Happy New Year. As we turn the page to 2026, the market landscape is a study in contrasts. Consumers who feel poor, but spend big. A tech sector that has reached a historic peak in dominance, but productivity shows signs of cooling. Concerns over growth, just as the economic expansion appears to be broadening. Here is the story of the market as we enter the first week of the year.

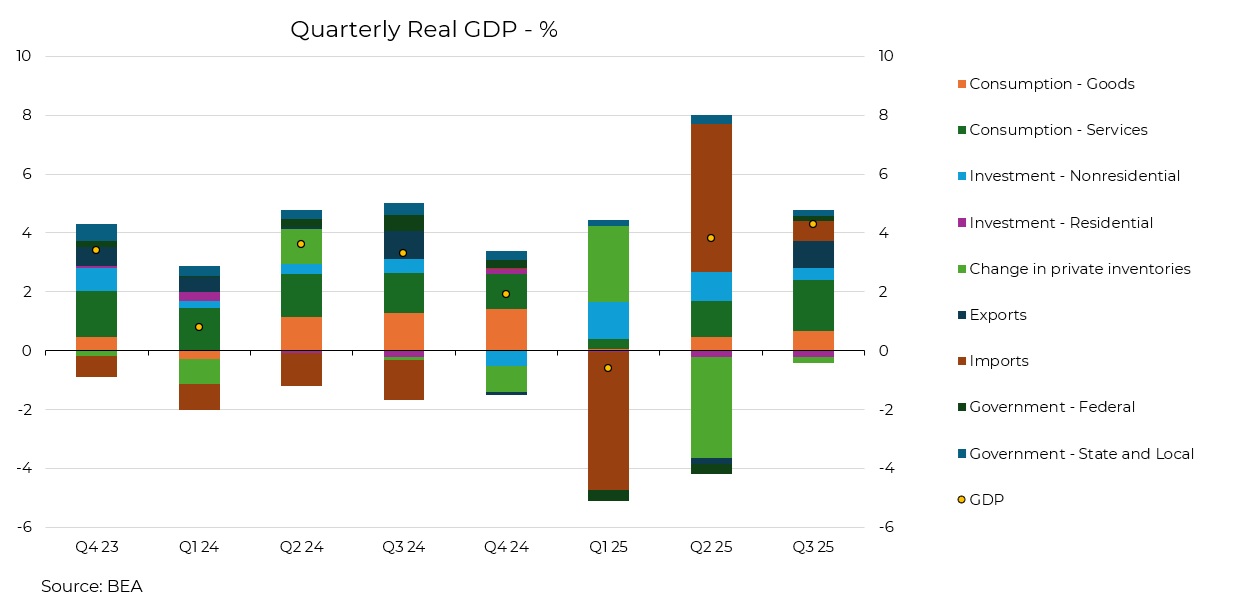

Dave: We head towards the year end with a robust 4.3% real GDP print for Q3. While some of that was a normalization from the frantic inventory stockpiling we saw ahead of the 2025 tariffs, the underlying data shows a healthy broadening of growth drivers across the economy.

Data as of 12.29.2025

Data as of 12.29.2025

Beckham: That growth is fueled by a consumer whose net worth has hit another all-time high. While liabilities are growing, the asset side of the household balance sheet continues to easily outpace that growth.

