Our team looks at a lot of research throughout the day. Here are a handful of charts we think are good summations of investor activity, from a historic rally with improving breadth, to record earnings and margins, the AI buildout reaching the labor market, and aligning portfolios with the mountain of maturing government debt. Have a great weekend!

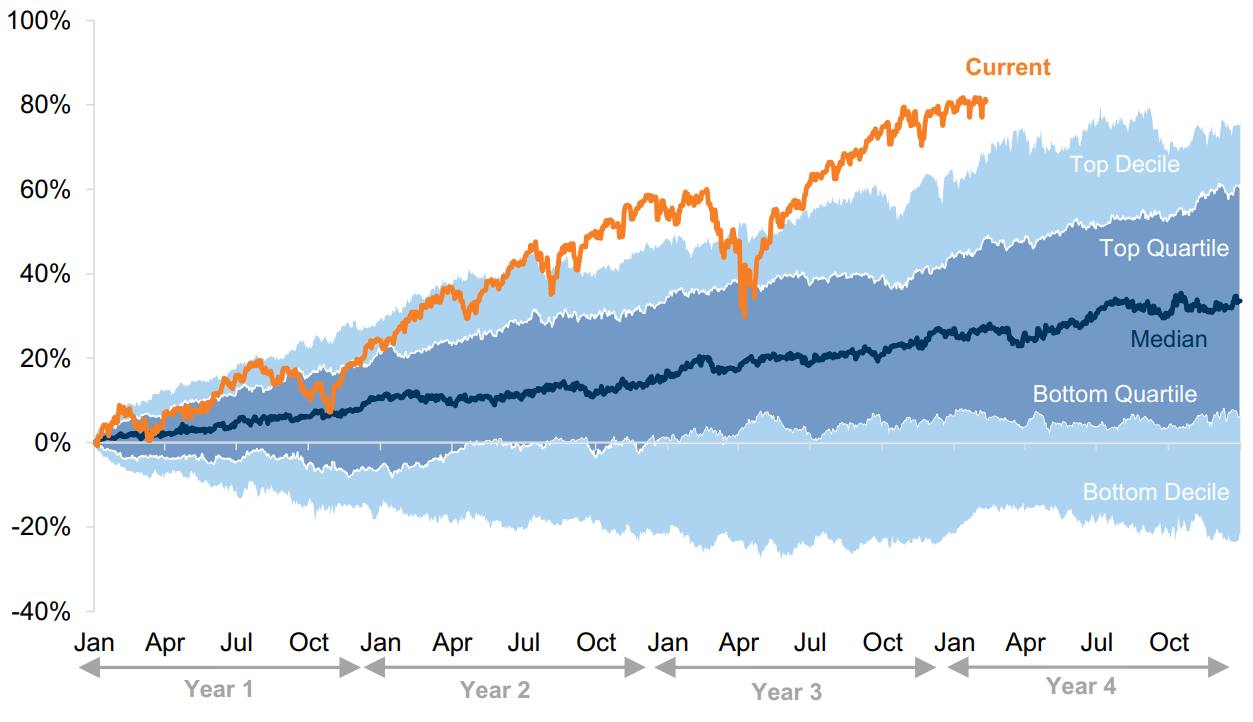

Brad: Three and a half years in, this bull market is tracking above the top decile of history.

Source: Goldman Sachs as of 07.06.2026

Source: Goldman Sachs as of 07.06.2026

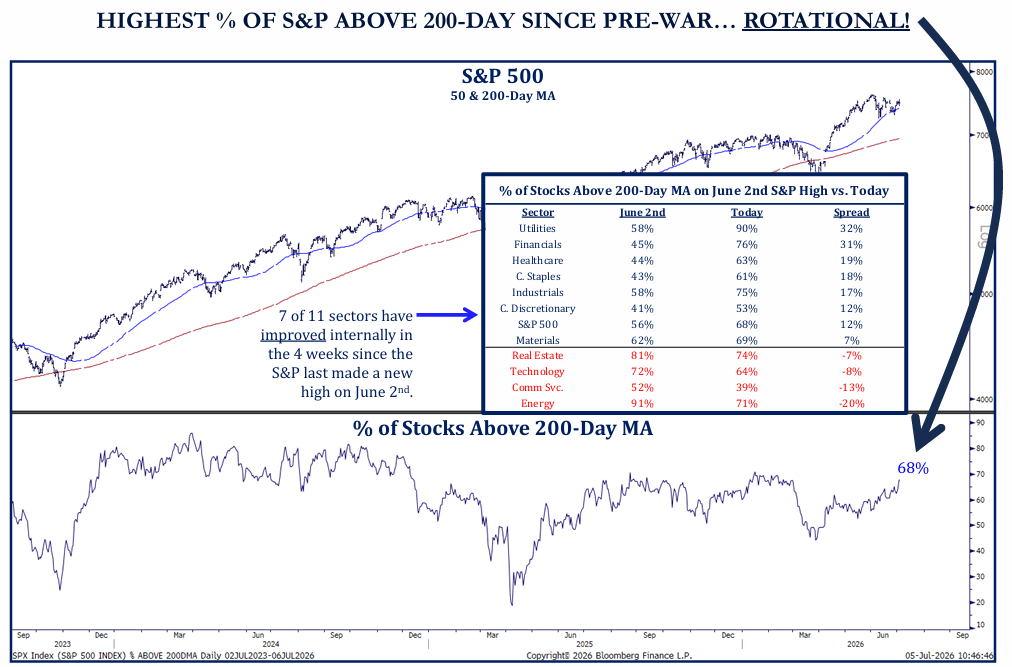

Brian: It is no longer a handful of names doing the work. 68% of stocks are above their 200-day average, and 7 of 11 sectors are improving internally since the June high.

