For the first time in a while, we have something to discuss coming out of Washington D.C. On Tuesday, President Biden signed into law the Inflation Reduction Act (“IRA”), which should be termed the Build Back Smaller Act, as the package is a slimmed down version of what Democrats have tried to push through Congress over the last year. I’ll be frank with you – the legislation does not match the name. Inflation will likely be more influenced by monetary policy and the money supply growth. Not to mention, most of the provisions included in the bill have nothing to do with inflation.

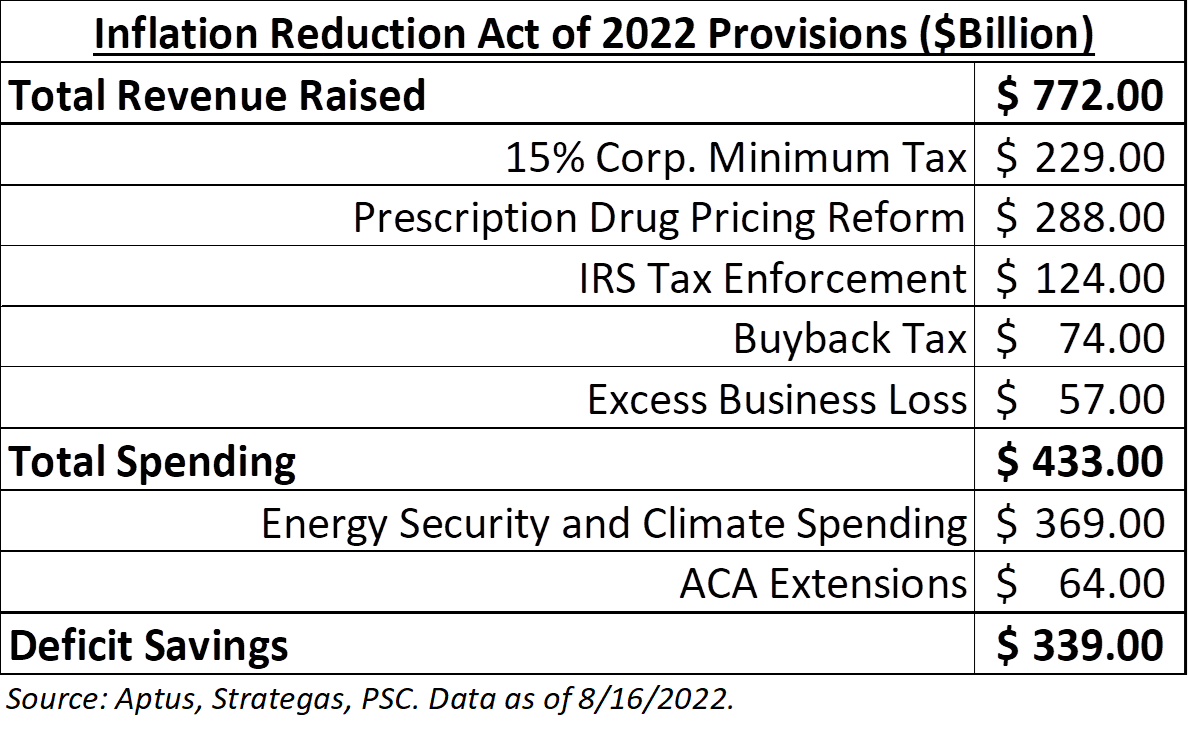

What does the bill include?

- An extension of existing health insurance subsidies through 2025

- A price control being placed on prescription drugs starting in 2026

- Renewable energy spending via tax credits

- A 15% minimum corporate tax rate and 1% buyback tax

- More IRS funding

Since we’ve been focusing on earnings a lot lately, let’s take a look at the bill’s effect on corporate profitability. Strategas has calculated that 2023 EPS will be reduced by ~2% due to the corporate tax law changes. Luckily, this is just a minor change, especially when compared to the original bill that was expected to decrease earnings by ~9%. This was largely done by dropping the most growth-killing tax increases on income and corporate profits.

My largest takeaway for the drug pricing and the buyback tax is that this could just be the beginning of more increases down the road.

Let’s walk through the bill – I obviously won’t touch on everything, but I’ll hit the major points.

