Our team reviews a vast amount of market research and economic data every day. This week’s selection highlights the resilience of the labor market, the broadening dominance of technology flows, and the underlying shifts in U.S. infrastructure and business creation. Here is a summary of the signals shaping the current environment.

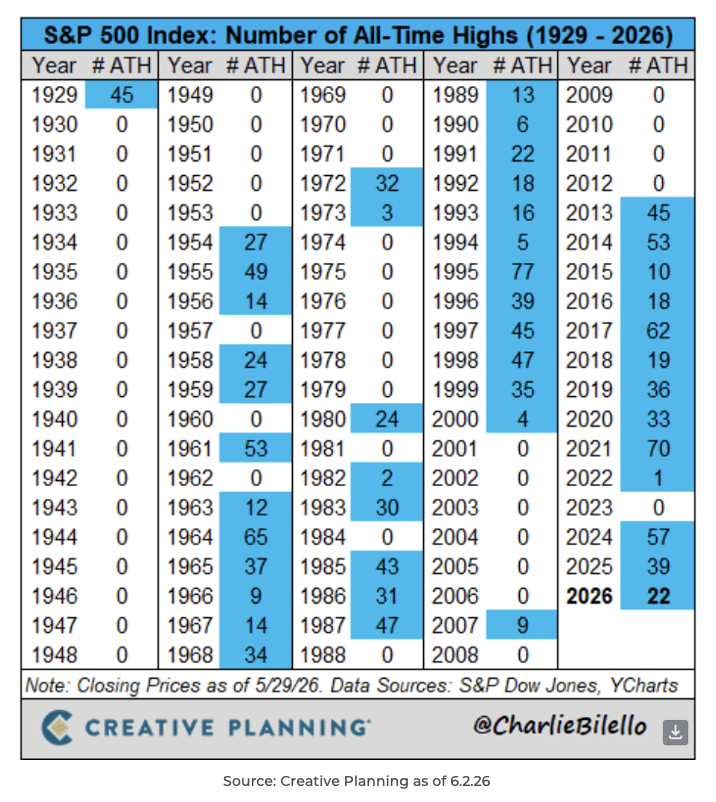

Brad: The S&P 500 continues its historic upward march, having already logged 22 all-time highs so far in 2026. With seven months still left in the year, this relentless pace highlights the fundamental momentum anchoring the broader market.

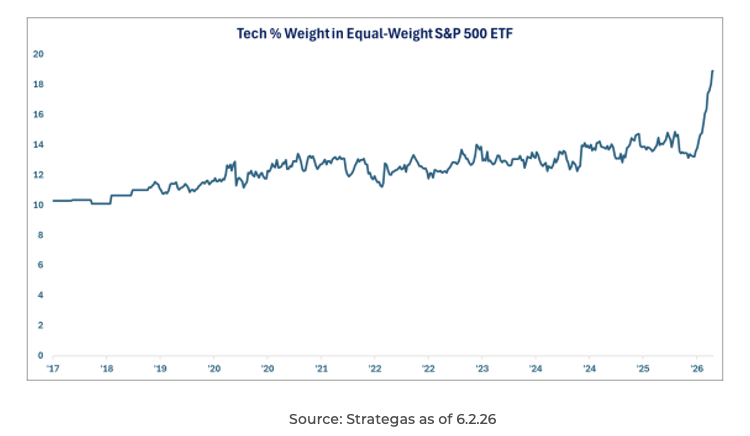

Jake: Tech dominance isn’t just a market-cap-weighted story anymore. The Information Technology sector’s percentage weight in the Equal-Weight S&P 500 ETF has surged.

