Our team looks at a lot of research throughout the day. Here are a handful that we think are good summations of investor activity, from market expectations to corporate fundamentals, a resilient economy relative to others, and changes in business over recent decades. Here’s to a great year ahead!

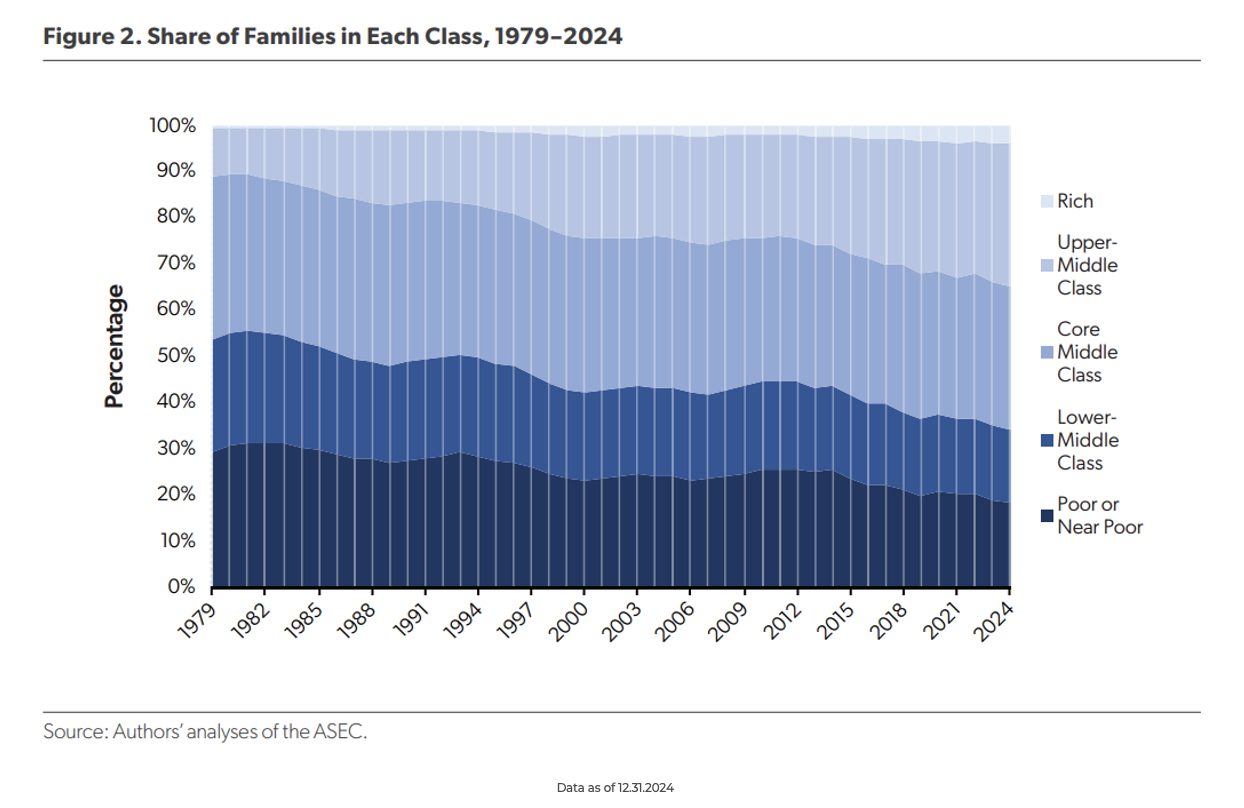

John Luke: We hear a lot about the “death of the middle class,” but the long-term data tells a more nuanced story. The group is getting smaller primarily because people are getting wealthier and moving into the upper-middle or high-income brackets rather than falling into poverty.

