Our research team parses vast amounts of data daily to identify the signals that truly matter. This week’s selection highlights a concentrated equity rally, the resilience of corporate earnings, and evolving signals regarding consumer health and inflation. Have a great weekend!

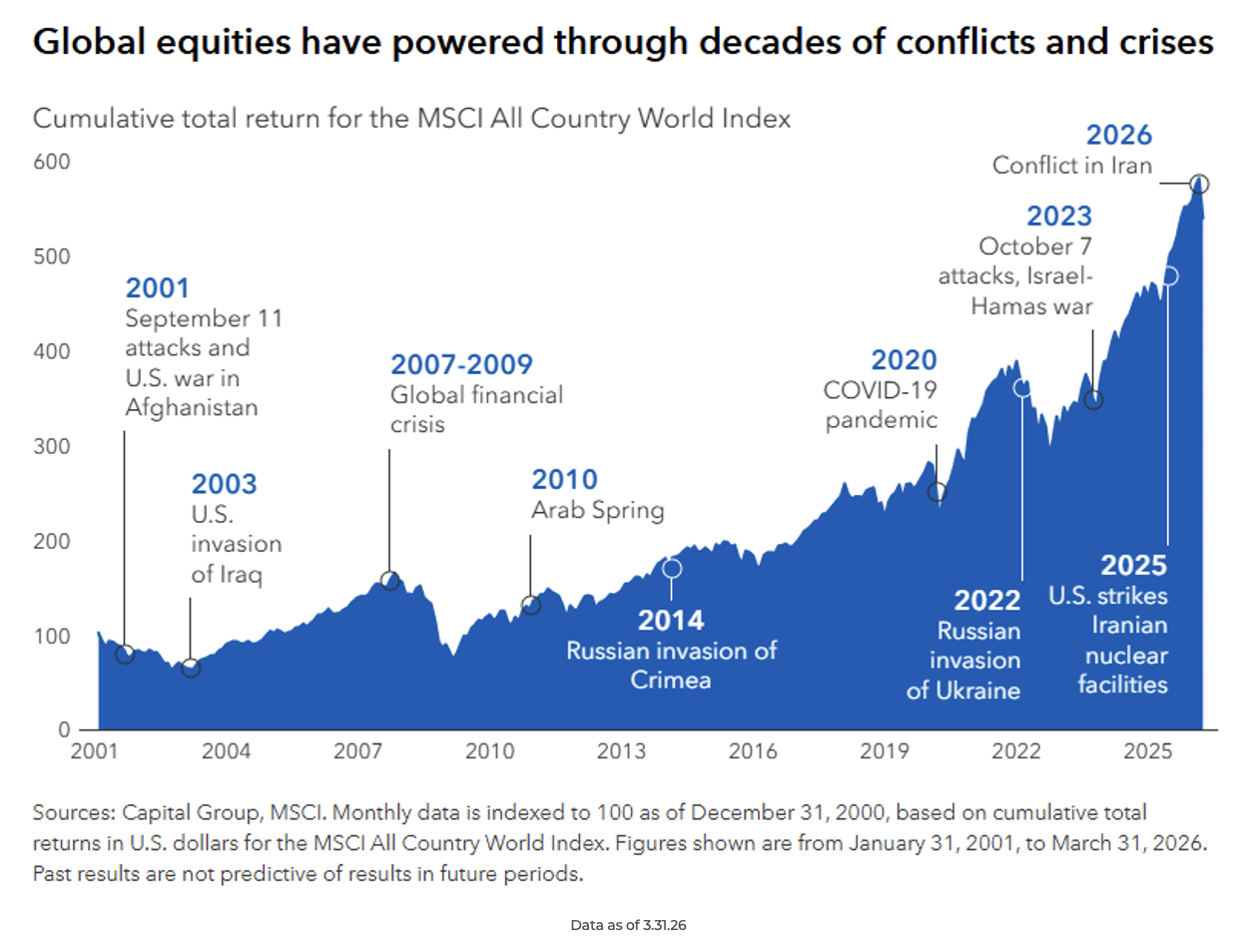

Mark: History is the best cure for geopolitical anxiety. We’ve navigated conflict after conflict over the last 25 years, and time and again, equities have powered through the noise to trade higher.