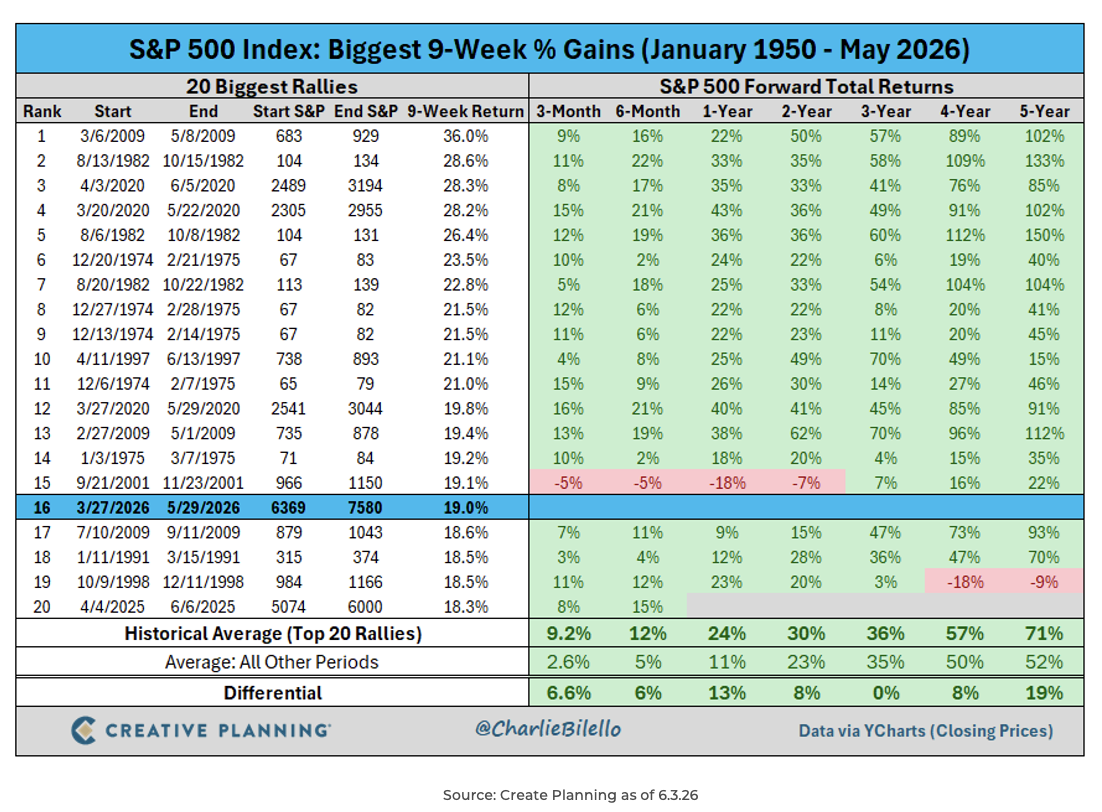

Beckham: This rally has earned its place in the history books. The current 9-week surge (+19%) ranks as the 16th strongest since the 1950s. Crucially, historical data reveals that out of the top 20 strongest 9-week rallies, almost all were followed by further sustained gains over the subsequent 3, 6, and 12 months.

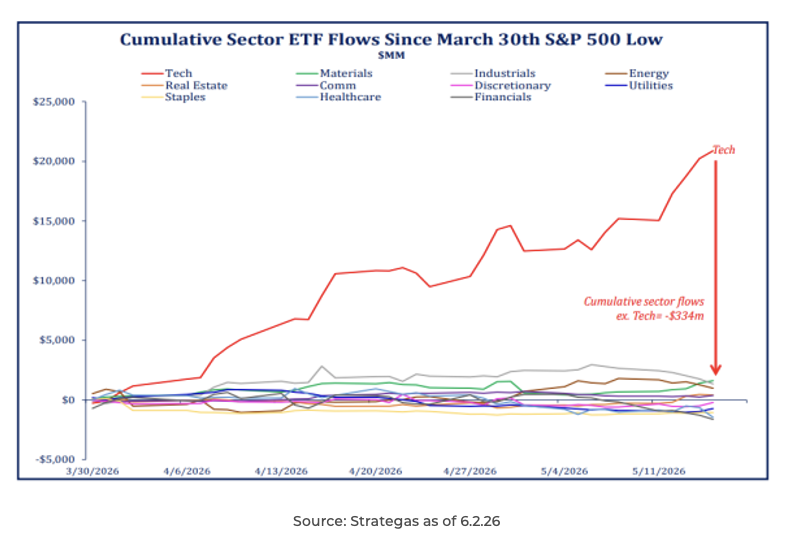

Ten: Performance has been aggressively concentrated, driven by non-discretionary flows into technology as the fear of missing out on the AI trade keeps investors single-mindedly focused on one sector.