Source: Strategas as of 07.05.2026

Source: Strategas as of 07.05.2026

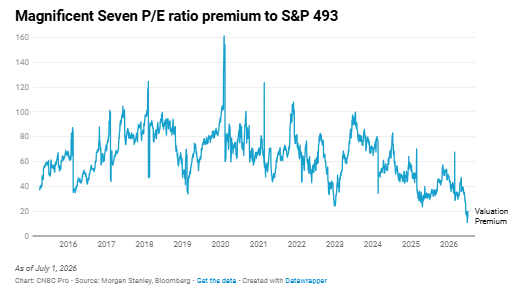

Mark: Mag 7 valuation premium over the other 493 has nearly vanished, a healthy de-rating rather than a derailing.

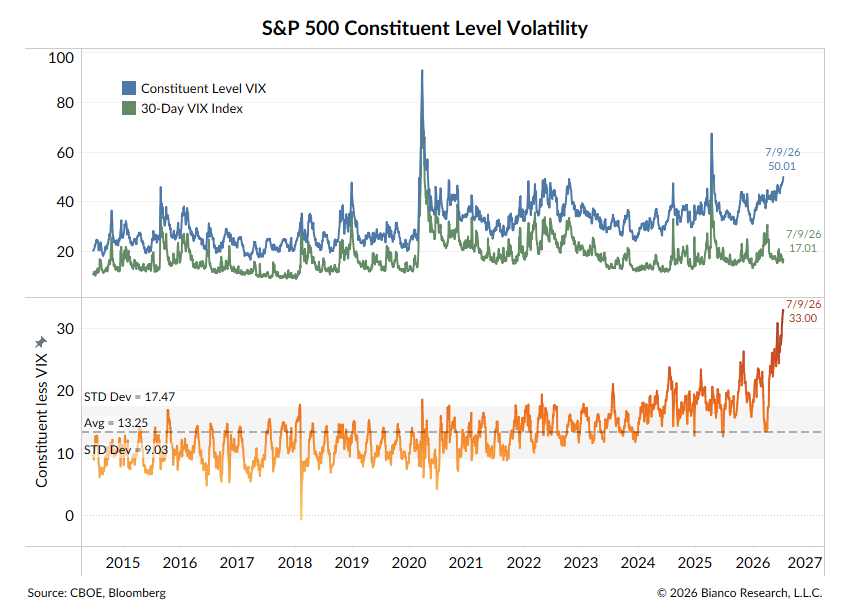

Joseph: Beneath a calm surface, single stock volatility is anything but calm. The gap between constituent-level vol and the VIX just hit a record.

Data as of 07.09.2026

Data as of 07.09.2026

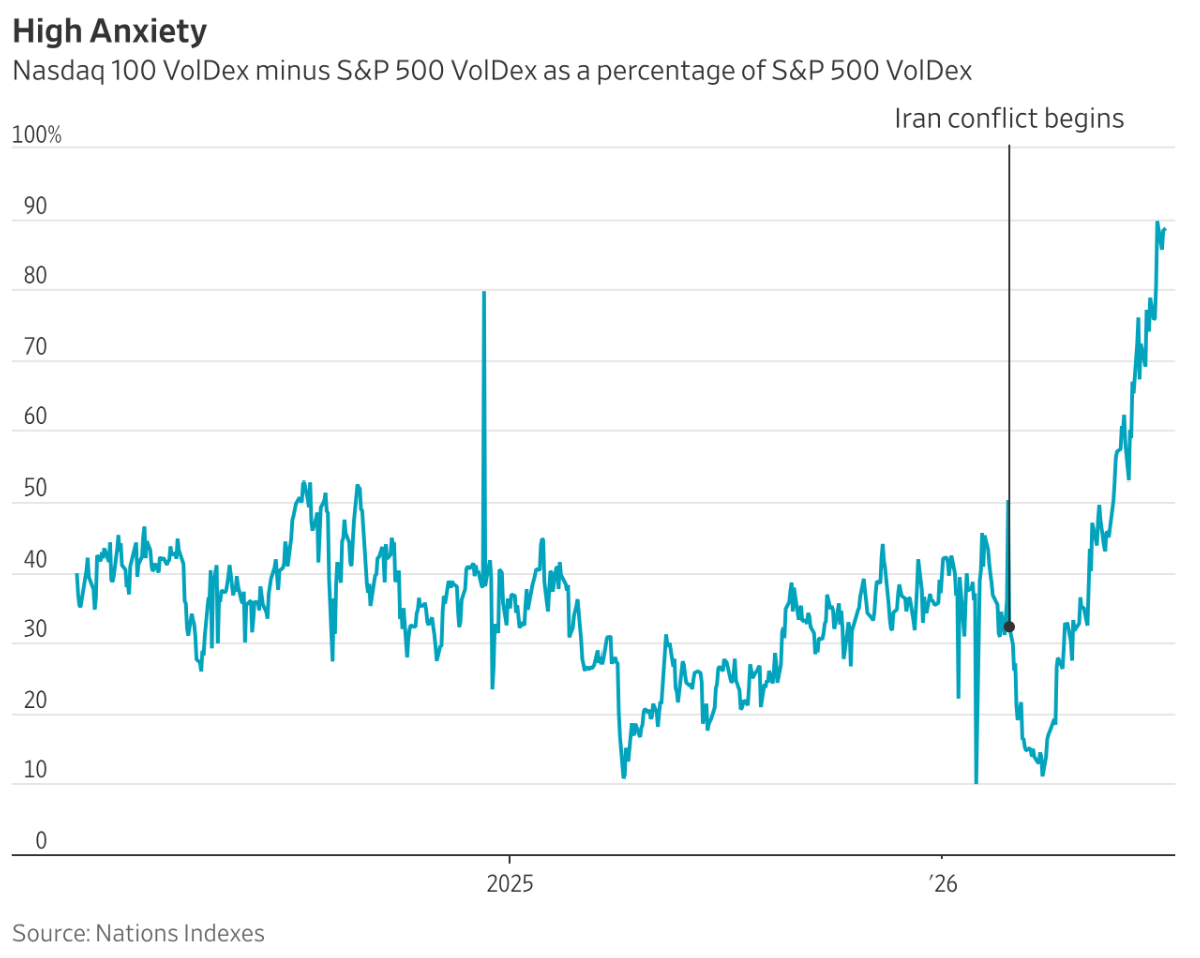

Dave: The anxiety is concentrated in tech, with Nasdaq 100 volatility commanding a near-record premium to the S&P 500.

