Our team parses a vast amount of research daily to identify the signals that truly matter. This week’s selection highlights a stellar start to the earnings season, the deepening impact of the AI investment cycle, and the ongoing debate between Fed policy and market reality.

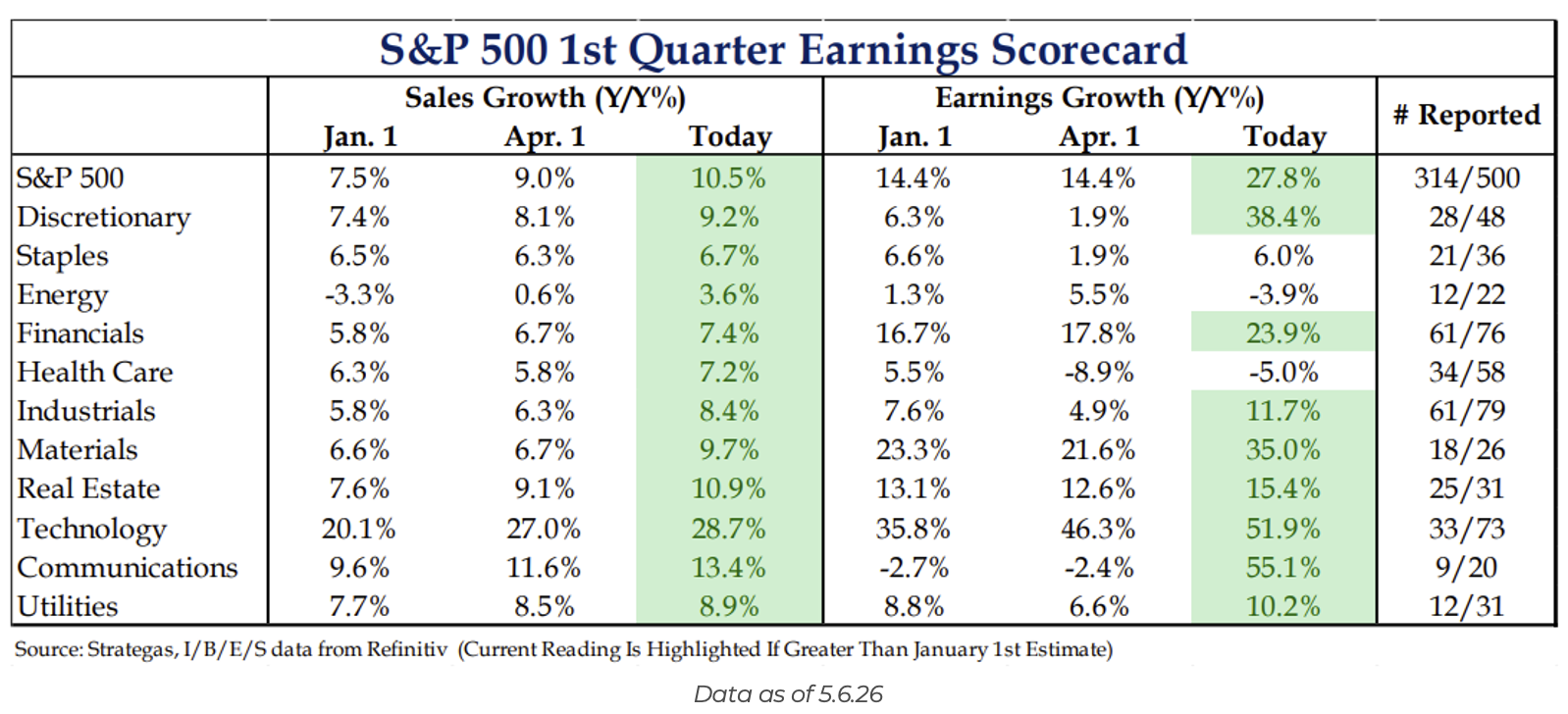

Brad: The equity rally has been all about earnings, and the first-quarter earnings scorecard has been impressive, with revenue growth particularly strong across every single sector. While defensive areas initially lagged, they have improved significantly since April.