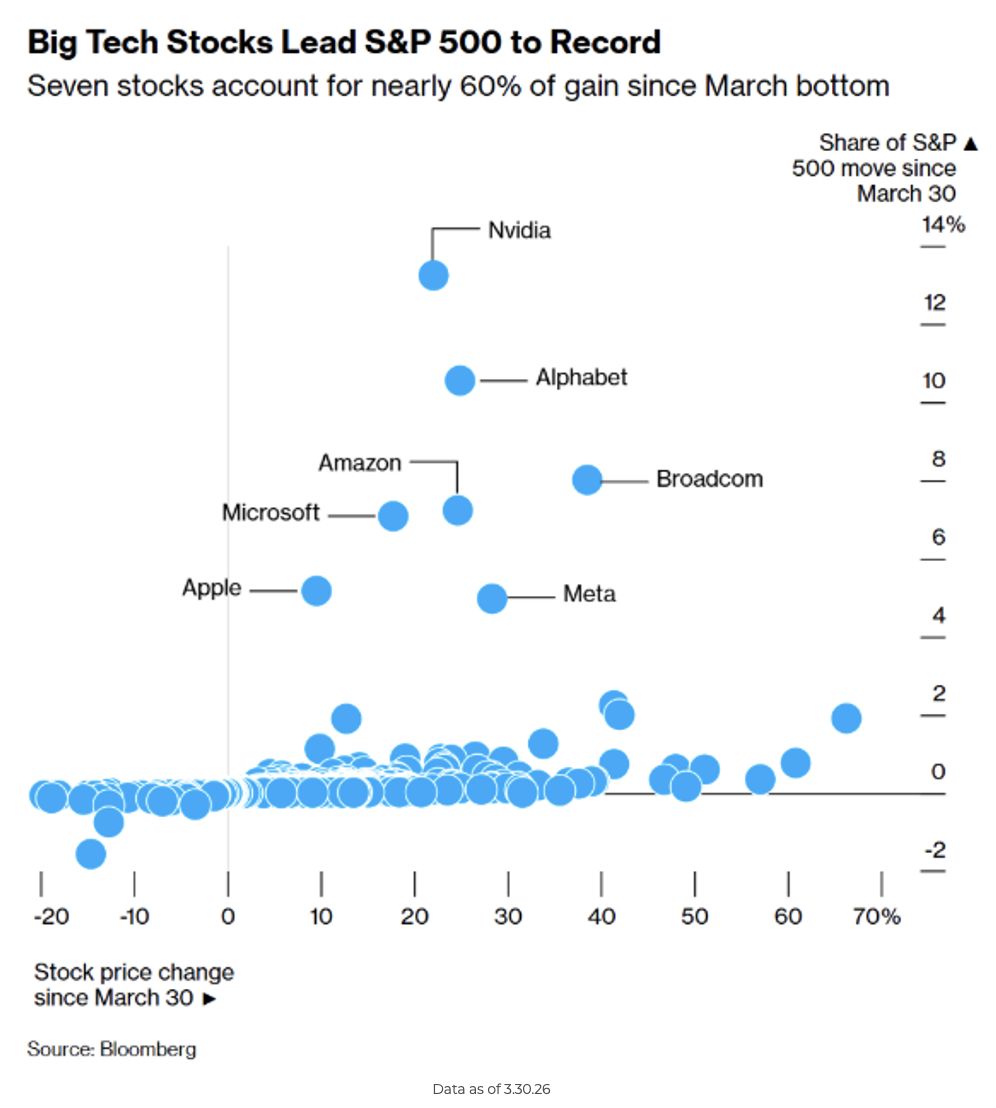

Joseph: Big Tech is back, powering the S&P 500 to new highs. Since bottoming on March 30th, the “Magnificent Seven” have surged 20%, effectively reversing their decline from the October peak and signaling that the rally has room to run despite geopolitical noise.

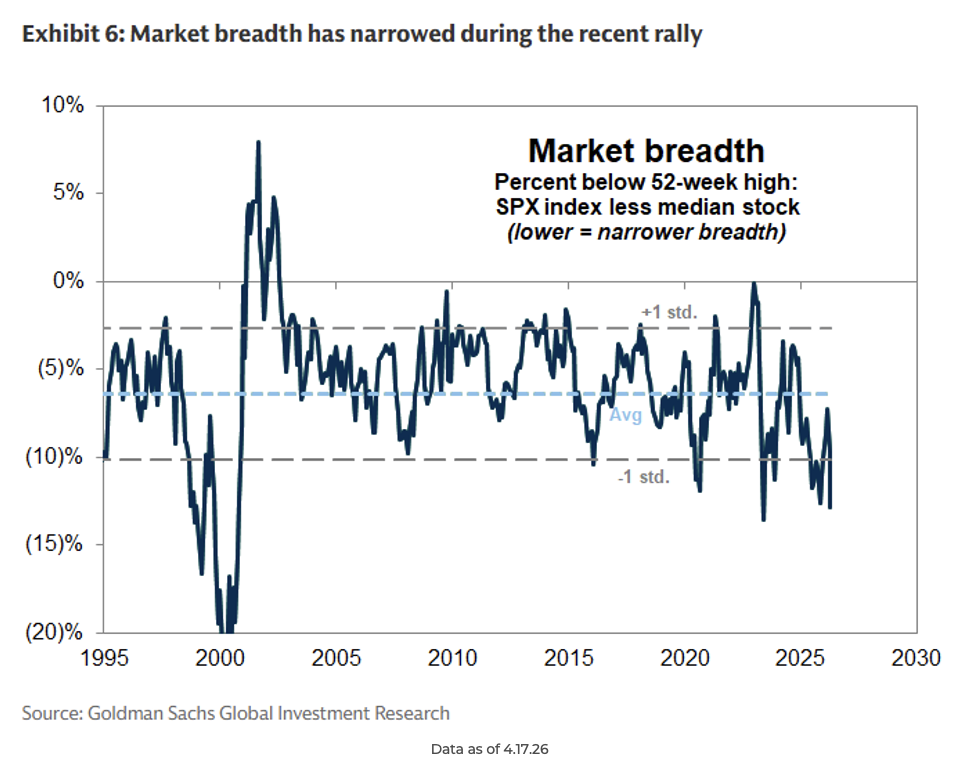

Dave: The rally, however, is incredibly narrow. Market breadth has dropped to its lowest level since mid-2023, with Tech and Communication Services accounting for roughly 70% of the S&P 500’s 12% rebound since late March.

