Our research team analyzes daily data to identify essential market signals, and this week’s selections highlight market uncertainty, geopolitical tensions, AI’s impact on productivity, and a significant disconnect in credit markets. These charts explore why markets historically recover quickly from global shocks and how AI is driving both new business formations and higher corporate efficiency. We also examine record-level corporate margins that persist despite rising costs and why diverging high-yield credit may signal risks for public markets.

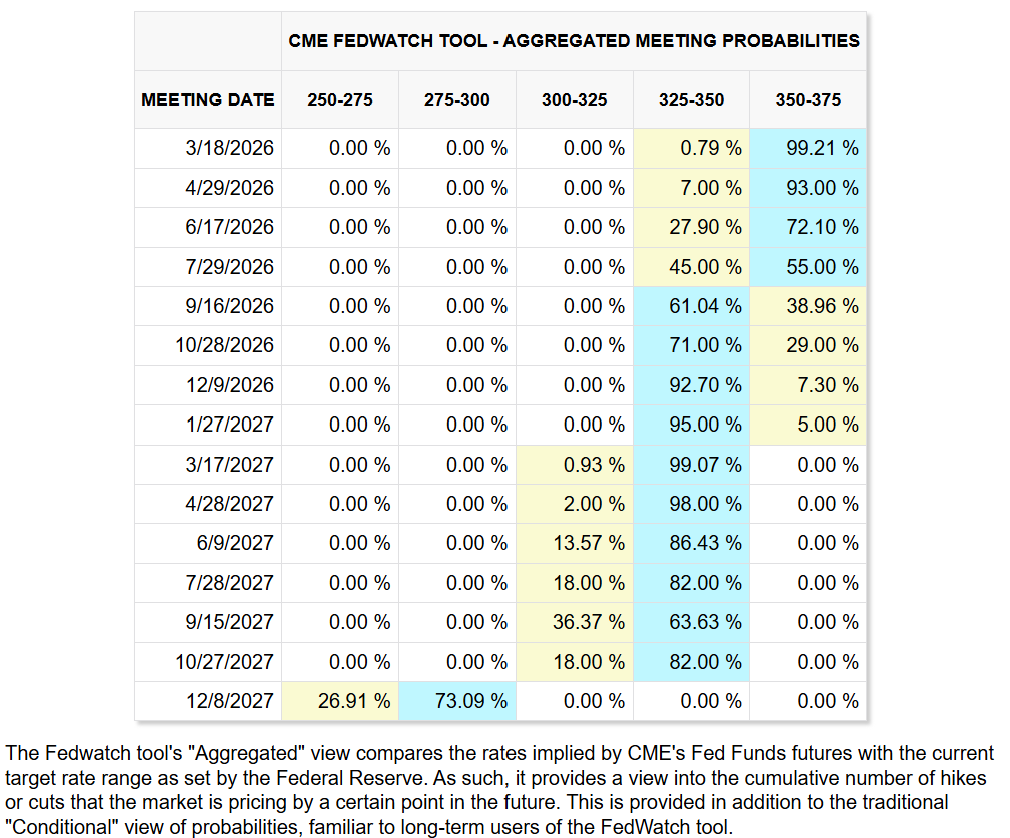

Beckham: Markets are now expecting just one rate cut over the next year, sometime this summer

Source: CME FedWatch Tool as of 03.13.2026

Source: CME FedWatch Tool as of 03.13.2026

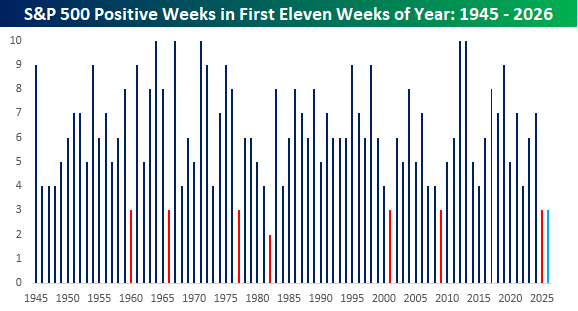

JD: with the adjustment in expectations resulting in a choppy start to the year for the S&P 500.