Source: Macrobond as of 12.26.2025

Source: Macrobond as of 12.26.2025

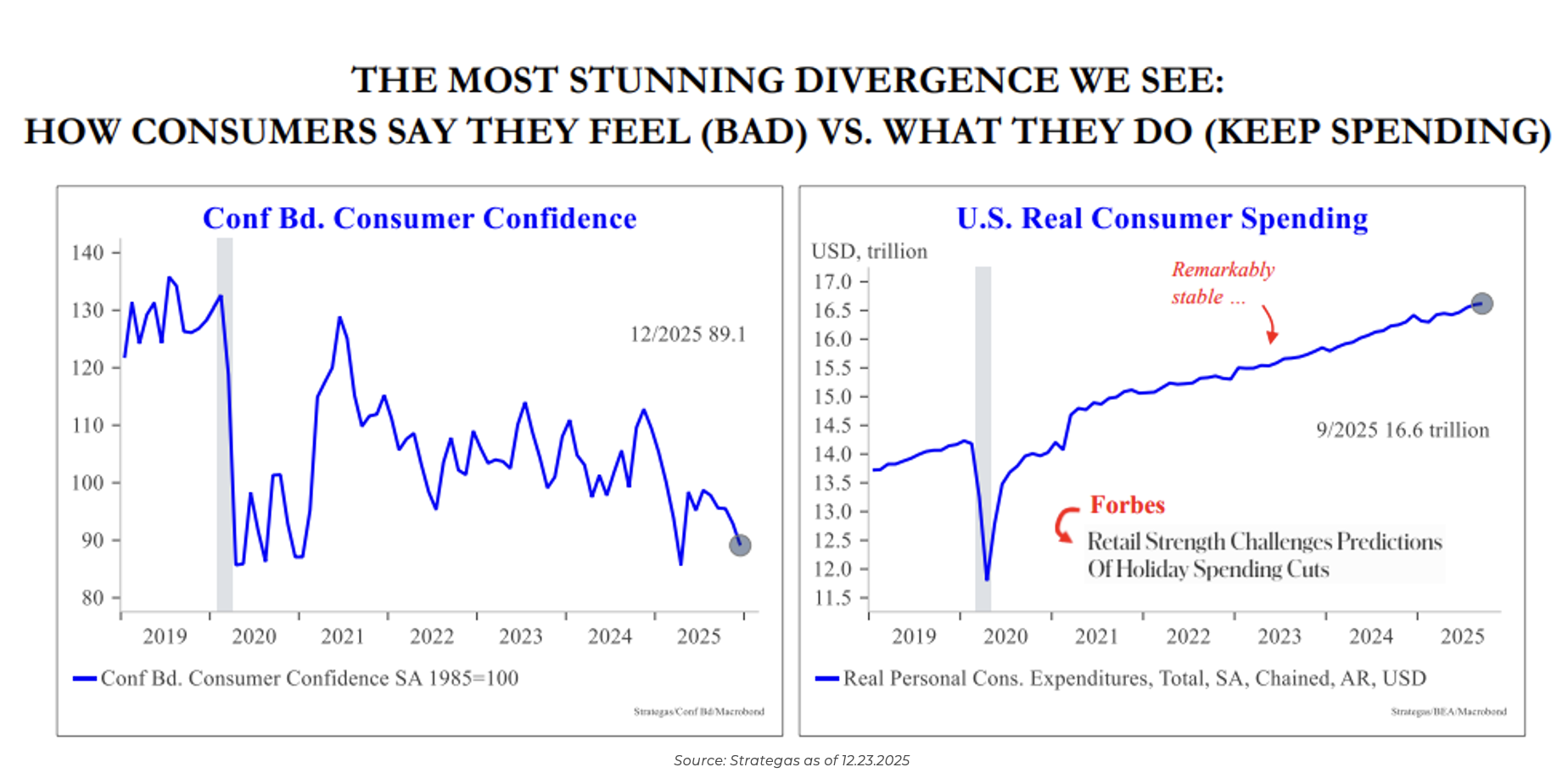

Jake: Despite those high net-worth numbers, there is a glaring disconnect in the “vibes.” Consumer confidence has been sliding toward COVID-era lows, yet real spending continues to climb.

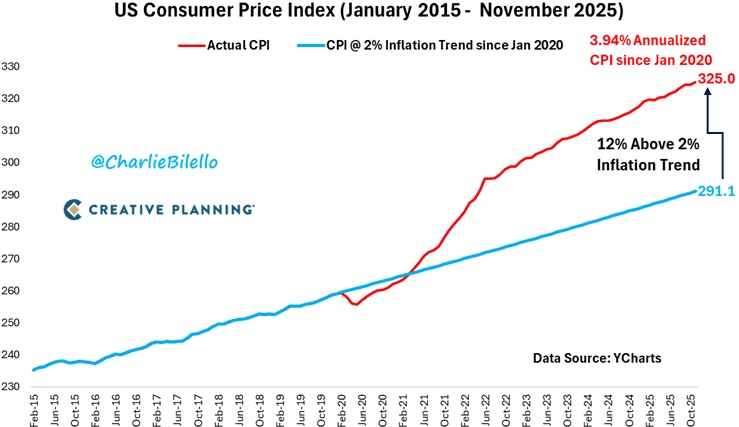

John Luke: Perhaps the bad mood stems from the “new normal” cost of living; US CPI officially broke away from its long-term 2% trend back in 2020 and has stayed structurally higher ever since. We may see inflation easing, but prices aren’t returning to past levels (or trend of past levels).

