Our team looks at a lot of research throughout the day. Here are a handful of charts we think are good summations of investor activity, from the anatomy of market pullbacks and shifting geopolitical risks to the energy demands of the AI revolution and the resilience of the U.S. consumer. Have a great weekend with the return of baseball and more March Madness!

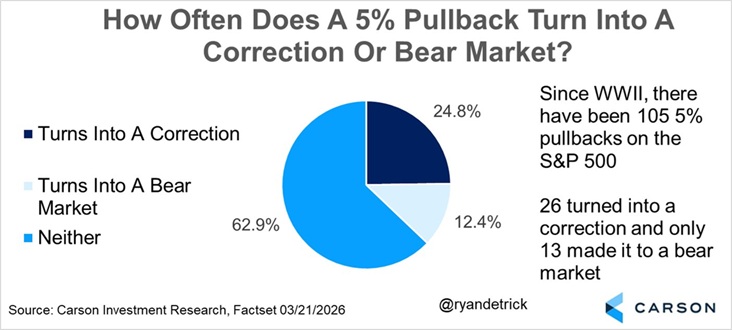

John Luke: We’ve finally added another 5% pullback to the long list of those that have come and gone before. Historically, only about 12% of these minor dips turn into a full-blown bear market, with the vast majority serving as a healthy reset within a larger trend.

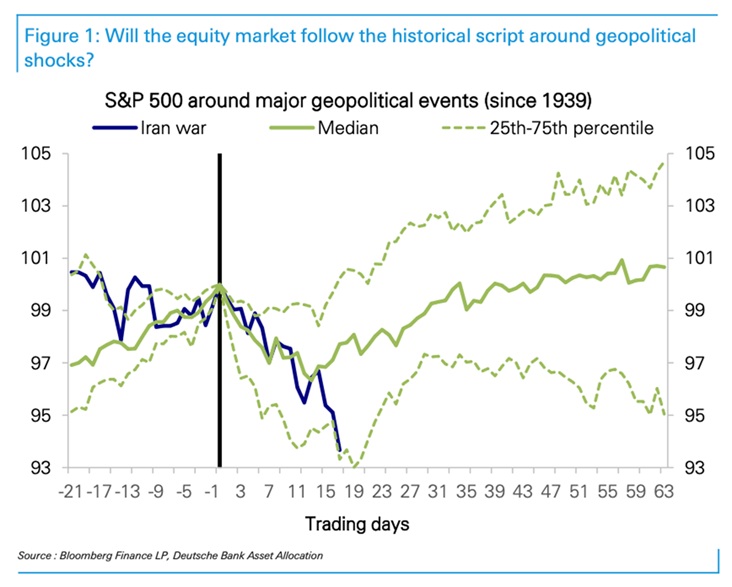

Brad: The historical playbook for these types of sell-offs usually involves a 6% to 8% decline that bottoms within three weeks. We are currently right in the vicinity of that typical bottom in both size and timing, often recovering long before the underlying headlines are resolved.

Data as of 3.23.26

Data as of 3.23.26

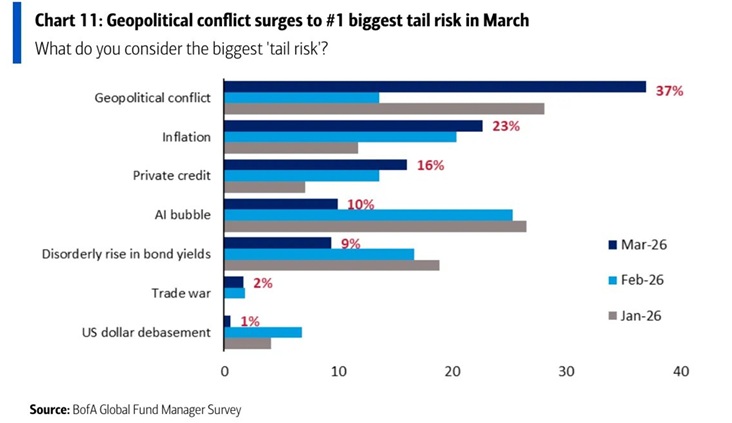

Bennett: Investors are concerned and geopolitical risk has moved fast, officially surpassing “AI bubble fears” as the biggest tail risk currently cited by investors.