Source: Bespoke as of 03.13.2026

Source: Bespoke as of 03.13.2026

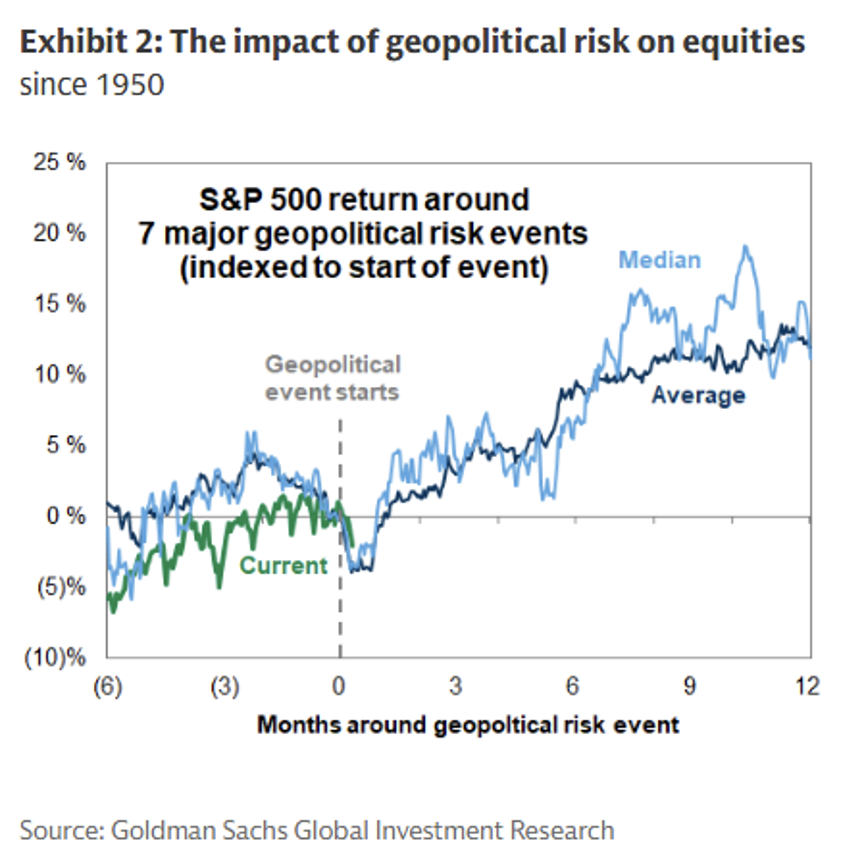

Brad: Markets have historically reacted sharply, but briefly, to geopolitical shocks. While the recent Middle East escalation caused an initial sell-off, the S&P 500 recovered quickly as it has done in the past.

Graphic as of 03.06.2026

Graphic as of 03.06.2026

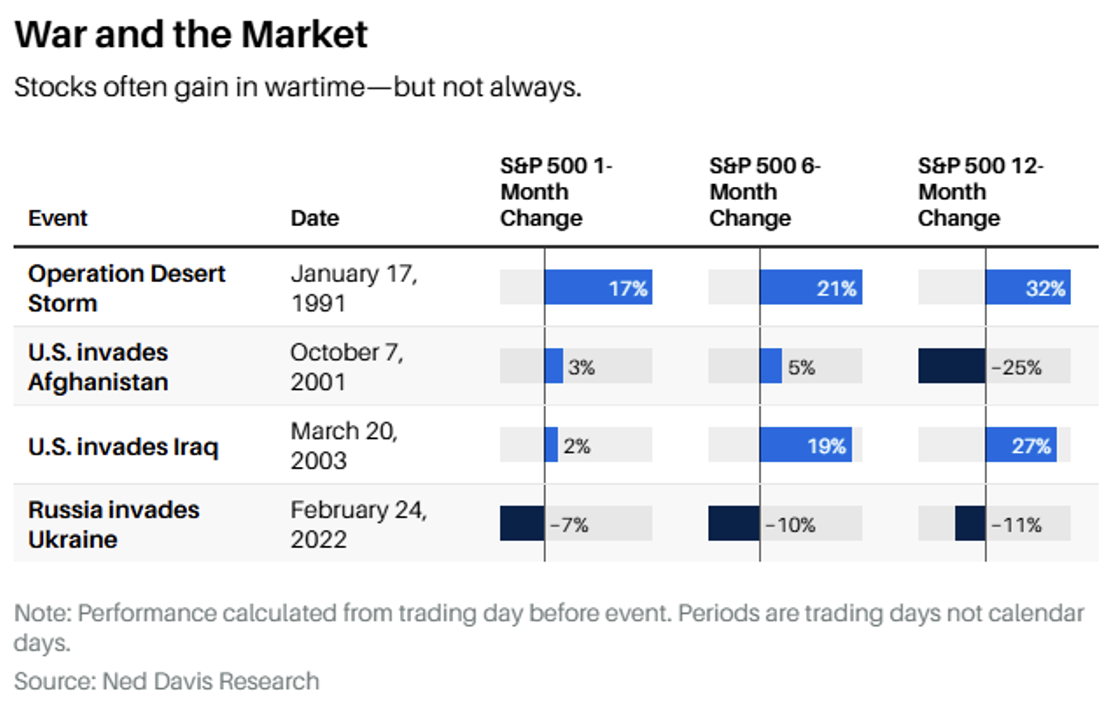

Dave: Another view is that shows geopolitical events are often much scarier in the headlines than they are to subsequent market returns.