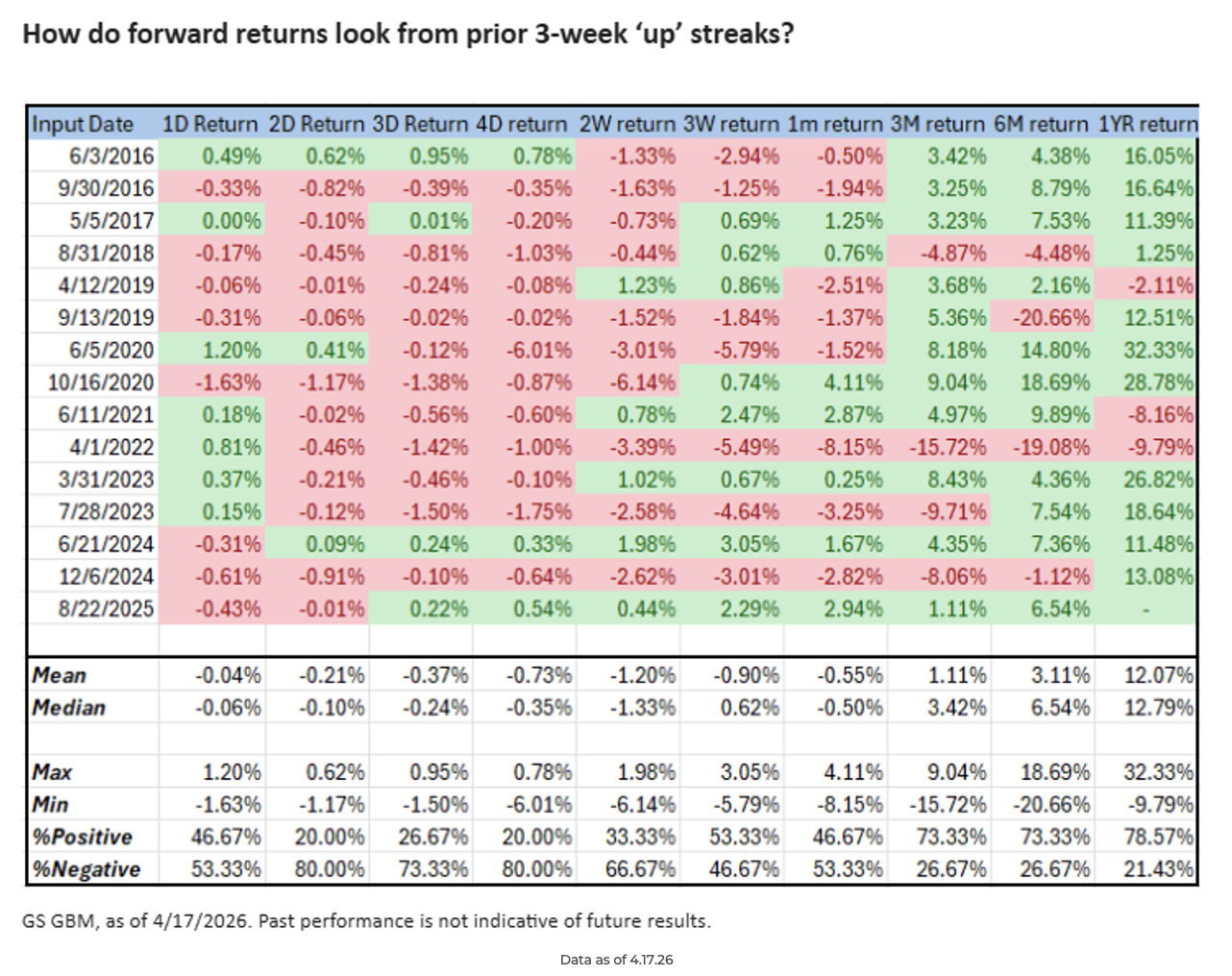

JD: History suggests caution is warranted after such rapid ascents. Over the last decade, following a 3-week “up” streak, the market has often given up short-term gains, though one-year returns have remained strong.

