Our team looks at a lot of research throughout the day. Here are a handful that we think are good summations of investor activity, from a choppy S&P 500 to wild individual stock rotation, to mixed feelings around inflation and jobs, and a renewed enthusiasm for small cap stocks. Have a great long weekend!

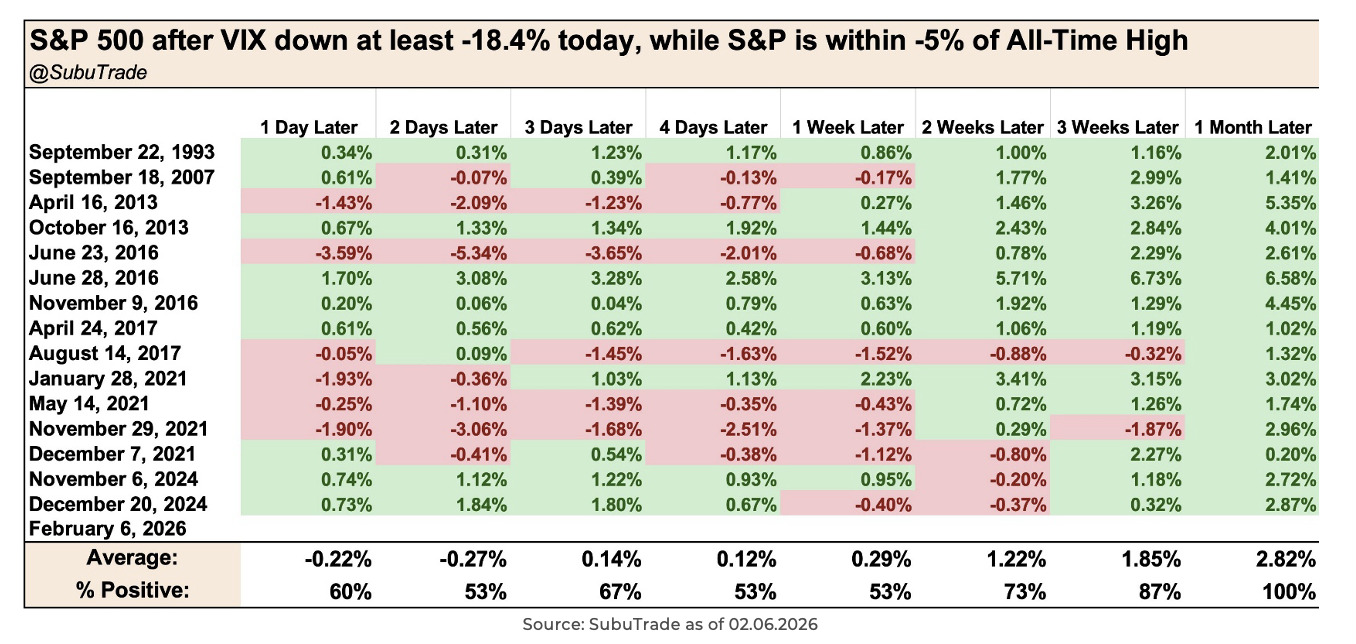

John Luke: The VIX just experienced one of its most dramatic single-day retreats in history. Historically, when volatility collapses this sharply while the market is near all-time highs, it has served as a powerful green light for equities over the following month.