Data as of 12.22.2025

Data as of 12.22.2025

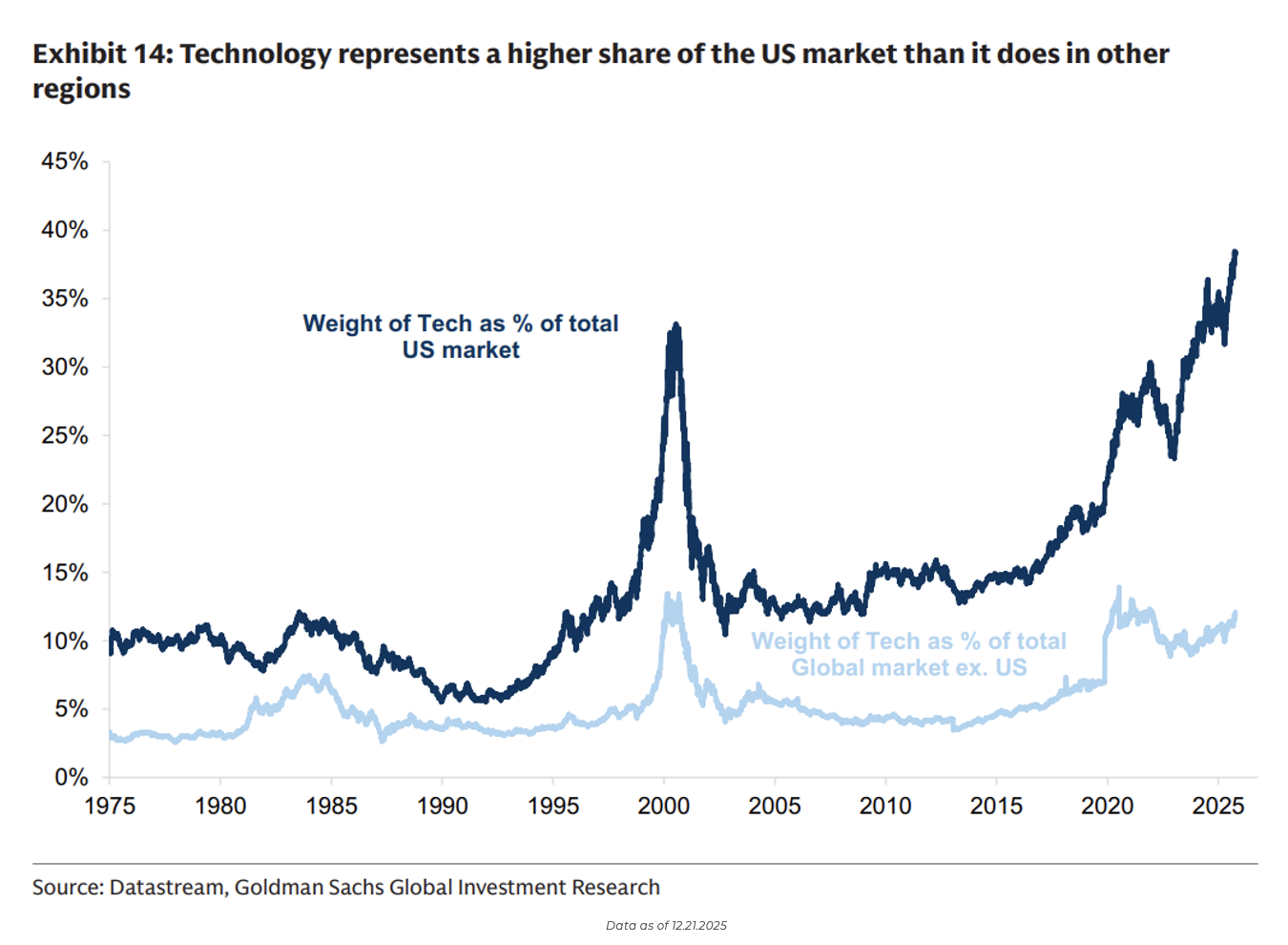

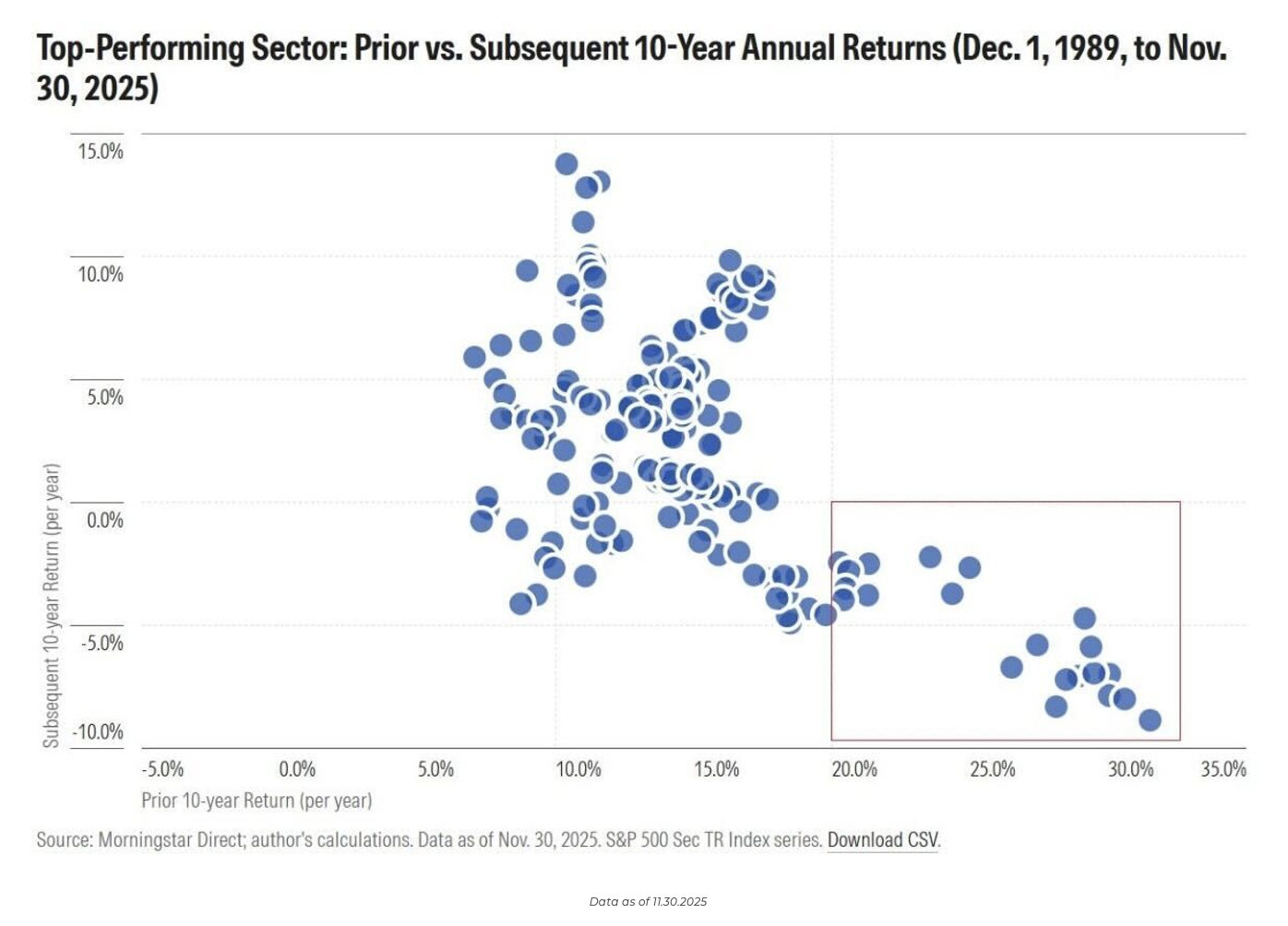

Brad: Technology’s dominance of the US market has reached a new peak, officially outpacing the concentration of the sector seen during the height of the Dot Com bubble.