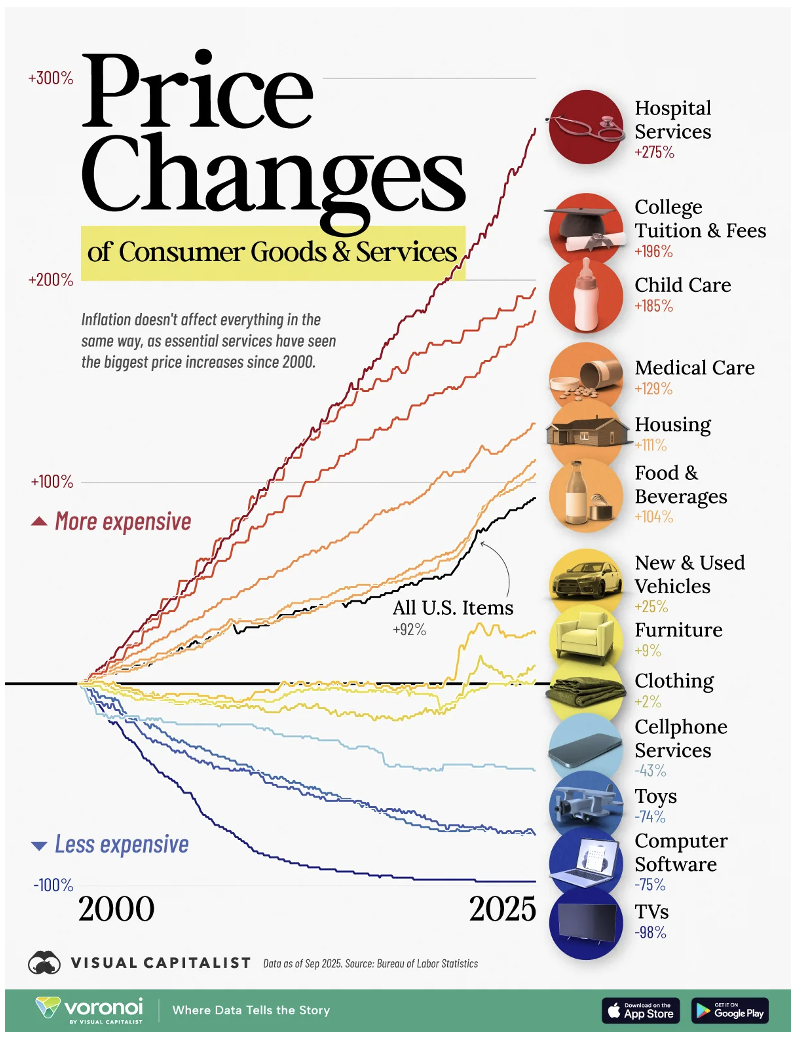

JD: That shifting wealth hasn’t necessarily made life feel cheaper, though. Price changes since 2000 show a massive decline in things that can be digitized or scaled, but a steady rise in things with finite supply or a heavy need for human services.

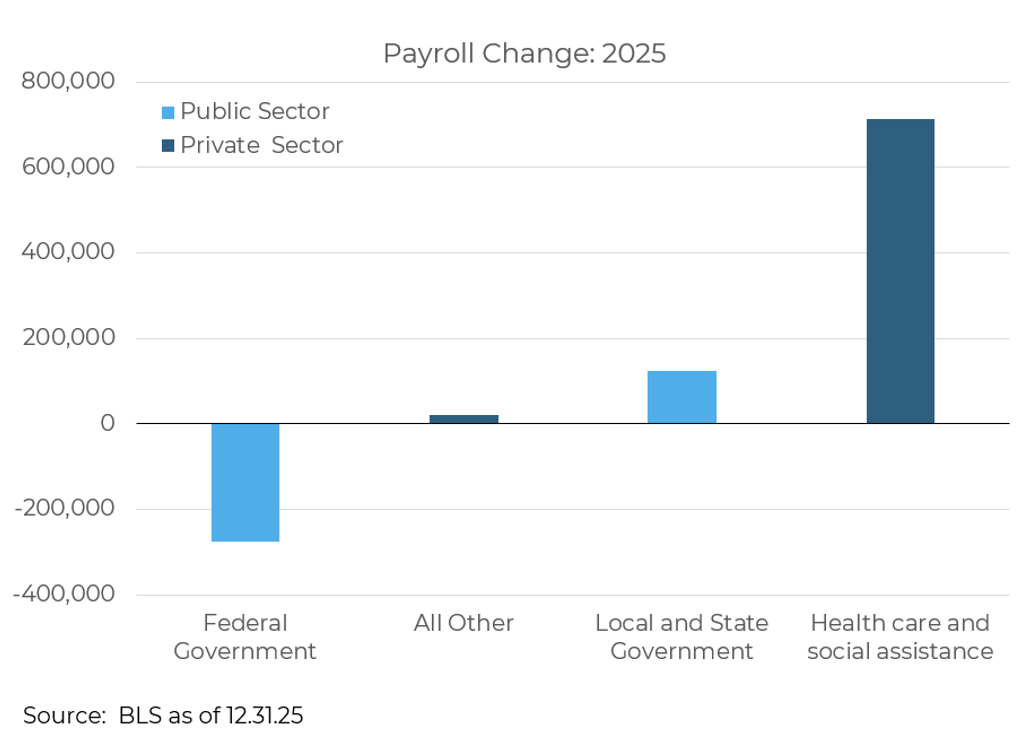

Brian: In terms of recent sentiment, it’s not just prices. One of the most significant structural shifts has been in the structure of the Federal government itself. Payroll data for 2025 came in mixed, but a clear trend is the shrinking of the federal workforce and government services.

