Our team looks at a lot of research throughout the day. Here are a handful that we think are good summations of investor activity, from market expectations to corporate fundamentals, a resilient economy relative to others, and changes in business over recent decades. Here’s to a great year ahead!

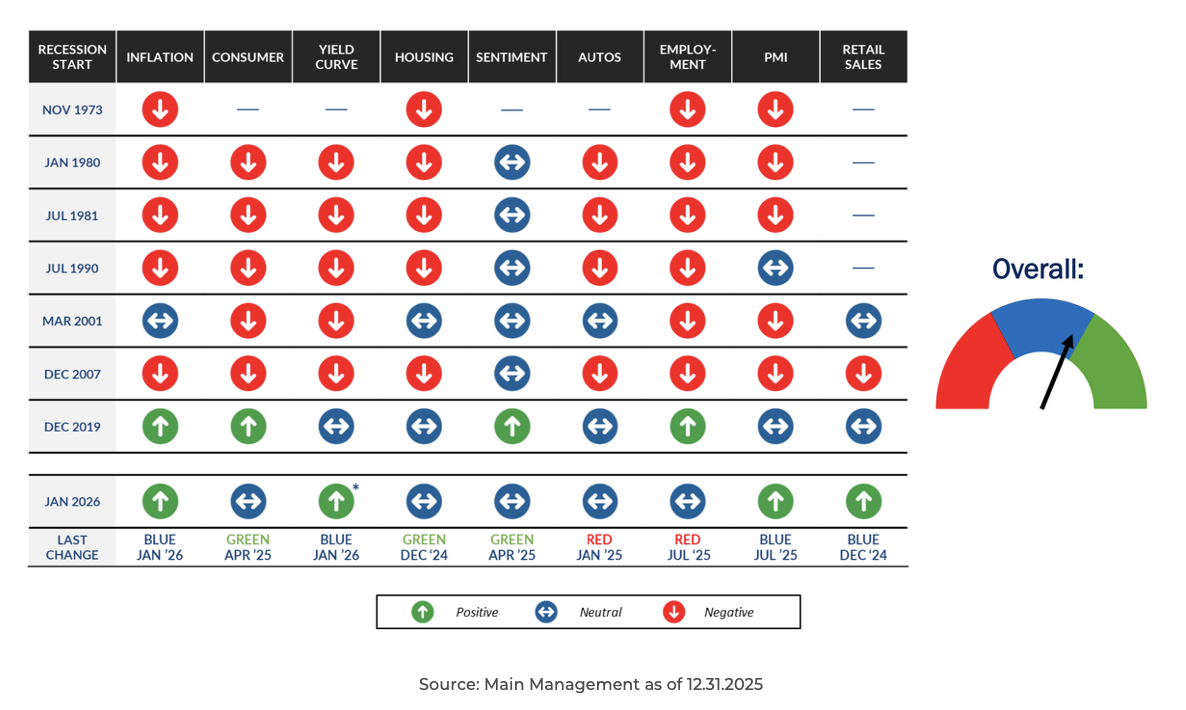

Dave: While history is littered with red flags, the current dashboard remains remarkably clean. Looking at various signals from past cycles, nothing is currently indicating that we are headed toward a recessionary environment.