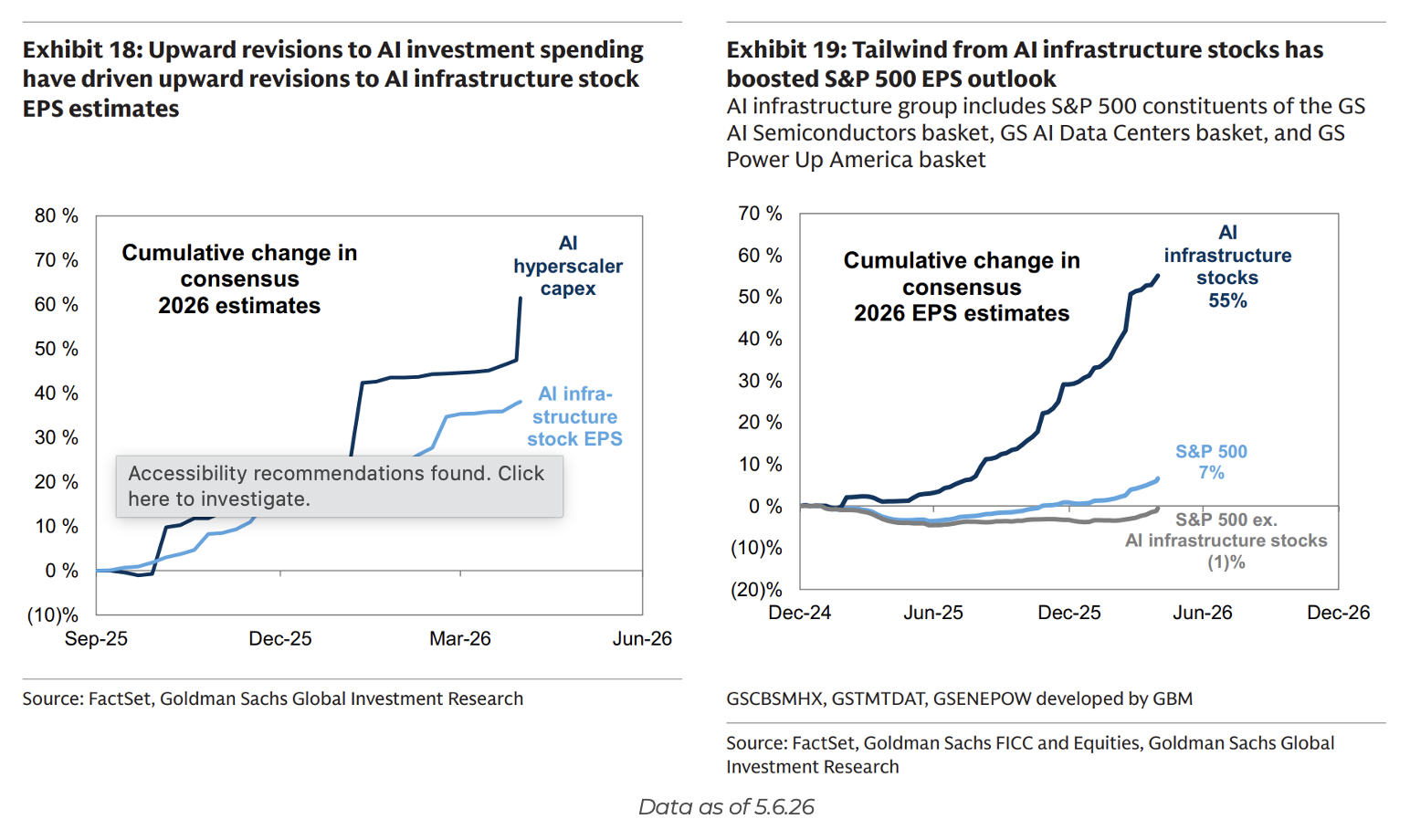

Mark: The AI investment boom is creating significant upside potential to S&P 500 profit forecasts. Infrastructure stocks are currently estimated to drive roughly 40% of index earnings growth this year. While macro headwinds exist, the “AI impulse” appears even stronger today than it did just a few weeks ago.