Source: Nations Indexes via WSJ as of 07.07.2026

Source: Nations Indexes via WSJ as of 07.07.2026

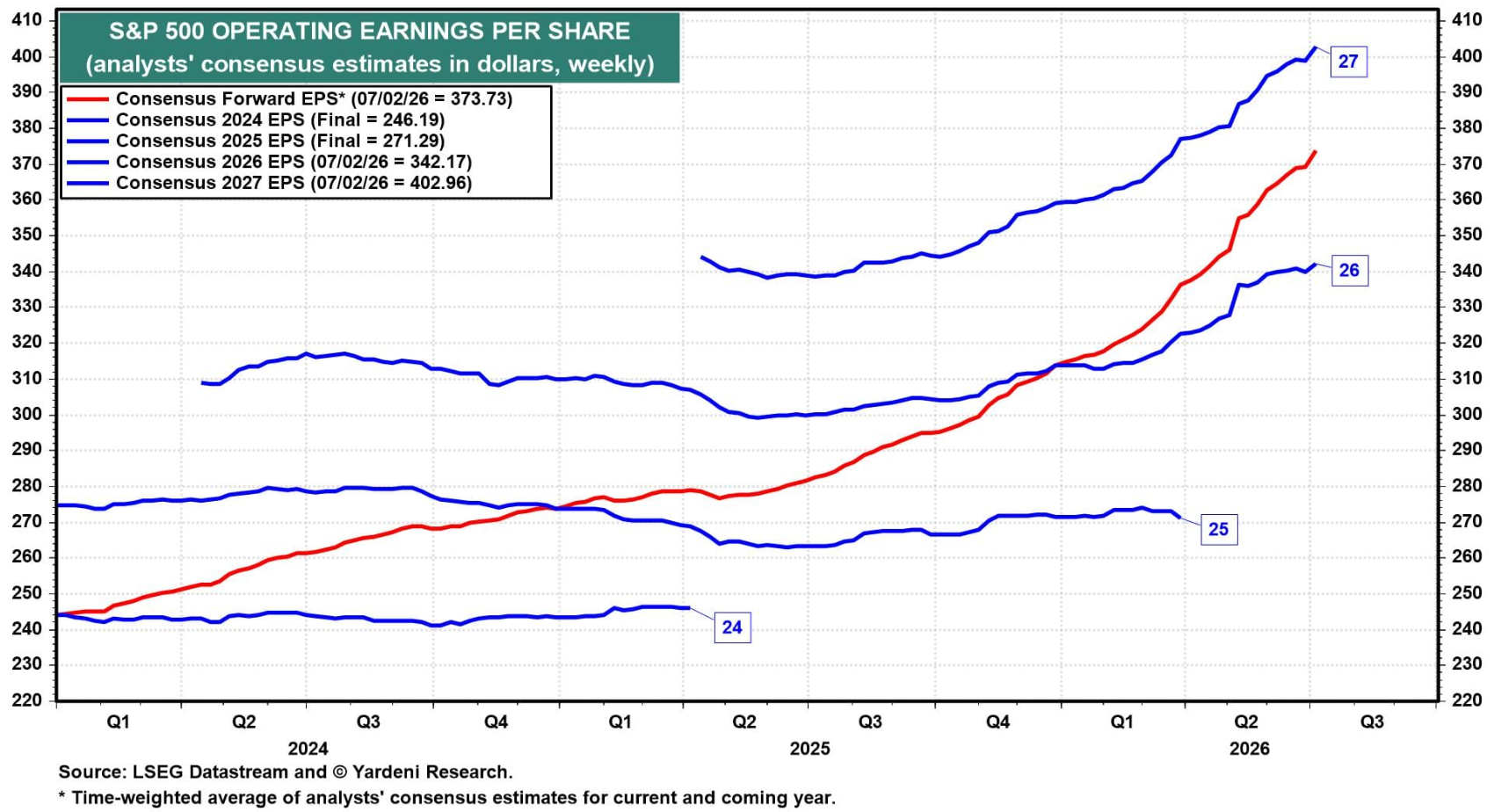

Beckham: Fundamentals continue to backstop the rally, with forward earnings estimates marching toward $400.

Source: Yardeni Research as of 07.02.2026

Source: Yardeni Research as of 07.02.2026

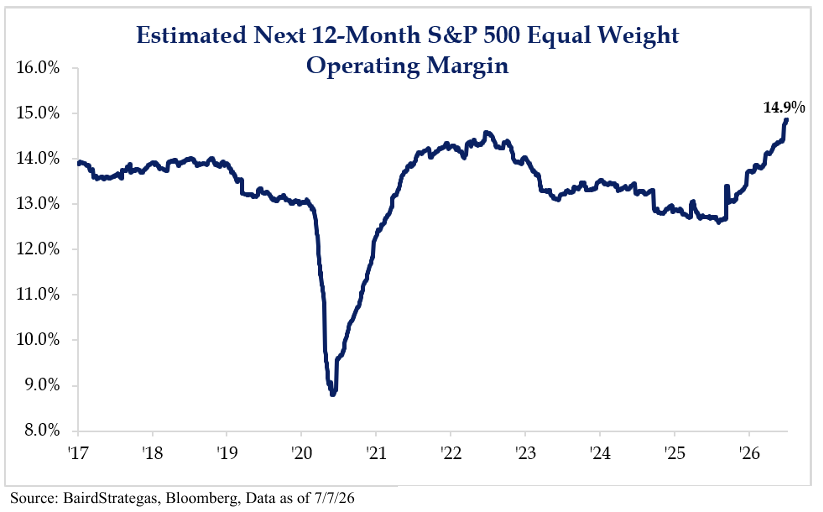

Ten: It is not just the giants. Margins for the average S&P 500 company just hit a record 14.9%.

