Markets Have Changed

Discounting is the mathematical practice of estimating what a cash flow in the future is worth TODAY. Higher rates used in discounting lead to lower values today, while lower rates used in discounting lead to higher values today.

Given that securities (stocks, bonds, etc.) are claims on future cash flows, 2022 was a living math lesson as we watched rates rise and the value of claims on FUTURE cash flows drop across the board.

We’ve said before, it’s more than pure math that’s impacting the markets. It’s the mentality of investors that’s shifting across the board.

The definition of ‘discount rate’ should be thought of as the rate of return investors demand on their capital. For example, if I am willing to pay 15x expected cash flows and you are only willing to pay 10x, that’s the same as saying you demand a higher return on your capital than I do.

From the Global Financial Crisis up until the beginning of 2022, the environment was driven by the fear of missing out. There was little concern with losses, and more concern with missing out on the upside. Yields were nothing, so we were all forced into riskier assets and these actions were supported by an incredibly accommodative Fed, liquidity everywhere, and no inflation. In other words, the required return (discount rate) investors demanded was low, and it led to speculative activities and the illusion that FOMO was the primary concern.

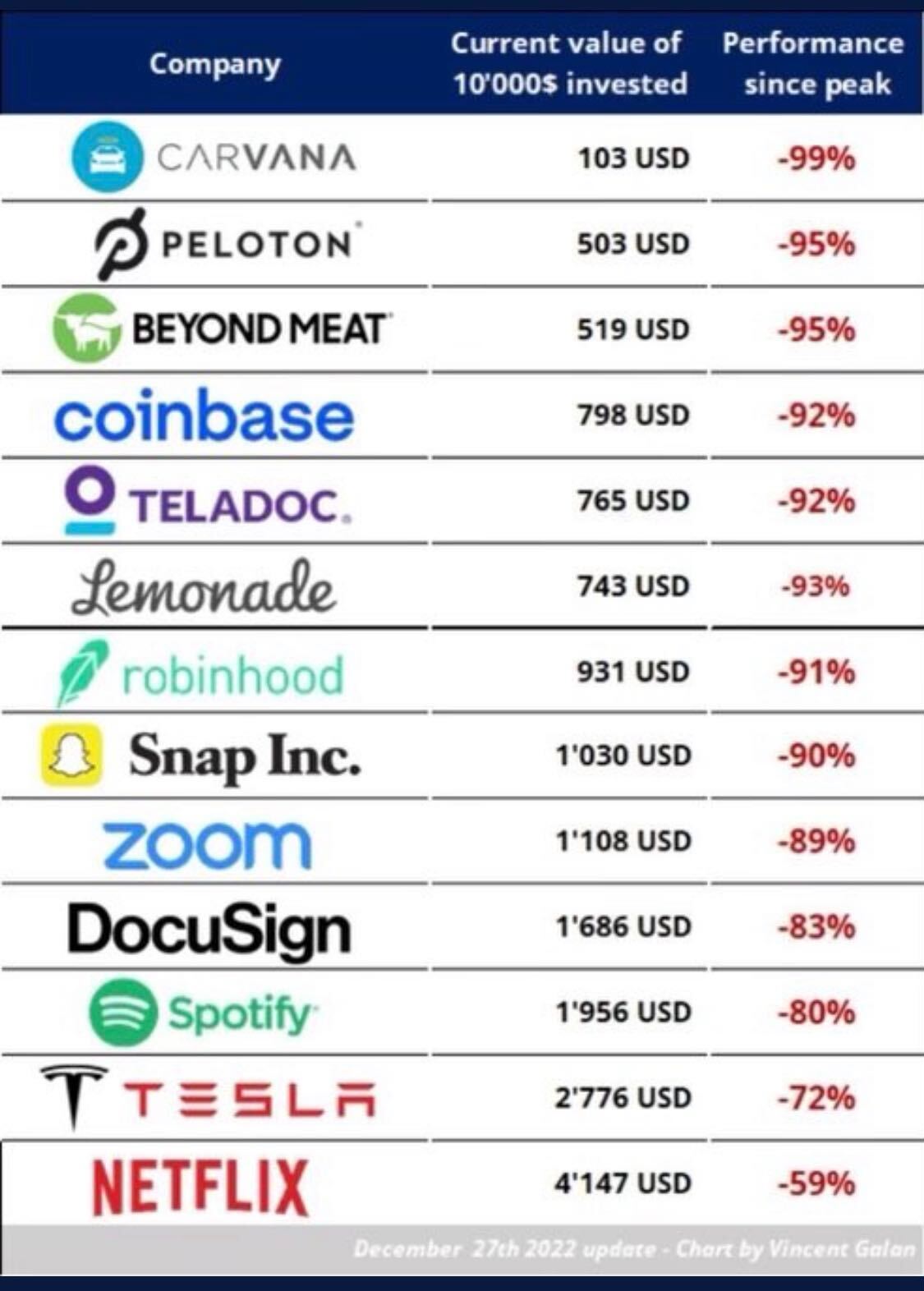

Then 2022 happened and hurt nearly every asset you can think of … some worse than others:

Source: Vincent Galan, as of 12.27.2022

Source: Vincent Galan, as of 12.27.2022

We’ll refrain from addressing the crypto space …

We believe the market environment today is far different from the one we had from 2009 to 2021. Inflationary pressure may last longer than we’d like, for several reasons. Globalization reversing course is a big one, as are the new normal rate environment and the Fed’s position in all of this.

The bottom line is that markets have changed, and investor mentality is a driver of that change.

