Our team reviews a vast amount of research and market data each week to isolate the signals that matter most. This week’s selection steps back to examine a market broadening beneath the surface: compressing mega-cap multiples, the resurgent 493, the unbreakable link between profits and prices, the staggering scale of AI investment, and a stickier inflation regime nudging the Fed toward tightening. Have a great weekend!

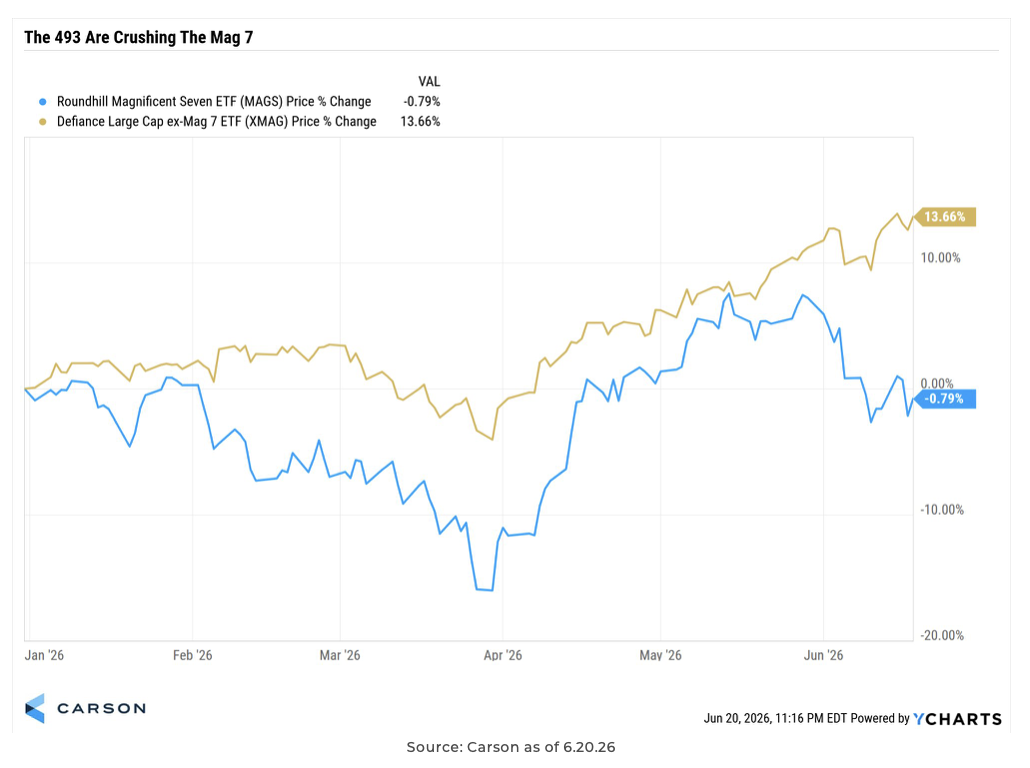

Ten: One of the most remarkable stories of a remarkable year: the Magnificent 7 are roughly flat on the year, while the other 493 are up more than 13%. It was not long ago that every client meeting asked why we did not simply own those seven names. Breadth, it turns out, still matters.