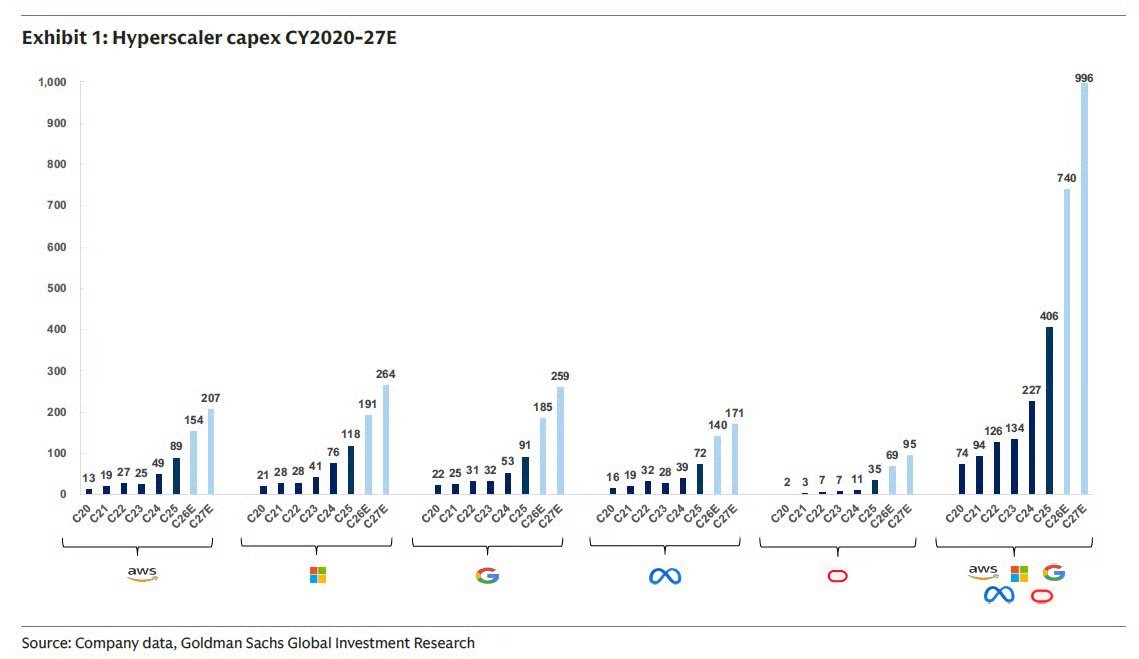

Brett: The AI buildout keeps getting bigger, with combined hyperscaler capex estimates now approaching $1 trillion for 2027.

Source: Goldman Sachs as of 07.02.2026

Source: Goldman Sachs as of 07.02.2026

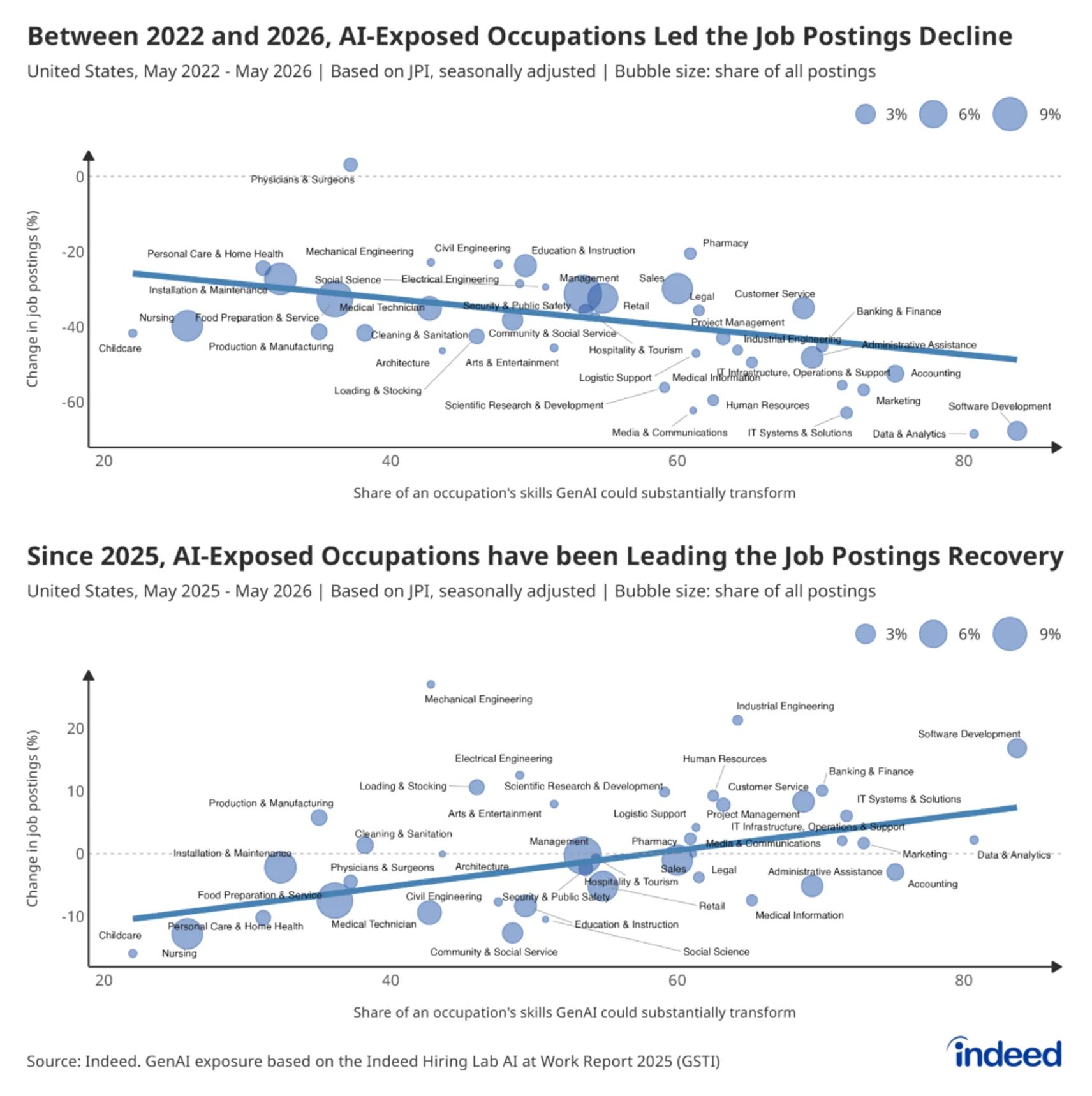

John: That spend is rippling through the labor market. AI-exposed jobs declined in terms of postings in 2022, but have been leading the recovery since 2025.