Graphic as of 03.02.2026

Graphic as of 03.02.2026

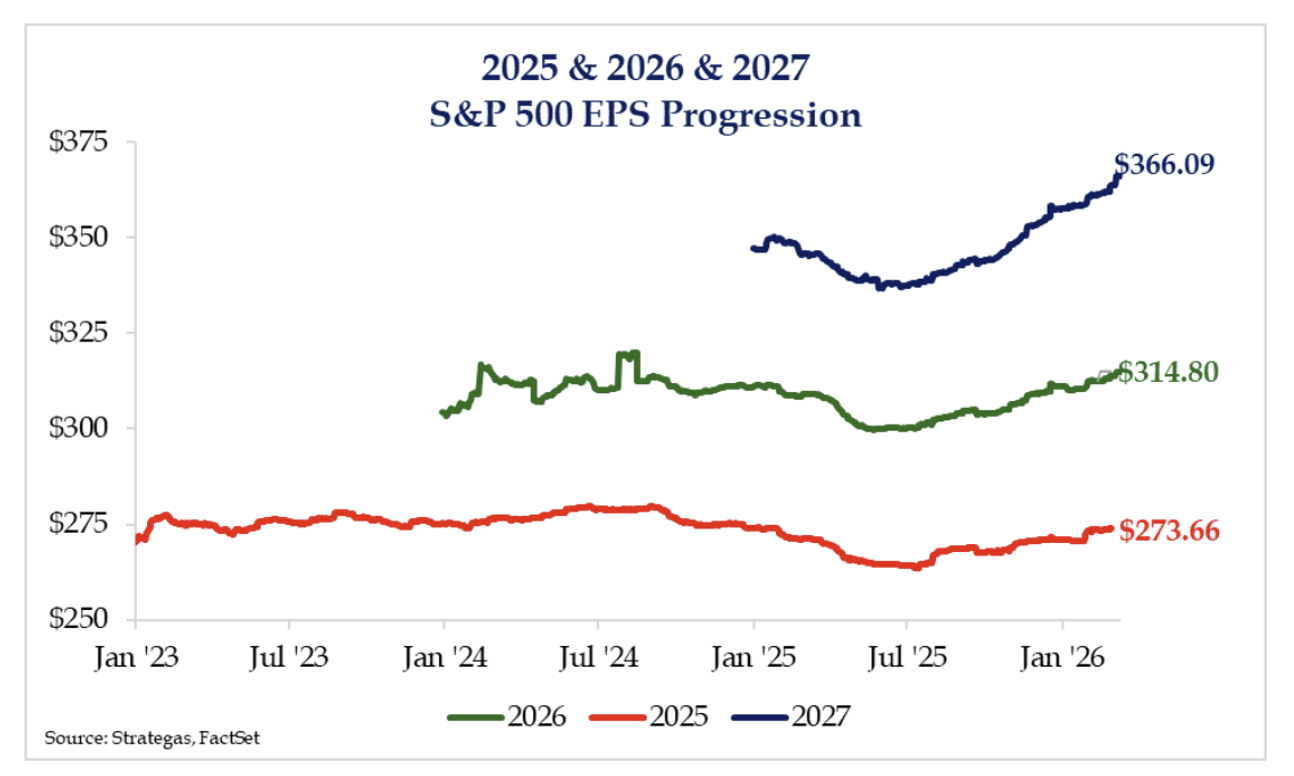

Derek: Despite recent geopolitical tensions, S&P 500 earnings forecasts have remained remarkably resilient, actually trending higher since the onset of the conflict. This upward revision suggests that fundamental growth drivers and corporate profitability are currently outweighing the macro uncertainty.