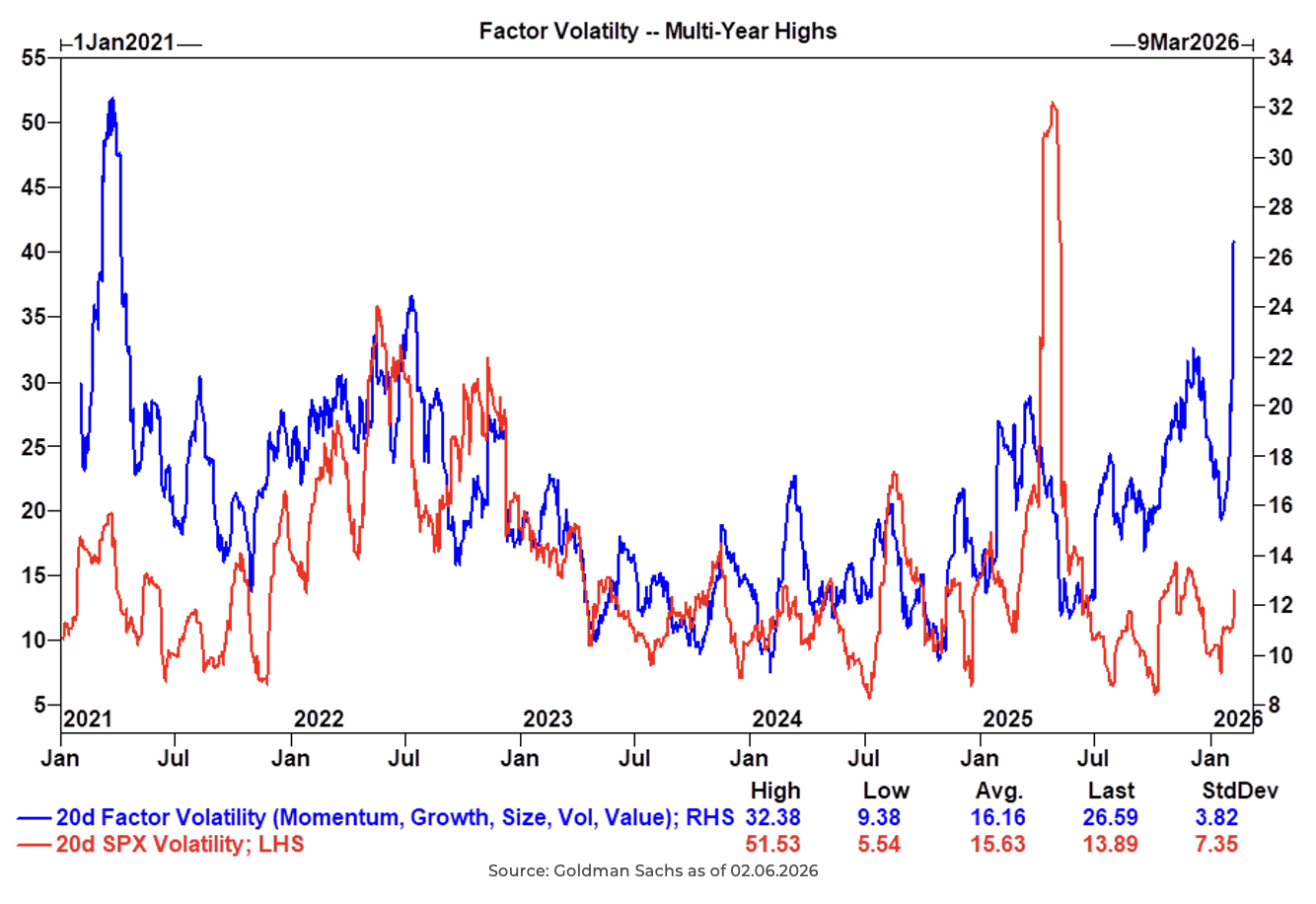

Brad: While the surface level had looked calm, the internal “violence” has been significant. We just witnessed a spike in factor volatility across Momentum, Growth, and Value to levels not seen since the 2021 meme-stock era. This suggests a massive, rapid unwinding of crowded positions and a real struggle for leadership at the single-stock level.

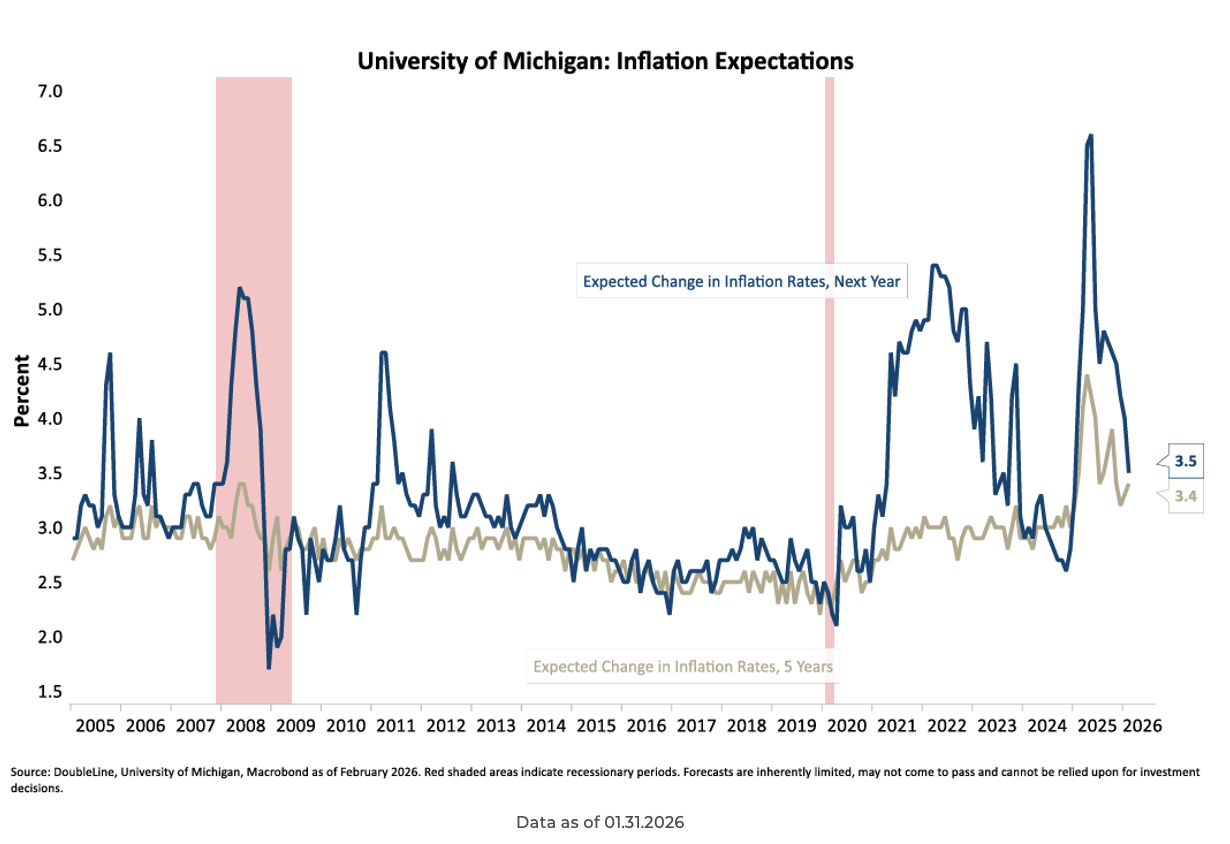

Brett: Inflation expectations are continuing to cool. While still high by historical standards, the clear downward trend in both near and long-term outlooks is a major development. This “fever break” provides the Fed with the breathing room necessary to consider a more accommodative stance.