Brian: But history suggests that being the “best” eventually becomes a burden. Historically, the top-performing sector over a 10-year period often posts the worst returns over the following decade. In fact, sectors with annualized returns over 20% for a decade (as Tech just did) have never seen positive forward 10-year returns.

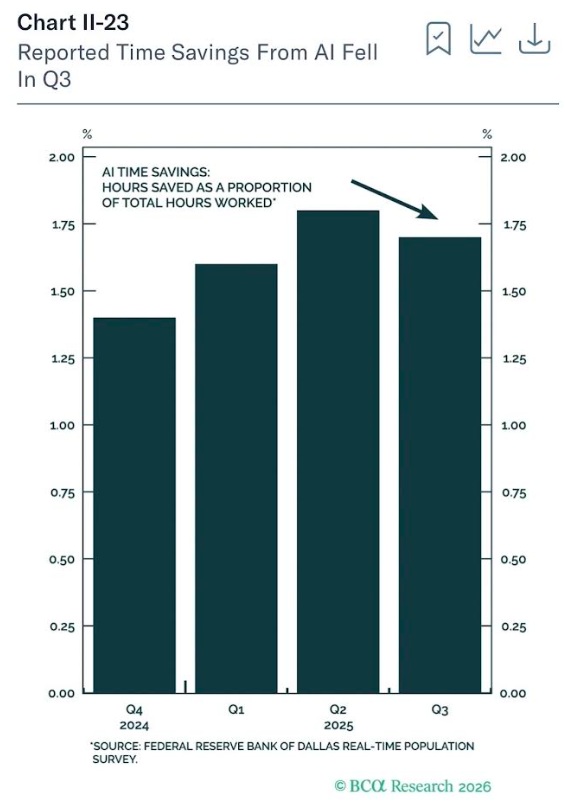

Ten: AI investment must be justified at some point, given current valuations, but the “productivity miracle” may be facing its first skeptical look. The percentage of hours saved relative to total hours worked appears to have hit a short-term peak and may actually be starting to roll over.