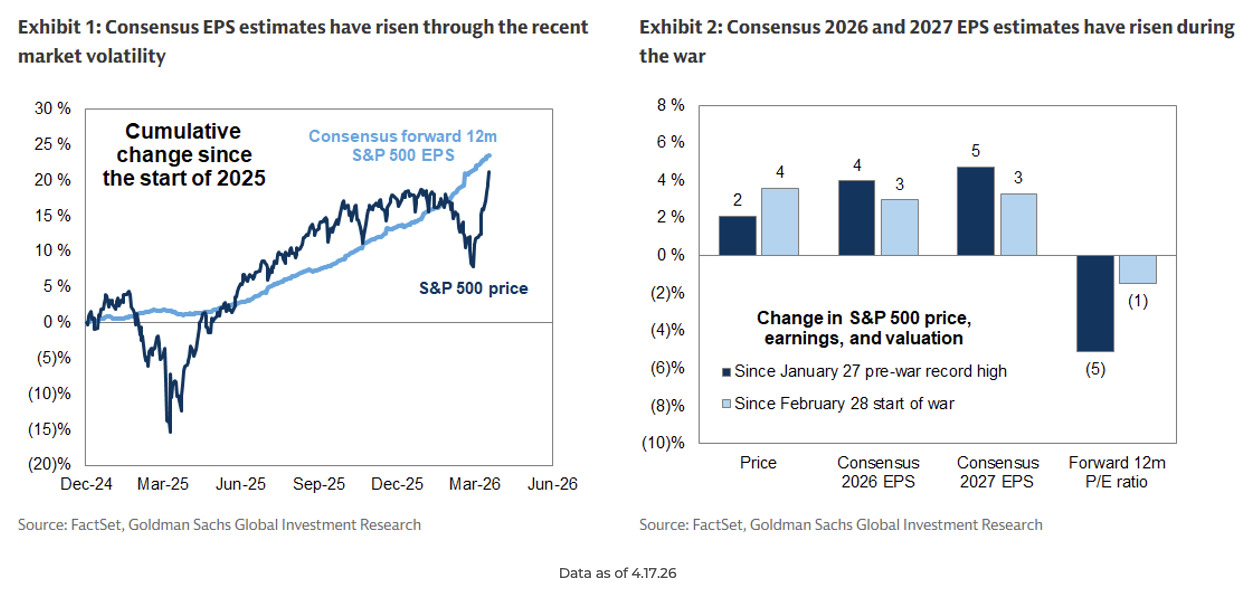

Brian: A resilient earnings outlook provides the fundamental underpinning for this rally. Despite the war in Iran, S&P 500 earnings estimates for 2026 and 2027 have risen 3%, bringing our forward P/E multiple down to 21x. 5% lower than where we started the year.