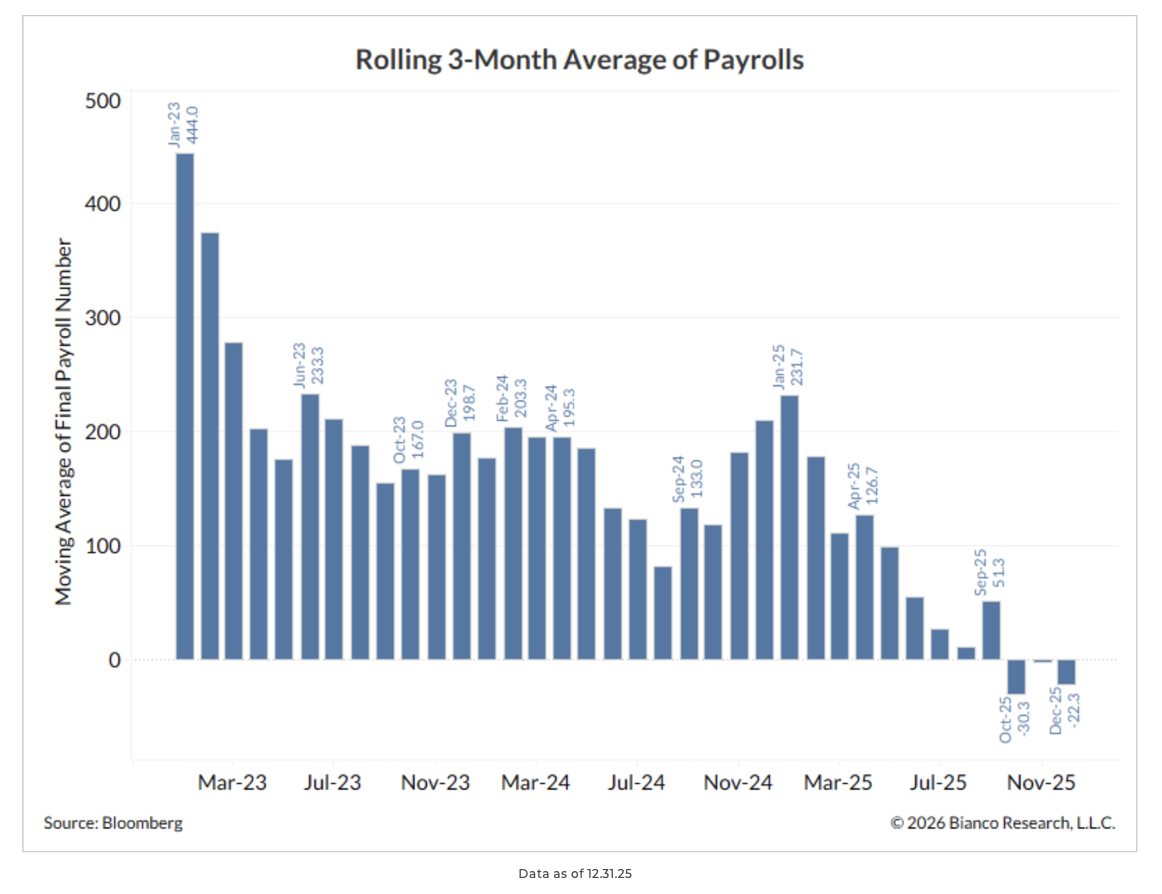

James: Meanwhile, private sector productivity continues to soar, with strong GDP figures even as total payroll numbers turned negative over rolling 3-month periods.

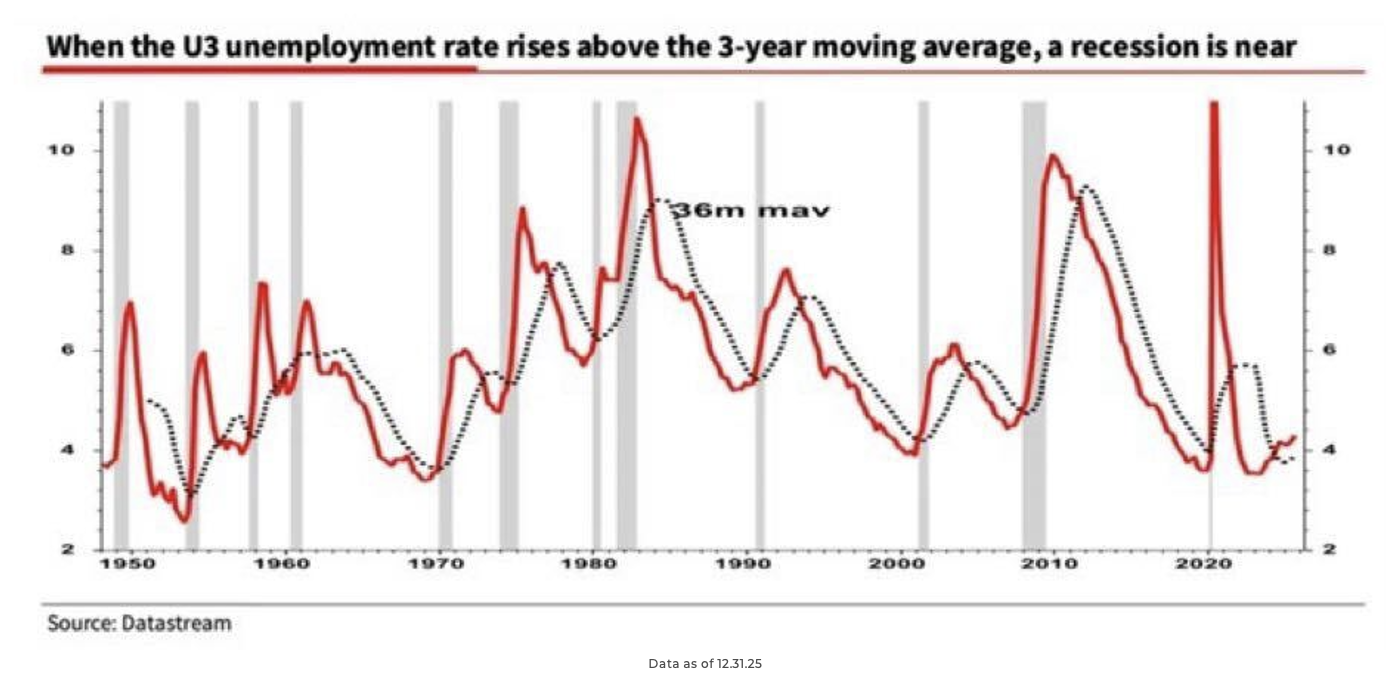

Joseph: This shift in labor dynamics is raising red flags for some. Historically, a rise in U3 unemployment has been a reliable predictor of recessions. However, things aren’t the same as they’ve been. With major changes to immigration policies and the rapid rise of AI, the old U3 “recession rule” might be broken for this cycle.

Brad: Speaking of the outsized impact of AI, the infrastructure phase is entering a new chapter. The growth in Capex from “hyperscalers” is finally moving lower from its extreme peaks. But don’t mistake slower growth for a lack of spending; the total base is now so high that even lower growth rates can have a large impact on the broader economy.

