Our research team parses a vast amount of institutional data and market research daily to isolate the key signals that matter. This week’s selection highlights a structural regime change in inflation, a fundamentally anchored equity rally, and the unprecedented scale of the ongoing capital investment cycle into artificial intelligence. Have a great long weekend!

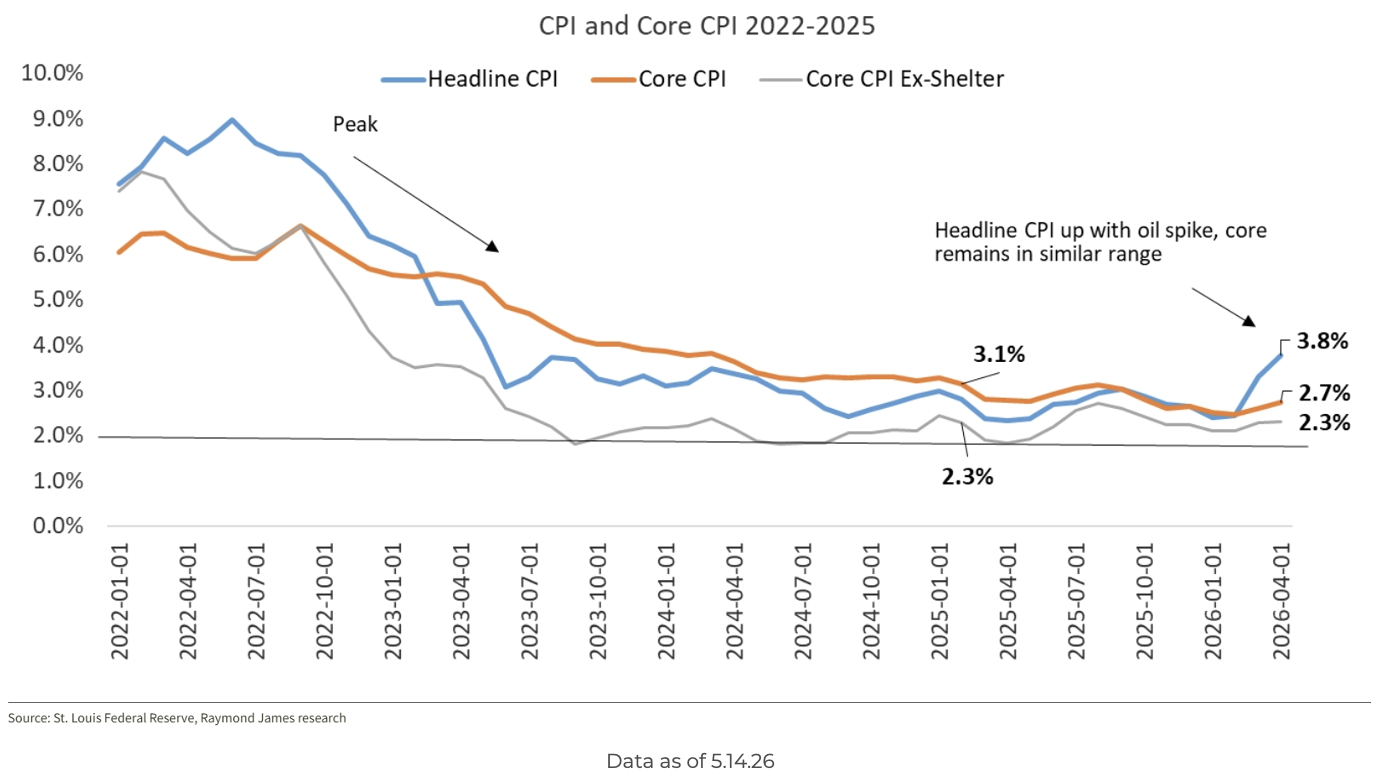

Dave: Headline CPI continues to break out, reaching its highest level since early 2023. This pressure is being driven almost entirely by the recent spike in crude oil prices. In contrast, Core CPI remains tightly contained, illustrating a distinct divergence between headline commodity shocks and sticky consumer demand.