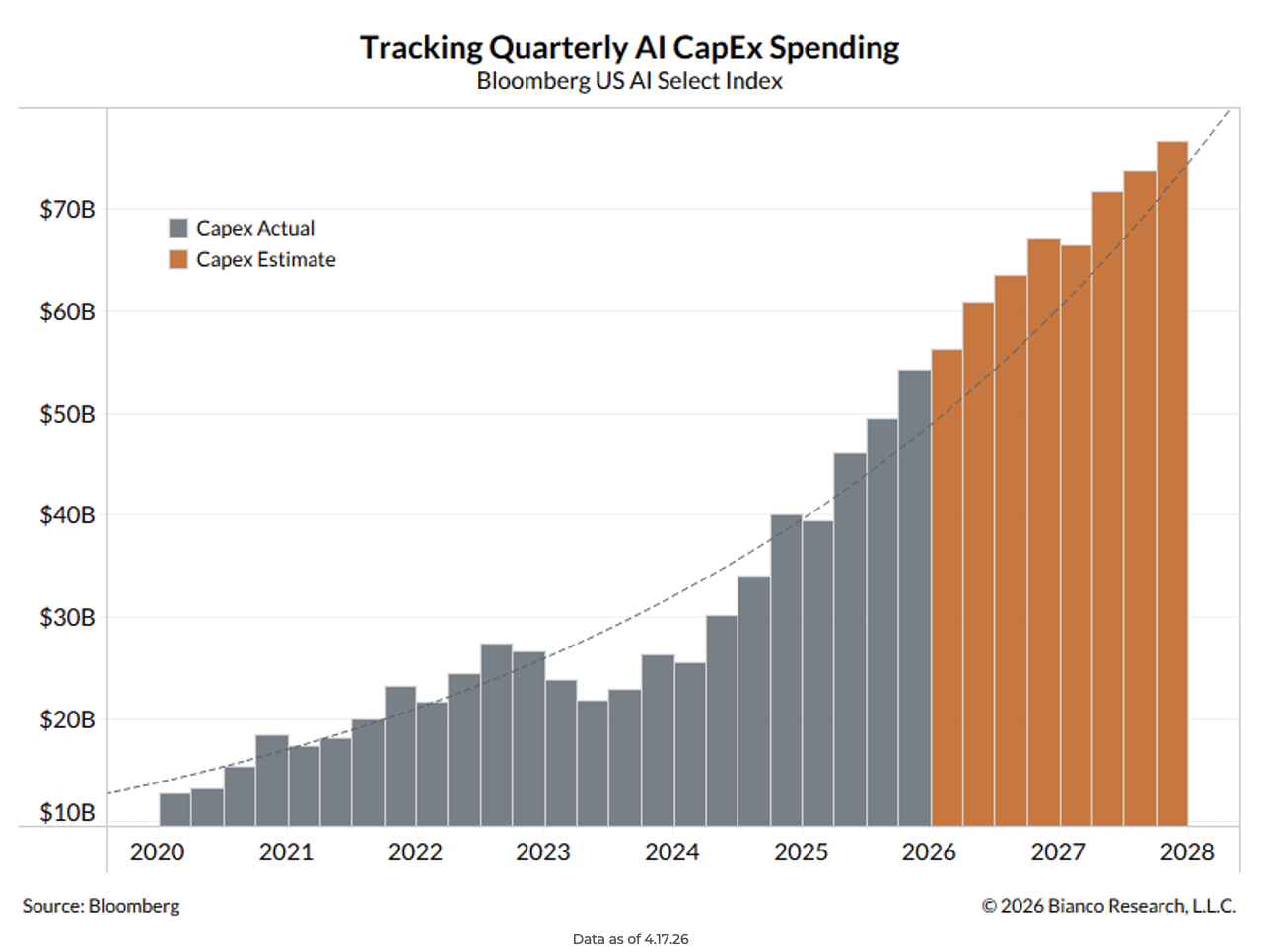

Jake: It’s all capex. Actual and realized quarterly AI spending continues to ramp higher, fueling that growth.

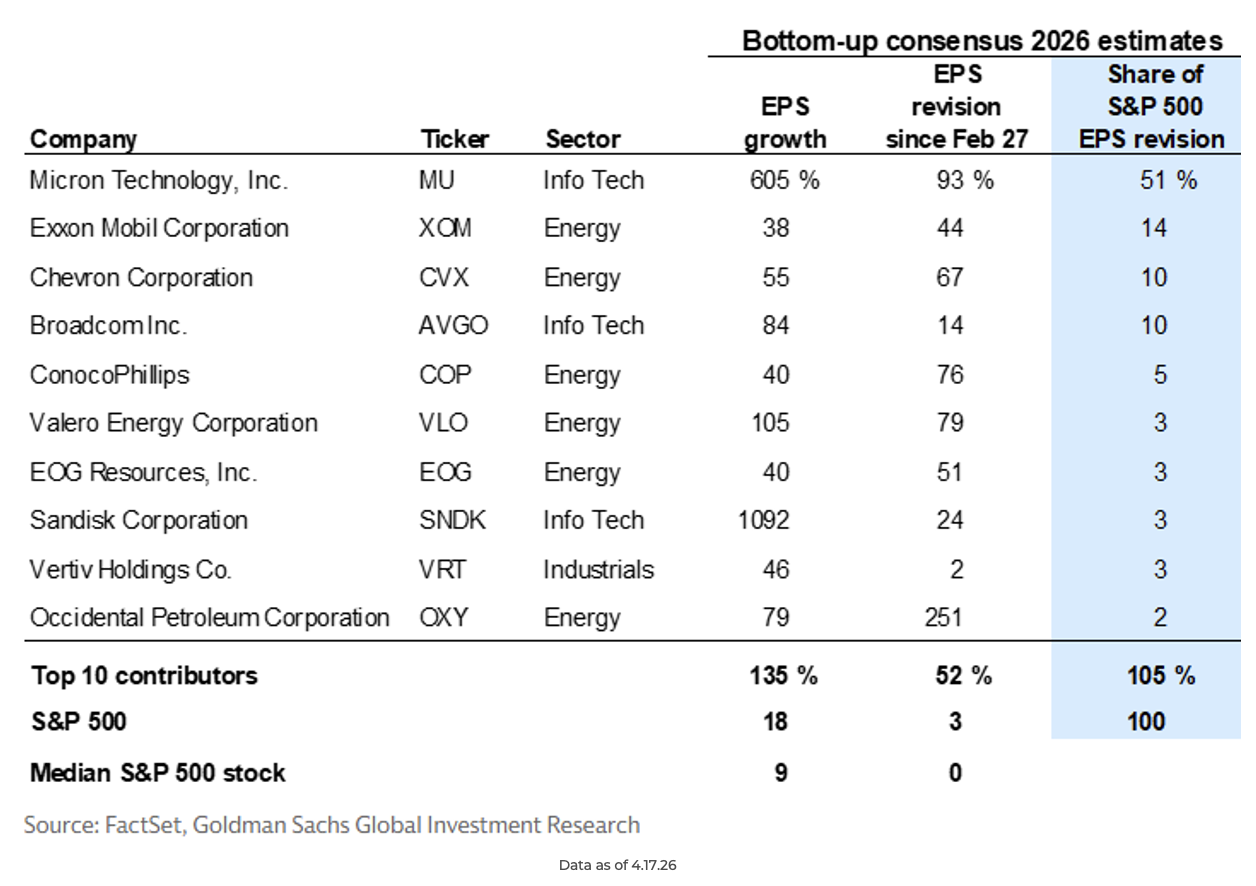

Derek: Micron Technology has been the standout performer, contributing over half of the S&P 500 EPS revision since the start of the conflict.