Dave: It makes me wonder if the market will start treating AI stocks like cyclicals if that Capex spend cools. Usually, you want to buy cyclicals when they look expensive, but it seems less clear if that traditional playbook applies here.

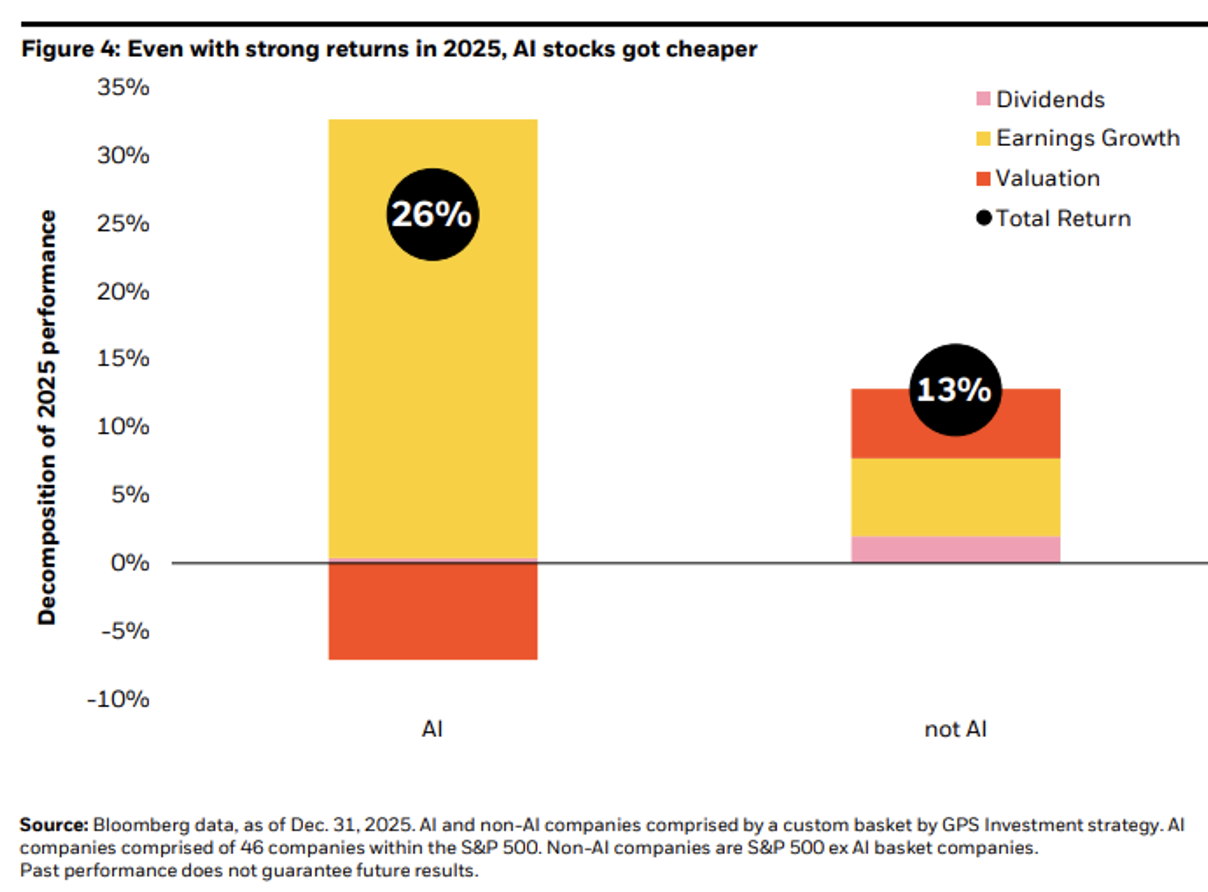

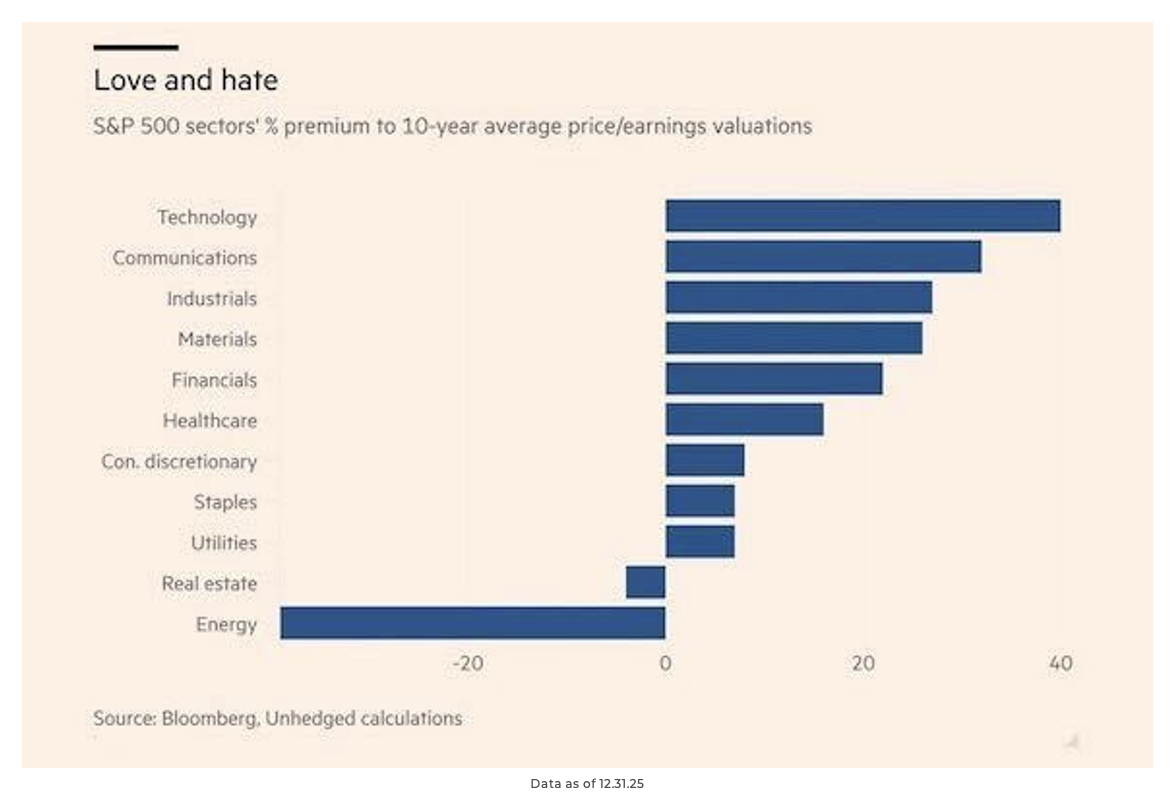

Derek: For now, any view of cyclicality does not show up in the valuations. While Energy remains one of the few sectors cheaper than its historical average, Technology and Communications remain expensive vs history, largely driven by their superior fundamentals.