Data as of 3.23.26

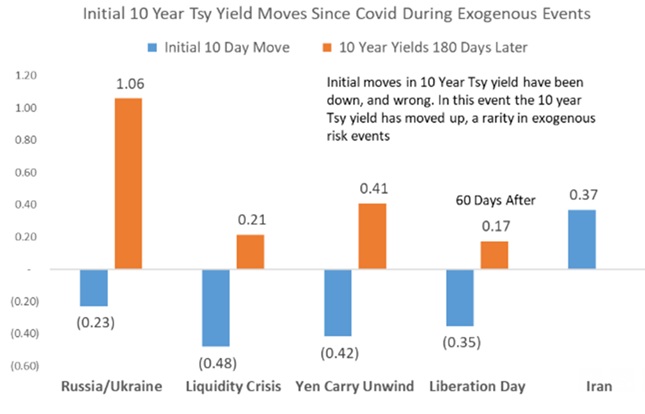

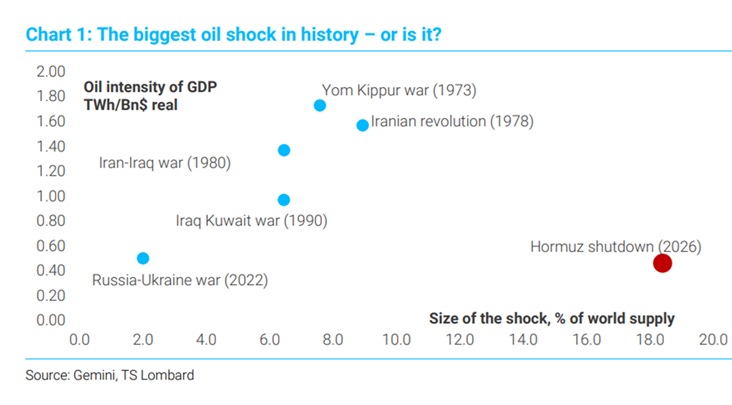

Dave: It hasn’t only been stocks that have been challenged, but the bond market’s initial reaction to the Hormuz headlines may not stick. During the last four major exogenous events, the 10-year Treasury’s first move was 180 degrees wrong. If oil continues to climb, central banks may pivot quickly from inflation talk to discussing economic growth risks.

Source: Raymond James as of 3.20.26

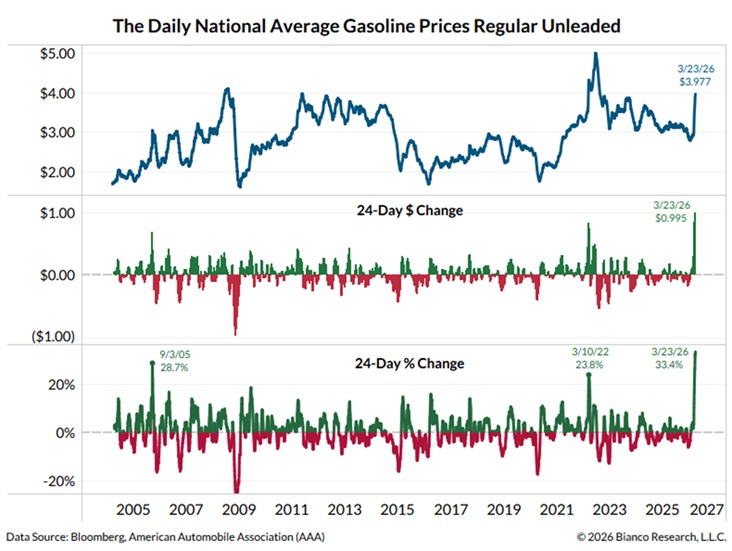

Derek: The impact of the war has started to hit the pump. After a long move lower, gas prices just saw a historic 3-week jump of more than 30%, raising questions about the trajectory of future rate economic growth.