Data as of 12.26.2025

Data as of 12.26.2025

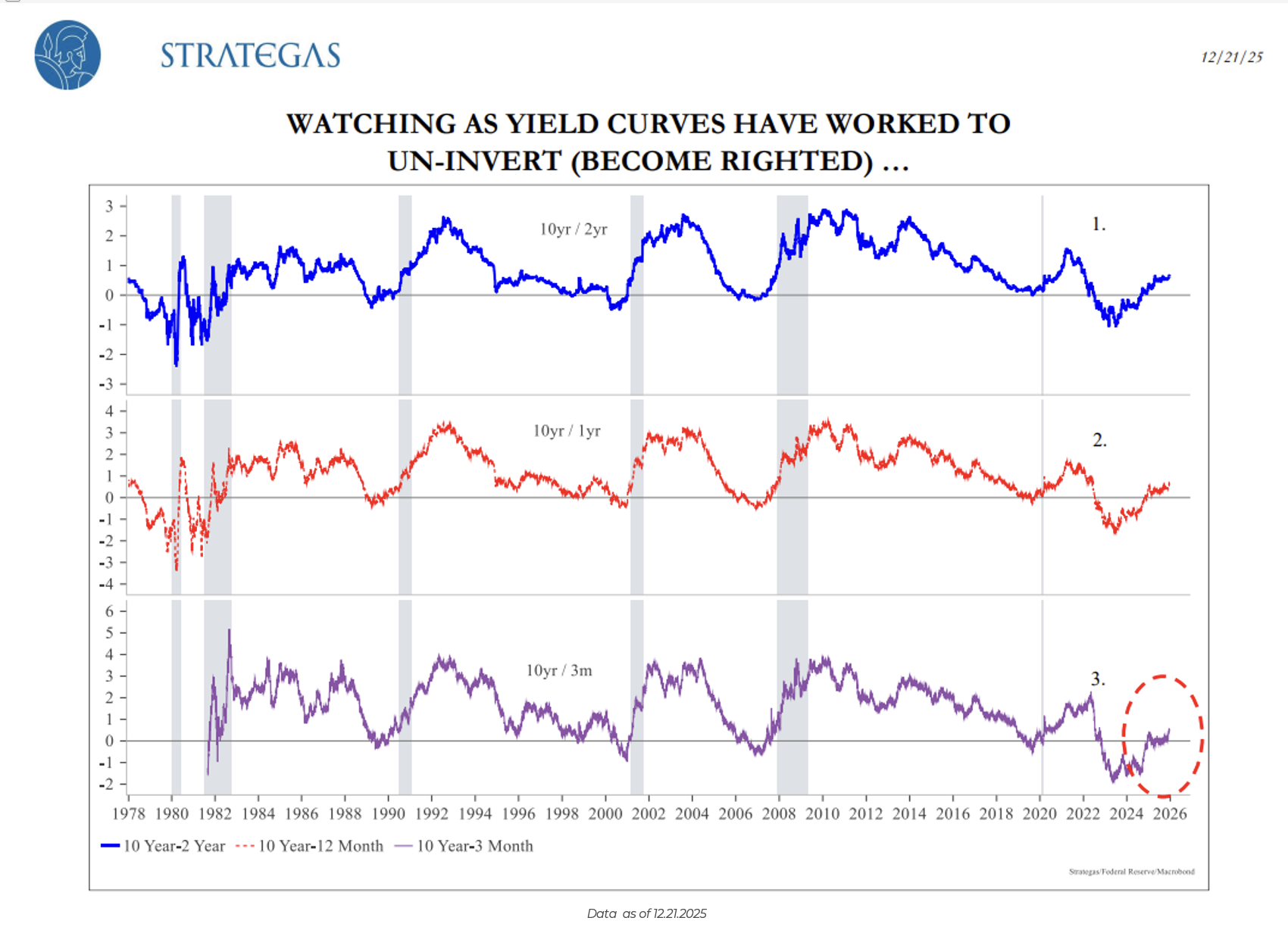

Beckham: While Tech faces a high bar, the “boring” parts of the market are shifting. After years of inversion, the yield curve is now officially un-inverted across the entire curve. A transition that historically marks a major new phase in the economic cycle.

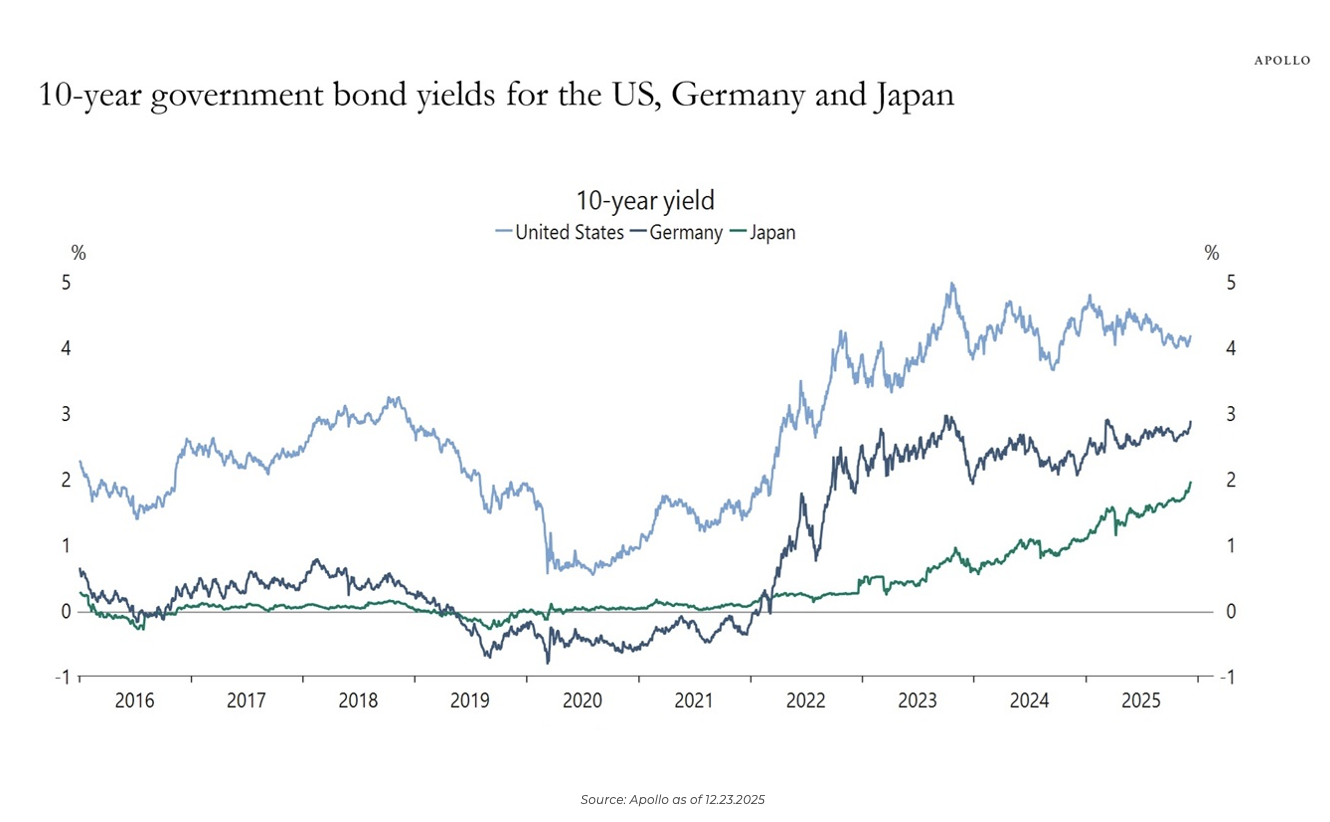

John Luke: We’re also seeing a global convergence in rates. While yields in Germany and Japan continue to climb, US yields have remained relatively flat, bringing global borrowing costs into closer alignment.