Your Needs Have Not Changed

At Aptus, we work with advisors that cater to what we call the lifeblood of financial services. It’s the $500k to $3mm household that’s focused on maintaining or improving lifestyle while keeping longevity and behavior risks at bay. Sure, we work with larger families, but the overwhelming majority of our time is for the lifeblood.

Hurdle rates of return that keep a financial plan on track are not astronomical. This is great news. For most plans, if we can compound capital in the 6% to 12% range, all is well. That’s our objective…to position portfolios for returns that keep plans on track. We want to empower advisors to deliver consistently around the following three questions:

Am I going to be ok?

Can I maintain my family’s quality of life?

Can I improve it?

We are making portfolio shifts and creating new strategies to aid in our best effort to position based on the windshield and not the rearview.

Return Reminder

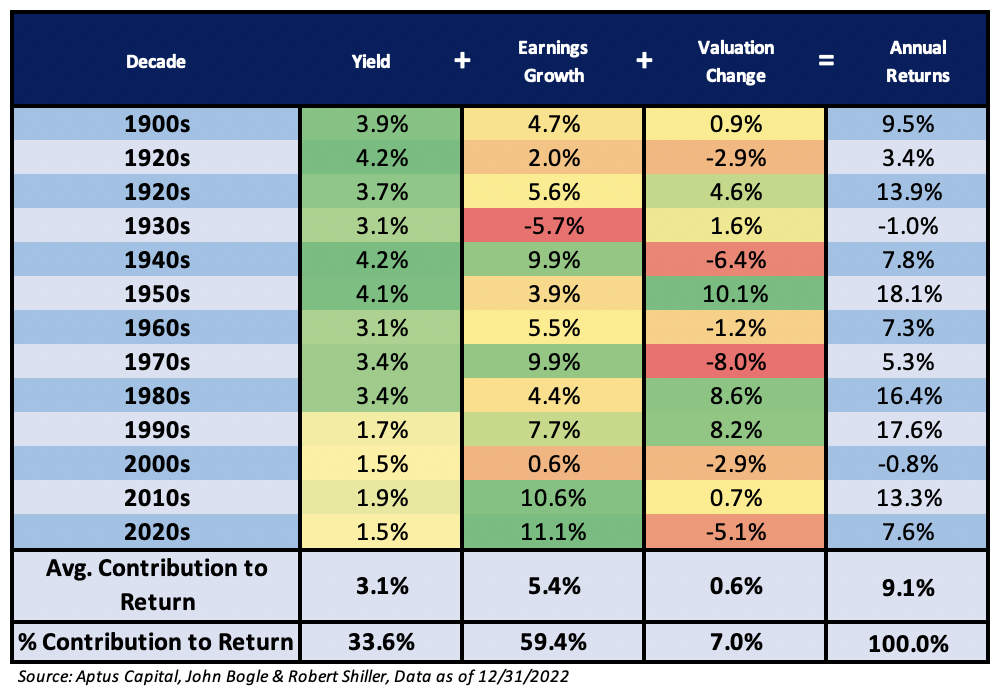

A quick reminder of the formula for generating investment returns looks like this:

Return = Yield + Growth +/- Valuation Change

Here’s the graphic we use to illustrate each of the 3 potential drivers of return, broken out with annualized return of each component, by decade:

Notice the ‘yield’ piece. According to Bank of America’s data as of 11/28/2022, the dividend contributions to the S&P 500 Index’s total return from 1936-2021 was 36%. That’s close to our breakdown above through 2019.

Bank of America notes that since 2013, dividend contribution to the S&P 500’s total return is only 14%. Yield has been important to total returns historically. In the past decade it’s been less important. We think portfolio’s attention to yield should be a priority moving forward.

What has happened matters less than what could happen moving forward. Rearview vs windshield…our job is to make sure we make allocation decisions with a sound forward look.

Our Positioning

We think quantitative tightening will be a challenge for risk assets. We think the Fed’s appetite to ‘hike and hold’ is real, to tame inflation. We think slowing growth, and the potential for cash flows available to businesses and households to fall while borrowing cost increase, is something to think about.

Thinking about a portfolio’s ability to generate yield, we believe yield’s importance is elevated, as growth and valuation expansion both face headwinds for the foreseeable future.

Volatility is an asset class to us, and a tool we can harness to help alter portfolios to better position for future returns. We are leaning into ways we can harness volatility to:

- Mitigate Risk

- Enhance Yield

- Capture Upside

We’ve gone as far as launching new strategies to help facilitate this. Rising volatility is not something we worry about. It’s something we are constantly preparing for. It’s something that can help illustrate how effective our approach to risk can be, and elevated vols helps improve the overall yield profile of certain strategies.

We continue to believe more stocks and less bonds is the needed allocation shift when hunting for long-term real returns. Our approach to volatility is what helps facilitate this shift while keeping risk in check. The traditional approach to portfolio construction that relies on the historical relationship of stocks and bonds is broken…I’m sure glad we don’t subscribe to the old line of thinking as we enter 2023.

As always, thank you for your trust and please don’t hesitate to reach out.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

The content and/or when a page is marked “Advisor Use Only” or “For Institutional Use”, the content is only intended for financial advisors, consultants, or existing and prospective institutional investors of Aptus. These materials have not been written or approved for a retail audience or use in mind and should not be distributed to retail investors. Any distribution to retail investors by a registered investment adviser may violate the new Marketing Rule under the Investment Advisers Act. If you choose to utilize or cite material we recommend the citation, be presented in context, with similar footnotes in the material and appropriate sourcing to Aptus and/or any other author or source references. This is notwithstanding any considerations or customizations with regards to your operations, based on your own compliance process, and compliance review with the marketing rule effective November 4, 2022.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2301-1.