This musing is basically a 2:1 special. In the opening monologue, let’s talk about what’s going on underneath the hood of the market, then we’ll get to the Kevin Warsh nomination and what that means for asset allocations (for more on Warsh, here is JL’s February Bond Market Update).

Many investors expected that the market would likely continue to reward the AI winners in 2026. Now that we are 7 weeks into the year, we’ve quickly recognized that the market has instead decided to torch the “AI” losers. For example:

-

- Semiconductors Industry outperforming Software Industry by 36% YTD, as software has been declared obsolete;

-

- Disruption from a potential AI tax planning tool that rocked Charles Schwab and other Wealth Managers;

-

- Insurance underwriters have been hit with concerns that AI agents sitting in consumer channels can quote, compare, and bind coverage directly, squeezing traditional distribution margins; or

-

- Or, a new trucking firm called Algorhythm, that used to solely sell karaoke machines (that’s cool in my book IMO) until it came up with an algorithm that could help trucking companies increase load by 300% without adding headcount.

Whether or not the disintermediation will turn out to be true in these industries, the market has taken the shoot first and ask questions later approach, even though the definition of “AI losers” is changing almost daily to the point where it is impossible to track. AI has been framed as supportive for equities, which we believe to be true; it’s just causing some volatility underneath the hood, as we go through a digestion phase of this revolutionary technology.