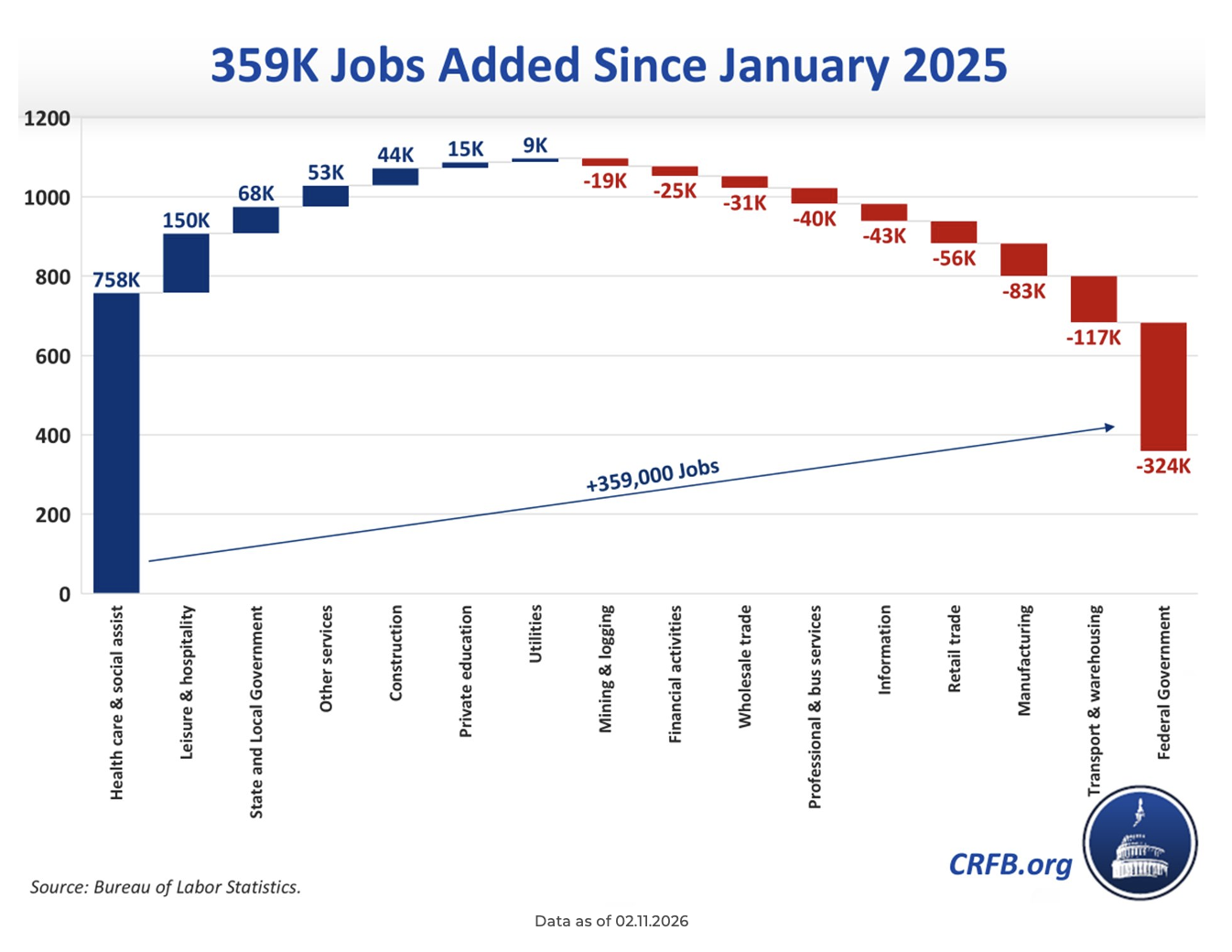

Brian: While the economy and markets continue to perform, there is less optimism around the job market. Nearly the entirety of our recent job growth over the past year has been concentrated in healthcare. Without this specific sector, the broader economy would be showing net job losses over the year. This is a trend that bears watching as AI begins to impact productivity.