Data as of 03.12.2026

Data as of 03.12.2026

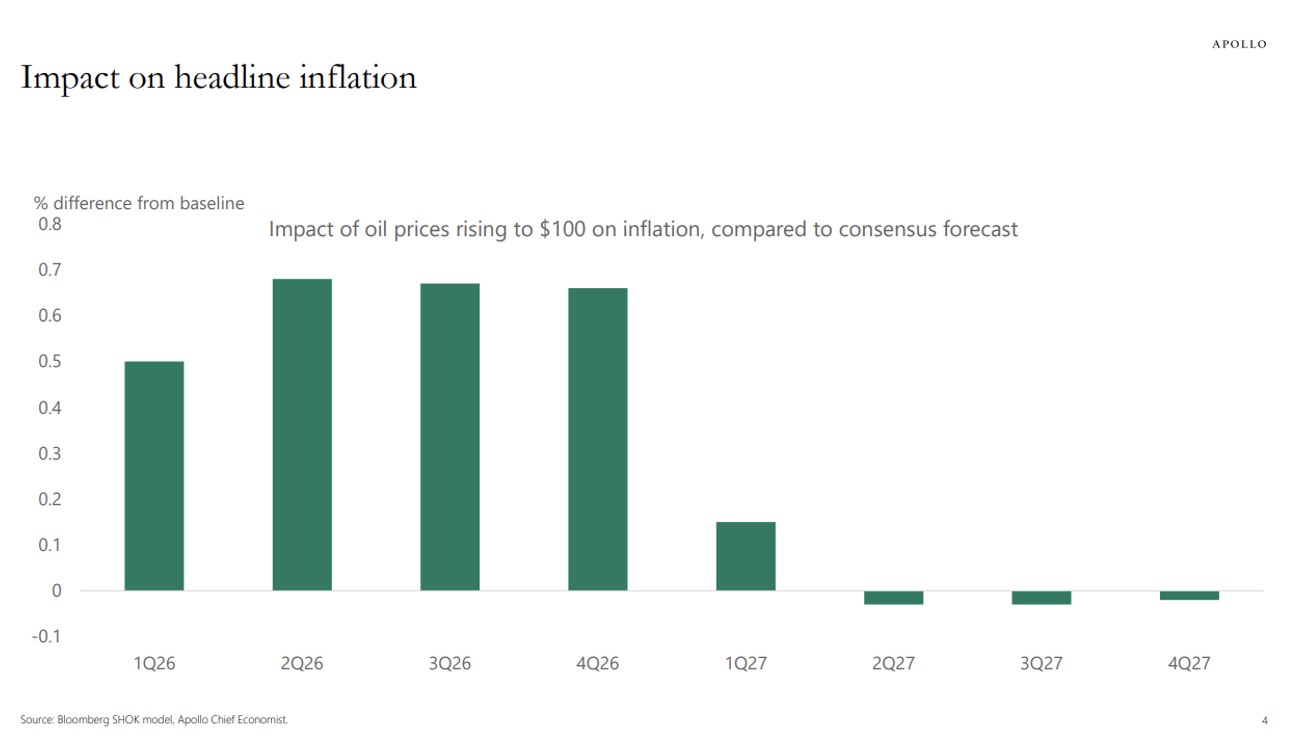

Ten: One area to watch is the longer-term impact of rising oil prices. If they get to and remain at $100, the resulting spike in headline inflation could alter the consensus forecast for the remainder of 2026.

Source: Apollo as of 03.09.2026

Source: Apollo as of 03.09.2026

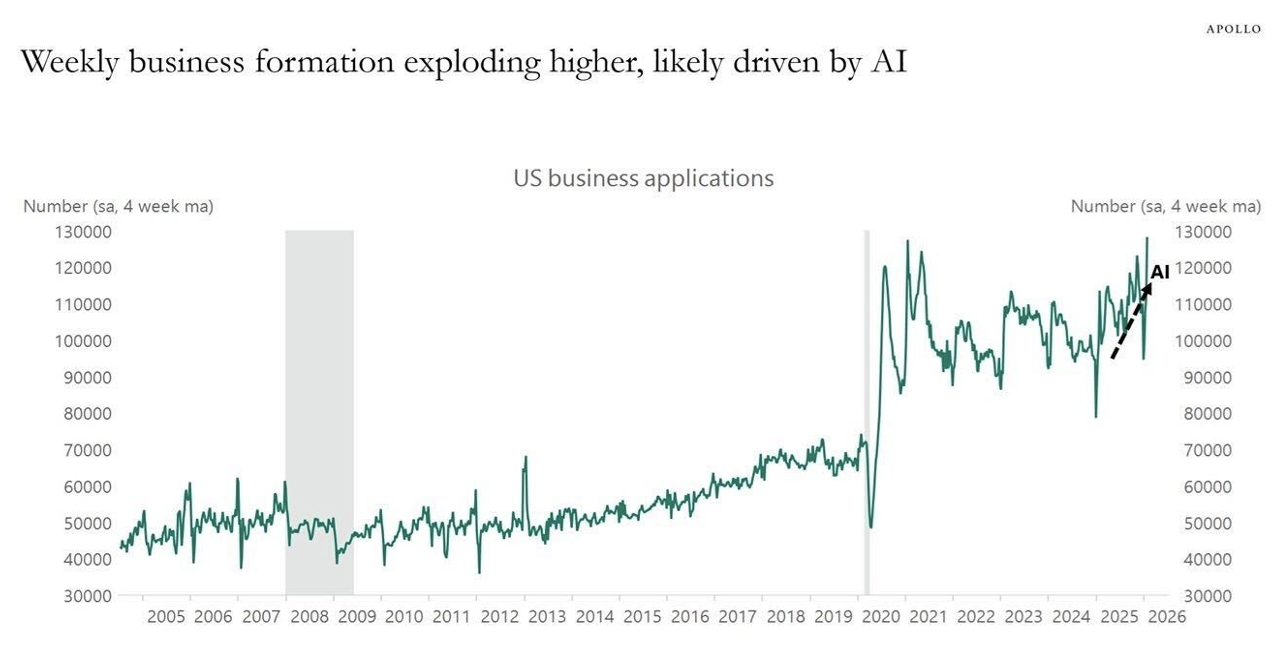

John Luke: Despite the fears, economic growth remains strong, supported by a massive surge in new business formations. AI tools are allowing much smaller teams to operate with the scale of much larger companies, making it easier and faster to launch new ventures than ever before.

