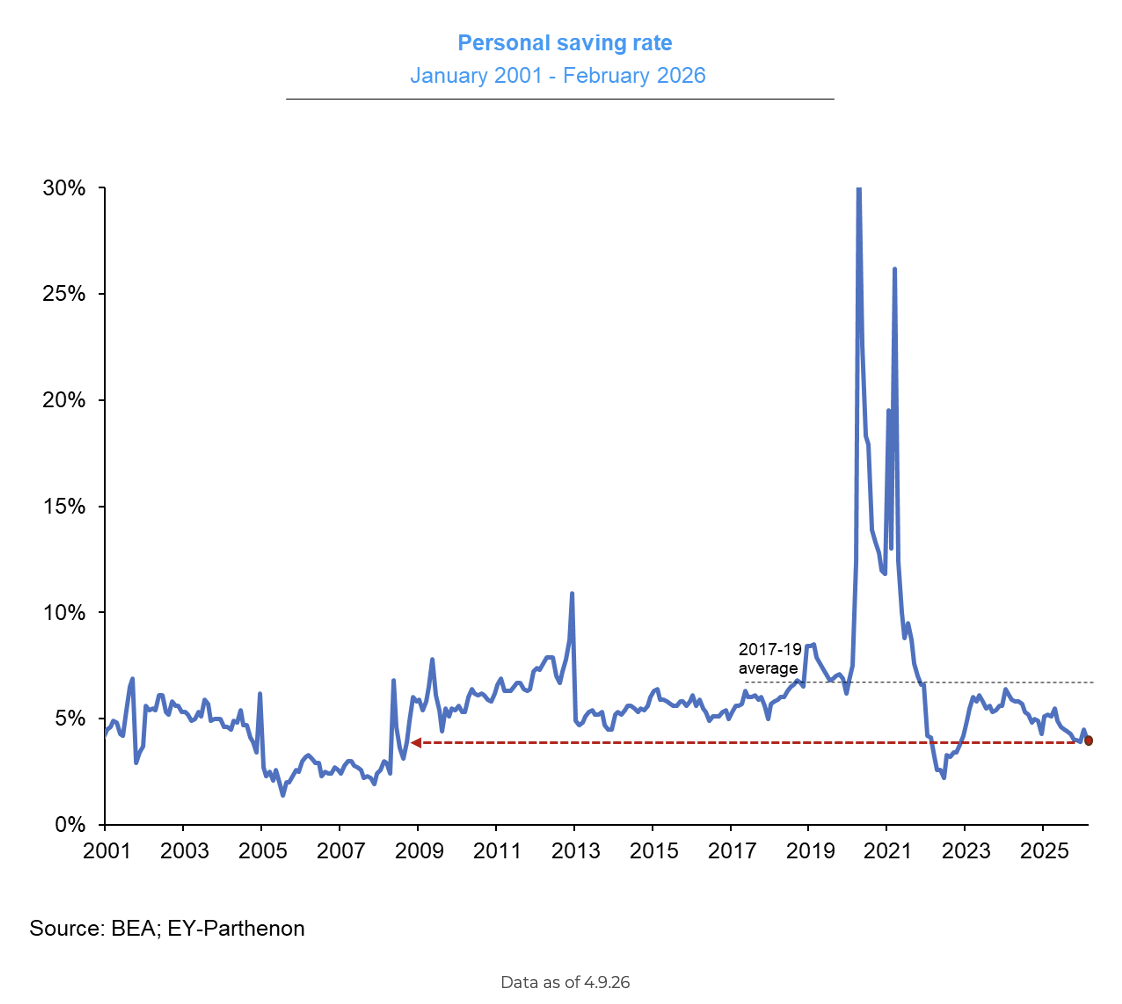

Jake: Consumer spending has remained resilient, but has been a result of reduced savings. With higher oil prices, there is a question of whether consumers will dip into their savings further.