Data as of 3.23.26

Jake: The 1990 recession is a potential template for this energy spike. Back then, higher inflation handcuffed the Fed’s ability to respond to weakness, putting them behind the curve. They will likely watch for similar non-linear risks today, particularly with labor demand already soft.

Data as of 3.24.26

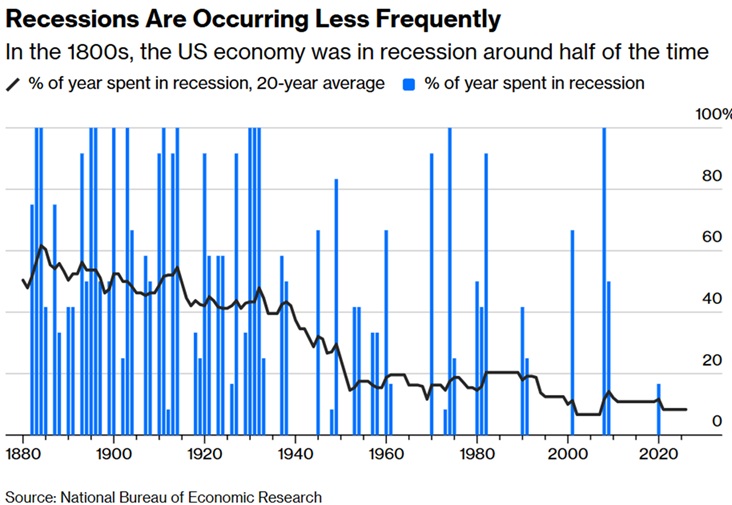

Beckham: Despite the tension, the U.S. economy does continue to look resilient. Over the last 20 years, we have spent very little time in recessions compared to the early 20th century.

Data as of 3.23.26

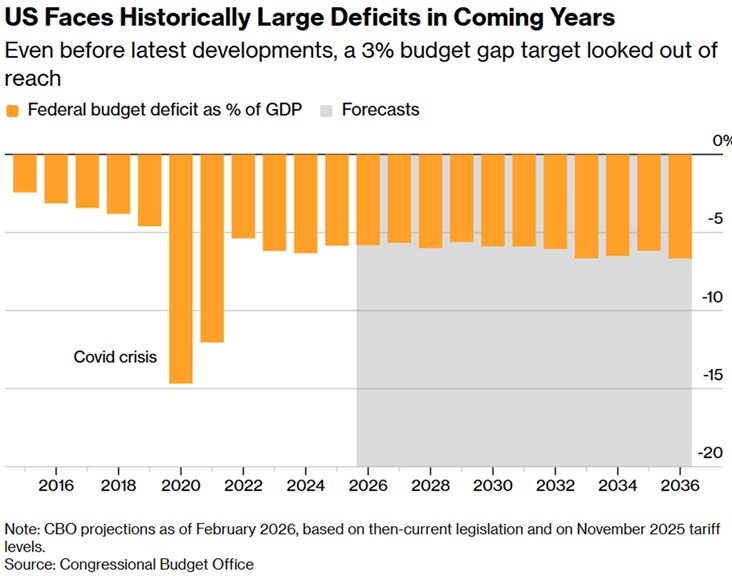

John Luke: Getting the fiscal deficit below 4% of GDP, Bessent’s “something with a 3 in front of it” goal, looks increasingly difficult. While the administration points to annual appropriations as a buffer for conflict funding, the CBO is still penciling in 6% deficits for the coming decade.