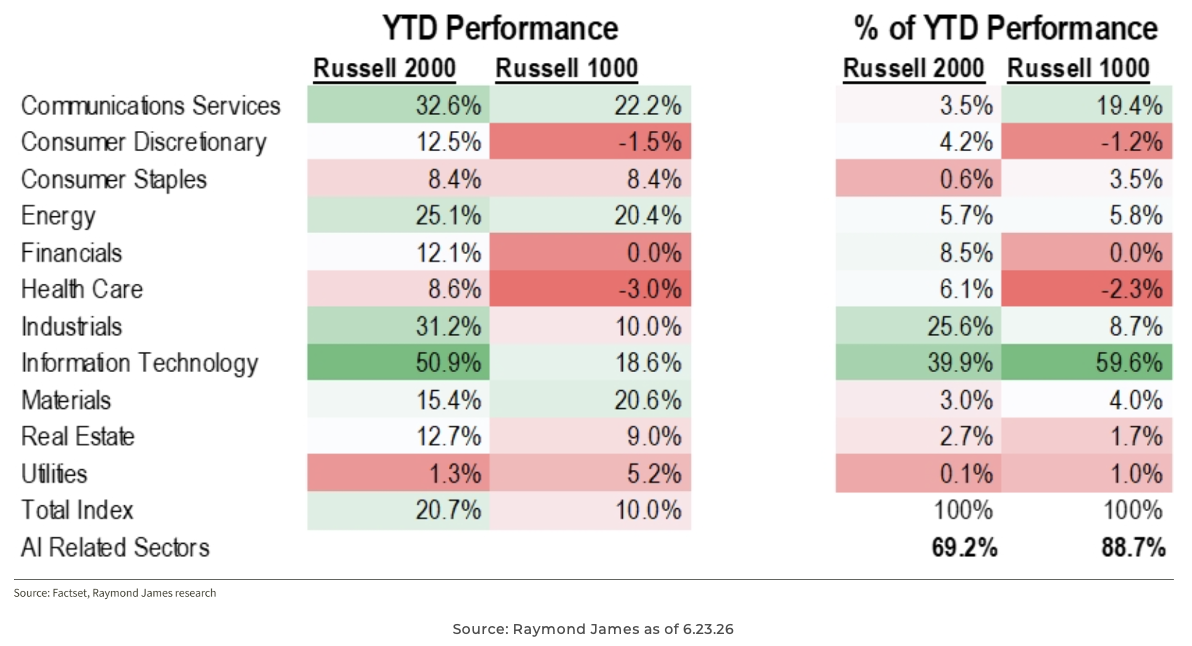

JG: AI-related sectors accounted for roughly 89% of Russell 1000 returns in the first half of 2026, versus 69% in the Russell 2000, where leadership has been considerably broader. Notably, small caps have outperformed large caps this year, with gains spread across nine of eleven sectors rather than concentrated at the very top.