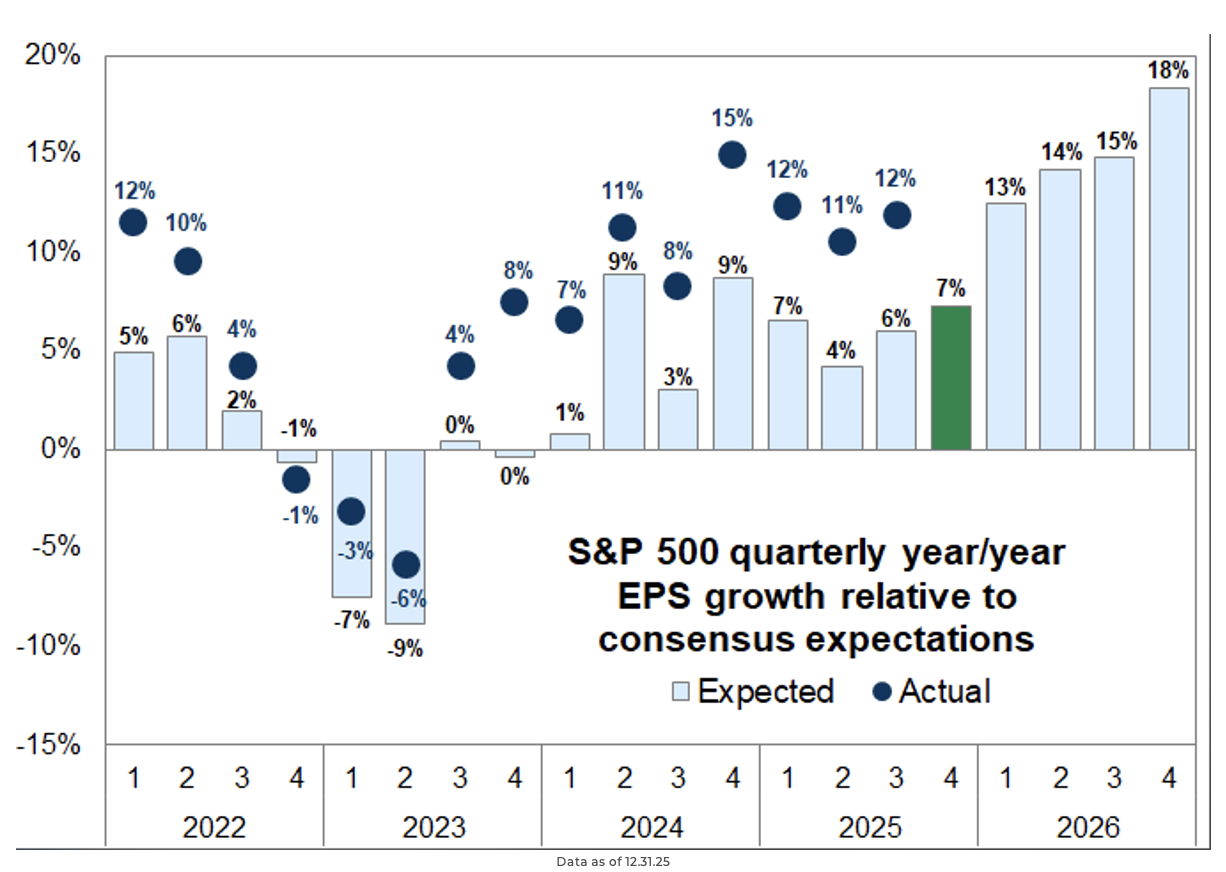

John Luke: As we pivot to the present, investor focus is shifting from macro headlines to micro fundamentals with the start of the Q4 2025 earnings season. But there is a clear “bifurcation” happening. While large-cap earnings expectations have picked up, small-cap estimates have trended lower in recent weeks.

Beckham: Consensus estimates are looking for 7% year-over-year growth for the S&P 500, but given that earnings have beaten expectations by an average of 6% in the first three quarters of 2025, these estimates might be too low again.