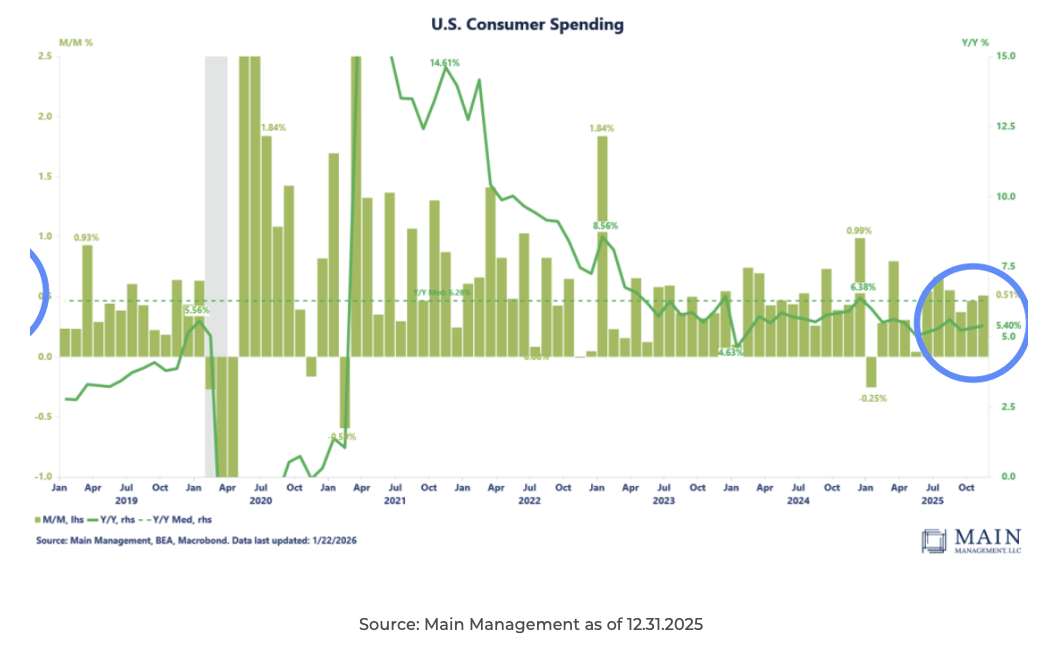

Beckham: The U.S. consumer continues to carry the torch, with spending currently quite strong. This persistent activity is a clear indication that the economic engine is still chugging along at a healthy clip.

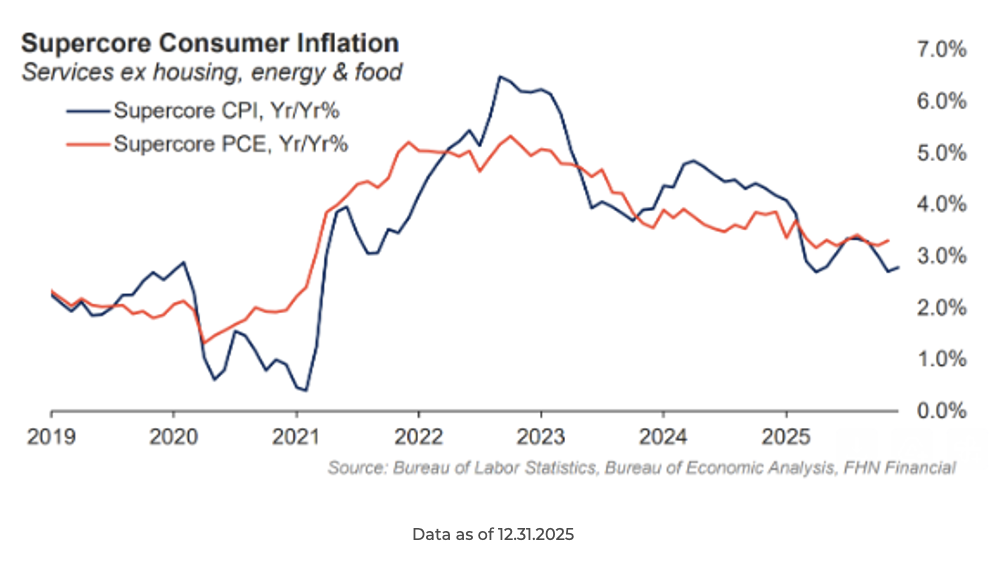

Ten: We continue to see encouraging trends in Supercore CPI (a refined gauge that excludes food, energy, and housing), which has steadily retreated from its late-2022 peaks. This may provide the disinflationary evidence for incremental rate cuts.

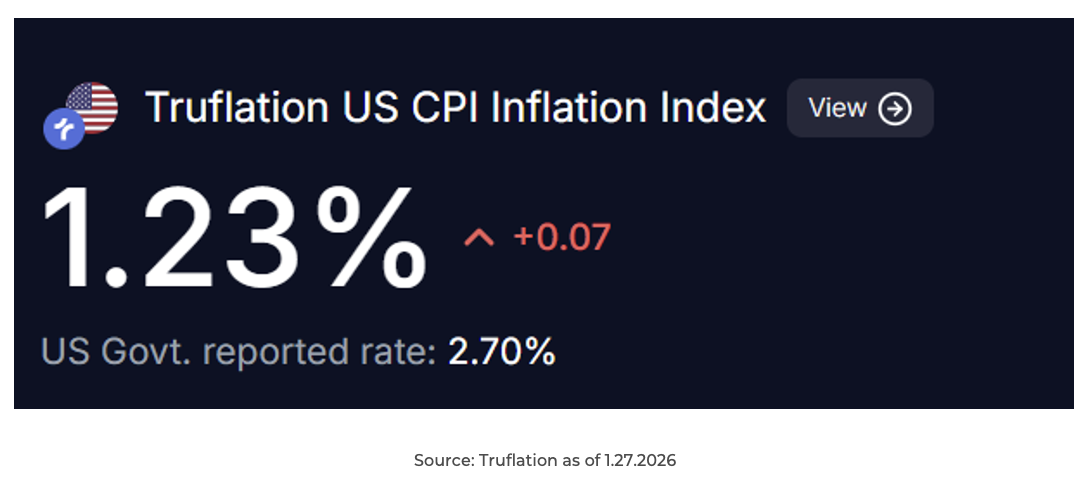

John Luke: For a more “live” perspective, Truflation (which tracks millions of items in real-time) is actually showing inflation well below the Fed’s 2% target. It’s a stark contrast to the 2.70% official government rate reported recently.

