Technology is deflationary. While we have views you could argue with, this isn’t one of them.

For example, the flat-screen TV you bought for $3,000 twenty years ago now costs $300 at Walmart.

If left to their own devices, competitive markets lead to more productivity gains. It’s kind of the entire point of economic progress. If you are in business and you aren’t passing productivity gains to consumers through higher quality or lower prices, you won’t be in business long. Competition leads to productivity gains, which should lead to deflationary forces, and this isn’t optional for those competing.

This type of deflationary force, which is a product of productivity gain, is a good thing. It leads to your dollar buying MORE. It leads to your dollar’s purchasing power improving.

Every efficiency introduced brings either higher quality or lower prices. Your money buys you more, not less…theoretically.

The Real World

This is where I start to get confused. Theory doesn’t jive with what we feel. I have so many questions:

Why do we target 2% inflation?

Why does everything get more expensive over time?

Do we really have free markets?

This list of my questions goes on…

Money Supply Expansion

In our system, central banks continuously expand the money supply. This creation of money absorbs productivity gains and robs the consumer. While it’s not direct taxation, it might as well be. Productivity gains should be viewed as a dividend to consumers’ pockets, but they’re not. They get inflated away before they reach your pocket.

We don’t experience deflation—the good kind—because our system cannot afford it.

We are burdened with a massive debt-to-GDP ratio. Deflation makes tomorrow’s dollar worth more. Those two conditions are in direct conflict, and it’s much easier to pay back debt with dollars that are worth less.

This is why we have this hallucination that 2% inflation is a good thing. 2% inflation means your money loses half its value every 35 years. It’s why you are forced to work harder just to maintain a standard of living. Your household needs two incomes now… it ain’t 1960 out here.

The AI Problem

Maybe the AI hype is overblown. Or maybe it’s the most deflationary force we’ve ever dealt with.

If it’s the latter, how does a system that is dependent on inflation deal with that?

I have a longer answer to that question (I could type so much here, but I try to keep these monthly notes short and to the point), but the quick takeaway for investors is to think clearly about exposure to cash, or anything that could be defined as ‘fixed’.

My guess is that more money gets printed.

Bonds and Equities

Inflation and productivity gains both destroy wealth for bondholders. One erodes purchasing power, the other creates a wealth gap built on opportunity cost.

Equity investors have a fighting chance. They can better deal with the inflationary force of our money printing and benefit from productivity gains.

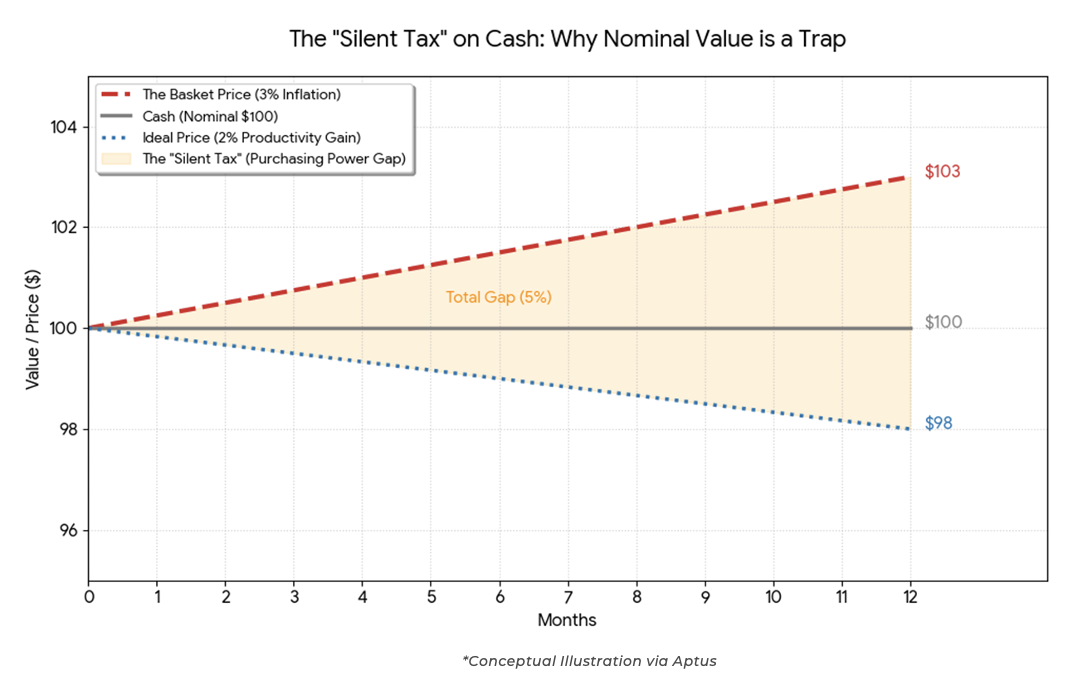

This chart is one that helps illustrate our point. If you have 2% gains in productivity and 3% inflation, the gap over a year is potentially 5%. Compound that out over a decade or so, and it will hurt more than just your feelings.

The Only Way

This is why the focus at Aptus is almost entirely around how we can create strategies and solutions to own more equities and less bonds in a risk-neutral way.

We’ve always argued the ‘safety’ of bonds isn’t safe, but we are entering a point in time where our conviction is in a bull market.

Technology is a deflationary force. Our system has been able to absorb those productivity gains through an expanding money supply, thus robbing us as consumers. Due to debt loads and the potential of AI, it seems things may be changing.

We continue to believe your asset allocation is critical to protecting and compounding your wealth. We will continue to build and work to improve the services and relationships we provide. We are thankful for your trust. I hope this note gets you thinking, and if you have any questions at all, please reach out.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

*Conceptual Illustration: Information presented in the above charts are for illustrative purposes only and should not be interpreted as actual performance of any investor’s account. As these are not actual results and completely assumed, they should not be relied upon for investment decisions. Actual results of individual investors will differ due to many factors, including individual investments and fees, client restrictions, and the timing of investments and cash flows.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2603-2.