Source: Bloomberg

Source: Bloomberg

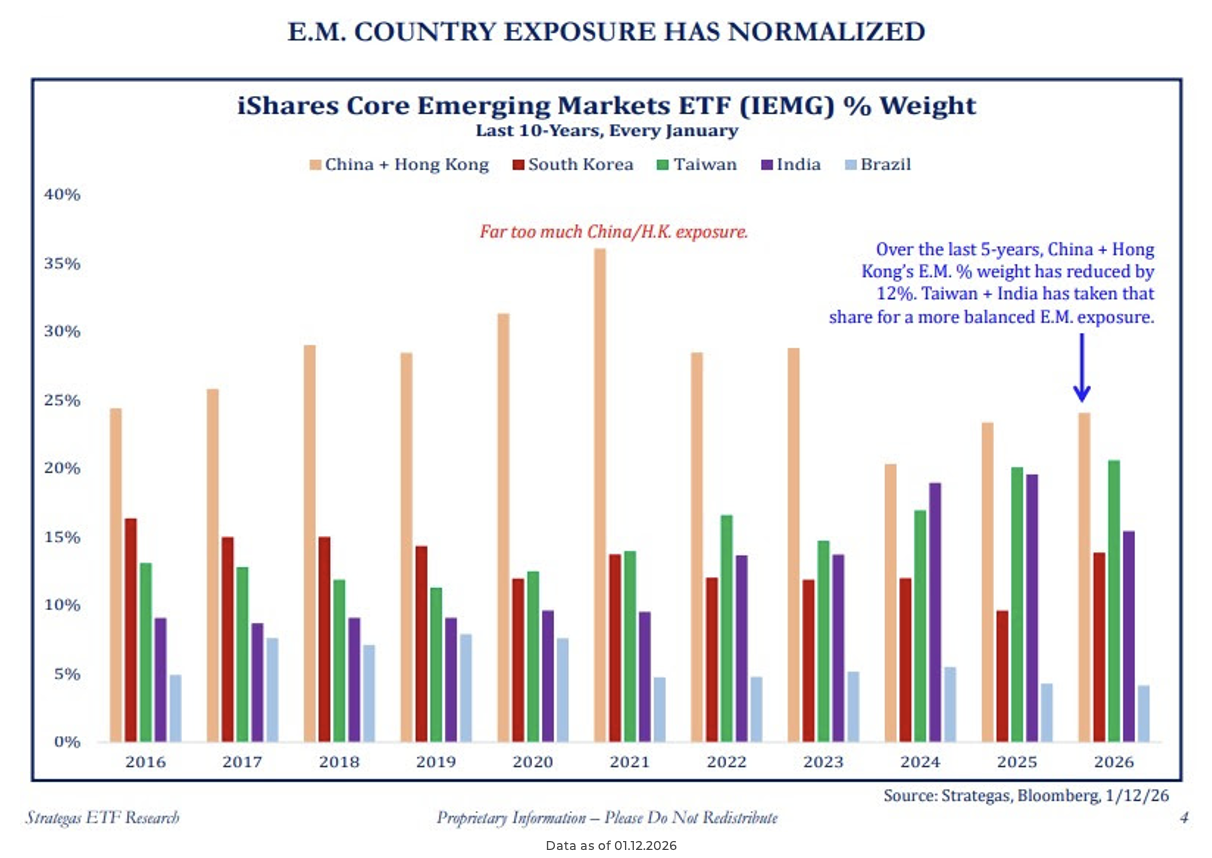

Dave: Globally, we are also seeing diversification in global markets. Emerging markets are no longer just a “China story”. In 2021, China made up over 37% of the EM index, while that is down to 25% today, with Taiwan and India picking up the lion’s share.