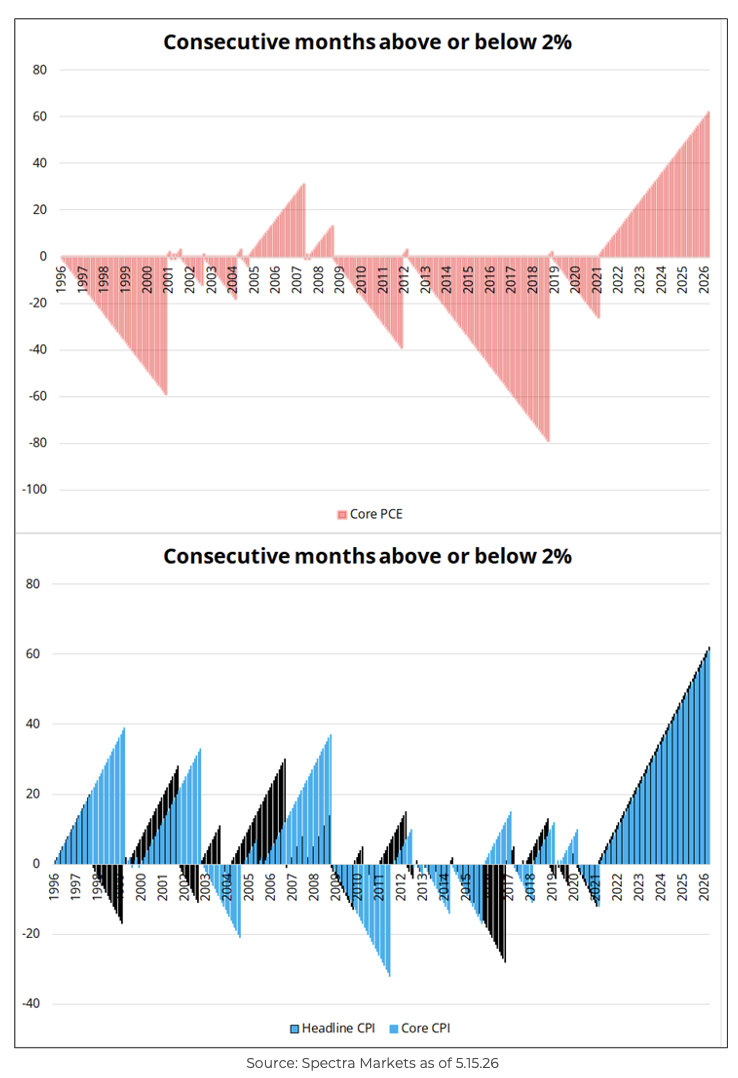

John Luke: Inflation has now spent 60 consecutive months holding above the Federal Reserve’s target. This marks the longest persistent overshoot in over three decades and stands in stark contrast to the post-Global Financial Crisis era, where long periods of disinflation below the 2% floor were the norm.