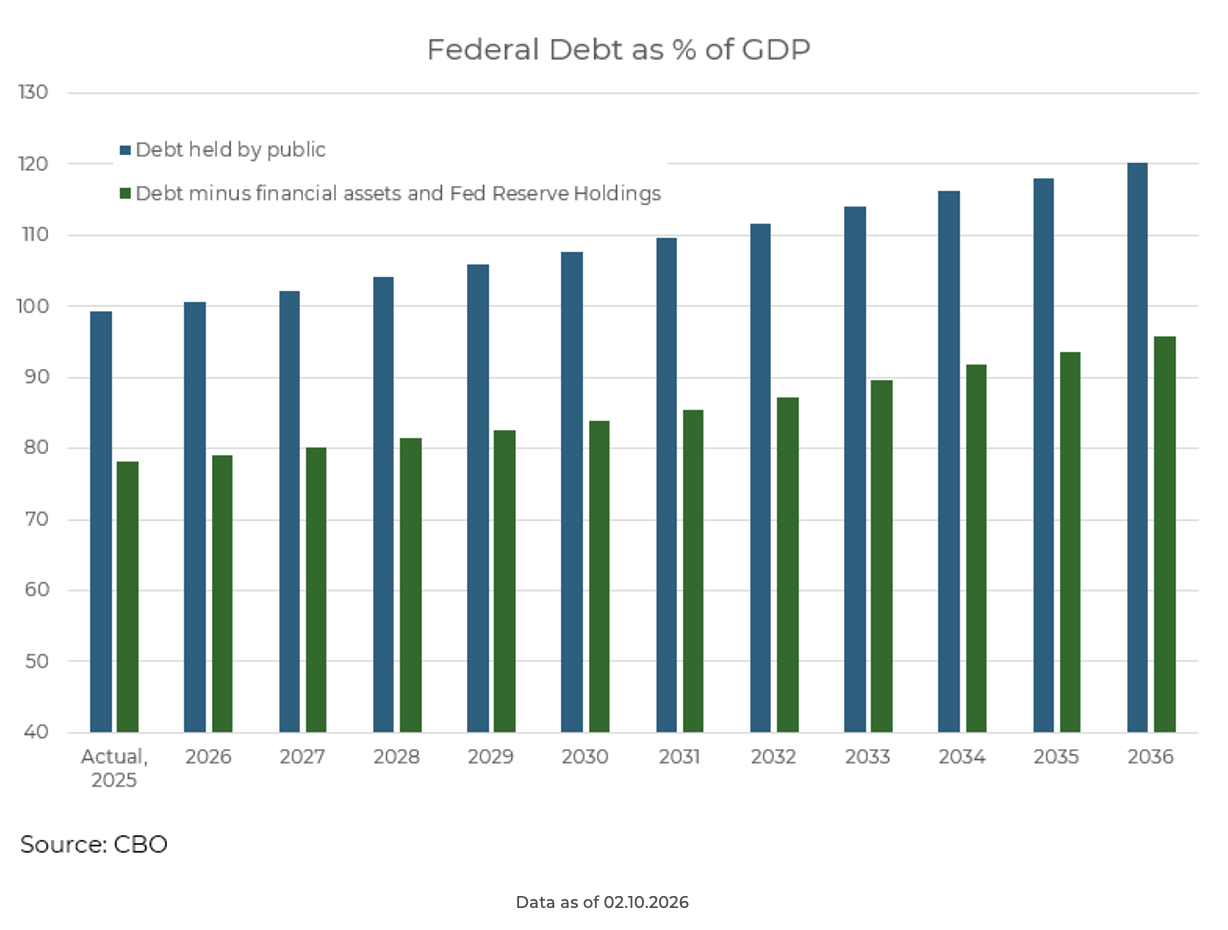

John Fox: Washington does continue to be supportive of the economy with a deficit that grew year-over-year and no end in sight per forecasts. We are on a trajectory where debt-to-GDP will climb relentlessly over the next decade as fiscal discipline remains absent.

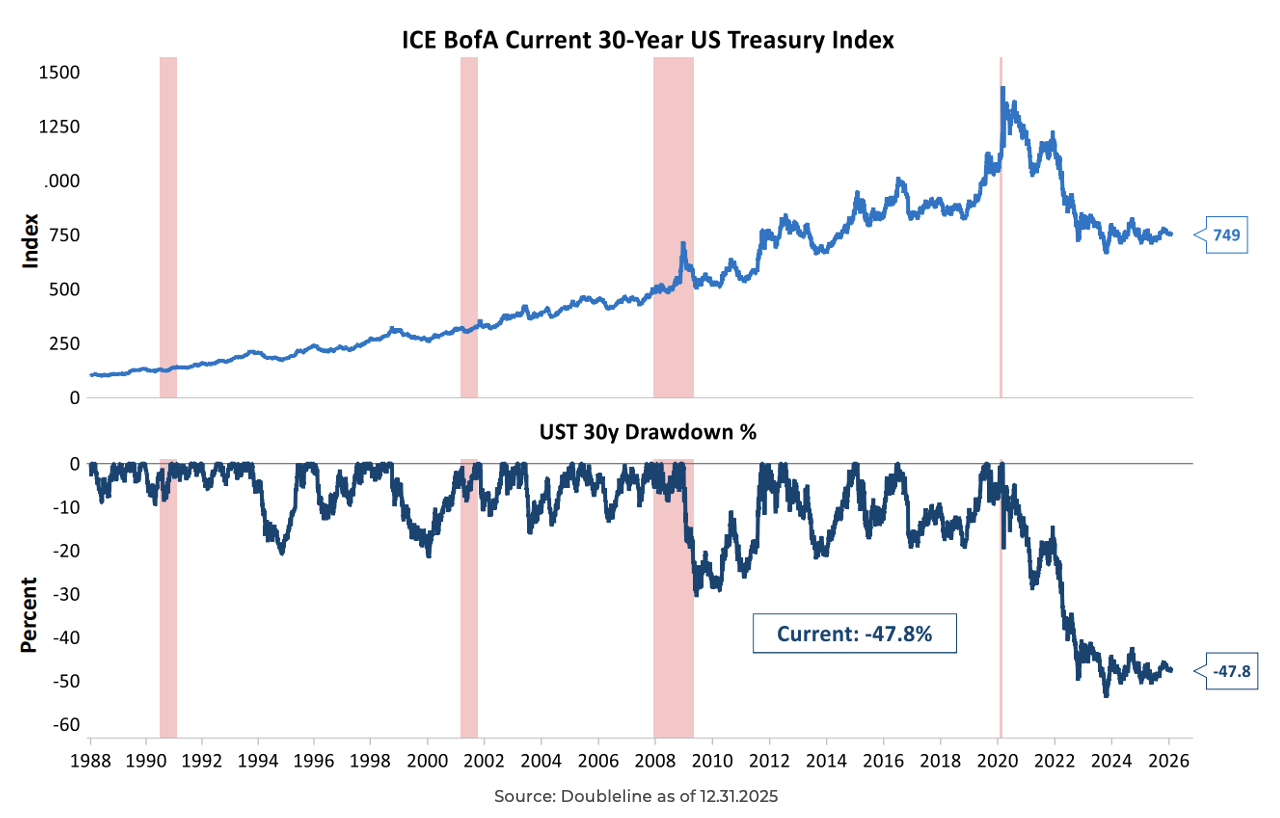

Derek: This Treasury issuance (following the zero interest rate policy “ZIRP”) in part led to a bear market in bonds that has been historic in its severity. Even with the recent stabilization, long-duration Treasuries are still mired in a 50% drawdown from their 2020 peak. When you weigh the equity-like volatility against the less efficient tax treatment of interest, the “safety” of long bonds remains a difficult sell.