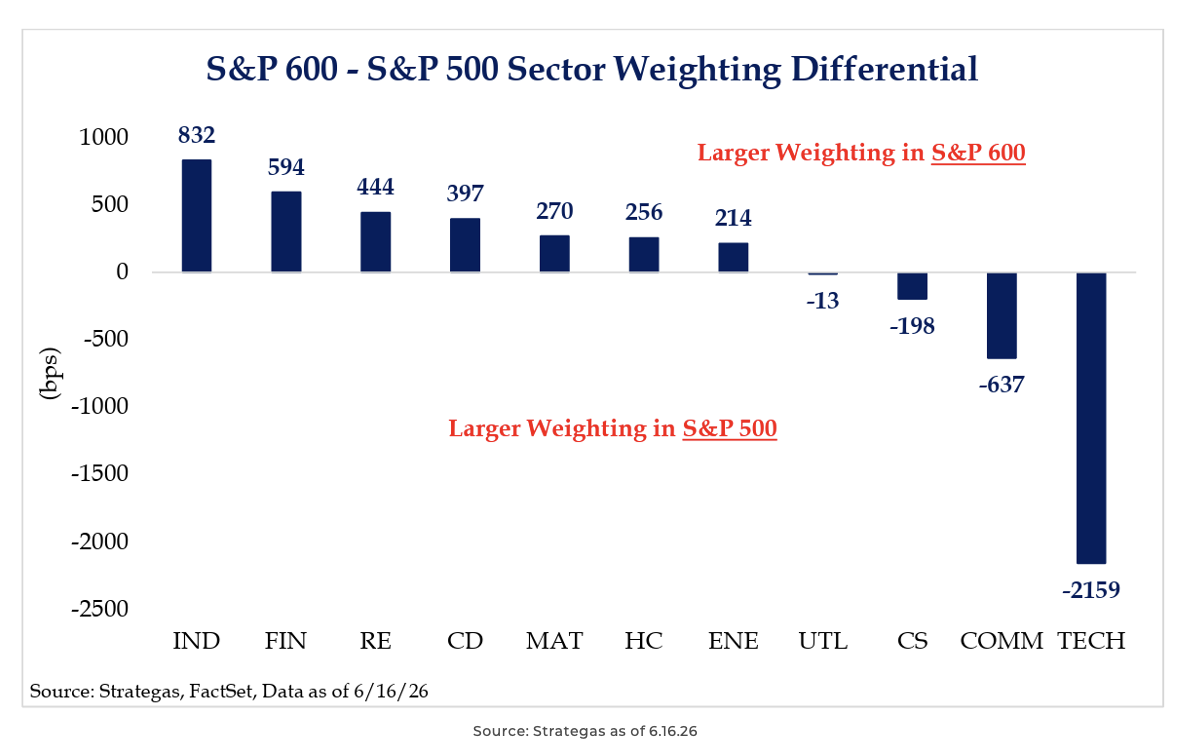

John: Small caps are not simply a smaller version of the S&P 500; they are a different bet entirely. The S&P 600 carries roughly 21% less Technology and far more Industrials, Financials, and Real Estate. For investors looking to diversify away from mega-cap concentration, the composition matters as much as the size.

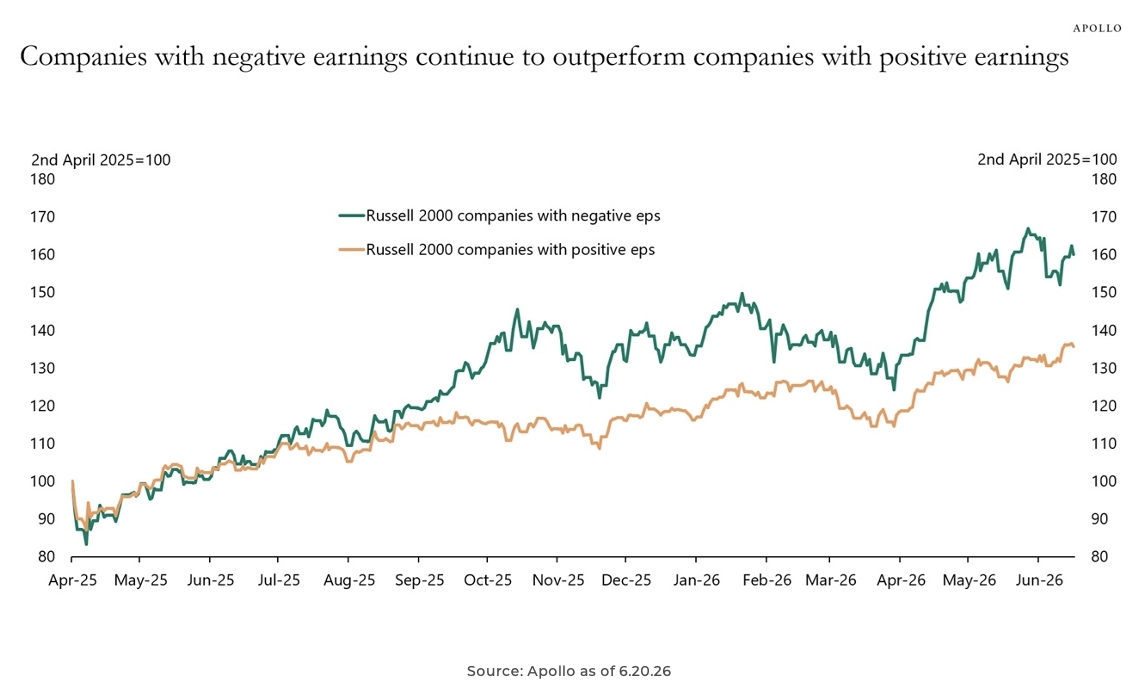

Dave: Underneath that small-cap surface, there is a fascinating quality anomaly playing out. Russell 2000 companies with negative earnings have continuously outperformed companies with positive earnings over the last year, highlighting the highly speculative, liquidity-driven nature of this specific cohort.