Source: Indeed Hiring Lab as of 12.31.2025

Source: Indeed Hiring Lab as of 12.31.2025

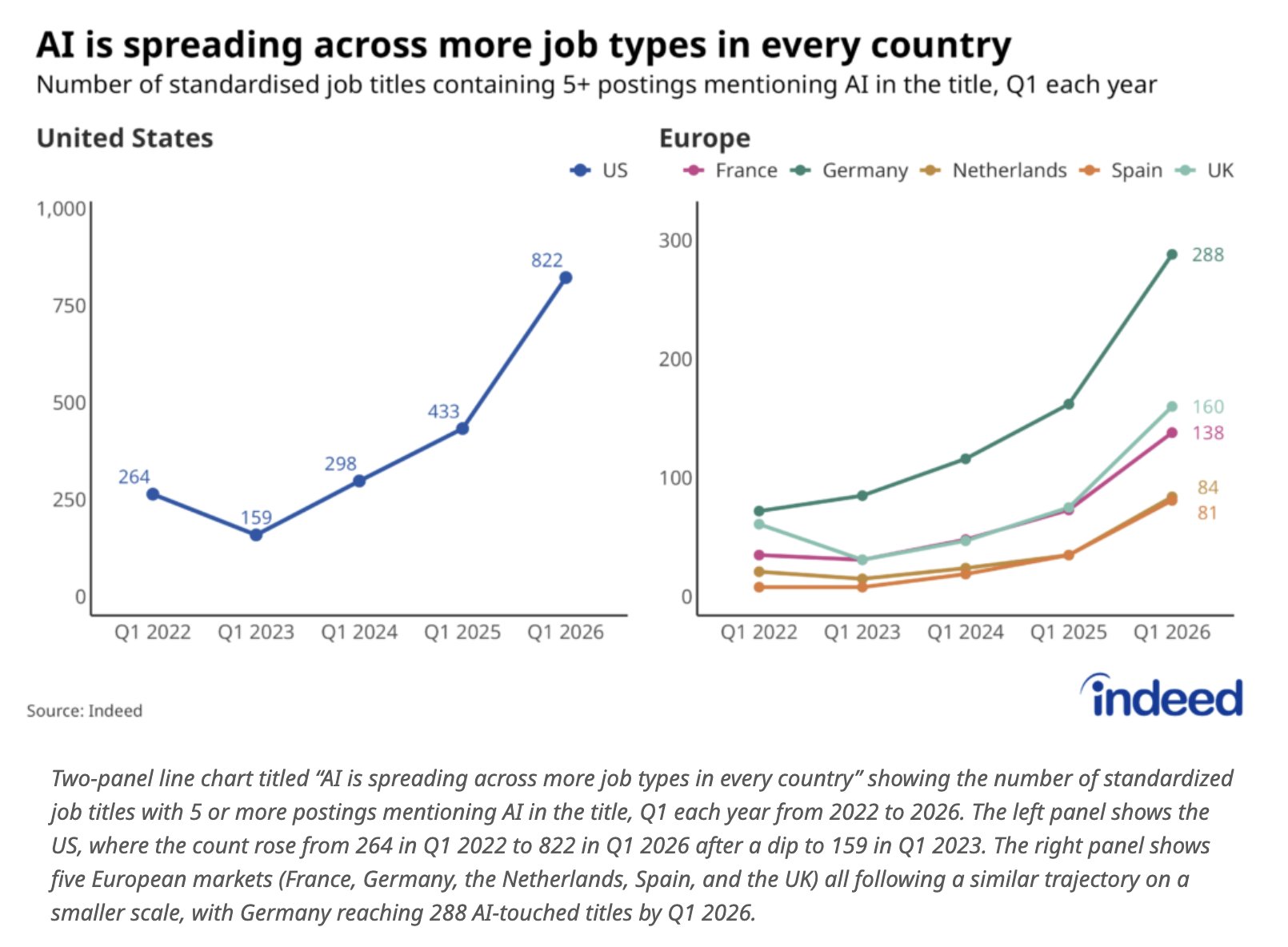

Mike: AI is showing up in the job titles themselves, tripling in the US in just four years.

Source: Indeed as of 3.31.2026

Source: Indeed as of 3.31.2026

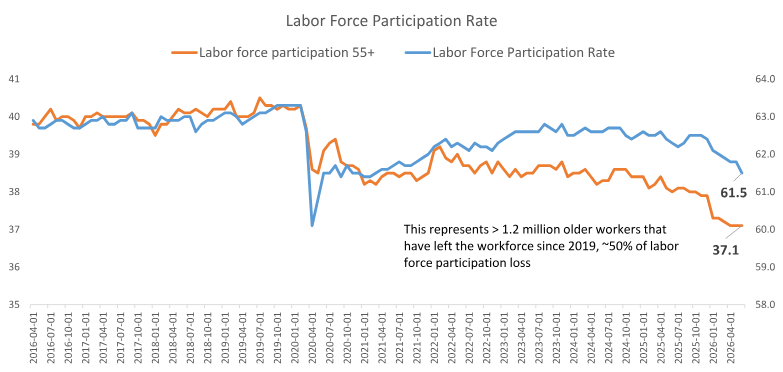

Matt: The broader labor story is still about supply, with more than 1.2 million older workers leaving the workforce since 2019.