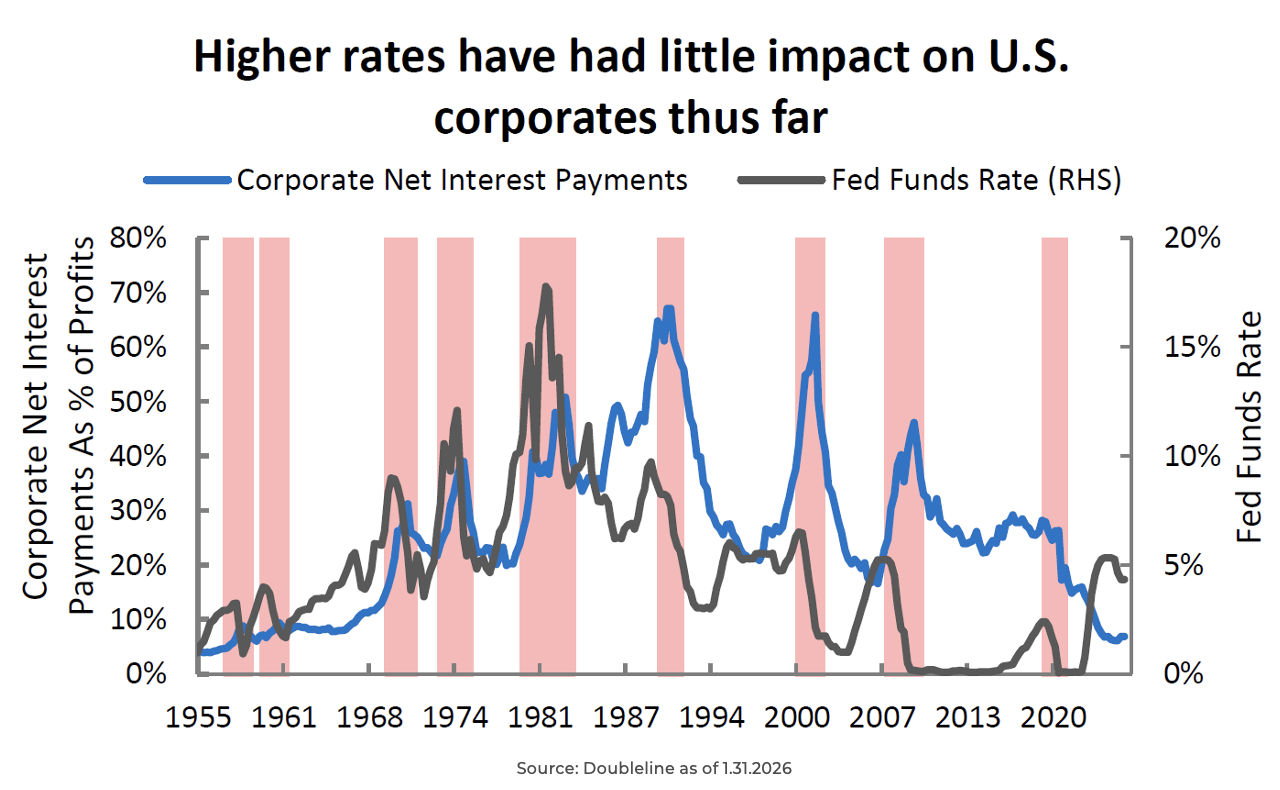

JD: Despite a rapid rise in interest rates, corporate America hasn’t felt the sting. Most large firms were smart enough to lock in generational lows years ago, meaning their net interest payments as a percentage of profits are still sitting near all-time lows. As long as profits continue to soar, the “higher for longer” regime remains manageable for the S&P 500.

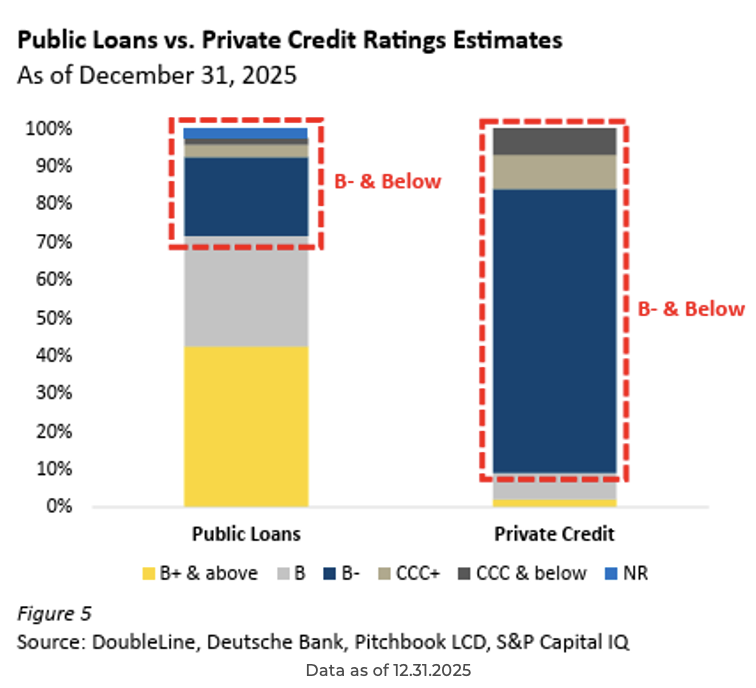

Brad: Private credit has grown tremendously to support corporate financing needs, but what’s been good for corporations may not be what’s good for investors. Investors should be wary of what they are actually buying. Roughly 90% of these private loans are rated B- or lower, meaning the sector has essentially become a massive warehouse for the lowest-tier high yield. The perceived lack of volatility in these books likely masks real underlying credit stress.