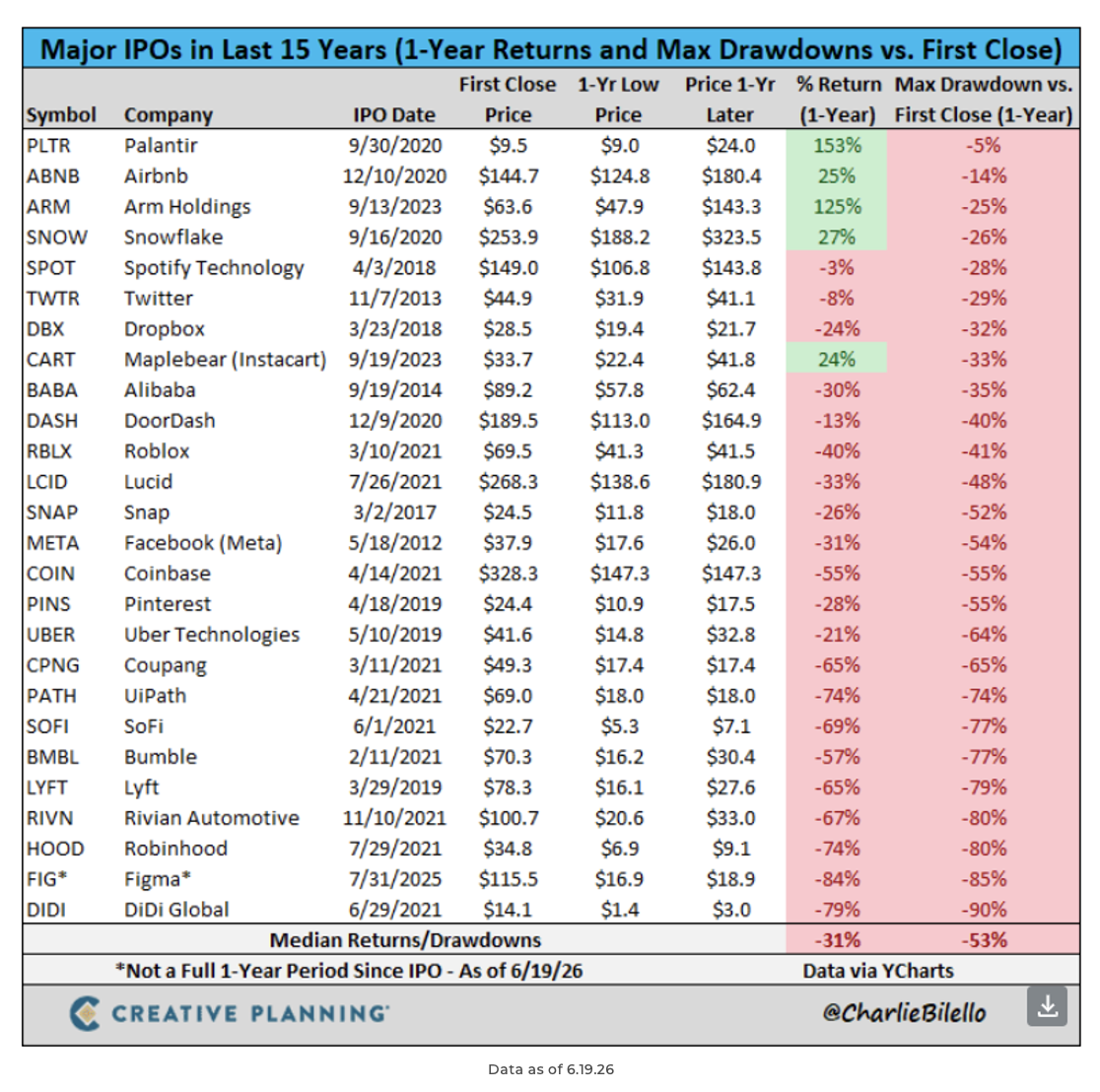

Mike: The historical data on major IPOs over the last 15 years offers a clear warning against chasing early hype. With a dismal median one-year return of -31% and a large max drawdown, high-profile market debuts typically face an uphill battle once the initial excitement fades.

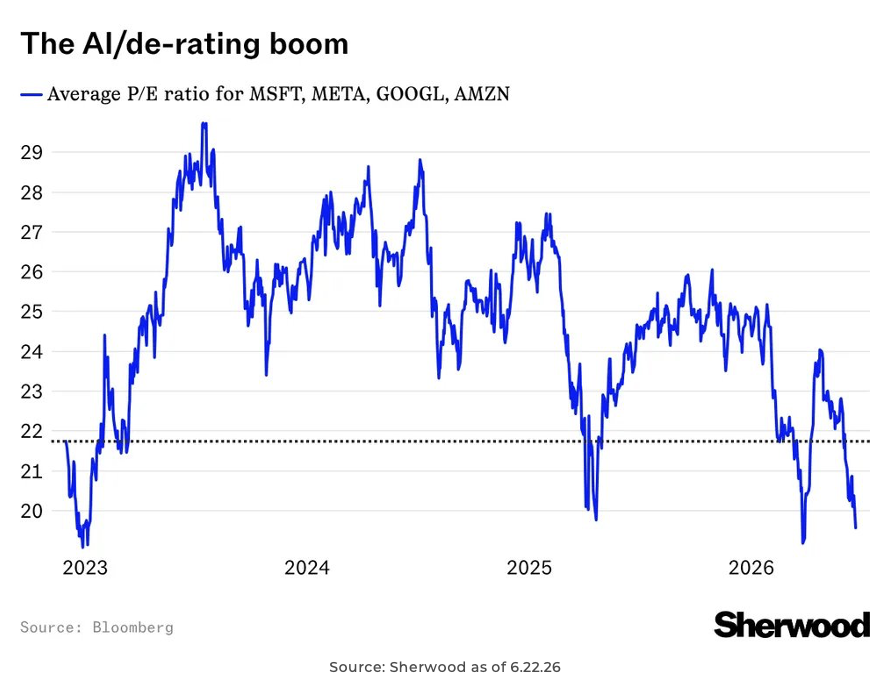

Brian: Shifting away from the headline noise about tech overvaluation, a significant under-the-surface de-rating has occurred. The average P/E ratio for Microsoft, Meta, Google, and Amazon has compressed off its highs and now sits comfortably below 20x.

John Luke: Semiconductors were long priced as a cyclical industry. When margins peaked, price-to-sales multiples fell. That relationship has seemingly broken. Over the past year, multiples have expanded right alongside record 41.7% margins, leaving one of two conclusions: 1) the industry has become structurally less cyclical or 2) this is a sign of exuberance.