Health Care Aspect

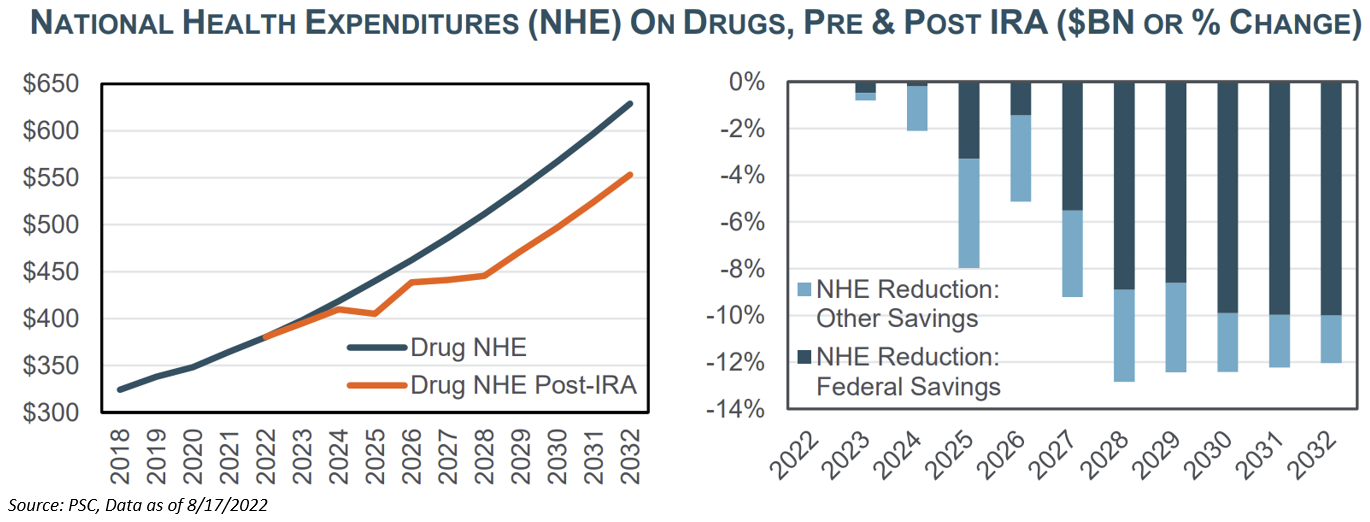

Congress enacted true pricing controls on some high-cost drugs covered under Medicare. Most of this will not go into effect until 2026, impacting the higher and older drugs. From there, the process ramps up quickly with 90-100 drugs that will see its price pushed down from 40%-60% by 2031. From a market perspective, I found it interesting that SMID-cap Biotech’s outperformed as the odds of the passage of this bill increased. My assumption is that the government overhang surrounding future pricing is now off the table, laying the groundwork for more M&A to occur in the space.

It is far more likely Democrats will be able to build on their drug price reforms in the coming years. With the architecture now in place, simple adjustments to the law would mean lower prices for seniors and more savings for the government. Additional drug price cuts could be used by Democrats to finance other popular benefits. Lower drugs prices for seniors and federal budget savings to pay for more benefits is a political winner, and some Democrats have already proposed going back to that as well.