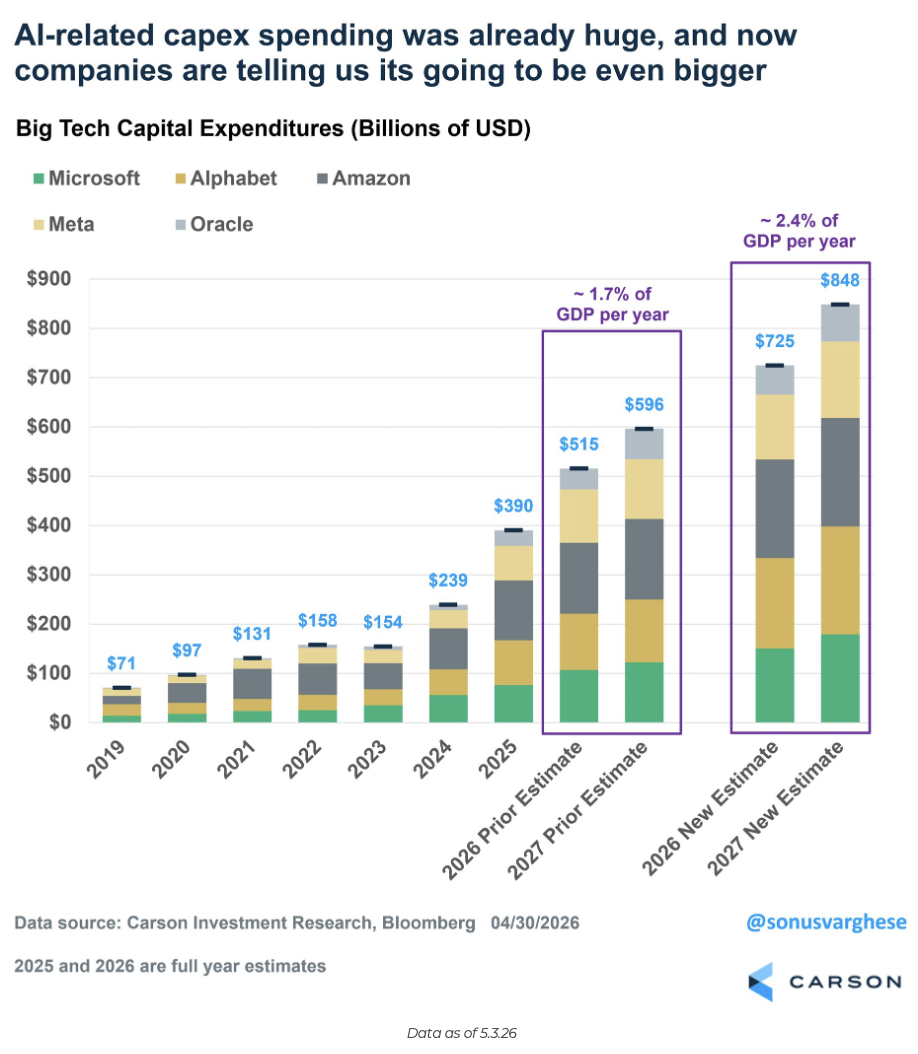

Beckham: We’ve reached a tipping point where AI CAPEX isn’t just driving the market, it increasingly is the market. Big Tech capital expenditures are now projected to reach roughly 2.4% of US GDP per year by 2027, a massive structural shift in how capital is deployed.

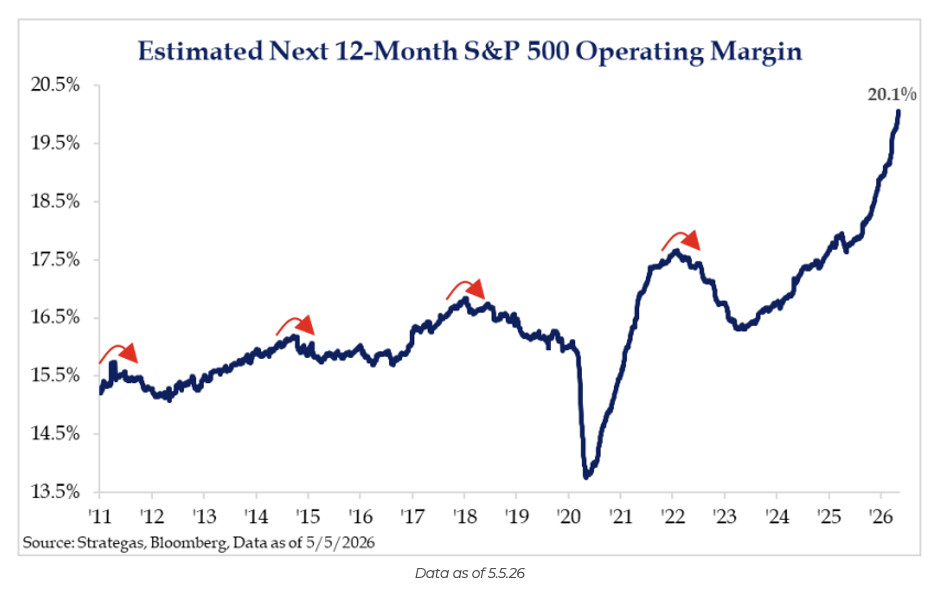

Ten: Operating margins for the S&P 500 have now climbed above 20%, providing a material cushion for the broader market. It’s historically difficult to be bearish during periods of margin expansion, especially as hyperscalers continue to contribute outsized strength to the bottom line.