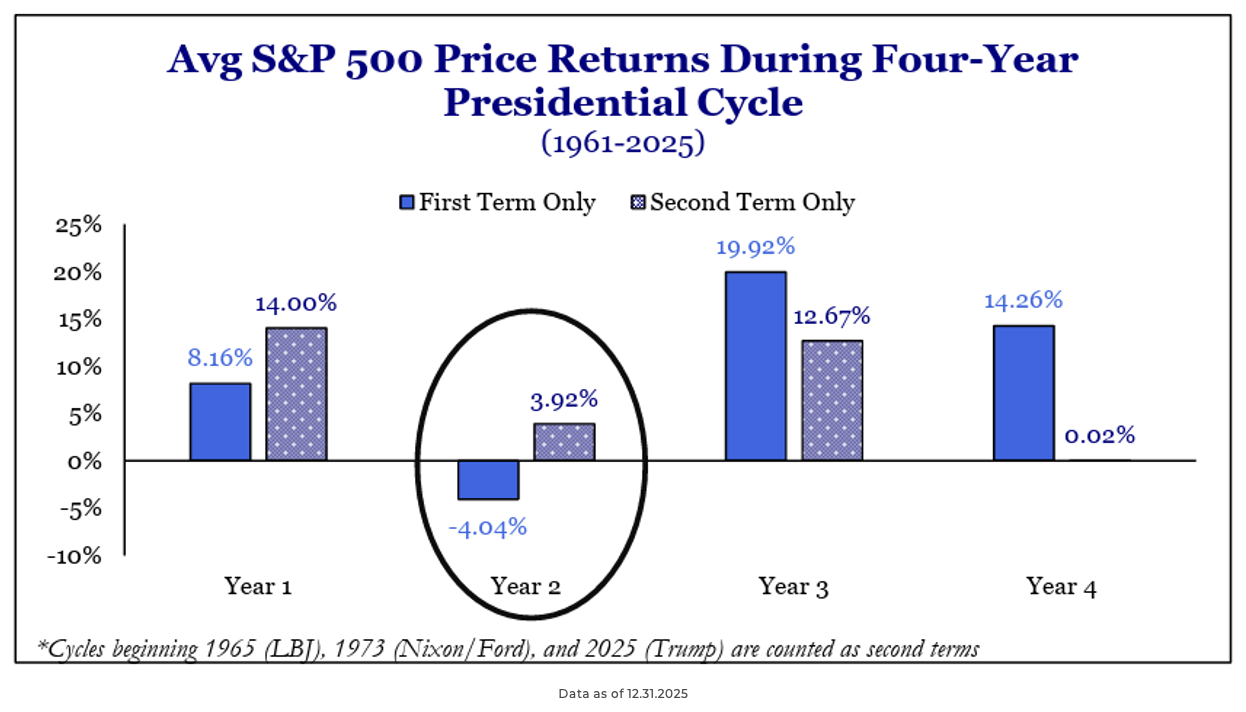

Brad: These shifts come as we move into a new phase of the political cycle. While Year 1 of a presidency is historically the best for markets due to expansive policy, Year 2 (midterm years) often brings policy friction that leads to lower historical returns.

Source: Strategas

Source: Strategas

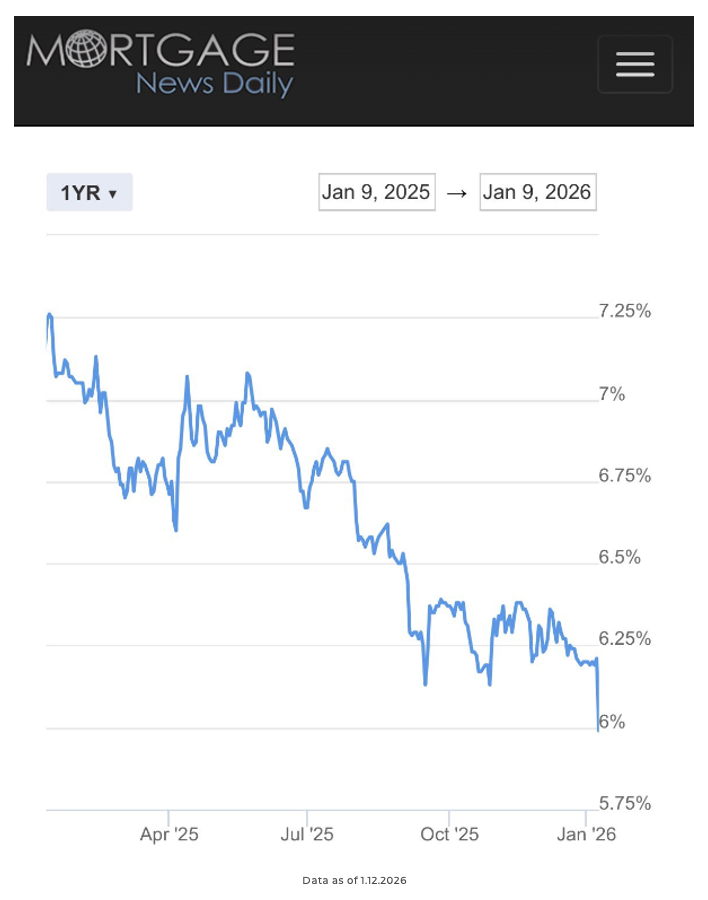

Mark: The government is providing some targeted relief, however. Following the announcement that the government would purchase $200B in mortgage bonds, mortgage rates dropped sharply, giving a much-needed boost to homebuyers.

Ten: Under the surface of these trends, market mechanics are creating unique opportunities. While the main VIX index seems calm, individual stock volatility has been very elevated. This allows investors to sell volatility on single names while buying protection at the index level.

