I’ll cover 2 topics in this Musing: 1) Iran, and 2) Citrini.

I’ve been asked about the Citrini report several times over the past few days, so I wanted to address those questions. The Citrini Research report (titled “The 2028 Global Intelligence Crisis“) presents a “thought exercise” where rapid AI adoption triggers a “human intelligence displacement spiral.” Citrini then went on to say that this spiral leads to a 10.2% unemployment rate by 2028 as machines hollow out white-collar sectors and destroy the middle-class consumption that sustains the economy. Ok.

To me, it’s comical that the market has shown incredible resiliency against many negative headlines in ’26, yet a literal work of fiction—a sci-fi short story that the market is trading as if it were a roadmap—sends it into a tailspin. Consider this: market economists struggle to forecast 2-month-forward payroll growth with any reliable accuracy, yet the forward path of labor destruction can apparently be inferred with significant certainty from a hypothetical scenario posted on Substack.

The War with Iran

Before we begin, let’s keep things in perspective because many people tell me the market’s chaos will prevent it from remaining resilient, citing the turmoil. I say, when things get chaotic, get back to basics.

It’s all about growth – and don’t tell me there’s a growth scare; the S&P 500 just posted its 5th straight double-digit EPS growth, which is a record.

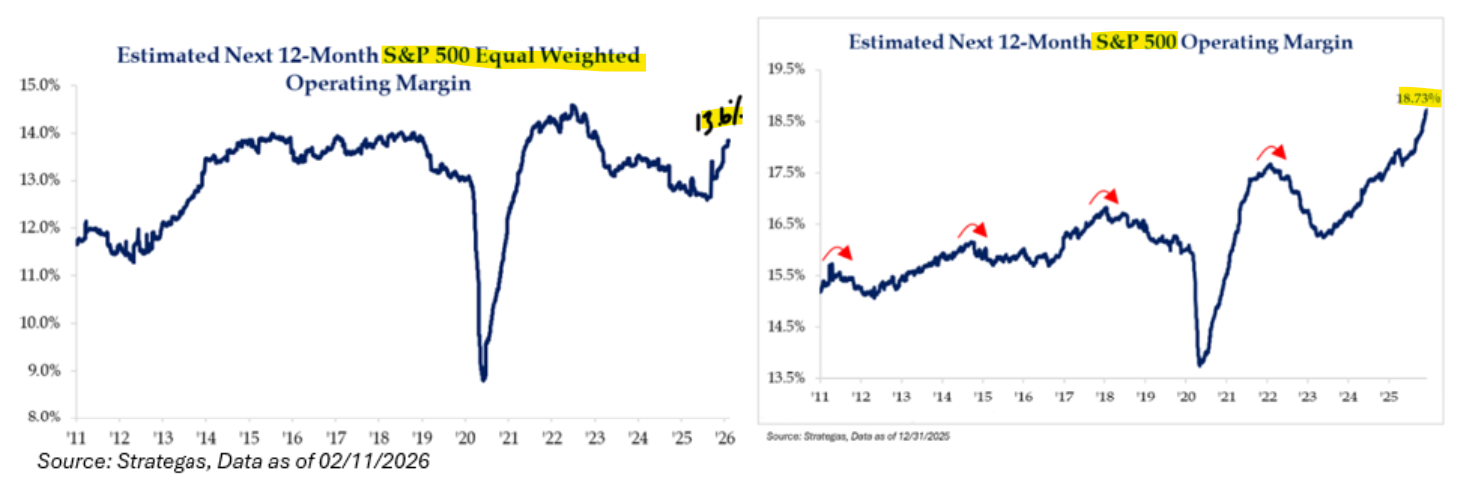

It’s all about margins – both the S&P 500 and the Equal Weighted S&P 500 have witnessed growth in their operating margin. Remember, it’s difficult for the market to get into trouble when margins are increasing or remaining stable.