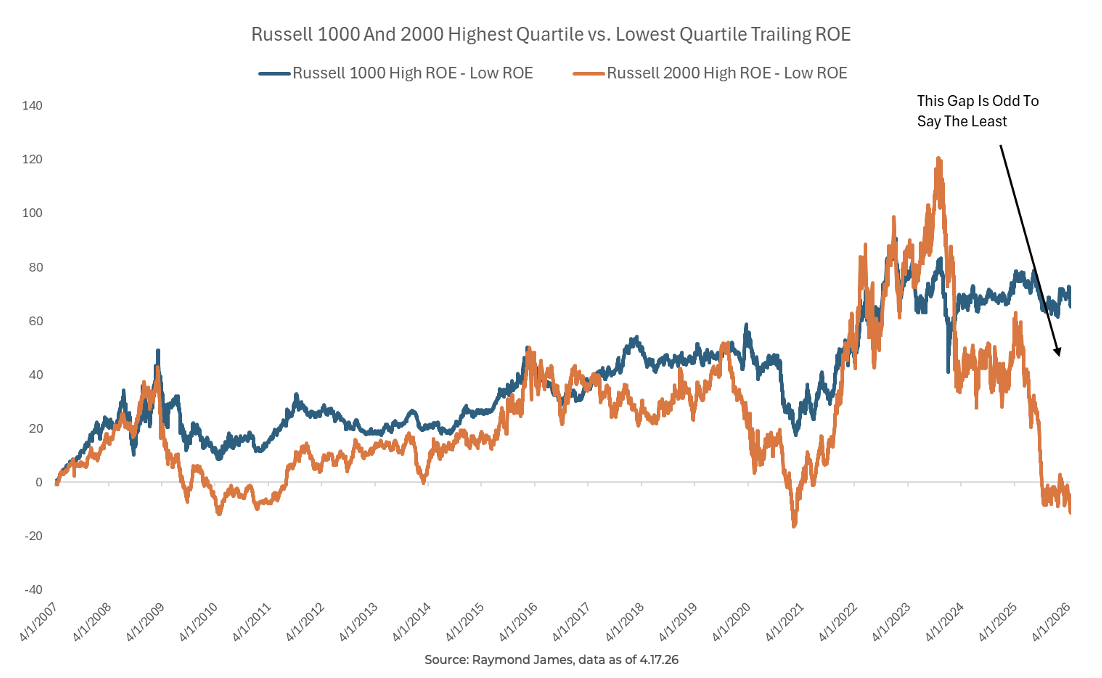

Brad: Regarding small caps, we are seeing a 20-year triple bottom in quality. The gap between the highest and lowest ROE in the Russell 2000 has plummeted, consistent with an extreme early-cycle recovery.