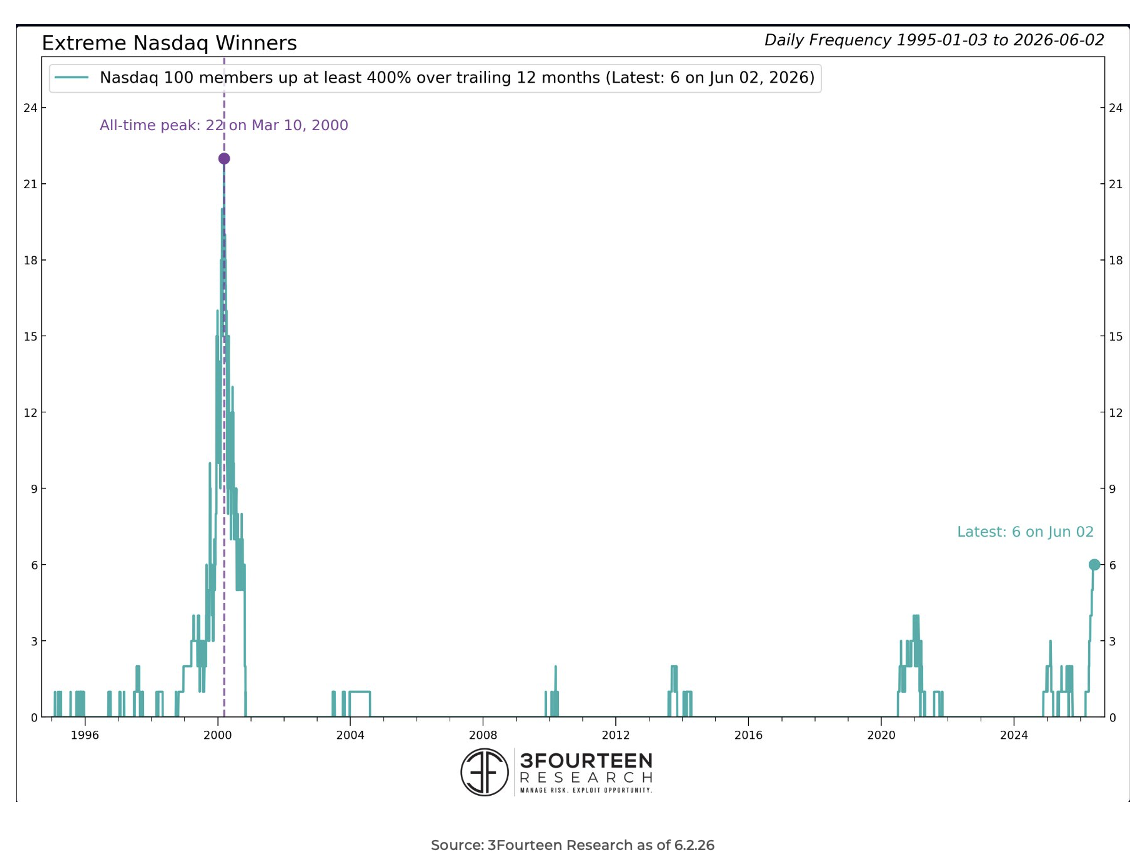

Mark: We are seeing a historic number of “extreme” Nasdaq winners—stocks up at least 400% over a 12-month period—reaching levels last seen in 2000. However, while the concentration is notable, a look at the data shows we still have a long way to go to match the sheer breadth and mania of the dot-com bubble peak.