Graphic via Raymond James as of 07.03.2026

Graphic via Raymond James as of 07.03.2026

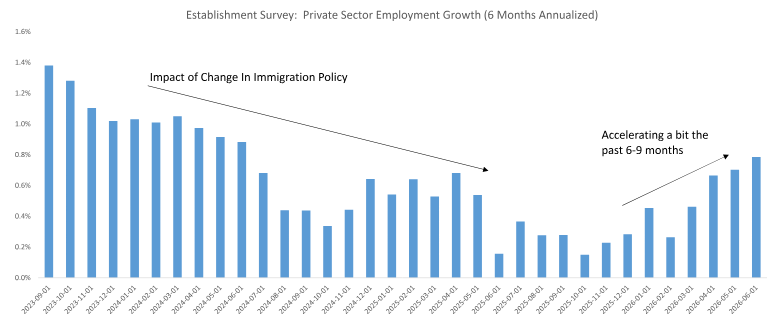

JG: Yet private hiring has quietly accelerated over the past 6 to 9 months.

Graphic via Raymond James as of 07.03.2026

Graphic via Raymond James as of 07.03.2026

JD: That resilience is showing up at the Fed, where the tone of the minutes just turned its most hawkish on inflation since 2022.

Source: Bloomberg Intelligence as of 07.08.2026

Source: Bloomberg Intelligence as of 07.08.2026

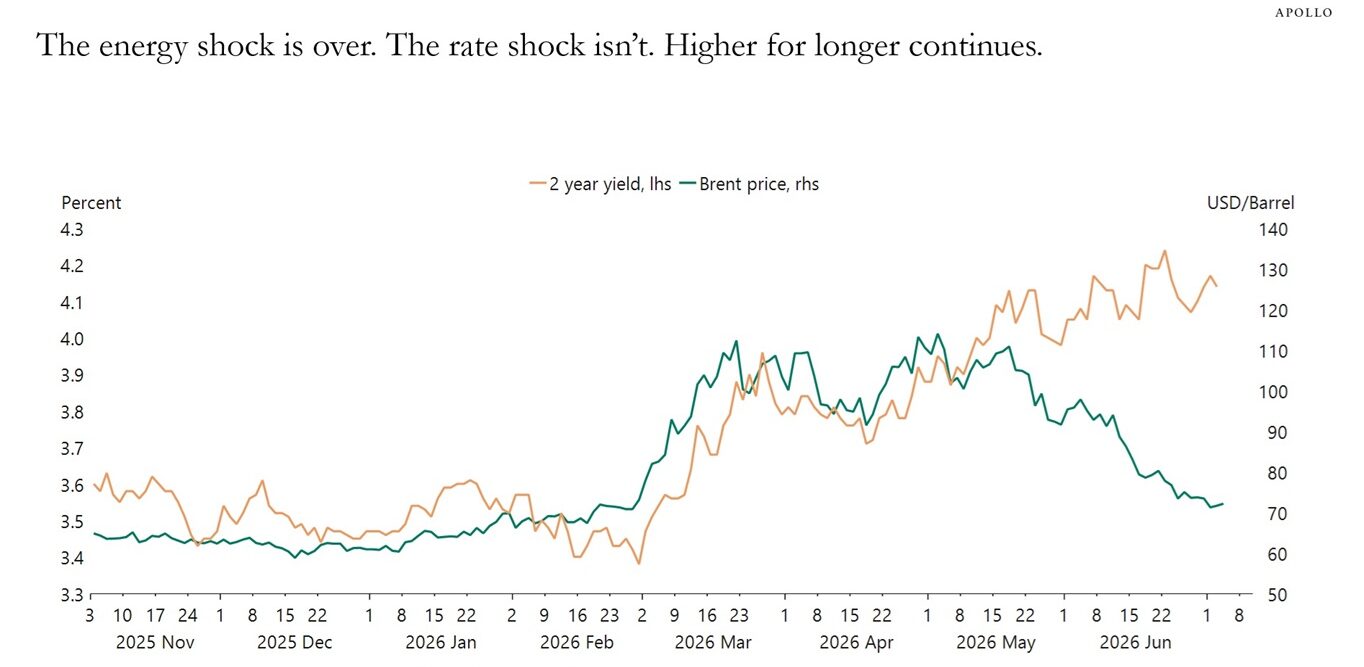

Beckham: Markets agree. While oil has round-tripped the entire Iran spike, 2-year yields have not. The energy shock is over; the rate shock is still to be determined.