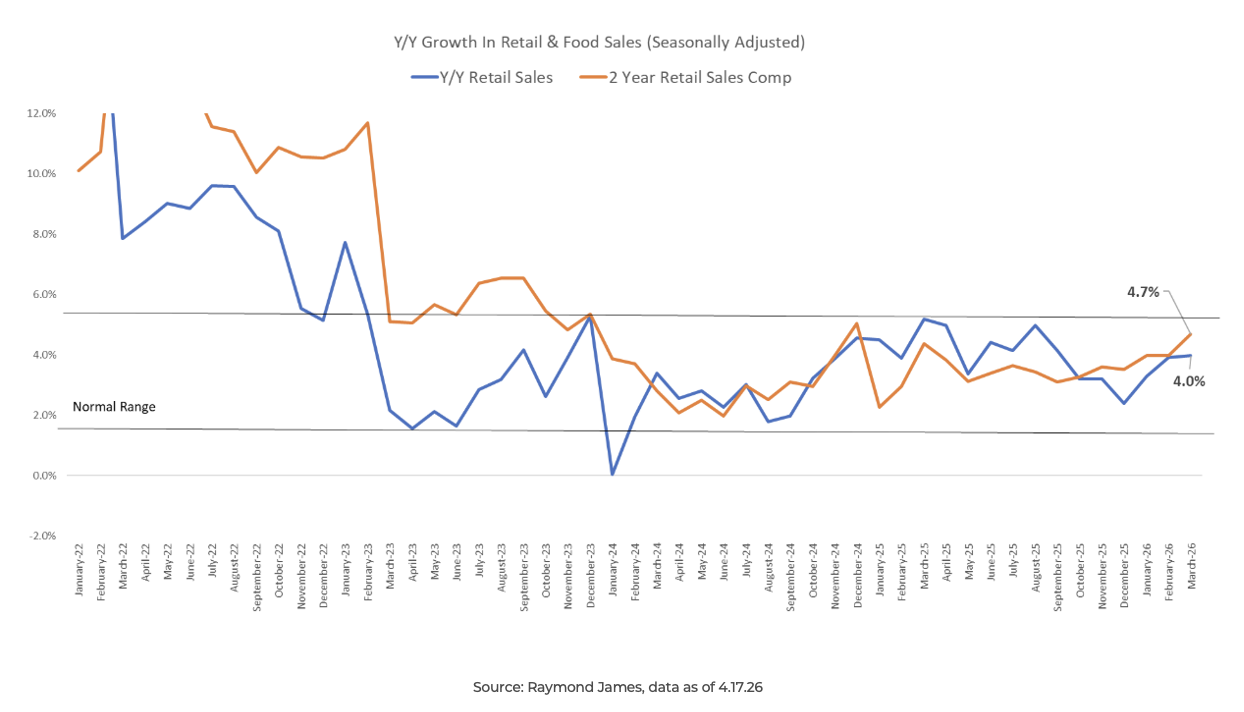

John Luke: Retail Sales were stronger than expected in March. While the gas spike created a ~$10–$15 billion headwind, this was offset by a ~$30 billion+ tailwind from tax refunds and lower withholding, keeping consumer spending broad.

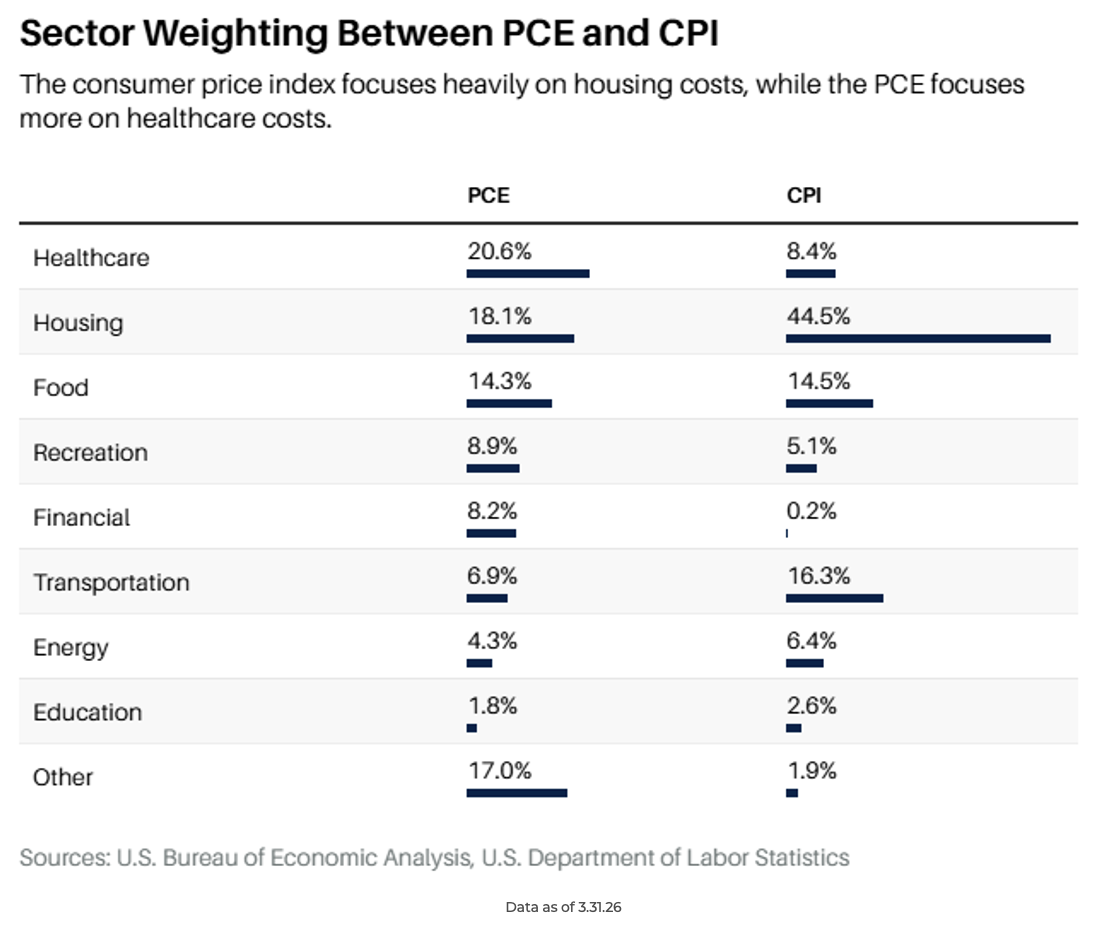

Brett: What matters to the Fed matters to investors. With PCE data coming in hot, many economists are abandoning their rate-cut outlooks for the remainder of the year.