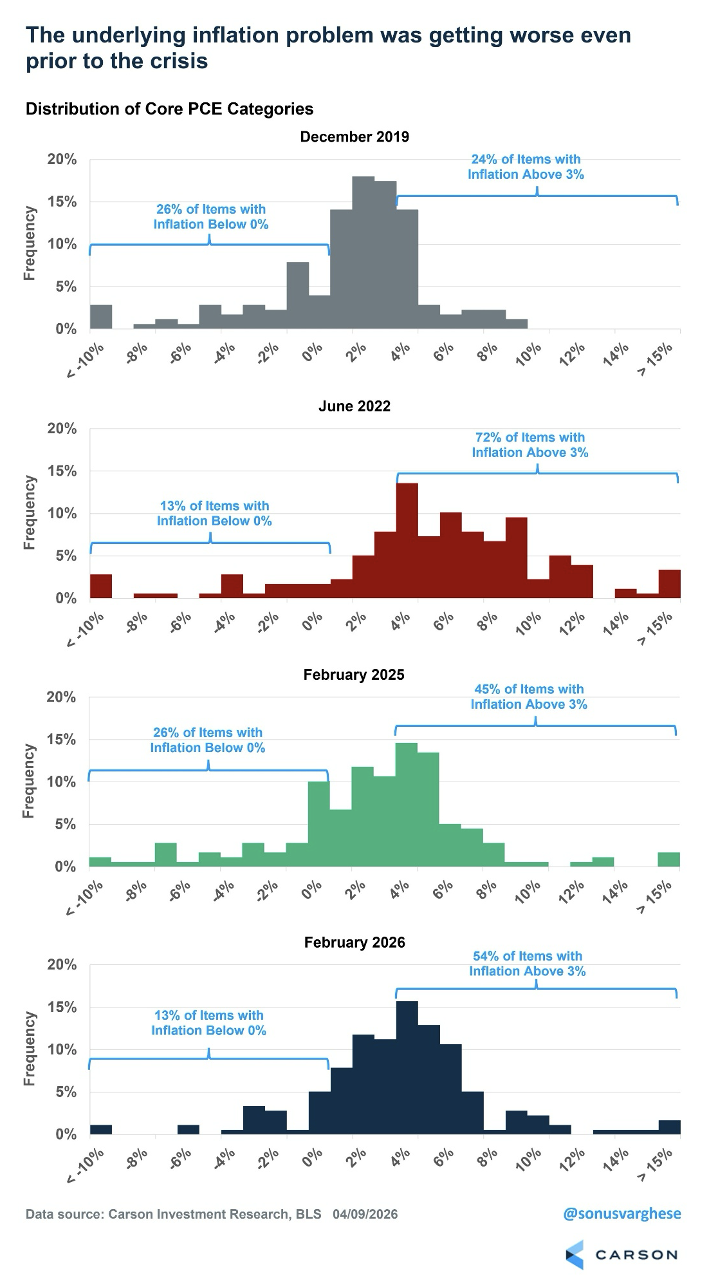

Ten: Underlying inflation data is showing a re-acceleration with core services trending at a +4.1% annualized rate. With 54% of PCE categories now rising faster than 3%, last year’s rate cuts may have been a premature victory lap.

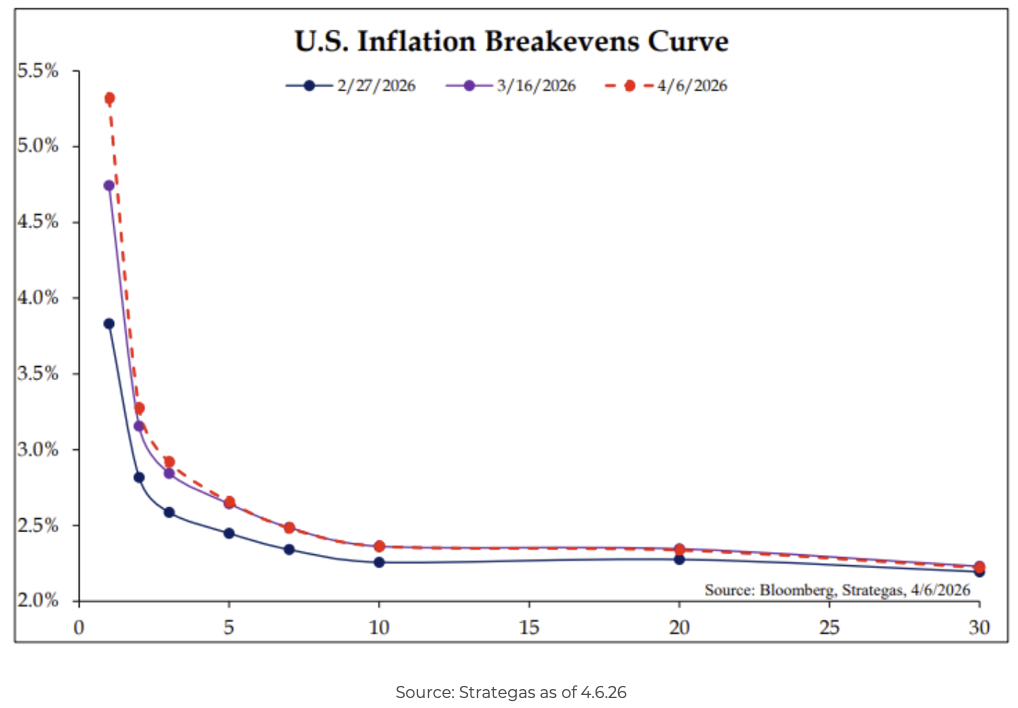

John Luke: So far, inflation fears are heavily front-loaded. Market breakevens show significant concern for the next 12 to 24 months but stay anchored long term, suggesting investors view current price pressures as a transient spike rather than a structural shift.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2604-13.