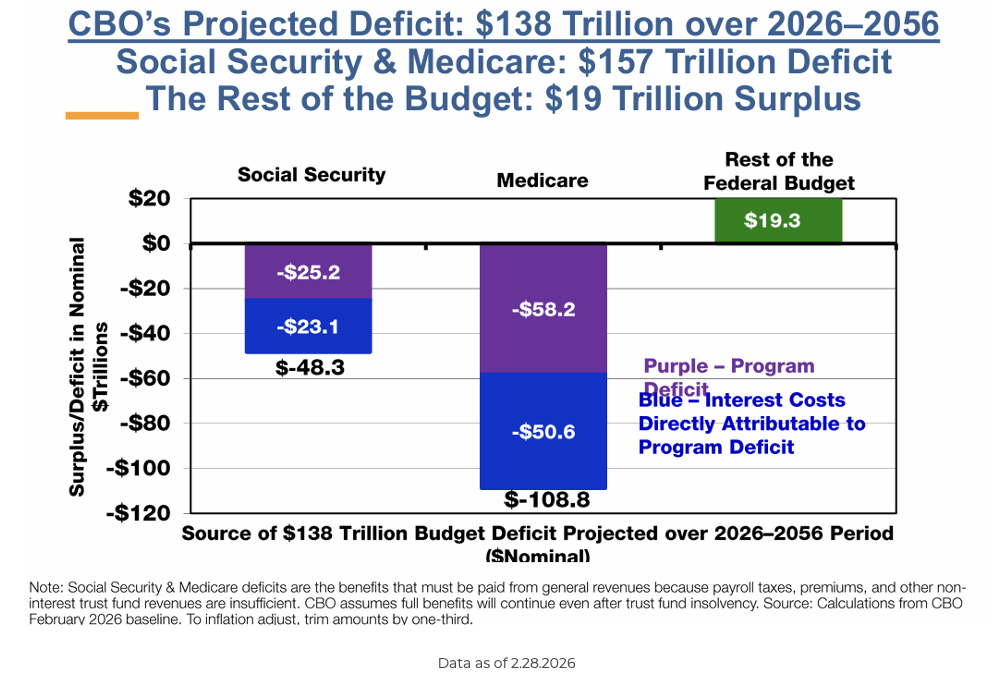

Beckham: When diagnosing long-term deficit projections, the math is heavily concentrated. According to the Congressional Budget Office’s 30-year projections, mandatory outlays for Social Security and Medicare account for the entire structural deficit shortfall. Stripping those two items out, the remainder of the federal budget actually runs a cumulative surplus.

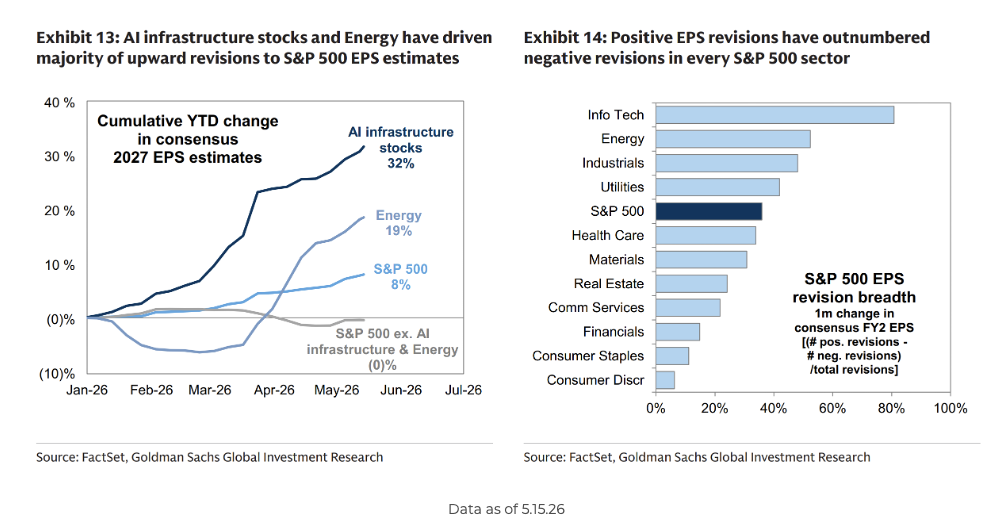

Mark: Unlike the speculative market melt-ups of the late 1990s or 2021, the current equity rally is heavily anchored in fundamental reality. Bottom-up consensus EPS estimates for the S&P 500 in 2026 and 2027 have steadily marched 8% higher year-to-date, providing objective fundamental support for higher equity valuations.

Brad: Corporate execution in the United States continues to demonstrate a clear global advantage. Near-term EPS growth expectations for the S&P 500 significantly outpace international developed markets, extending a multi-year performance edge over the MSCI EAFE index.