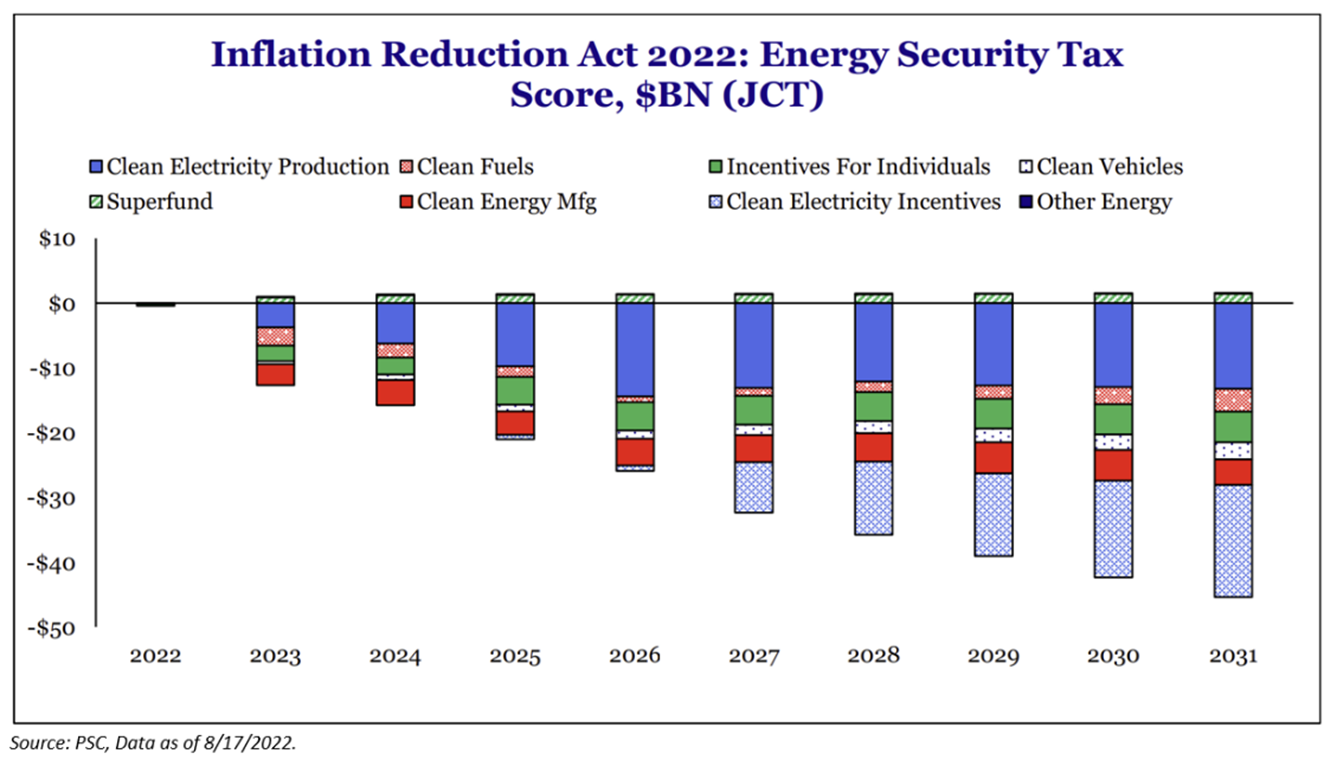

Renewable Energy

It’s no secret that one of the Democrats top policy goals revolves around climate change. The main takeaway from this aspect of the bill is that there are now long-term incentives in place for solar, wind, and energy storage development. Below are some of the major tax provisions:

- Residential Energy Property Credits: Extended through 12/31/2032, credits for installation of energy efficient appliances and certain home improvements.

- New Electric Vehicle Tax Credit: Beginning 2023, through 12/31/2032, the 200,000 vehicle cap per manufacturer is removed. The $7,500 credit is divided so that there is a $3,750 credit for meeting the critical materials requirement and a $3,750 credit for meeting the battery component requirement. Credit includes income and vehicle price limits.

-

- Vehicle prices are limited to $80,000 MSRP for SUVs, vans, and pick-up trucks while other vehicles are limited to $55,000.

- Income eligibility is limited to individual filers earning less than $150,000 or joint filers earning less than $300,000.

- Beginning 2025, critical minerals cannot be sourced from a foreign entity of concern and beginning in 2024, battery components cannot be sourced from a foreign entity of concern in order for vehicles to be eligible for the credit.

Honestly, there are about fifteen of these proposals that all attempt to try to increase capex on clean energy. Just ask and I can send them all over. Bottom line, it will take time for the clean energy spending to ramp up, with a small impact in the short run.

Tax Changes

The 15% minimum tax hits a small number of companies but is the equivalent of a 4% increase in the effective tax rate next year. Obviously one of the most affected companies is going to be Amazon.com (AMZN). From the reports that we’ve read, Utilities and Financial companies will be the most affected.