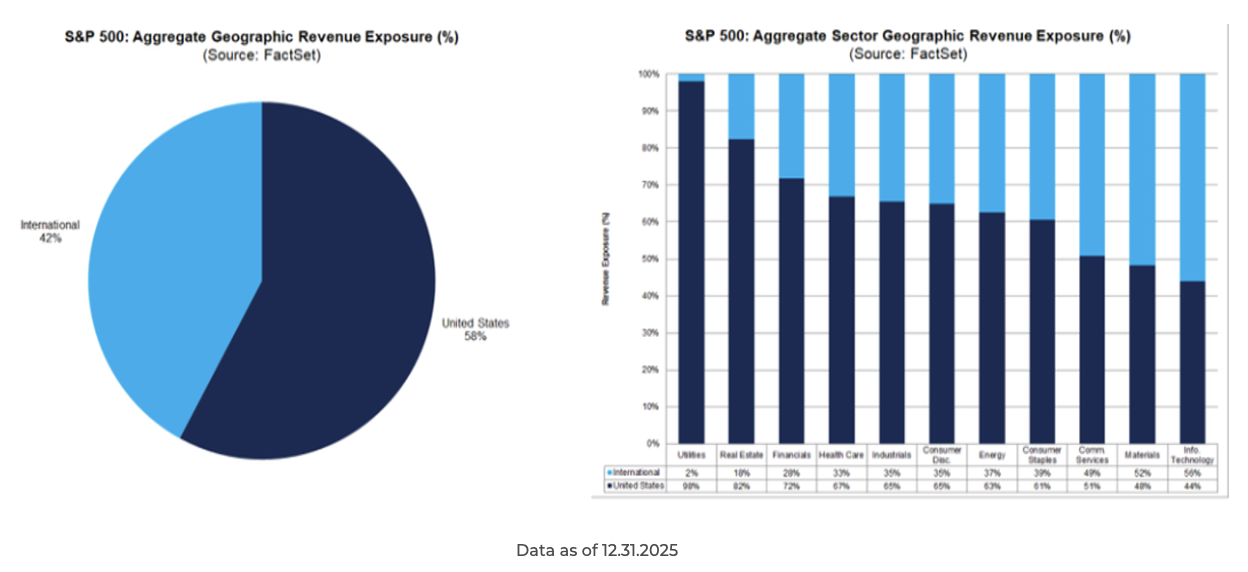

Jake: Many investors seek international diversification elsewhere, but the S&P 500 is already a global powerhouse. With over 40% of revenue coming from international markets, led by the Tech sector at over 50%, domestic large caps are a direct play on global growth.

Brad: It is difficult to predict the dollar’s direction because all currencies are weakening; it’s just how fast they are weakening relative to each other. However, US versus global stock market performance has been highly correlated with that relative strength.

JD: How you allocate depends heavily on the growth and inflation regime you believe we are entering. Gold, for instance, has found strong support during its recent run-up due to a combination of high nominal growth and elevated inflation levels.