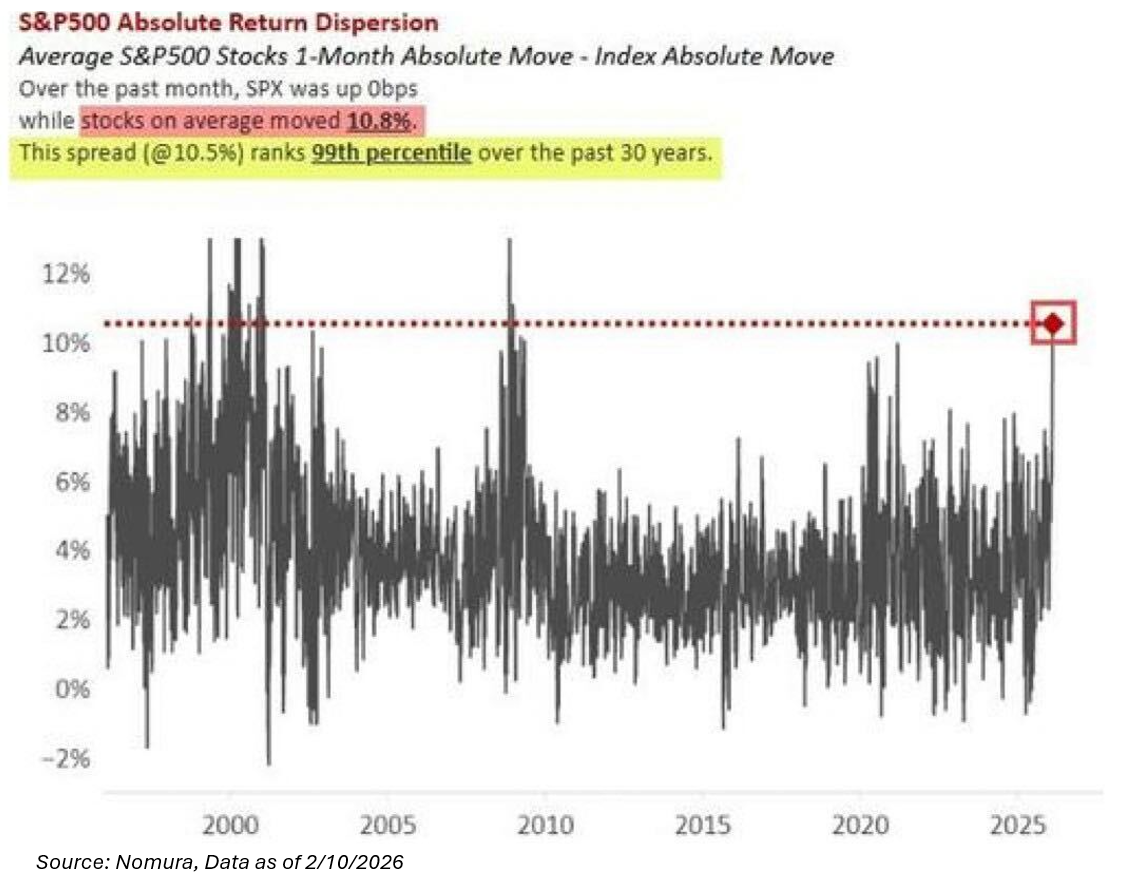

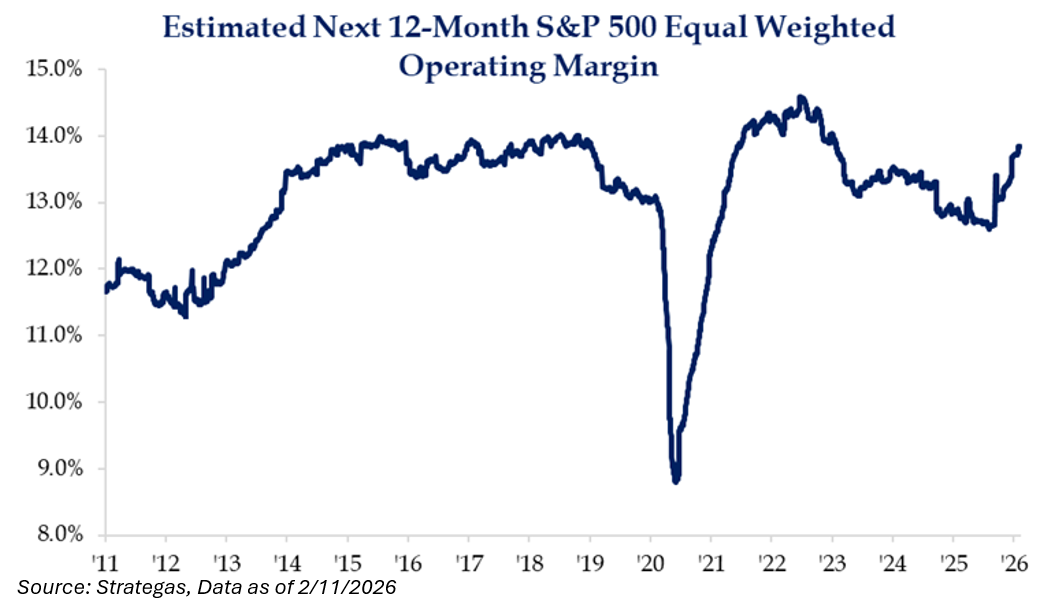

Outside of the equal weight operating margin table below (this is my favorite chart of the last month), it’s simply saying that while the S&P 500 is basically flat over the last month, the average price move for a stock in the S&P 500 is 10.8%, a level of volatility that has not yet reached the index level – which it may not.

Lastly, we’ll have our recap out on earnings next week, but the hyperscalers are still blowing the roof off capex estimates – something we’ve personally expected.

Consider this: at the start of January, consensus was for $540B of spending in 2026; now it’s already up to $657B (and the goal posts for 2027 have moved from $630B to $791B). In the shadow of mostly lower stock prices for the AI-universe, it’s not easy to disassociate the capex storyline from the absence of EPS upgrades, but the acceleration of spend continues to invite hard questions on returns and efficacy. Remember, in a winner-take-most construct, it’s not obvious whether these companies have much of a choice but to spend. This level of spend equates to 2.2% of GDP.

The fruits of their spend may be finally showing up in the smaller market-cap parts of the market:

Please reach out with any questions.

Can the Market Warsh Its Hands of Powell?

I believe that we need to attack this topic from two different perspectives: What it means for markets, and more importantly, what it could mean for asset allocations.

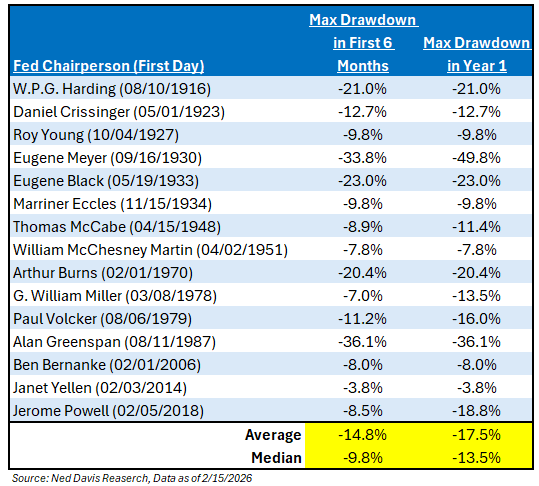

Markets tend to always quickly challenge the new Fed Chair (the average correction in the first six months is ~15%). When the chair faces its first crisis, investors don’t wait and see how they handle it; they instead quickly punish.

What Does this Mean for Markets?

We believe that Warsh is not as “Hawkish” as many first thought, but there are two reasons the market has some outstanding questions on his leadership.

First, he’s made some less-than-supportive comments about QE. Last summer, Warsh spoke about QE being “reverse Robin Hood”, in that it benefits asset holders more than non-asset holders. Specifically, Warsh thinks QE compounds inequality in the economy, which seems true to me. However, QE has become an integral part of the Fed policy, and many believe it is critical to the massive appreciation in asset prices over the past 17 years. Abandoning or altering the Fed’s reliance on QE would be a significant shift in Fed policy and markets.

Second, Warsh called for “regime change” at the Fed, essentially saying that the people running the Fed (Powell, etc.) are the same people who let the inflation genie out of the bottle, and because of that, there needs to be new leadership that can restore credibility from the public. Again, that’s not necessarily a bad thing (JL would say that his comments aren’t totally off base), but markets will want to hear more specificity on what exactly “regime change” means in the coming weeks.