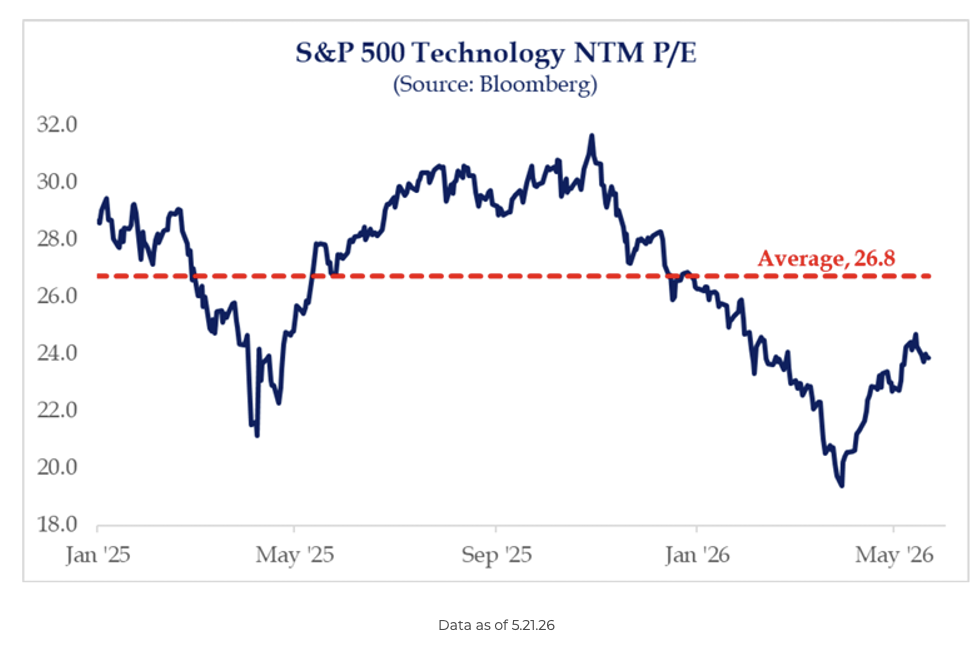

Joseph: A remarkable feature of today’s market is that while Technology remains the clear focal point for investors, aggregate tech sector multiples have seen very little expansion from their recent lows. Earnings growth is doing the heavy lifting, supported by multiple compressions in software acting as an internal counterweight. If this were a bubble reminiscent of the late 1990s, we would see a non-discretionary melt-up across every sub-industry.