John Luke: S&P 500 earnings forecasts for 2026 and 2027 continue to buck historical trends by ramping higher rather than following the typical pattern of downward revisions.

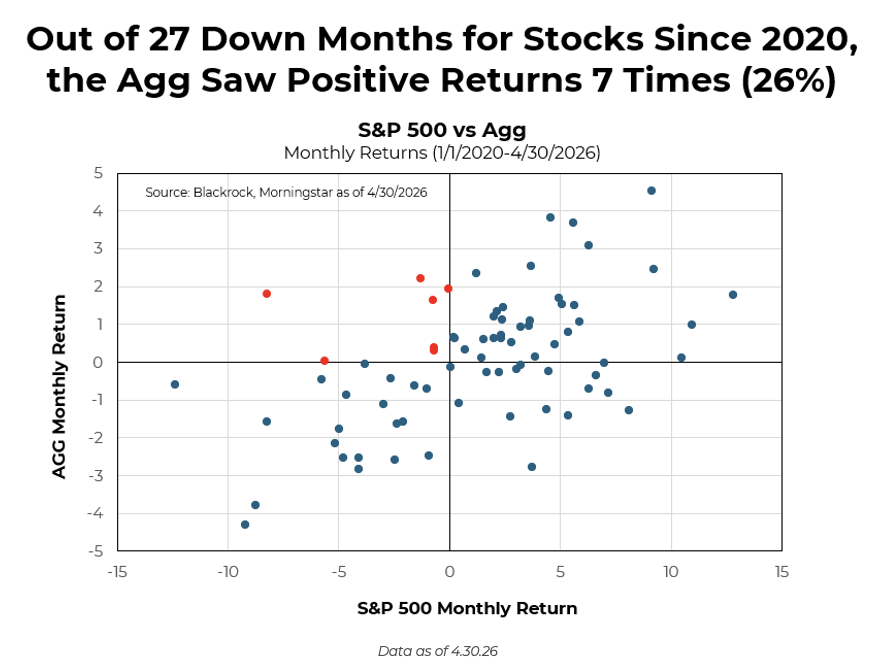

Jake: It is time to rethink the “bond as a diversifier” narrative. Since 2020, during the 27 months when stocks were down, the Bloomberg Aggregate Bond Index provided a positive return only 26% of the time. This lack of protection makes alternative hedging tools more essential than ever.

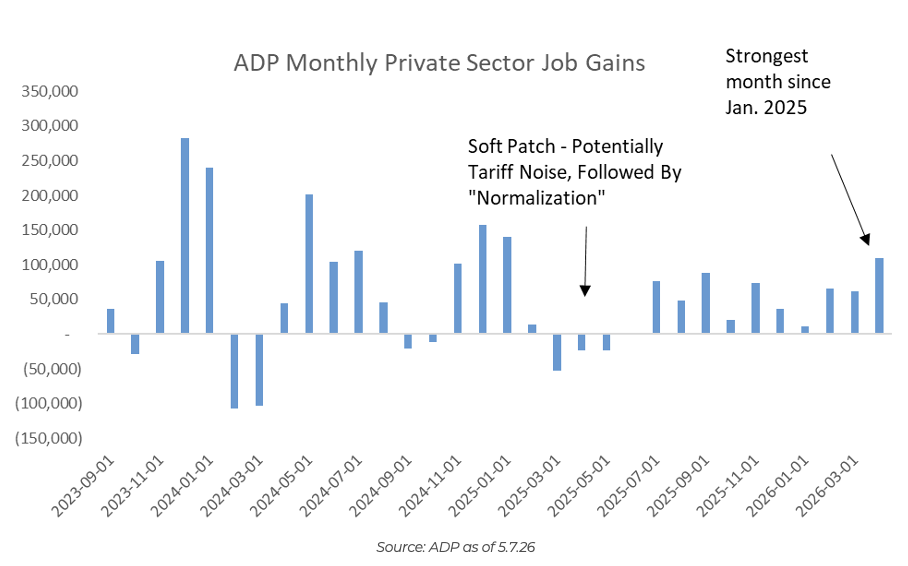

Joseph: The labor market is normalizing healthily. April’s ADP private sector payrolls hit 109,000, the strongest month since early 2025. With the impact of previous federal workforce cuts now largely through the system, we expect total job gains to align more closely with these improved private-sector additions