In my opinion, the 2026 baseline view is very optimistic, as we’ve stated multiple times. US GDP growth should approach 3% (that’s in real terms). The math behind that is fairly straightforward: the labor market has stabilized (question me on this, if you’d like), financial conditions are easy, and fiscal support is increasing. While there are certainly downside risks to this optimism, when everything is thrown into the blender, it’s tough to believe there could be a recession in the next few quarters. To repeat a well-worn point, bear markets without a recession are generally rare.

Regarding market implications for Iran, after 21 US airstrike campaigns in the MENA region, the S&P was higher 95% of the time eight weeks later. While that’s a guarantee of nothing, it’s worth considering as we lunge from headline to headline.

Why? Markets look at geopolitical events solely through the lens of the impacts of critical

Resources (mostly oil), and unless the event is going to reduce the supply of available oil (and make the price rise, which could slow global growth), then markets will largely ignore the event. In the case of Venezuela, if anything, the events could boost oil supplies… or do nothing to them, but do not decrease them.

Regarding the U.S. and Iran, as we saw last summer, direct conflict did not spike oil prices sustainably, in part because Iran isn’t a major global oil exporter anymore due to sanctions and poor infrastructure. However, with the conflict between the U.S. and Iran resulting in the “closing” of the Strait of Hormuz or other major global oil transit, that would create a negative impact on markets as oil prices would rise sharply in response. Which has obviously occurred. But, I think we need to recognize that the US is not dependent on this oil; over 70% of US oil is produced domestically, so we aren’t as constrained by the Strait as the rest of the world, i.e., China. Globally, there are likely more ramifications, and that is why international equities were down so much on March 3, 2026.

Remain pragmatic here, but I’m not too worried that the Iran situation will create a recession in the US. We remain very optimistic.

Citrini Report

The Great AI Labor Debate: Will We All Be Jobless in the Year 2028? While reading on this topic, I came across Tavis McCourt, Head Economist at Raymond James, and his relative take; I thought it was awesome. Let me summarize it.

I’m going to start hot here … communism. Simply, Tavis compares Citrini’s SciFi report to that of the 1848 Communist Manifesto by Karl Marx. Specifically, his theory about how capitalism would negatively impact the workforce. Marx’s take may have sounded very logical, but, in my opinion, it was also catastrophically very wrong. Here were his main thoughts:

The Drive for Efficiency: To maximize margins, business owners are forced to relentlessly optimize labor, typically by replacing human effort with more efficient technological solutions.

The Shift to Automation: Intense market competition compels capitalists to pivot their investment away from human workers and toward “constant capital”, i.e., machinery and automated systems.

The Labor Surplus: By automating roles, the system maintains an “industrial reserve army” of the unemployed. This surplus of workers keeps demand for jobs high and wages perpetually suppressed.

Wealth Concentration: As production becomes increasingly automated, wealth flows upward, concentrating in the hands of the few who own the technology and means of production.

The Consumption Gap: Eventually, the system faces a paradox: as wages are squeezed to boost profits, the working class loses the purchasing power necessary to buy the very goods being mass-produced.

Systemic Instability: This leads to a dual erosion of real wages and profit rates, creating a “death spiral” that renders the capitalist framework unsustainable for both the laborer and the owner.

Obviously, this didn’t work out in practice because, I think, people underestimate the power of capitalism; capitalism always finds a way.

But doesn’t this sound familiar? These risks, outlined in Citrini’s report, make Americans highly skeptical of advanced computing. Below is an excerpt from Tavis’ “AI Doomer” piece:

“Human beings could only invent these new products and services because their jobs on farms were disrupted by technology displacement. Those new products and services required new labor to bring to market and service customers. Those new jobs were higher wage/standard of living (because if they weren’t people wouldn’t take them), on average, than the farm jobs of 1848, and that’s how the system works (simplistically). The economy creates jobs, it always has, and it always will (as long as people are paid for their individual effort, which ironically is what brings down communist systems).