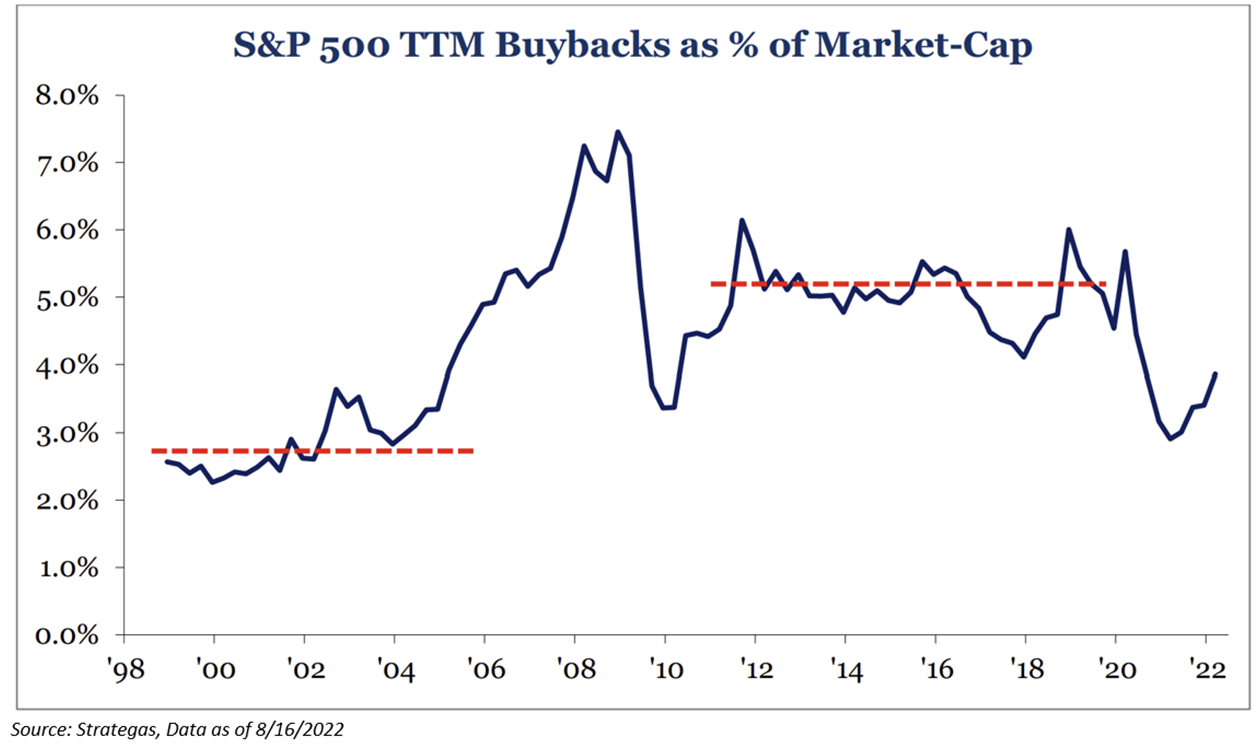

The wildcard for me is the 1% share buyback excise tax. Honestly, this is probably just the beginning of this tax. More importantly, this tax policy could be the beginning of a big sentiment change in capital allocation policies. Many people do not realize we had a 25-year decline in dividend paying companies before the tax treatment of capital gains and dividends were equalized in 2003. Previously, dividends were taxed as ordinary income at a much higher rate than capital gains. Once the two tax rates were equalized, the 25-year decline of dividend paying companies reversed and dividends became more distributed among sectors than just utility and tobacco stocks. Microsoft, in 2004, initiated a dividend and paid a special dividend nearly identical to their share buyback.

Our guess is that 1% will not make much of a difference. We can see companies pulling forward share buybacks this year because the bill doesn’t go into effect until 2023. But now that the tax is in place, it could always be increased. This will potentially make dividends preferable to buybacks over time.

I have spoken to several companies and part of that discussion is that buyback allocations could change to special dividends so as not to impact the indicated dividend tax rate.

What Does This Mean for Clients?

We’ve received this question a few different times. In a nutshell, not a whole lot. Once 2025 comes around, many people will see lower pricing in Part B and Part D drugs. Regarding share buybacks, the burden resides on the corporations. But here is where it gets more complicated – will it affect taxes on the middle class?

- Economic Ramifications: We believe that individuals ultimately bear the tax on all tax increases – whether it is through capital or labor.

- Tax Enforcement: It’s no secret that there is gap of what is to be owed to the IRS and what is paid. People misreport income all the time. If one owes additional taxes and get audited, that will increase their tax burden. What we don’t know yet is where the focus of the increased enforcement will reside, i.e., focused on high earners or everybody?

Honestly, I think one of my biggest takeaways is the political implications. This is a win for the Democrats because they finally got some sort of legislation completed.

If you made it this far – props to you.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2208-21.