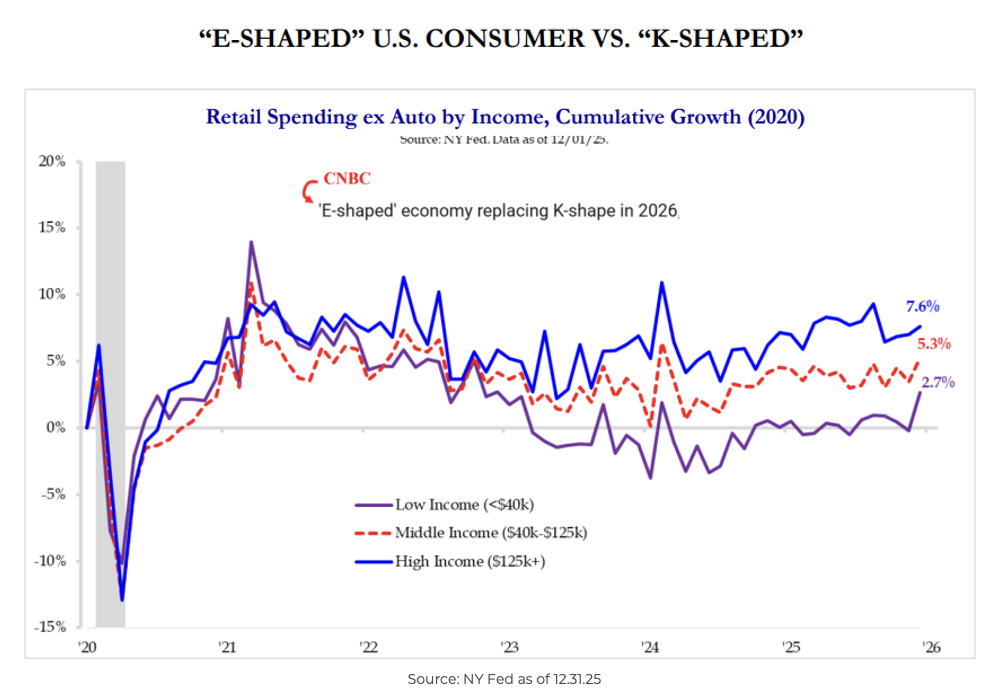

Jake: The traditional post-pandemic “K-shaped” consumer recovery is morphing into an “E-shaped” spending pattern. Real retail spending data reflects a clear divergence where middle-income and higher-income growth remains robust, while lower-income consumer footprints face ongoing pressures.

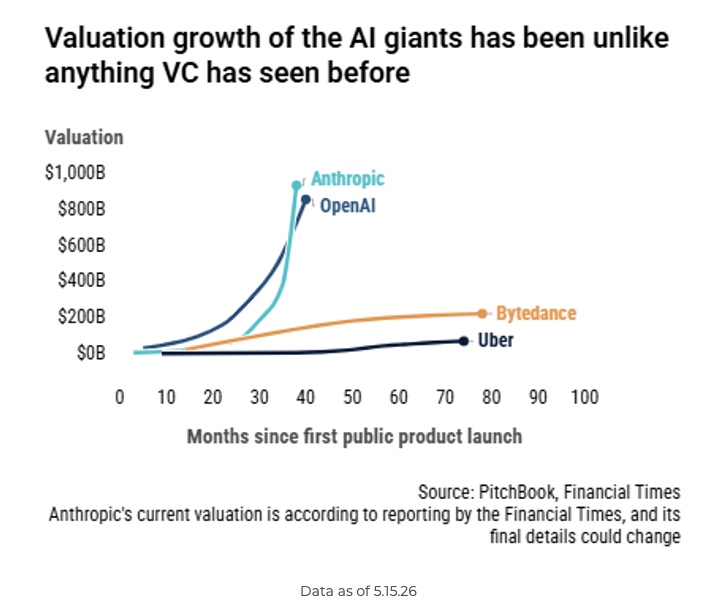

Joseph: The velocity of value creation within the generative AI ecosystem is entirely unprecedented in the history of venture capital. Valuations for industry frontrunners Anthropic and OpenAI are already rapidly closing in on the $1 trillion mark, less than three years since their first public product rollouts.