Source: Bloomberg

Source: Bloomberg

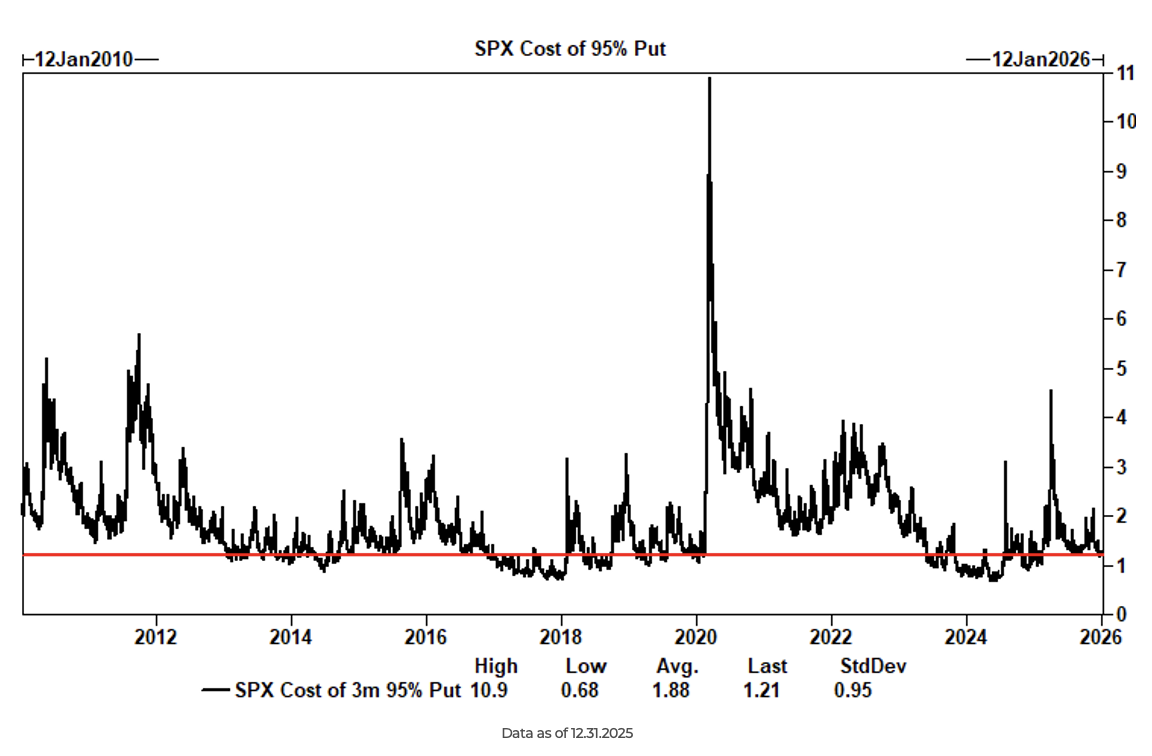

Jake: It’s been an opportunistic time for many options structures, especially since the cost of protecting against a 5% decline in the S&P 500 started the year at very low levels.

Source: Bloomberg

Source: Bloomberg

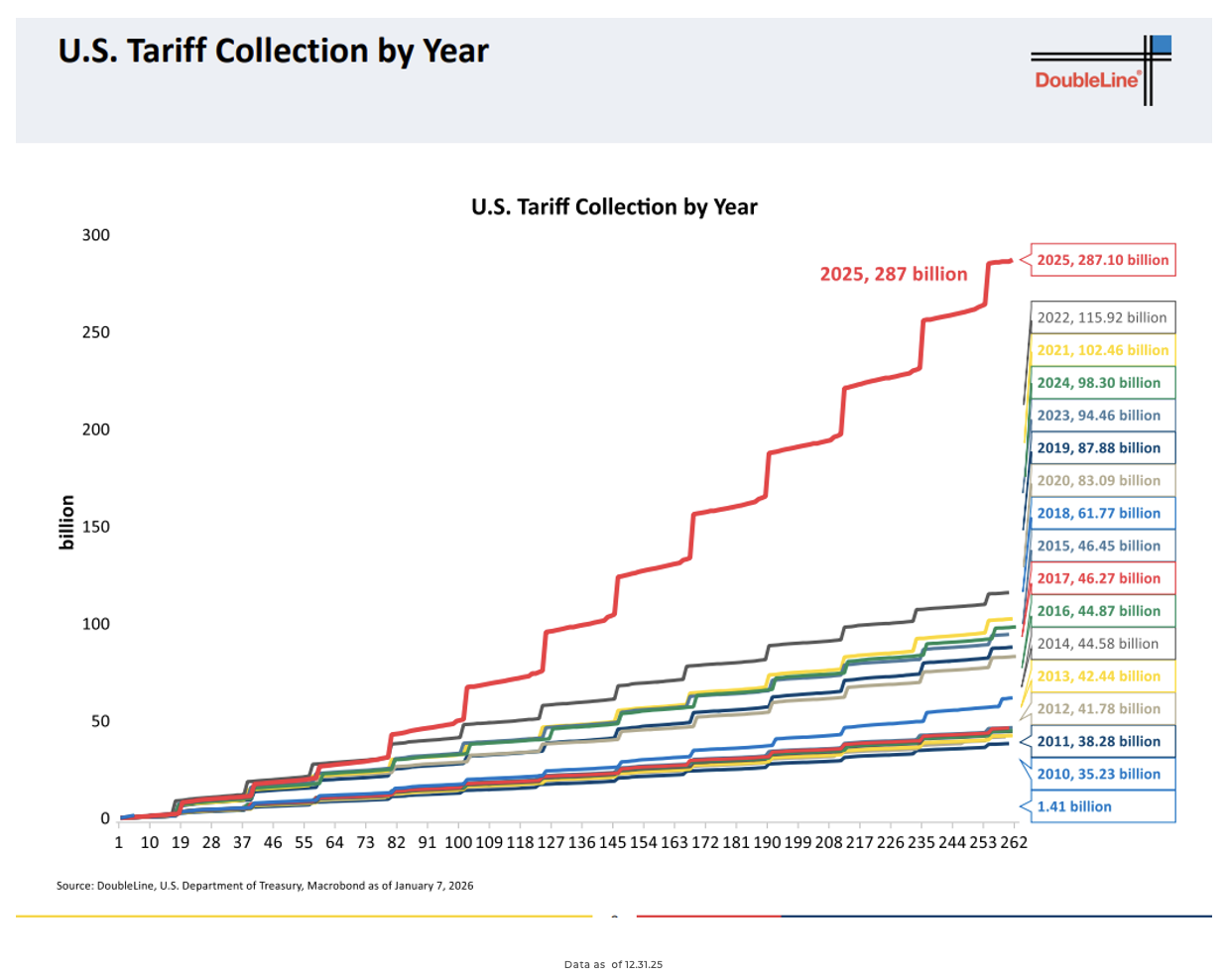

Beckham: 2025 was truly a landmark year for trade policy, as the US collected nearly $300B in tariffs, a staggering figure that is almost $200B more than any other prior year on record. We may find out shortly if this can continue.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2601-29.