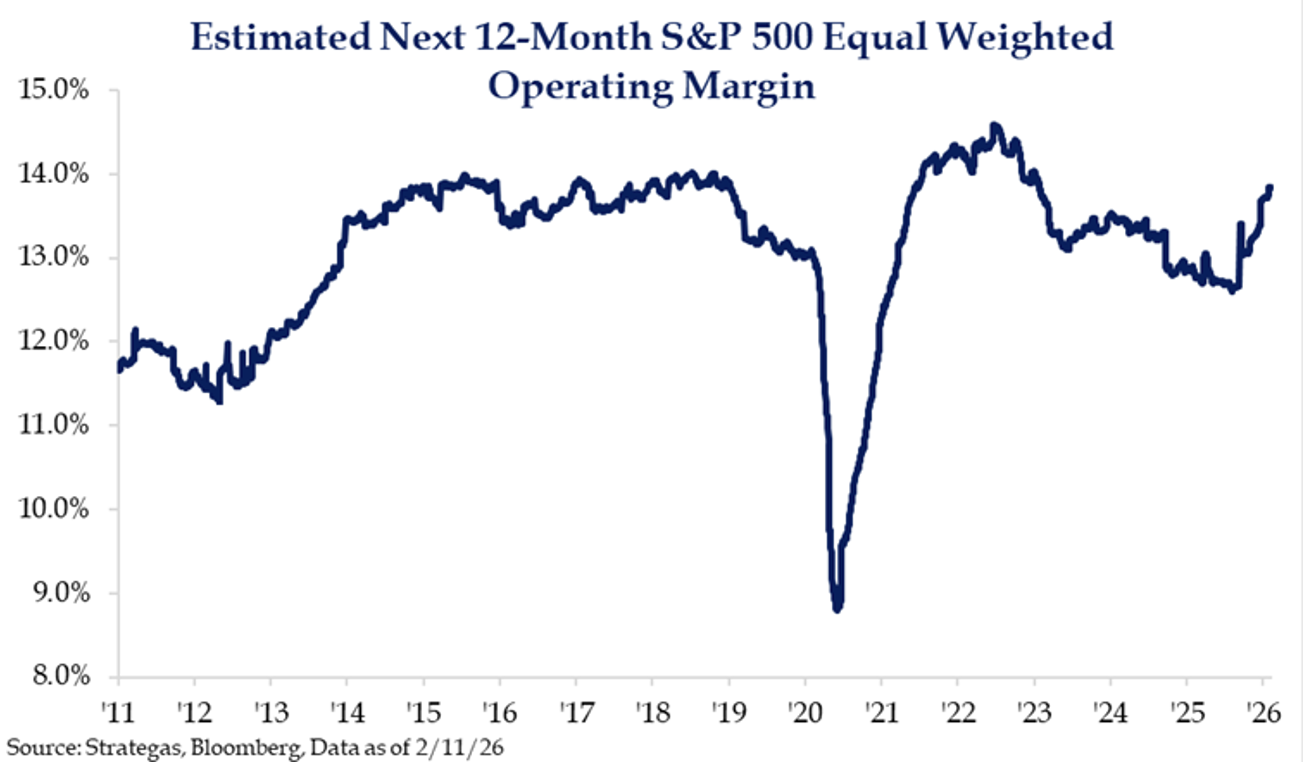

Joseph: We are starting to see some real nice broadening across US equity markets. Profitability is starting to expand beyond the top-heavy tech giants, with early signs of margin expansion within the equal-weighted S&P 500, suggesting that mid-sized and smaller large-cap firms are finding ways to drive efficiency and capture more bottom-line growth.