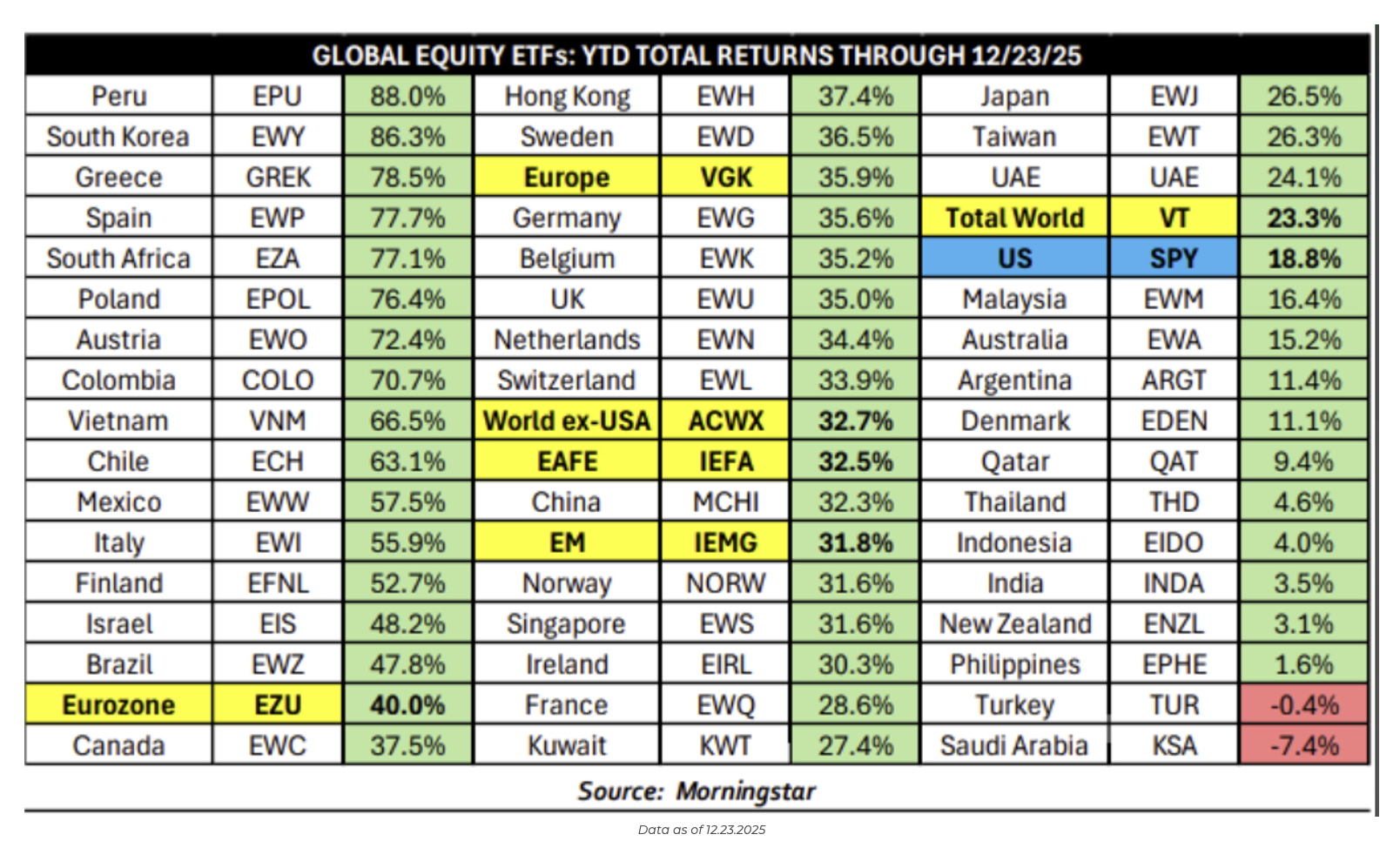

Joseph: 2025 will be remembered for the performance of global stocks. US markets performed well, but nothing compared to the scale of global returns.

Brett: In the private markets, repricing is grinding a bit slower. In 2020, 61% of exits were sales to corporations, but that has plummeted to 27%. Now, 36% of deals are just “sponsor-to-sponsor”… PE firms selling to each other.