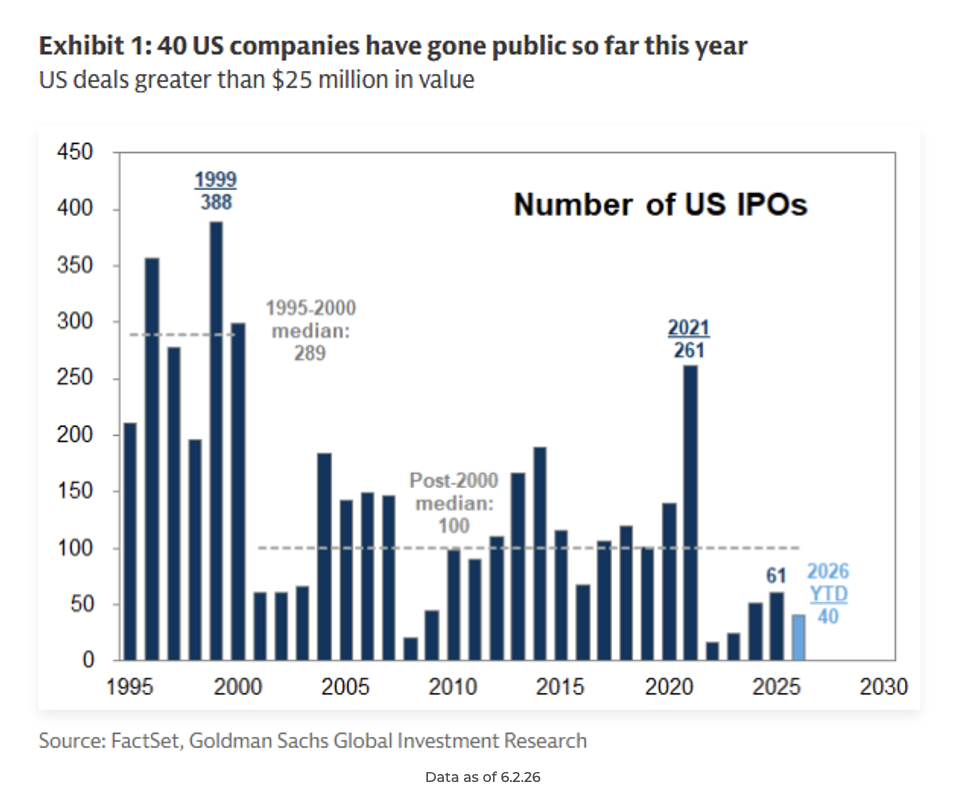

Brett: Public equity markets are showing continued stabilization. So far in 2026, 40 U.S. companies have gone public via deals greater than $25 million in value. While activity remains well below the extreme frenzy of 2021, it represents a steady, normalized pace for high-quality issuances.