Well over 10% of the entire US workforce today earns income in jobs today that couldn’t even be imagined 20 years ago (gig economy and social media influencer for example) all stemming from the internet renaissance. It would have been impossible to predict these jobs 20 years ago, and many would have fretted about how technology was going to crush newspaper, radio, TV jobs, retail jobs, etc… (it did), and create a permanent underclass resulting in permanently high unemployment (it didn’t). For those who remember, there was even a book in the late ‘90s called “The End of Work: The Decline Of The Labor Force”, highlighted by a book of the same name by Jeremy Rifken. It was hyped up relentlessly and referenced by those who thought the Internet would bring so much productivity that we’d end up with a permanent underclass of workers, but was also proven wrong (at least so far after 30 years). The Internet created jobs that replaced the jobs it destroyed. This is not because the Internet is unique, it’s how all technology advancements have worked. The unemployment rate today is similar to all prior periods of full employment and real wages have been compounding by ~1% annually since (which is about the same rate it always has increased). Maybe AI will be different, but if you are taking the “AI Doomer” view, you are ignoring ~175 years of evidence to the contrary.”

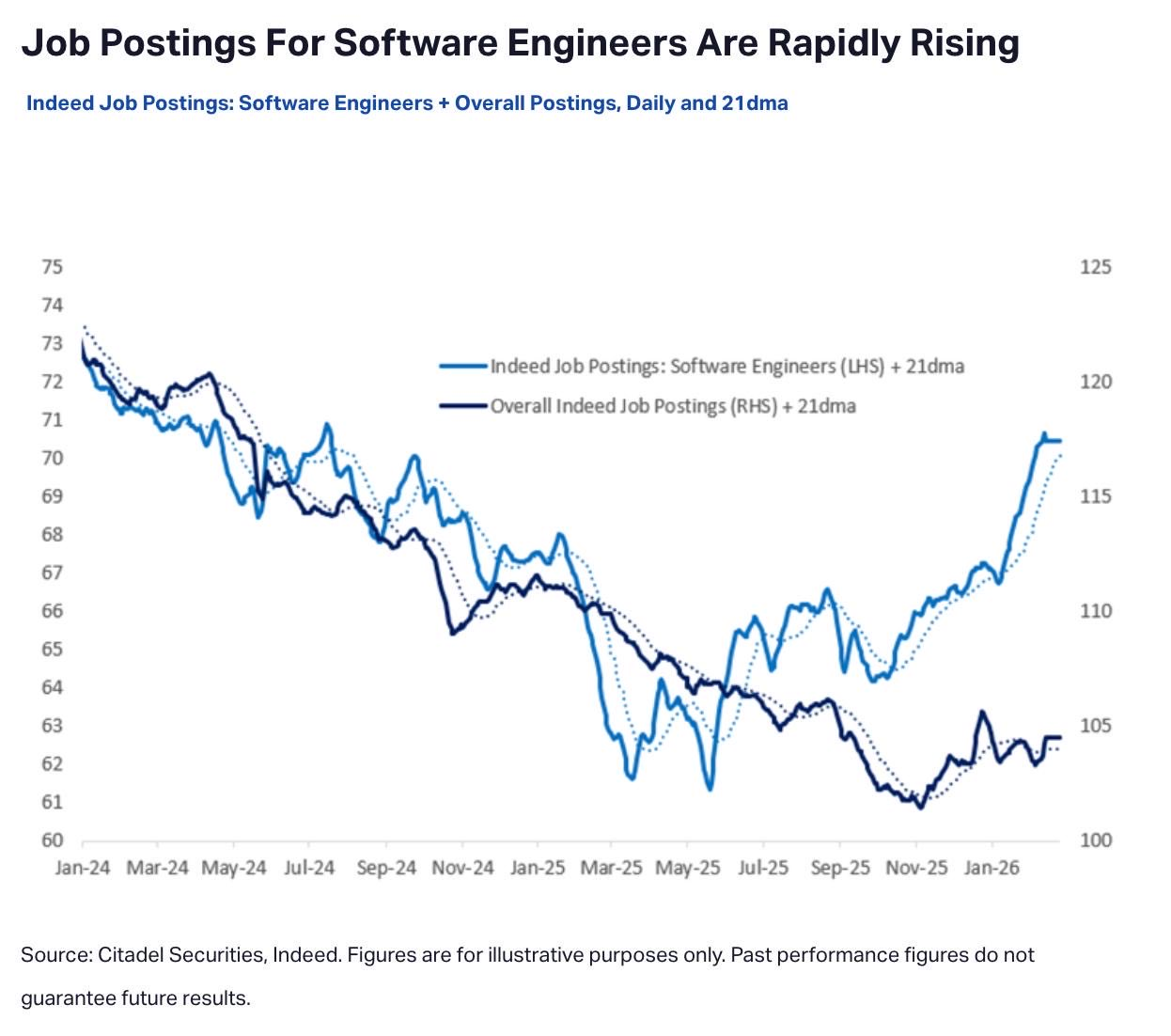

Let’s look at this in real time. If advanced computing will render all software obsolete, which seems to be what the market is currently pricing, why have we seen software job openings increase and meaningfully outrun overall job postings? I believe this goes against the disintermediation narrative.

Quick Synopsis

Structurally, history shows that a technological change has increased employment and living standards. So why is this time different? That’s the big question. Yet, many Americans are worried today because adoption and advancement are progressing rapidly, faster than they can perceive and at dollar amounts that seemed unfathomable just 10 years ago. The advancement of this technology scares people; that’s why the Citrini report hit so hard.

But, I believe investors need to stop framing AI as a zero-sum game. In my opinion, it can/will likely grow the pie of the economy, and when that happens with a capitalistic mindset, one could be off to the races. Again, I believe AI is a reason to be optimistic, but success depends on adoption, not the non-linear advancements of the technology itself, which the market has been witnessing and pricing in.