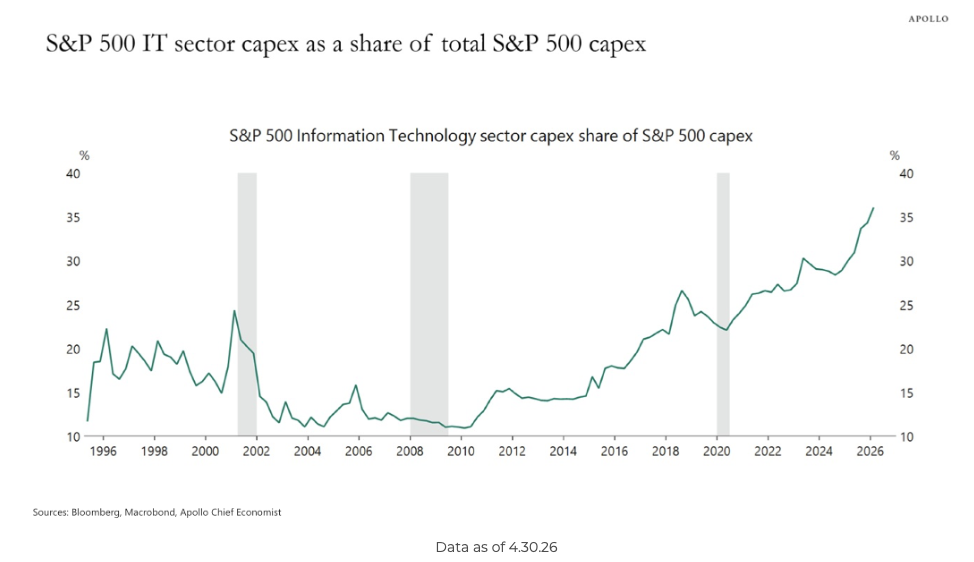

JD: To support this explosive technological footprint, hyperscalers and tech firms are deploying capital aggressively. Capital expenditure within the S&P 500 Information Technology sector has reached its highest share of total index capex in historical data.