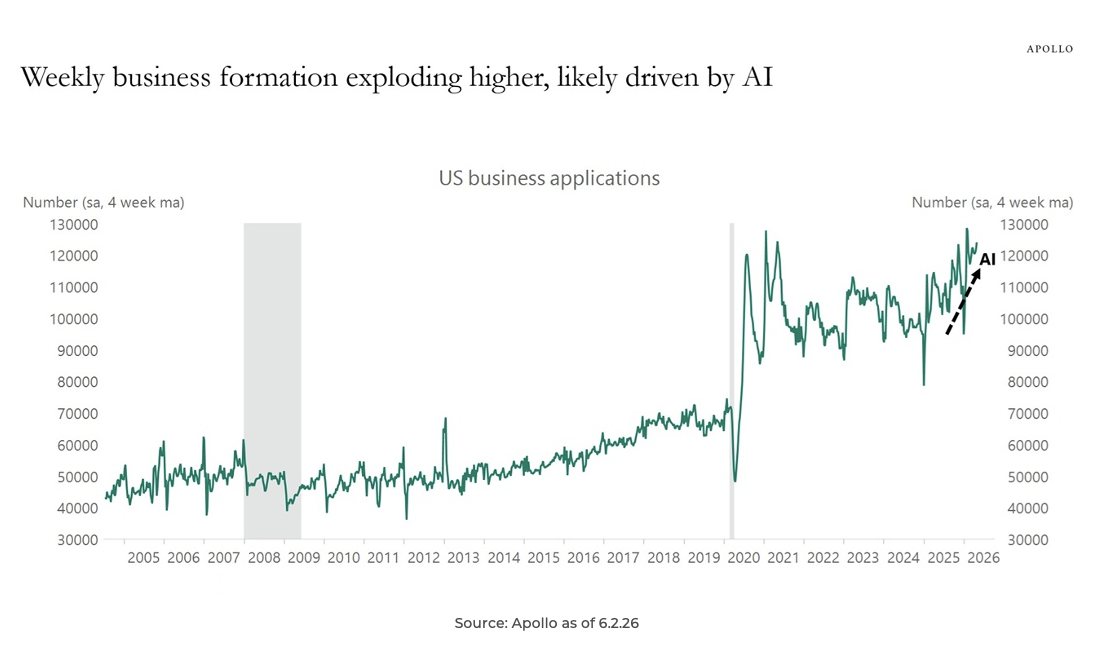

Dave: Artificial Intelligence is quietly igniting a massive entrepreneurial boom. By drastically reducing the cost and complexity of launching a company, AI and large language models are fueling an explosion in new U.S. business applications.

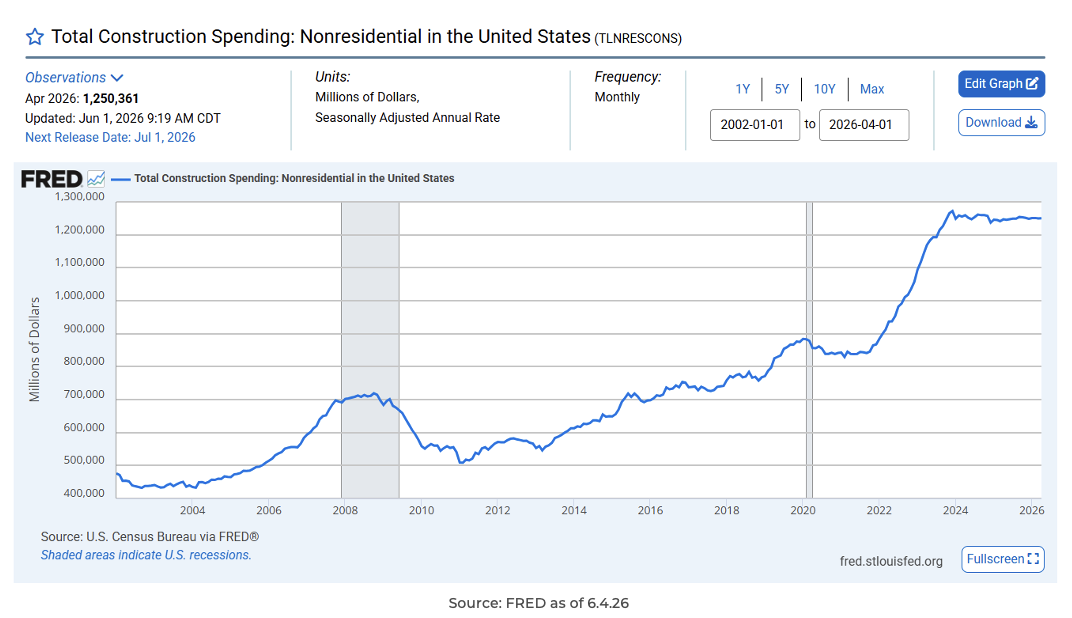

JD: A recent dip in the Manufacturing Construction index isn’t a sign of economic weakness, but rather a transition in the lifecycle of mega-projects. The initial phase of building physical structures for CHIPS Act mega-fabs has peaked, and capital is now shifting toward filling those buildings with highly specialized, expensive equipment. To track the true scale of the ongoing industrial and AI data center build-out, Total Nonresidential Construction Spending is the metric to watch, and it remains near all-time highs.