Data as of 6.30.2025

Data as of 6.30.2025

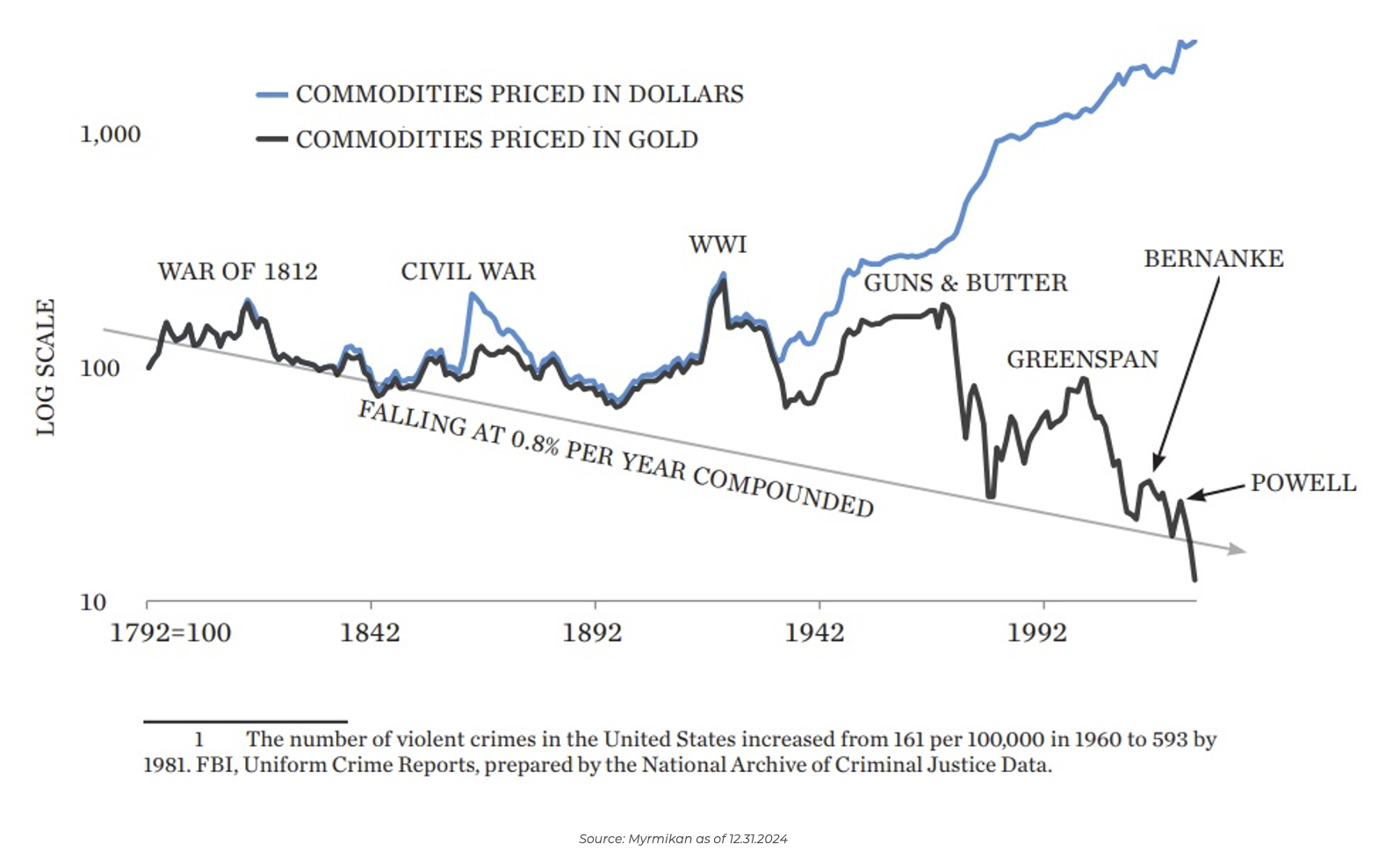

JD: If history is any guide, we might see a shift back toward hard assets. We often hear about rising commodity prices, but since 1942, they’ve actually fallen significantly when priced in gold. This suggests that the “commodity boom” has been more about dollar debasement than actual scarcity, a trend that may continue if inflation remains unanchored.