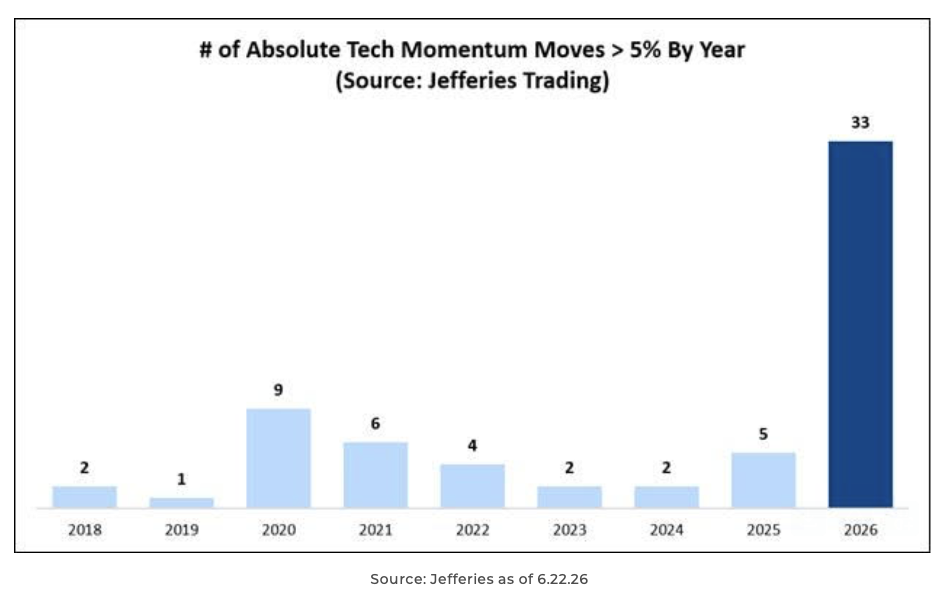

Mark: Beneath a calm-looking index surface, Technology has been trading with unusual ferocity in 2026. The sheer frequency of these outsized daily swings underscores how much now rides on every incremental AI headline.

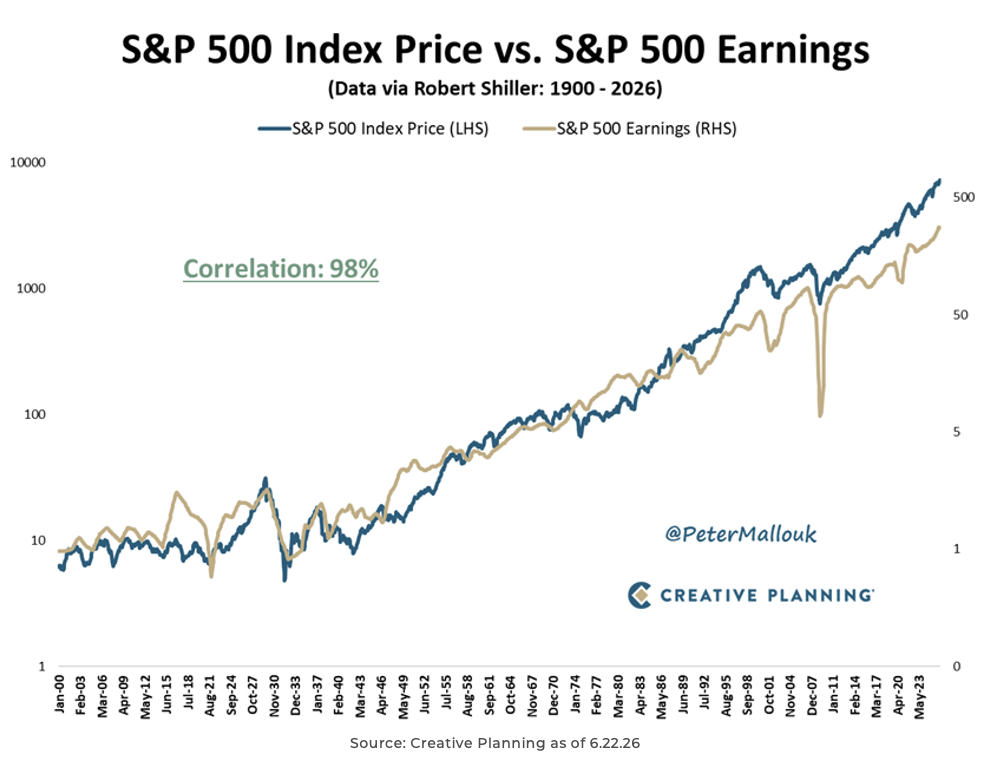

Brad: Through all the short-term chaos, 126 years of market history tell an incredibly simple story. Stocks and earnings move together with a 98% correlation. The short run is entirely about noise and speculation, but the long run is strictly about profits. Speculators chase the noise; true investors simply follow the corporate bottom line.