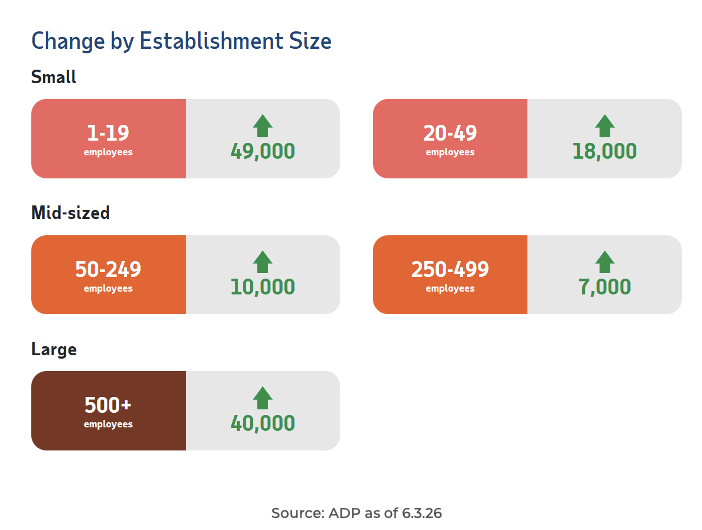

Joseph: The labor market is carrying sustained momentum into the summer months. Private employers added 122,000 jobs in May, with hiring remaining highly broad-based as eight out of ten supersectors showed gains. Notably, small businesses (1–19 employees) led the charge by adding 49,000 jobs, proving resilience at the grassroots level of the economy.

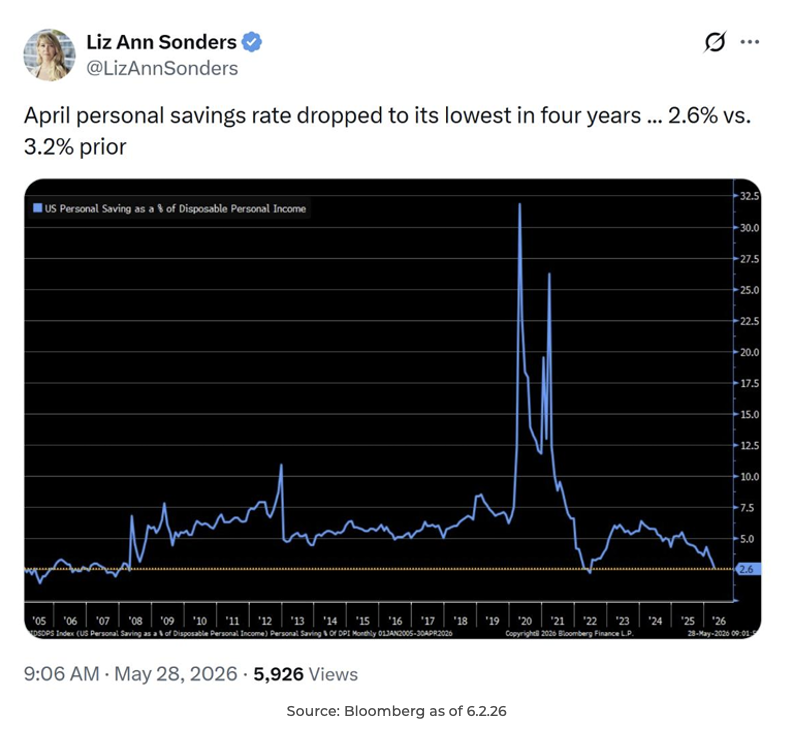

John Luke: The April personal savings rate dropped to 2.6%, hitting its lowest level in four years. Despite this, consumer demand remains resilient, largely due to intergenerational wealth transfers. With over 70% of Gen Z and Millennials borrowing from family to cover basic needs, this dynamic creates a “floor” for aggregate consumption from below, while Baby Boomer spending continues to drive it from above.