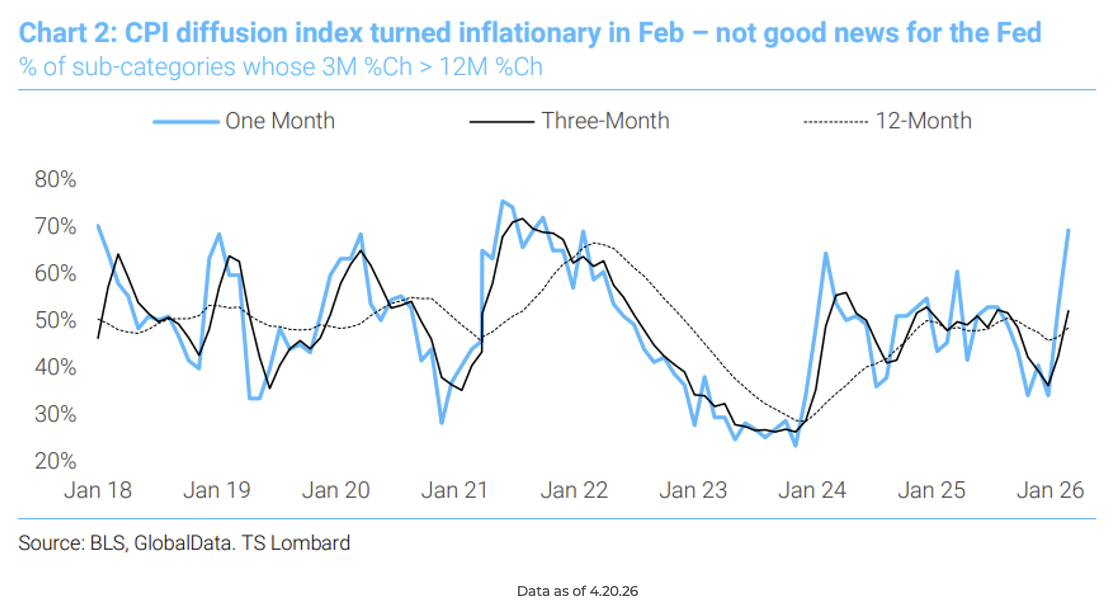

Beckham: The concern is the “2.5% inflation bottom” is likely in, and from here, it could be “up, up and away.” The CPI diffusion index jumped in the last two months, and unless a recession takes hold, it will be difficult to reverse this trend.

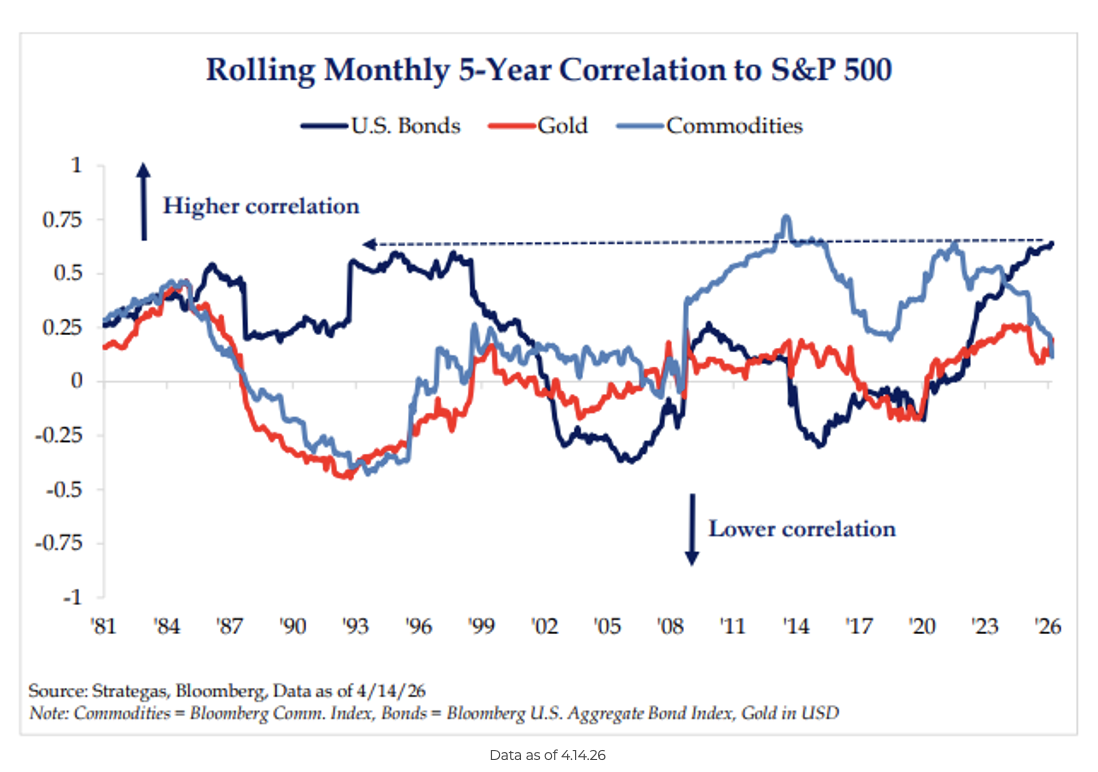

Ten: Diversification is getting harder. The correlation between the Bloomberg Bond Agg and the S&P 500 is now at its highest level since the late 1990s, making traditional 60/40 hedging less effective than before.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2604-24.