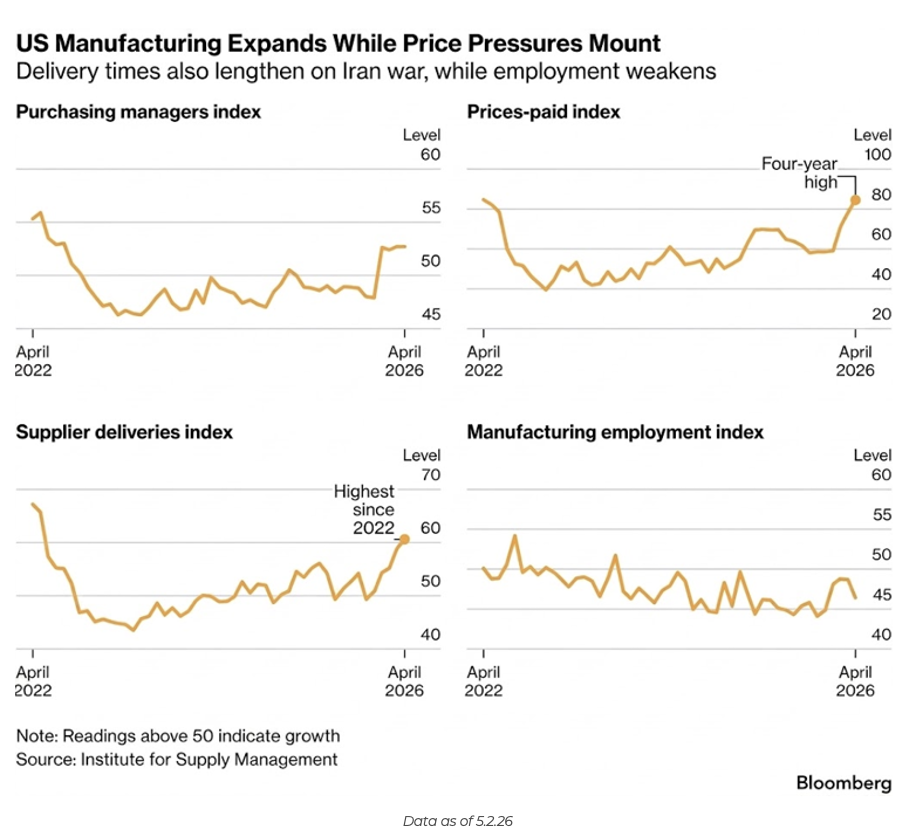

JD: Manufacturing continues its breakout, showing expansion even as delivery times lengthen due to geopolitical noise. While price pressures remain a factor to watch, the sector’s growth trajectory is clear.

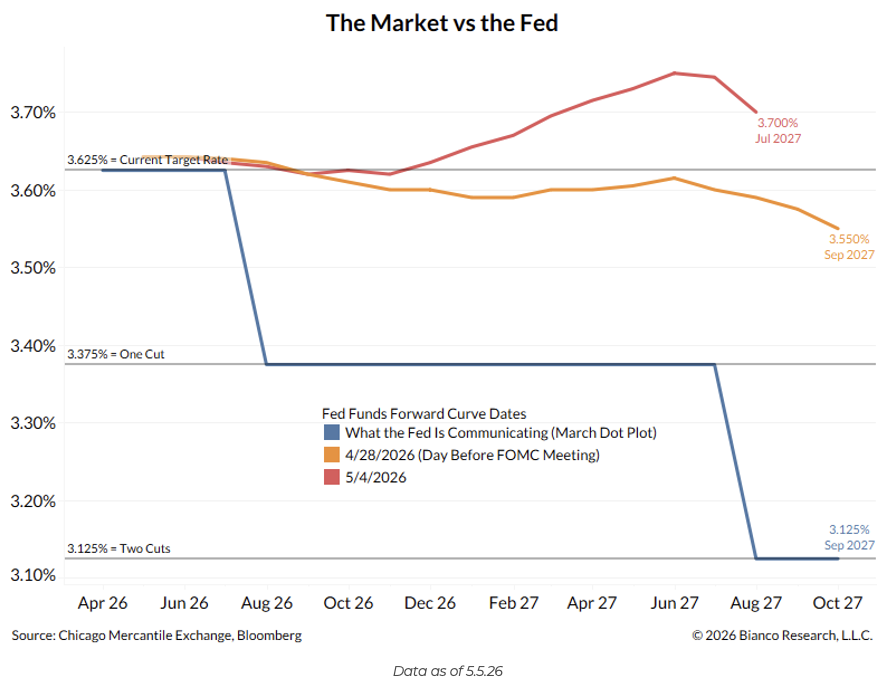

Dave: A major disconnect persists between the Fed’s communication and market expectations. History often suggests the market is the better predictor of the two, and the current forward curve implies a path that diverges significantly from the Fed’s recent “Dot Plot”.