Source: Apollo as of 07.08.2026

Source: Apollo as of 07.08.2026

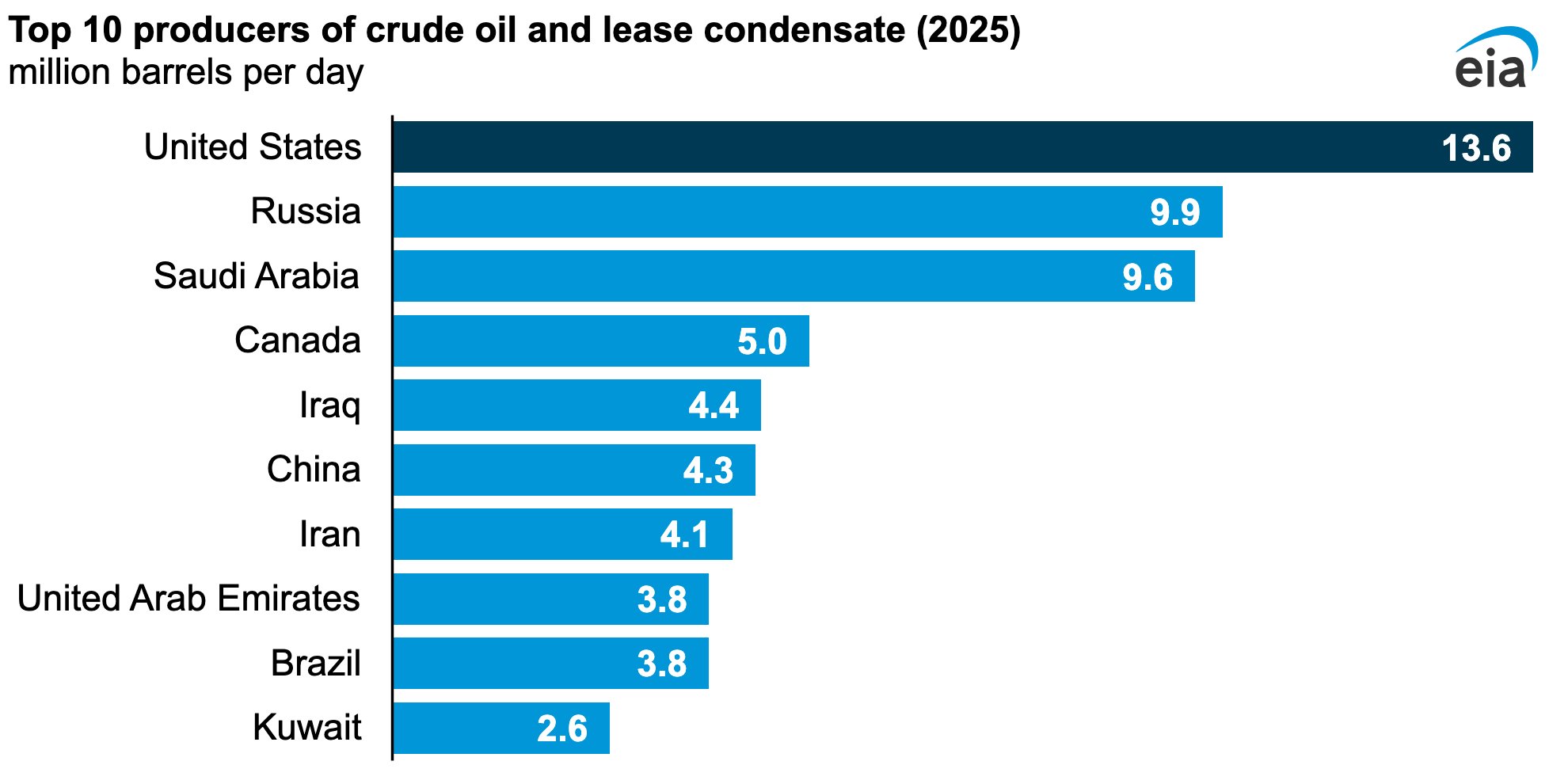

Dave: Cheaper energy remains an American advantage, with US production still lapping the field.

Source: EIA as of 12.31.2025

Source: EIA as of 12.31.2025

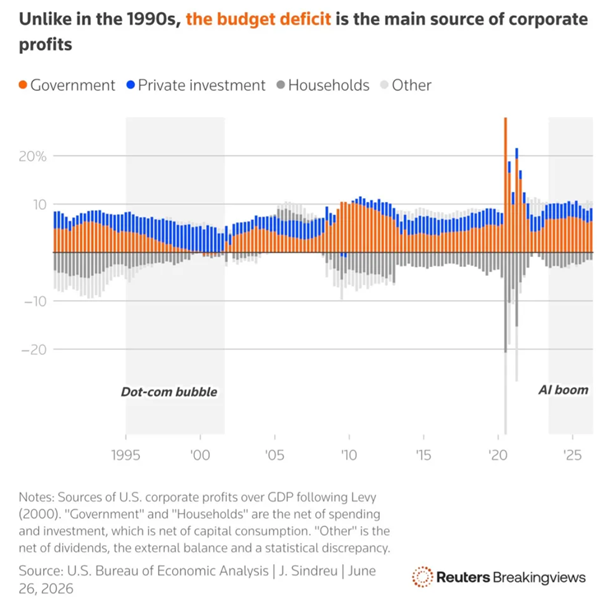

John Luke: Meanwhile, unlike the 1990s, the budget deficit is the main source of corporate profits in this cycle.

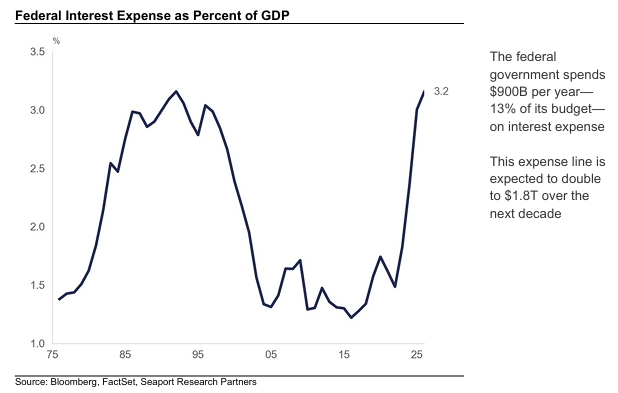

Derek: That support is not free. Federal interest expense has surged past 3% of GDP, roughly $900B per year.