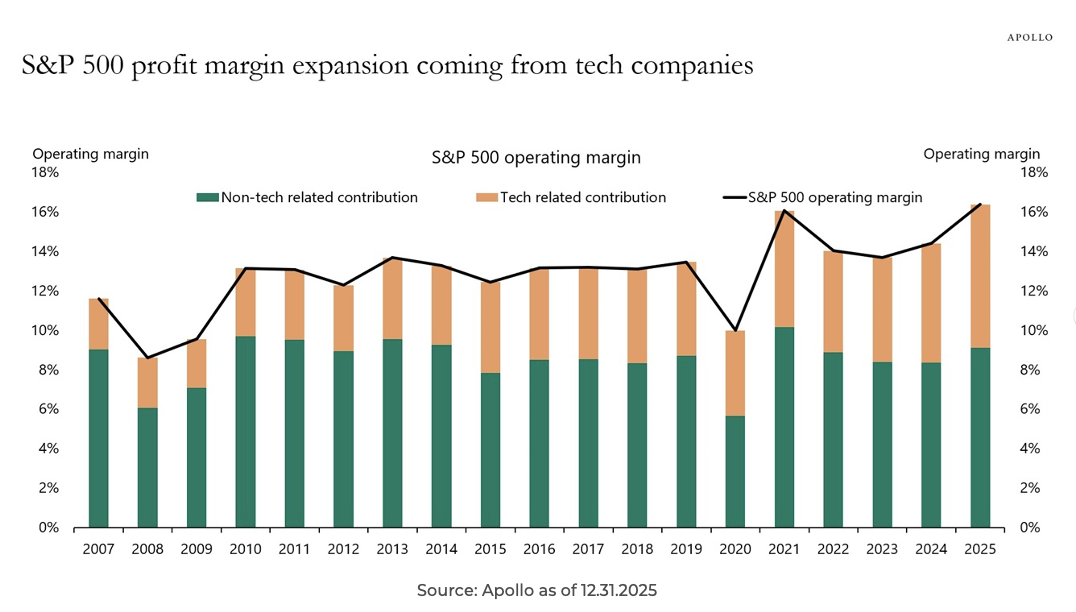

Brett: Profit margins for the S&P 500 remain historically wide, but that strength is highly concentrated. Almost all the margin expansion we’ve seen over the last two decades has been driven solely by the scale and efficiency of technology companies.

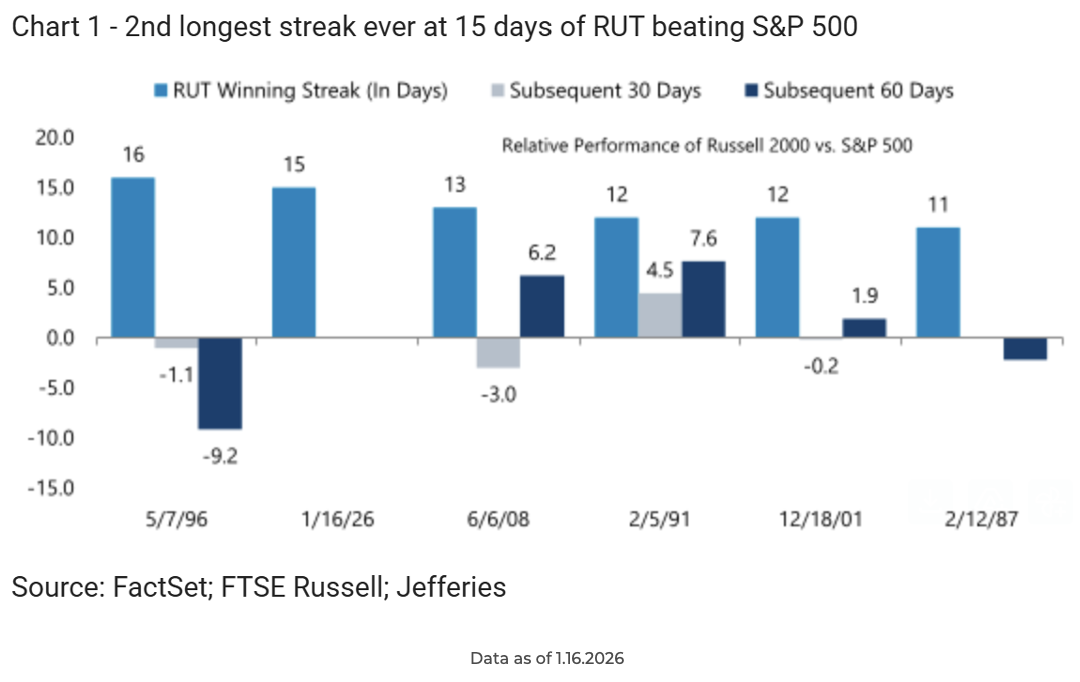

Dave: Small caps surged into 2026, recording a historic 15-day winning streak against the S&P 500. This marks the second-longest streak in history, highlighting a sharp rotation in investor sentiment.

Derek: It is important to remember that not all small caps are created equal. The Russell 2000 is heavily weighted toward “lower quality” companies that don’t yet have earnings, whereas the S&P 600 small-cap index requires companies to be profitable.

Brian: This quality gap is driven by sector exposure; the majority of non-earners within the Russell 2000 are concentrated in Biotech and Tech. This is why the performance of medical breakthrough indices often mirrors the relative movement of the broader Russell 2000.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2601-35.