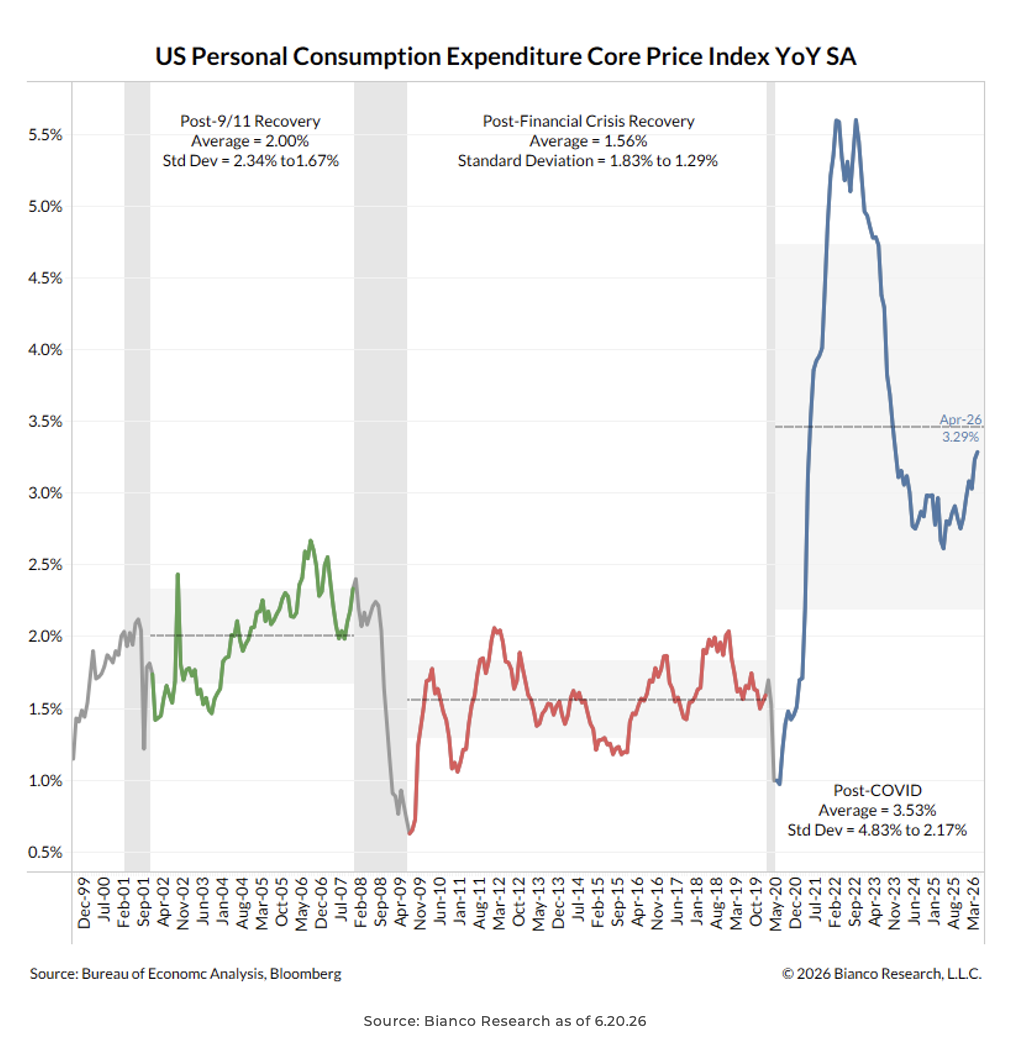

Joseph: Core PCE continues to run near 3.3%, a full point above the post-financial-crisis regime. This is not a return to the 1.5% world that defined the last expansion; inflation has reset structurally higher. That backdrop is exactly why the Fed’s path has turned hawkish rather than accommodative.