Source: Apollo as of 03.07.2026

Source: Apollo as of 03.07.2026

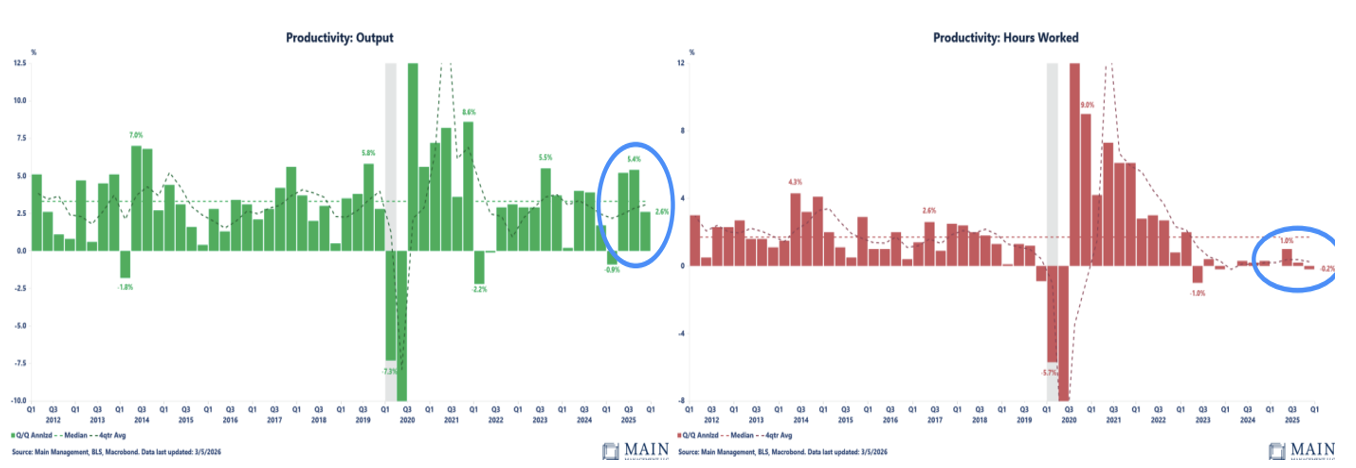

Jake: We are seeing these “efficiency gains” in real-time across the economy. Quarterly output rose 2.6% even as hours worked declined by 0.2%, the first such decline since 2023. This may suggest AI adoption is already boosting productivity.

.