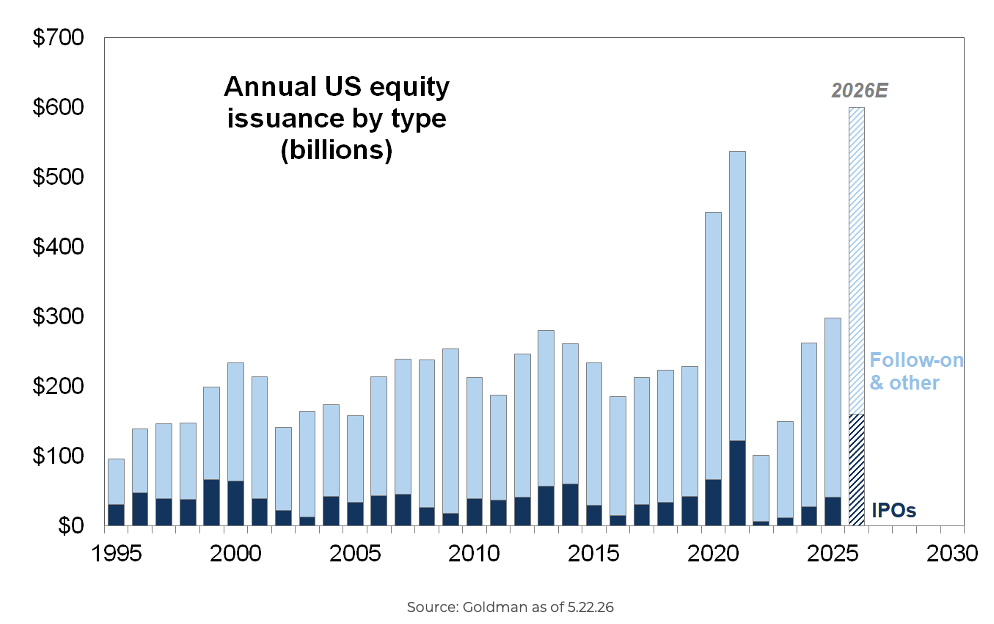

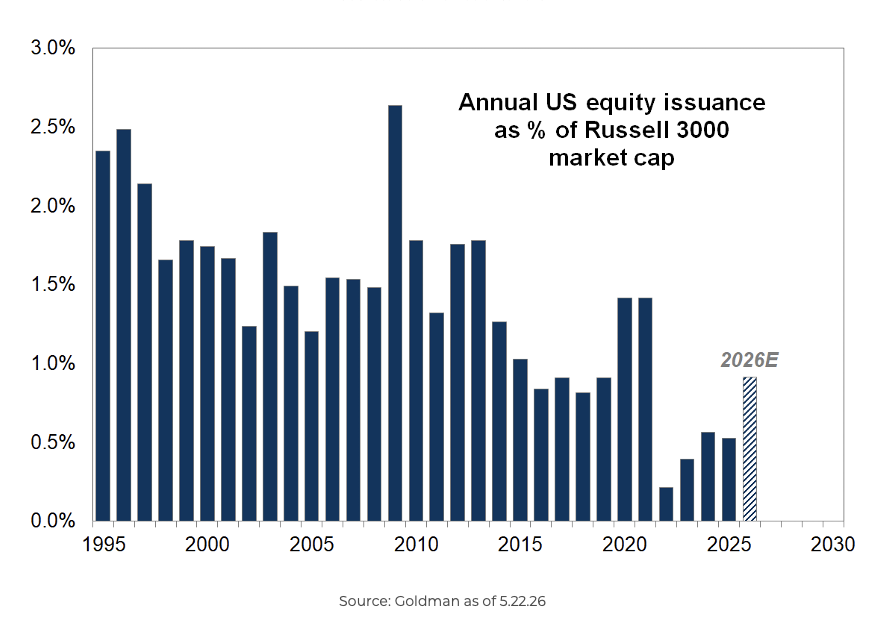

James: Looking at the absolute dollar volume of annual U.S. equity issuance, fueled by standard IPOs and follow-on offerings, the numbers appear eye-watering.

However, before this raw dollar surge sparks concern, converting that total issuance into a percentage of total Russell 3000 market capitalization tells a very different story. Compared to the extreme capital-raising environments of the late 1990s tech bubble, the 2009 banking recaps, or the 2021 SPAC frenzy, today’s volume is highly manageable. The market possesses ample depth to absorb these high-quality assets.