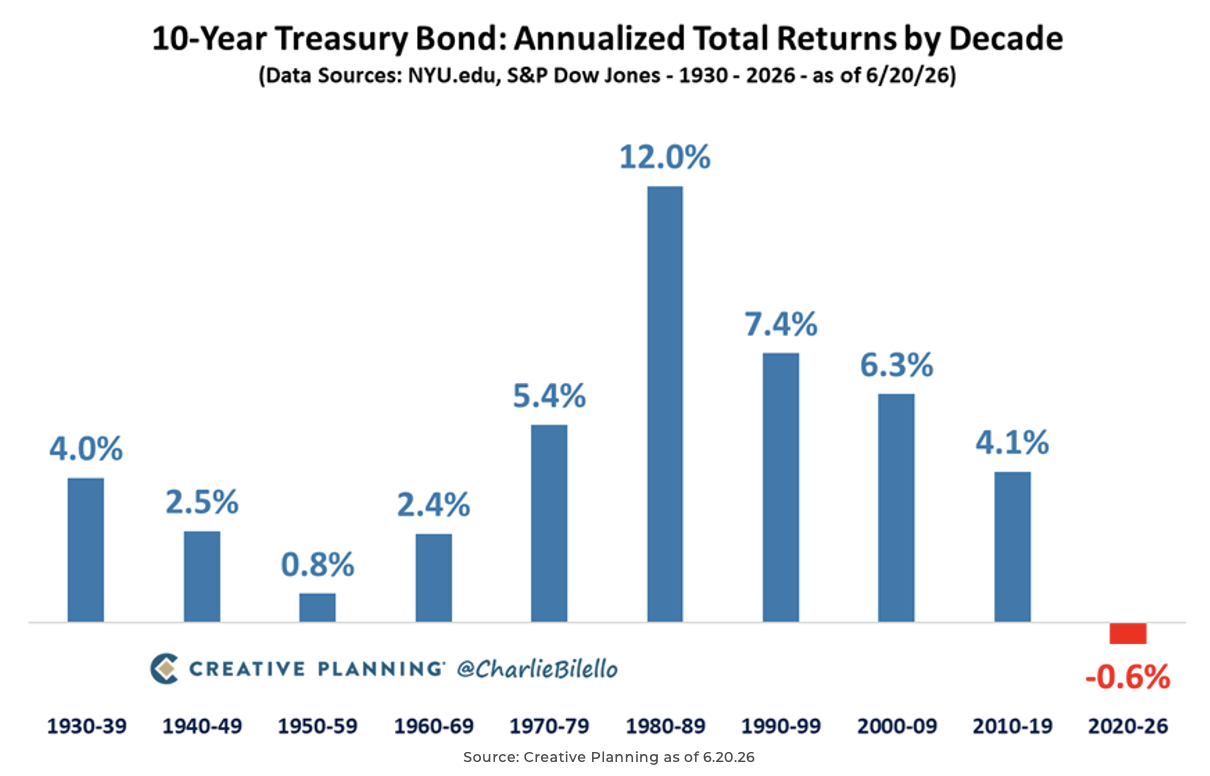

Derek: The 2020s are on pace to be the worst decade in history for 10-Year Treasury bonds with annualized total returns of -0.6%.

Beckham: A great chart for the current macro. Technology investment (teal) has now eclipsed residential fixed investment (purple), a remarkable role reversal for the U.S. economy. The question for the Fed: can rate hikes actually slow tech spend, or will they simply hurt housing further while leaving the AI build-out untouched?

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2606-16.