Source: Main as of 03.06.2026

Source: Main as of 03.06.2026

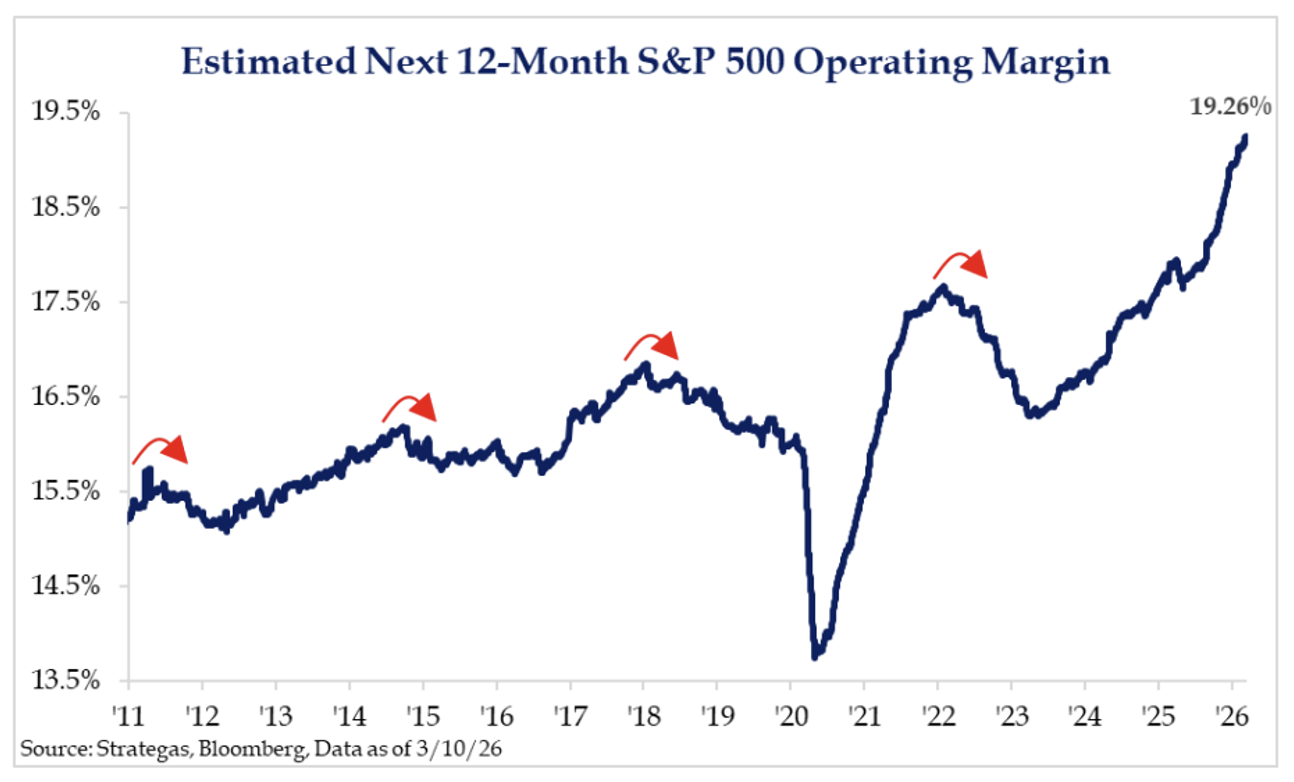

Brad: This may also be feeding into operating earnings. S&P 500 operating margins have climbed to 19%+, suggesting that productivity is overwhelmingly rising costs for big business.

Source: Strategas as of 03.10.2026

Source: Strategas as of 03.10.2026

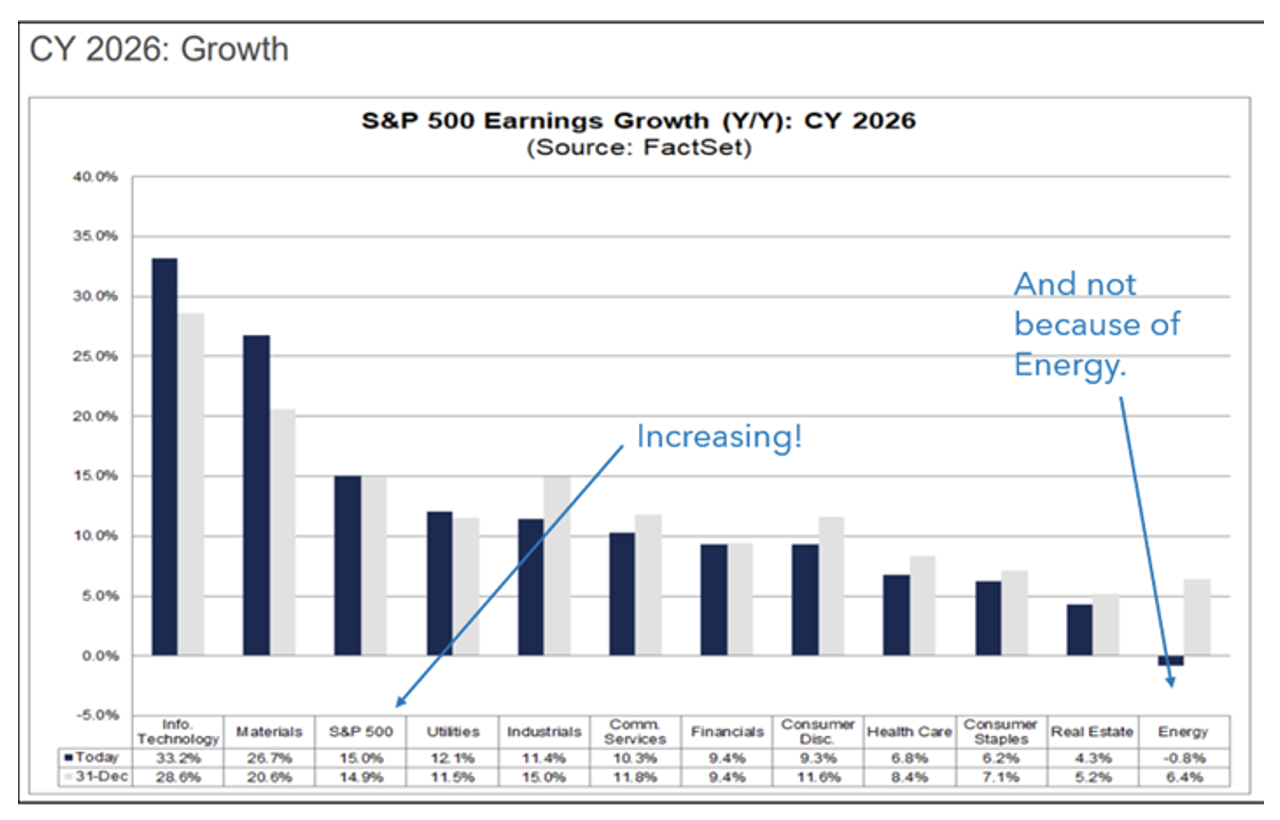

Brett: It’s not just margins widening. Earnings are forecast to grow materially over the next 12 months, and that has been priced in with an earnings reduction in energy, which may become less of a drag given higher oil prices.