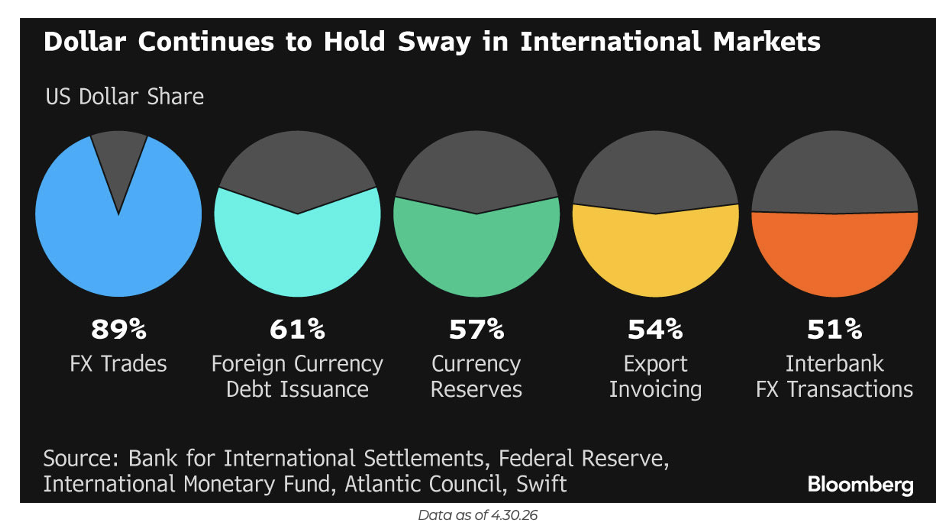

Brett: The US dollar continues to exert absolute dominance in global finance, accounting for almost 90% of FX trades and the majority of interbank transactions. Despite frequent headlines about diversification, the greenback remains the undisputed anchor of international markets.

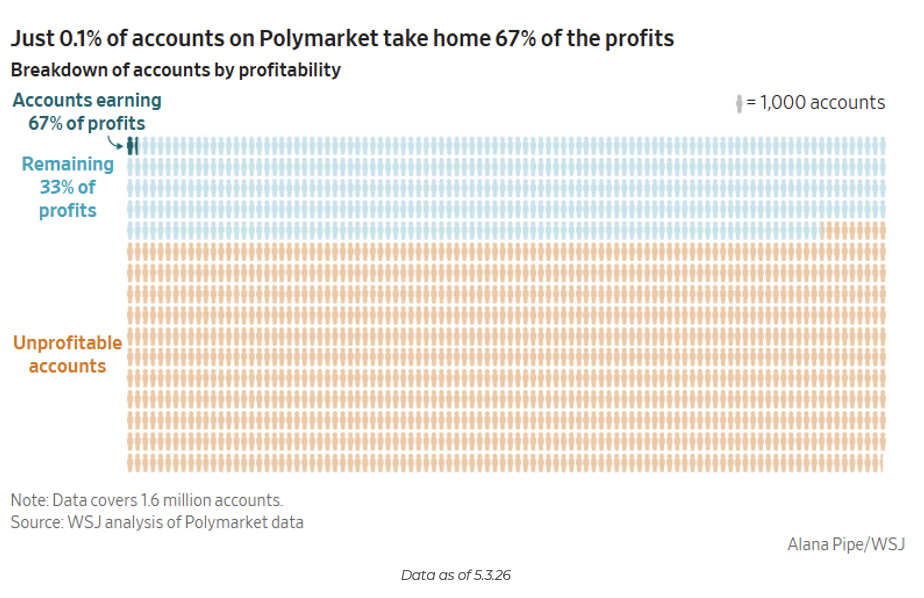

Brian: While prediction markets like Polymarket are gaining popularity, they are often more entertainment than true investing. Data shows that just 0.1% of accounts capture two-thirds of the profits, proving that for most, the “vig” makes this a losing game compared to traditional asset ownership.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward-looking statements cannot be guaranteed.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2605-10.