Data as of 2.28.26

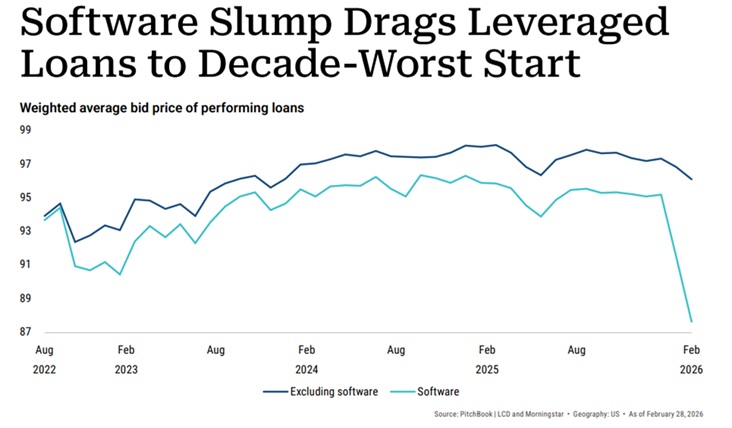

Joseph: Private credit continues to be a front and center concern for investors, but there are some concerns in credit within public markets as well. While performing loans outside of software declined modestly in February, the software sector has dropped over 7.5% since year-end. This specific pocket of stress is far outstripping the rest of the market.

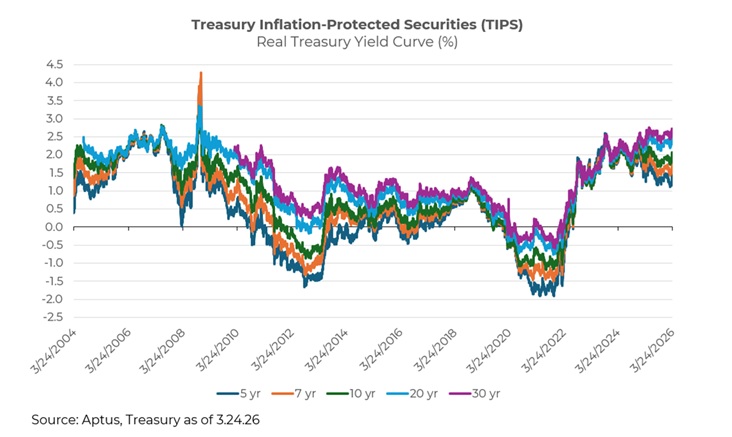

Brian: For those looking for some additional sources of return within fixed income, TIPS are now offering real yields (yield after inflation) quickly approaching 20-year highs.

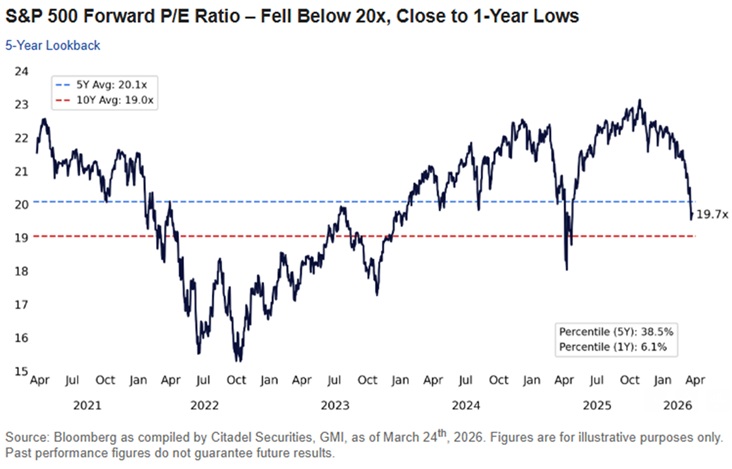

Ten: Given the recent volatility and continued strong forecasts for earnings, valuations have reset significantly. The S&P 500 Forward P/E is now trading back below 20x, near one-year lows and below its 5-year average.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2603-24.