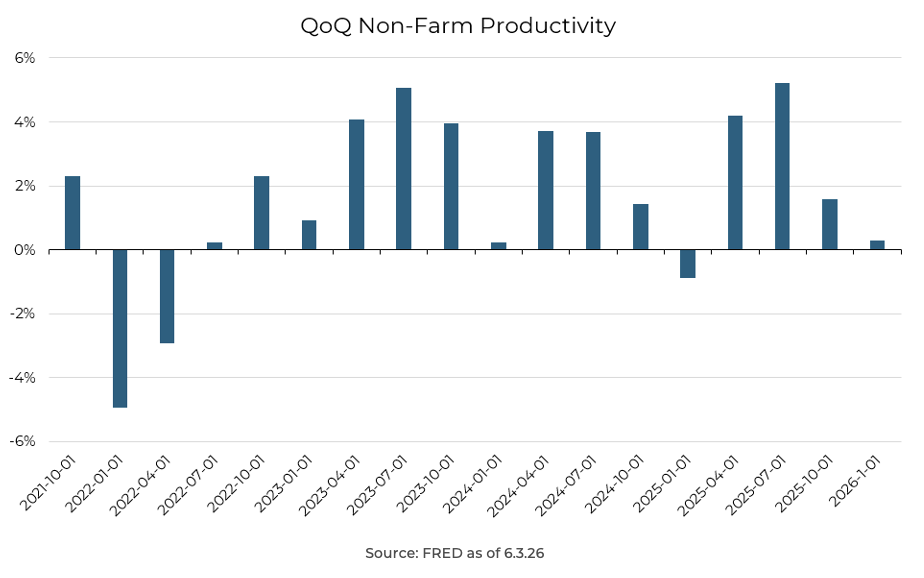

Brian: If AI is radically improving productivity across the economy, it sure isn’t showing up in the data. That’s 0.3% annualized in 1Q and 1.6% in 4Q, well below long-term trends or pre-AI rates.

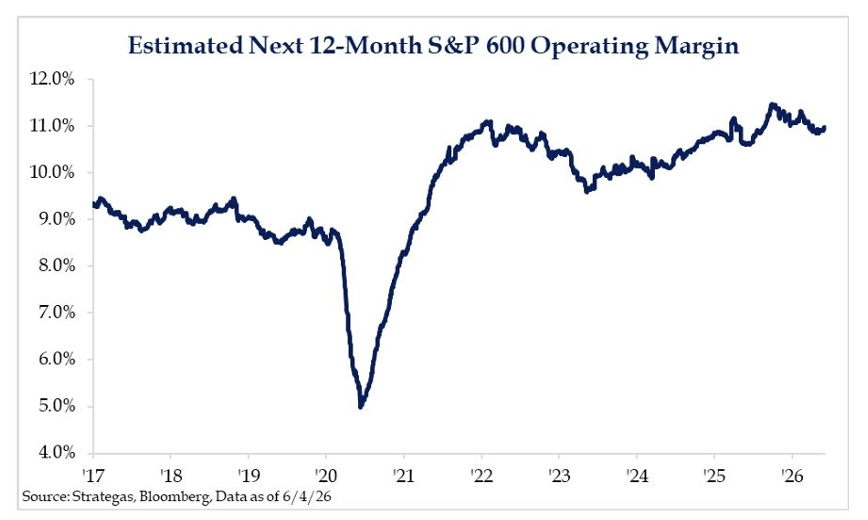

Derek: Forward-looking margins for small-cap companies tell a similar story. S&P 600 operating margins have not experienced the same structural lift seen in the S&P 500 or the equal-weighted index. If AI is to deliver the sweeping efficiencies expected, we should eventually see meaningful margin expansion in smaller enterprises, making this a critical data series to track.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2606-7.