Source: Factset as of 03.10.2026

Source: Factset as of 03.10.2026

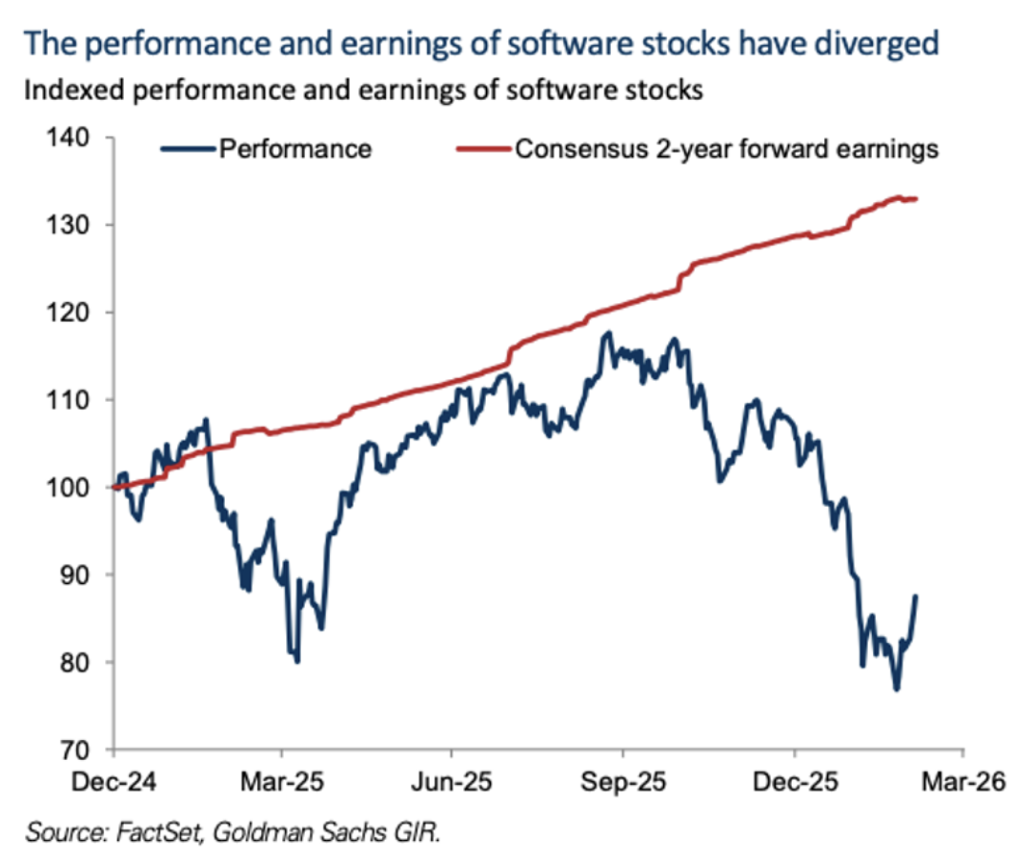

JG: One area where we’ve seen the negative impact of AI on sentiment, but not fundamentals, is the software sector. While stock performance has struggled, actual earnings growth remains in the double digits with profit margins that are nearly twice the rest of the market.