Here’s the optimism. Modern work has become a boring cycle of “babysitting” data. Many people spend their lives glued to screens, fixing other people’s typos (Brad Rapking fixes mine – S/O), tweaking the same PowerPoint slides, and fighting with messy spreadsheets that no one even reads. Our entire world now depends on these systems. You can’t travel, buy a house, or even renew your license unless a database says “yes”, and we all know those systems fail constantly. This way of living is expensive and broken, but for a long time, we didn’t have a choice. Now we do. Agentic AI isn’t just a luxury; it’s what I view as a necessity to save us from this digital grind. When that weight lifts, work transforms, and that’s healthy.

Overall Take

For AI to truly trigger a permanent economic downturn, several extreme conditions would have to be met at once: adoption would need to skyrocket, machines would have to replace humans almost entirely, and the government would have to stand by without intervening (LOL). This would require massive computing power to scale without limits, while new investments fail to create new jobs, of which we are nowhere close to that, given infrastructure bottlenecks.

In a way, displacing white-collar work would require orders of magnitude and compute intensity than the current level of utilization. If automation expands too rapidly, demand for compute definitionally rises, pushing up its marginal cost. If the marginal cost of compute rises above the marginal cost of human labor for certain tasks, substitution will not occur, creating a natural economic boundary. It seems more likely that AI will complement labor rather than substitute it in many areas. History suggests productivity gains do not automatically translate into labor withdrawal or demand collapse because they alter the composition of demand, expand real incomes, and generate new industries. Economists underestimated the elasticity of human wants.

Lastly, just because adoption rates may take longer than what investors believe is priced into the current market, it doesn’t mean that one should be bearish. Macro news can seem overwhelming, just remember, it’s still all about stocks, which are all about underlying businesses. Think of how quickly companies adapted in a post-COVID world, or during COVID for that matter. I wouldn’t bet against corporate America and its overall resiliency to quickly conform to new technological standards. That’s why we’ve been able to witness continued and exponential margin growth in the U.S.

Again, it’s a reason to be optimistic.

… That’s a great thing for the market.

As I said in my last Musing:

“I’ll leave you with one thing: The hardest way to get new ideas into one’s head is to get the old ideas out. Change is not bad; it is just different. When economic regimes change, so must the assumptions that govern our thinking of the state of the economy. There’s lots of change in our economy right now: 1) Supply side economics, 2) Jobs & remote work, 3) Sticky inflation, 4) Higher LT Rates, 5) Advanced Computing and 6) Immigration. Don’t deny change because it’s difficult to understand, embrace it and see if there’s an alternative way of thinking.”

Onward.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2603-9.