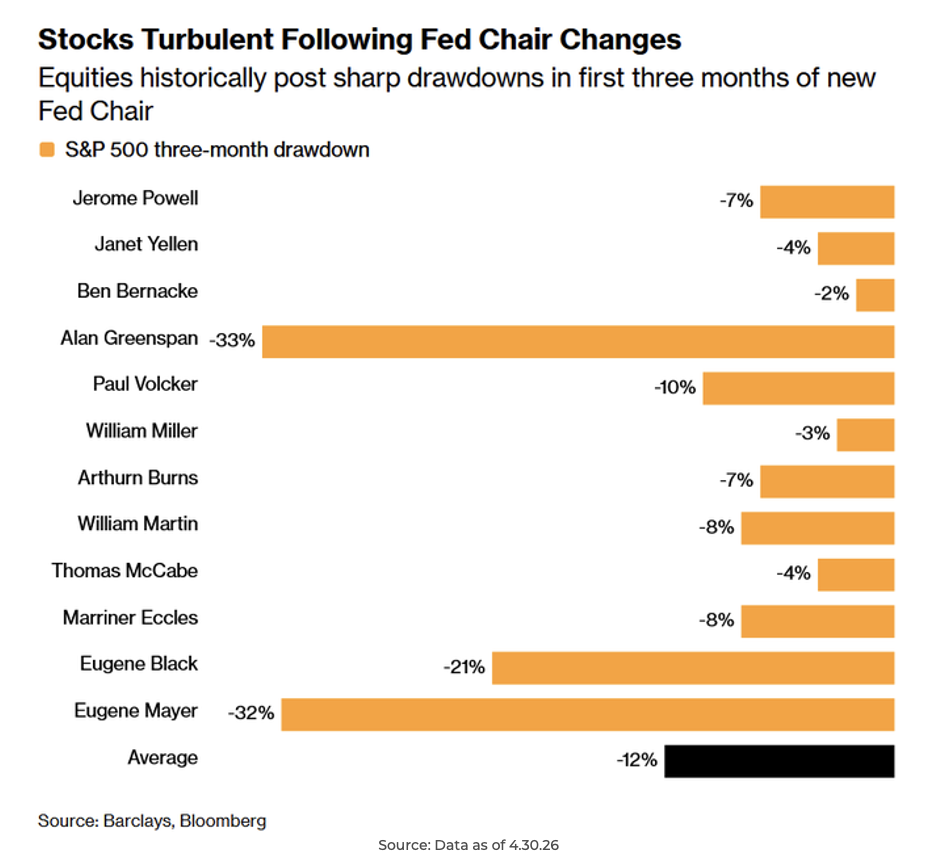

Ten: Investors should anticipate some near-term noise following changes at the Federal Reserve. Historical data indicates that the S&P 500 has typically experienced heightened volatility and sharp drawdowns during the first three months of a new Fed Chair’s tenure.

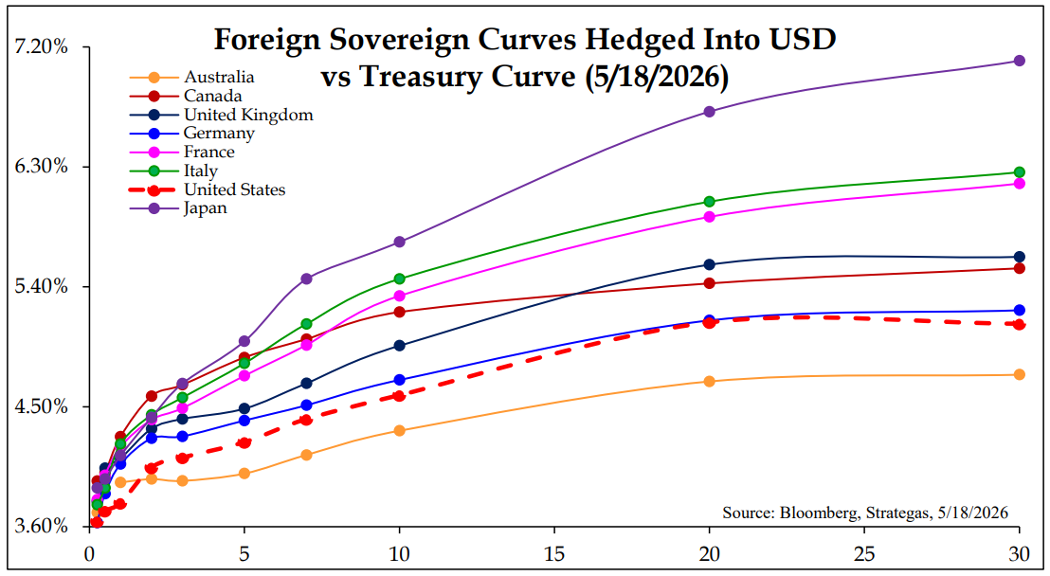

Brian: Income-focused investors are seeing a dramatic shift in global fixed-income opportunities. The United States is no longer the only developed game in town when it comes to nominal yield, as foreign sovereign yield curves hedged back into USD now offer highly competitive alternatives.

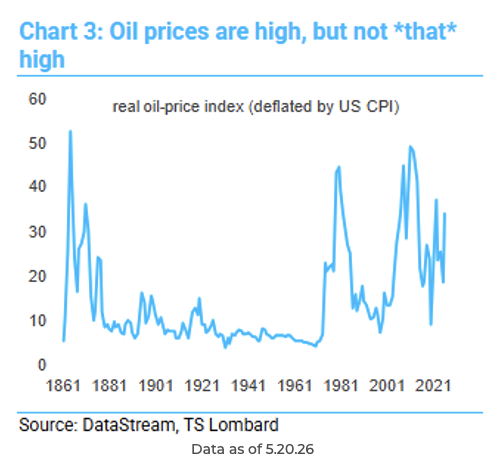

Brett: While the current energy spike dominates headlines, a look at real, inflation-adjusted oil prices over the last 170 years provides some long-term perspective. When deflated by headline CPI, long-term historical data shows that today’s energy prices are high, but not near historical parameters compared to the severe commodity shocks of decades past.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2605-19.