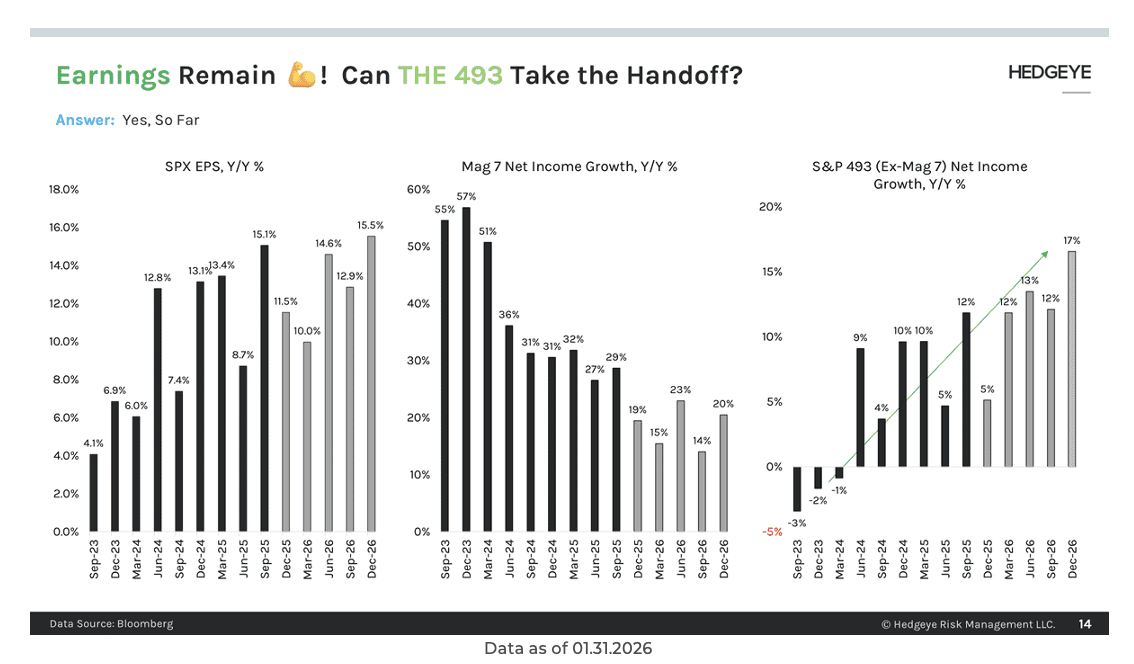

Jake: We are seeing the “handoff” that bulls have been waiting for in income growth, driven in part by these widening margins. While the Magnificent 7 continue to see high, but no longer astronomical growth rates, the other 493 stocks in the S&P 500 are accelerating.

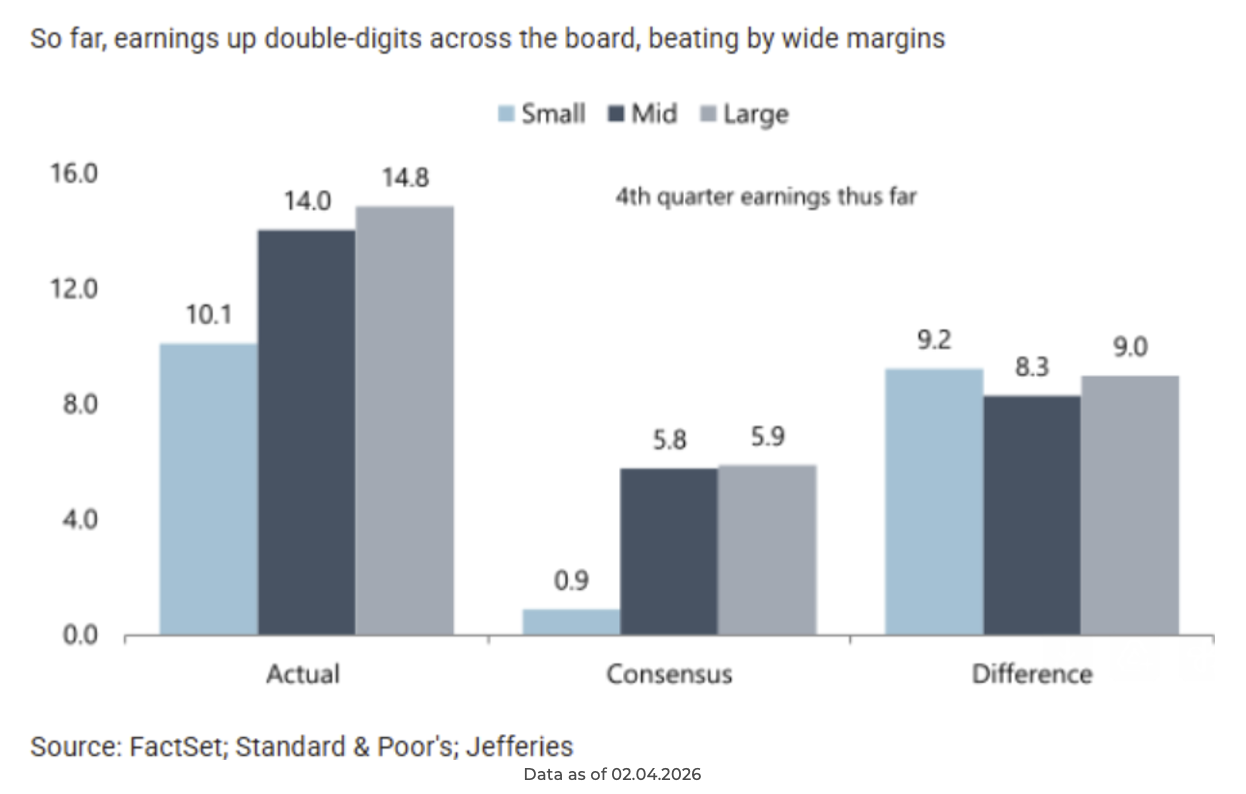

Beckham: Smaller cap companies are also now beating expectations. Earnings that are 9% higher than consensus, suggesting that the “small-cap gloom” may be coming to an end.