Source: Seaport Research Partners as of 07.07.2026

Source: Seaport Research Partners as of 07.07.2026

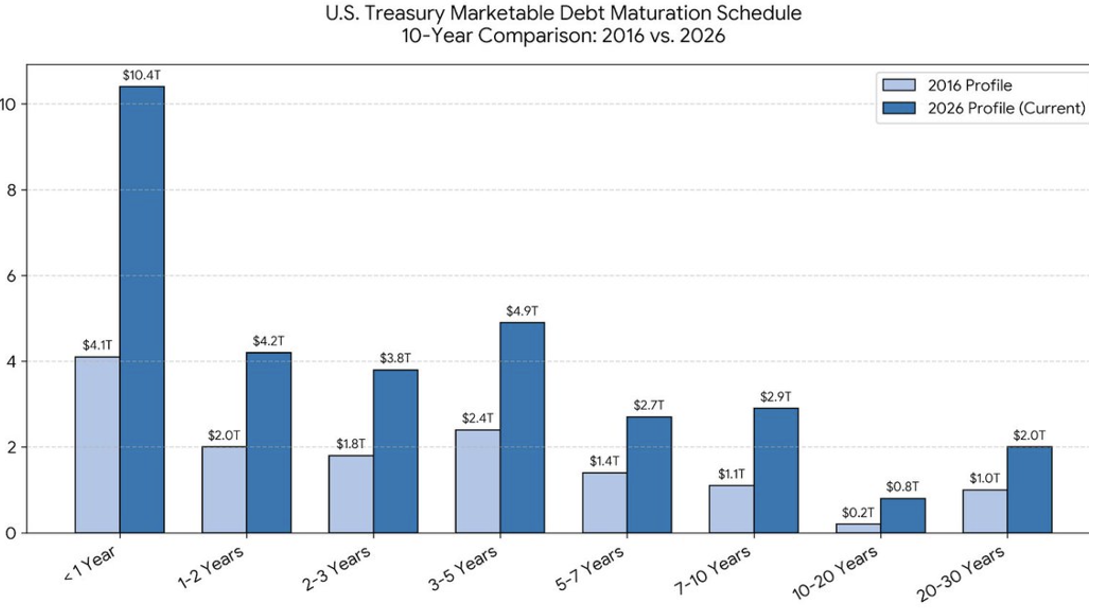

Jake: This is likely to go higher. $10T of Treasury debt will roll within a year at average rates well above the maturing coupons.

Source: Michael Taylor (@Mike_Taylor1972) via X as of 07.09.2026

Source: Michael Taylor (@Mike_Taylor1972) via X as of 07.09.2026

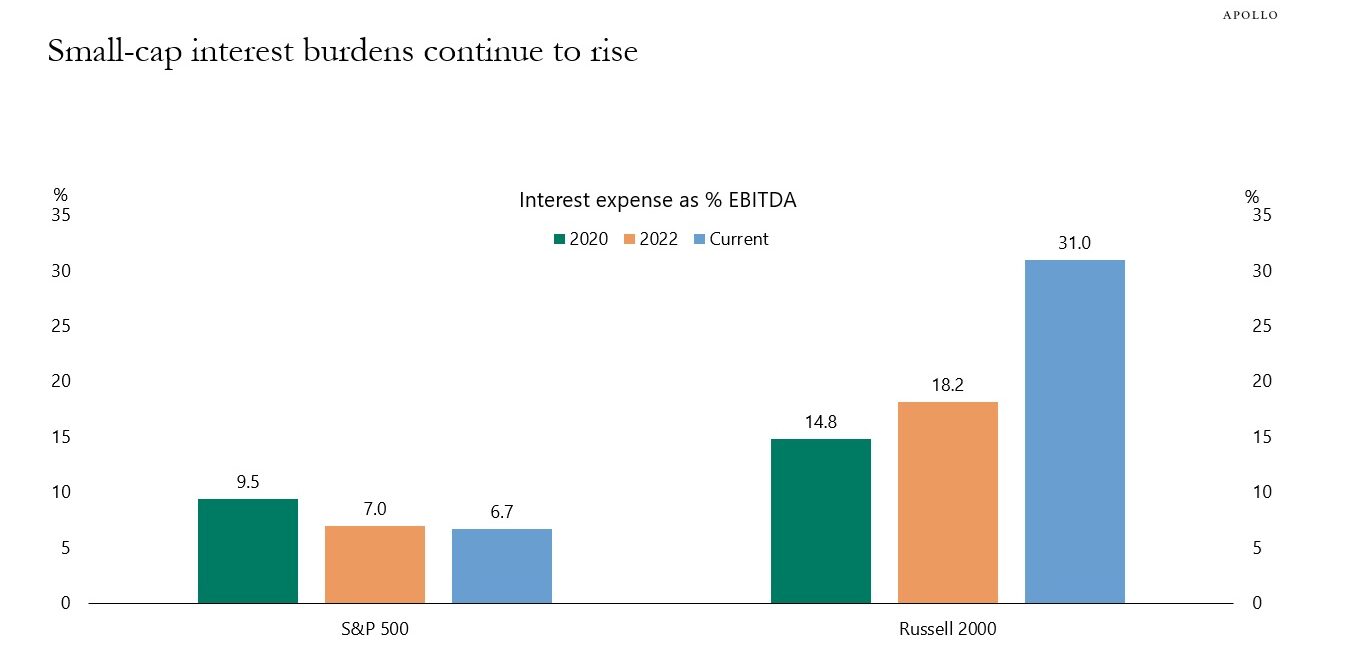

Brian: Small companies feel rates too. Russell 2000 interest burdens have more than doubled since 2020, while the S&P 500’s have fallen. Higher for longer is not a uniform tax.

Source: Apollo as of 07.03.2026

Source: Apollo as of 07.03.2026

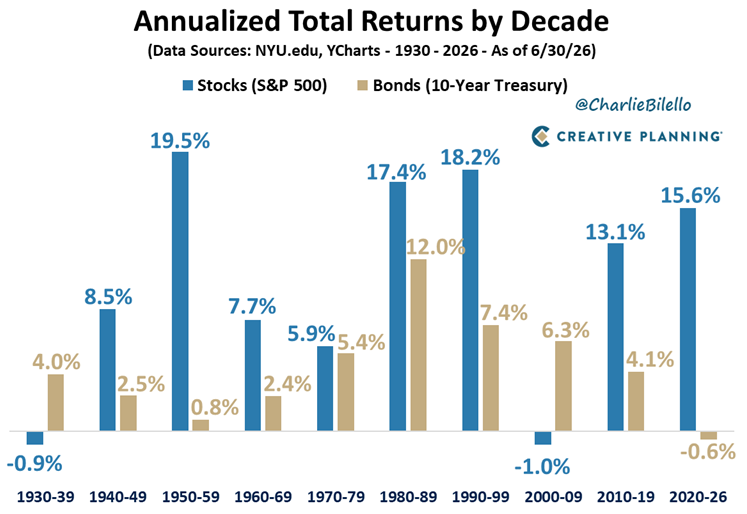

John Luke: Zooming out, the 2020s are shaping up as another strong decade for stocks and the worst on record for bonds. A reminder that how you allocate matters.

Source: Charlie Bilello as of 06.30.2026

Source: Charlie Bilello as of 06.30.2026

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2607-11.