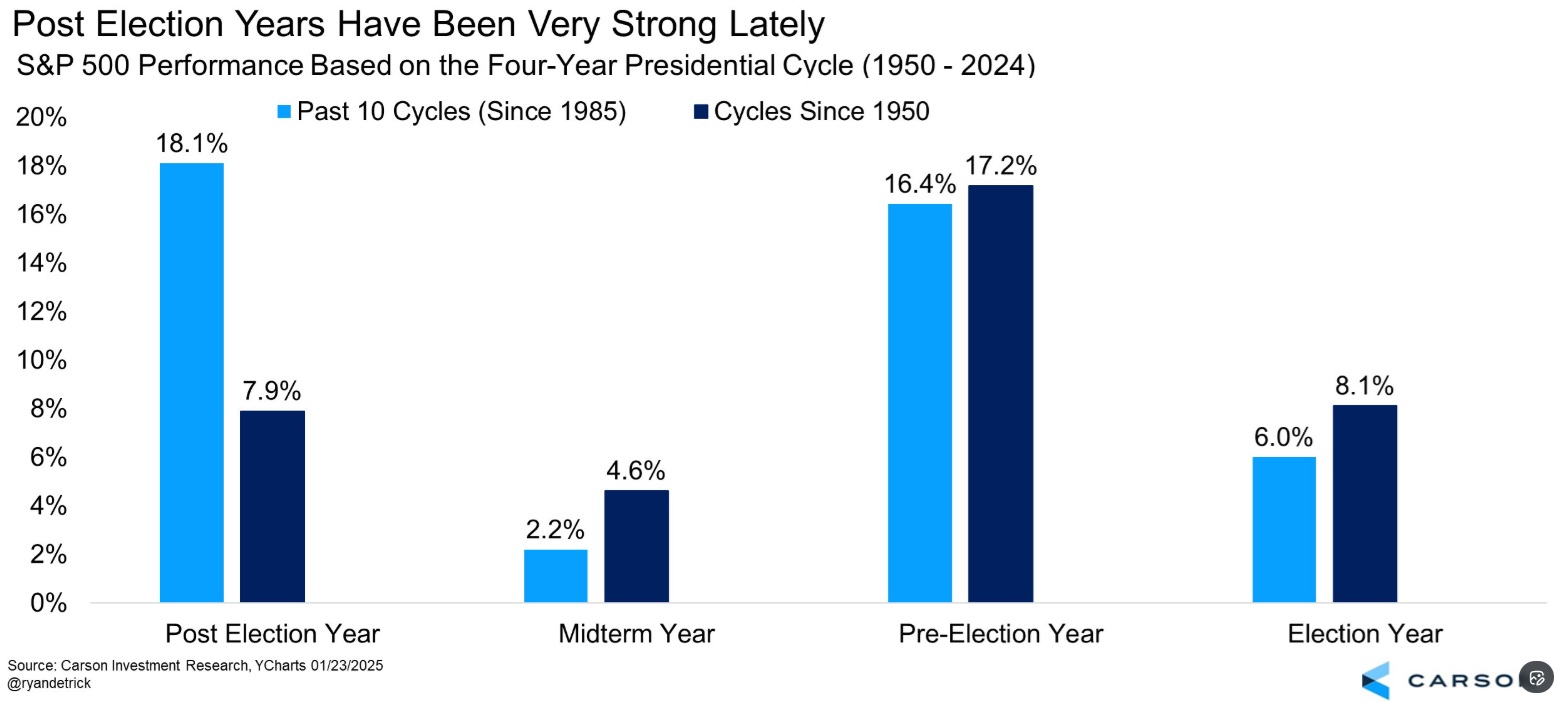

Brad: As we look at the 2026 calendar, we have to acknowledge the Midterm year hurdle. Since 1985, midterm years have averaged just 2.2% gains. Granted, the GFC in 2008 and the COVID crash in 2020 dragged that average down, but it’s a reminder that despite the smooth path we’re currently on… things can change quickly.

Data as of 12.29.2025

Data as of 12.29.2025

Derek: For now, investors are optimistic that the underlying fundamental strength will continue, and recent forecasts for continued EPS growth support a lot of that optimism.

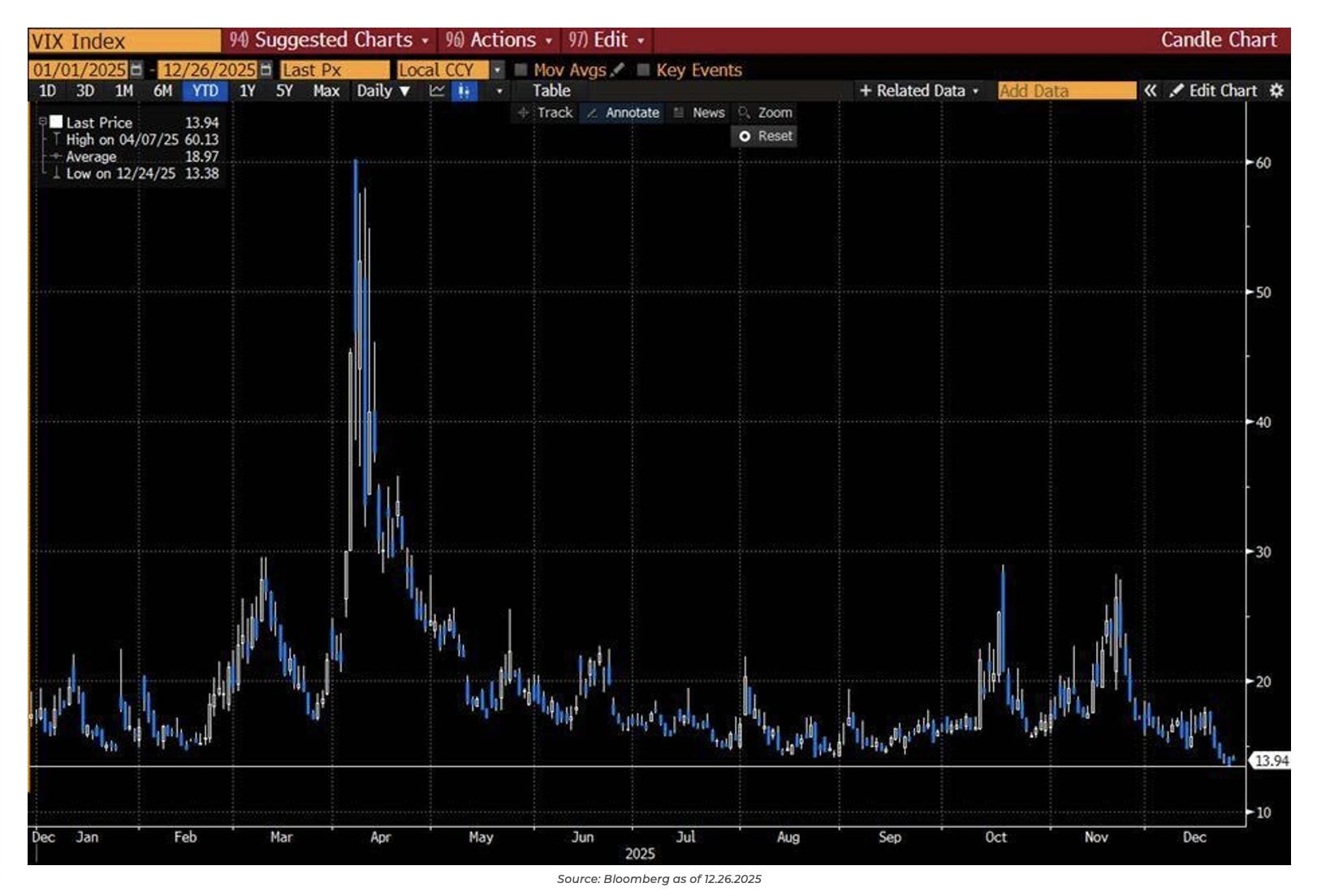

Brian: Investors don’t seem worried, though. The VIX moved back below 14, showing a level of confidence (or complacency) that suggests the market expects the New Year to be all clear skies.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2512-28.