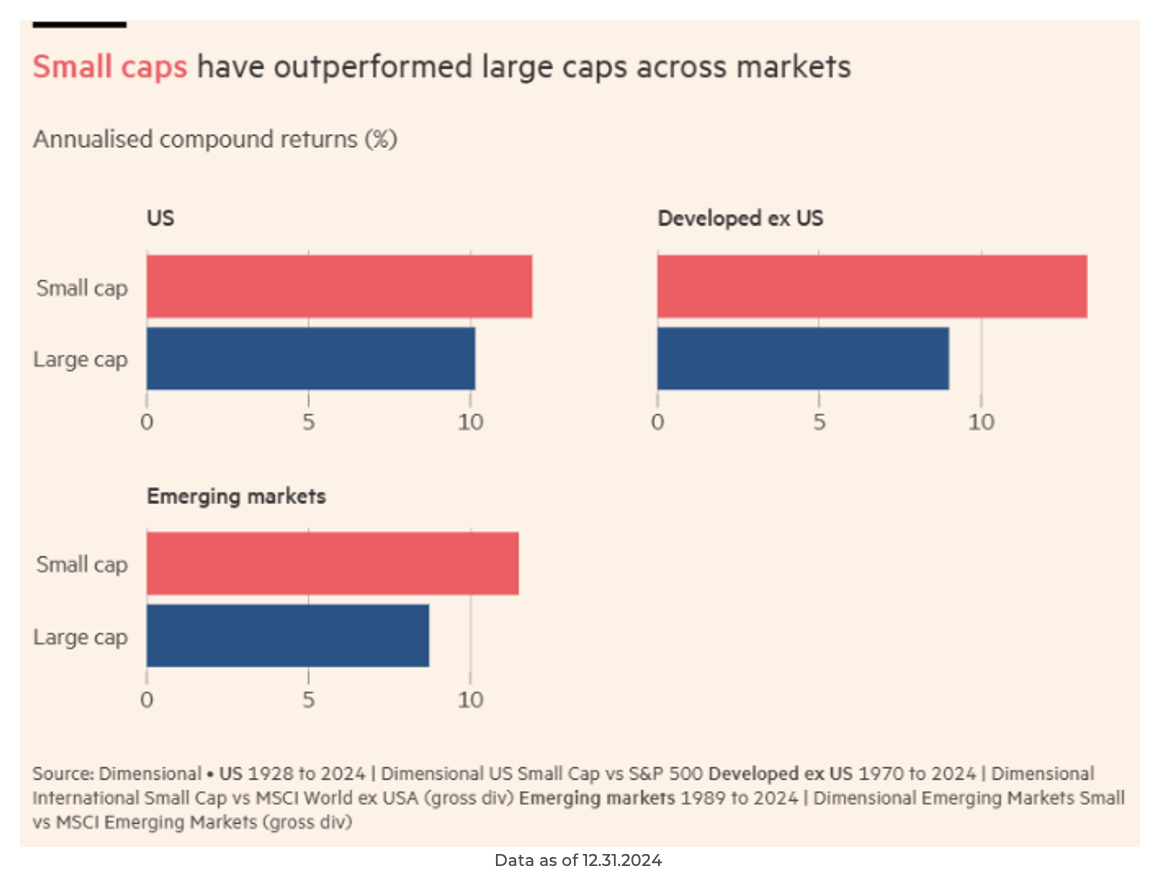

Joseph: The past few years may make it hard to believe, but over the longer term, small-cap outperformance isn’t just a theory; it’s been the global reality for nearly a century. If anything, the recent period of megacap tech dominance is the historical outlier. If we are truly entering a more “normal” market regime, history suggests the advantage may eventually shift back to the smaller, more agile players.

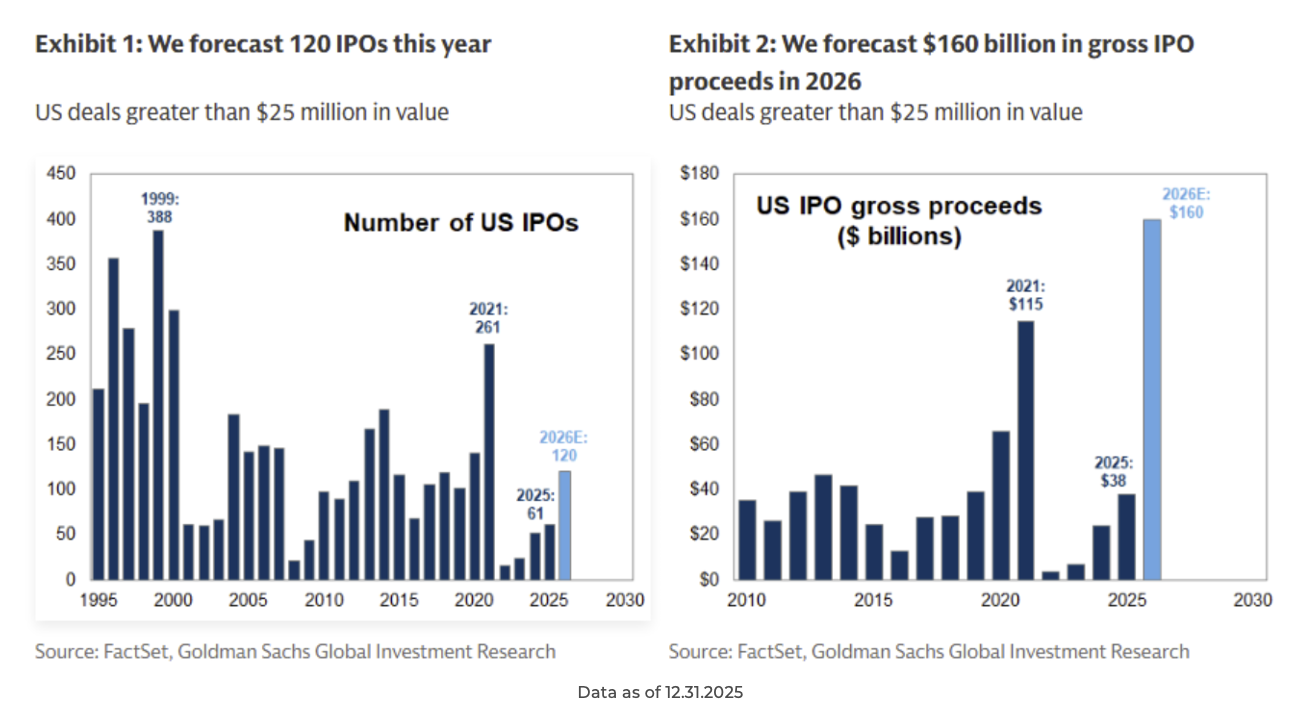

Ten: The upbeat sentiment of smaller companies is turning into “animal spirits” in the primary market. After a long drought, forecasts are for a surge in IPO activity that could rival pre-pandemic levels. This influx of new companies and capital is a clear signal of growing investor confidence in the long-term growth outlook.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2602-13.