Graphic as of 03.09.2026

Graphic as of 03.09.2026

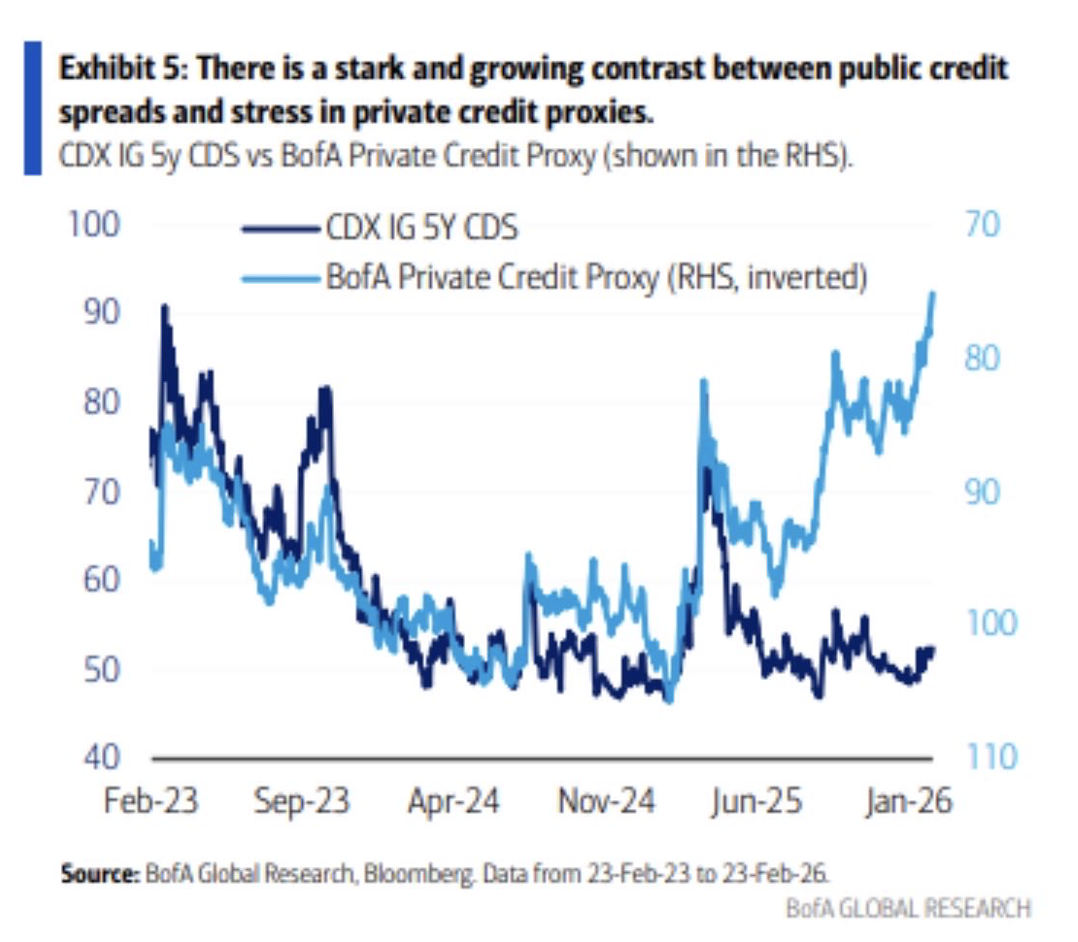

Brian: An asset class becoming more interesting is credit, specifically the increased concern within private credit. There is a stark contrast between public credit spreads and the stress seen in private credit. Will investors sell public credit to de-risk when they find they cannot exit their private positions?

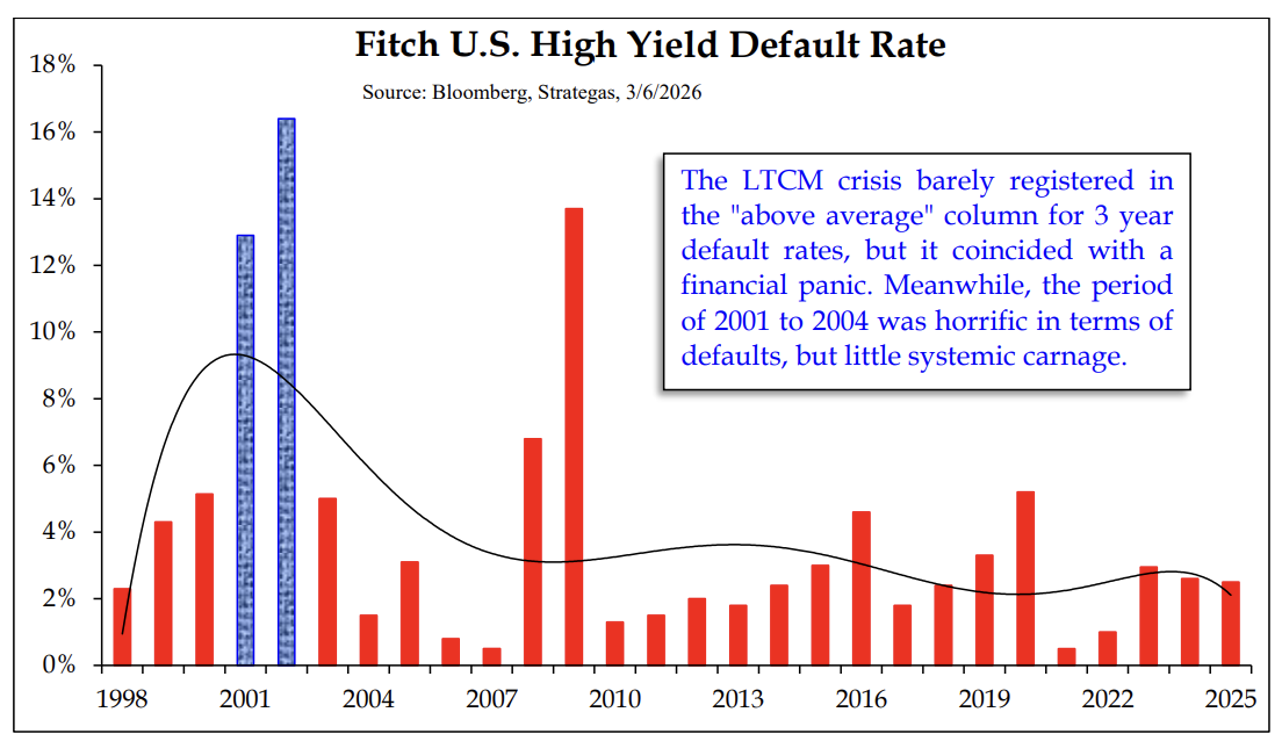

Joseph: High-yield default concerns are often overlooked because they’ve been so rare since the 2008 crisis.

Source: Strategas as of 03.06.2026

Source: Strategas as of 03.06.2026

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2603-14.