Bottom line, in my opinion, markets don’t “hate” the Warsh choice, but markets view the Fed as a major ingredient of the 10+ year bull market in stocks and risk assets, so any potential change makes investors nervous.

What Does this Mean for Asset Allocations?

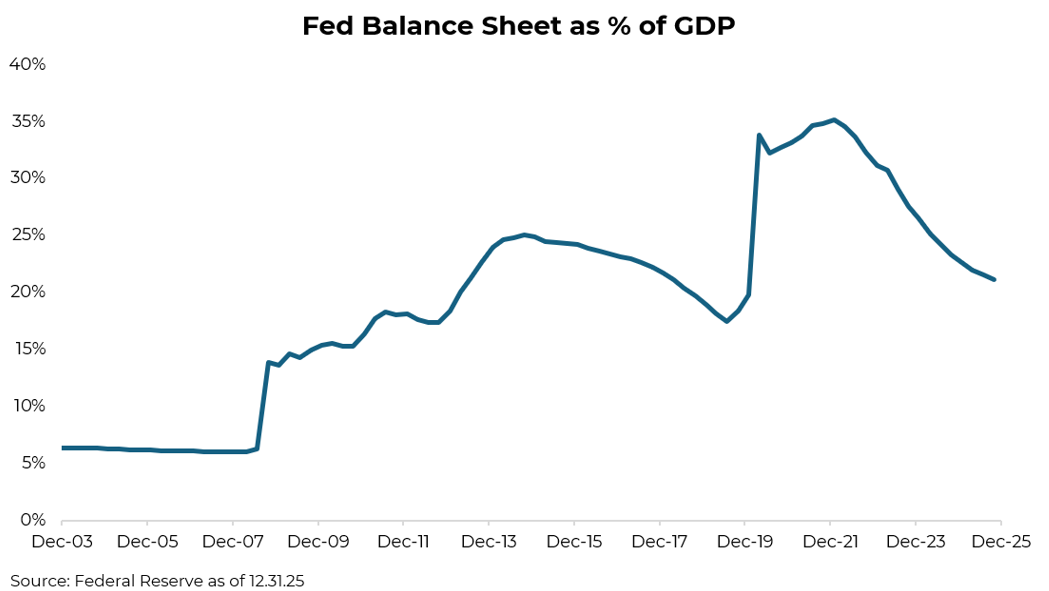

I believe that investors spend too much time focusing on the federal funds rate and not enough on the balance sheet operations. Thus, we should take note of Warsh’s balance sheet commentary; he wants to push for a smaller Fed balance sheet.

Personally, I don’t think he’s talking about the aggregate size of the balance sheet, but more from a relative perspective, as some balance sheet expansion is necessary to make sure the economy’s financial plumbing is in order. As you see below, the Fed’s balance sheet is finally back to pre-COVID averages – that’s a great thing.

And Kevin Warsh prefers to use the balance sheet only in extraordinary time periods like the GFC and COVID, not like how it was utilized post 2011 (one of the main reasons he originally left the Fed as a governor). Here are our two market thoughts:

Higher Rates

Cause: We know that the balance sheet cannot be cut without sacrificing the Treasury market, as the Fed could lose control of the overnight rate, which caused previous efforts to reduce the balance sheet to fail. Given the amount of debt coming due for the U.S. in the near future, there is plenty of Treasury supply available, and the Fed’s balance sheet has been one of the main areas of consistent demand, helping bid rates lower. If the balance sheet is utilized less, then there’s a chance that longer-term rates could increase, or at least stay at elevated levels.

Effect: Aptus was built on the framework that bonds are diversifiers, not hedges. If the balance sheet only gets utilized in certain situations, or less frequently, then our conviction only grows in the belief that fixed income may not be as insulative during bouts of volatility. Investors need to recognize the difference between diversifiers and hedges, as we believe it’s the best way to minimize drawdown risk.

Markets May Witness Fewer “V-shaped” Recoveries

Cause: Historically, the market has been able to sniff out the quick effects of QE. Think back to the depths of COVID when the market bottomed on 3/23/2020. It’s no coincidence that the market bottomed on the exact day that the Federal Reserve announced an unlimited QE program that would immediately hit the market; cue 03/23/2020.

Effect: If the Fed only uses aggressive balance sheet actions during extraordinary periods, then the market may see more prolonged downturns during the regularly scheduled recessions. Much like the above point, this should signal to investors that downside protection is even more important moving forward than it has been in the recent past, and maybe 2022 is the perfect case study for this.

Lastly, there remains a lot of unknown about Kevin Warsh’s policies. The above analysis is just a knee-jerk reaction to what we know so far. To be frank, in my opinion, Warsh likely relinquishes some of his convictions on balance sheet utilization in order to get more conformity amongst board members. Nonetheless, his ideas for a “regime change” at the Fed need to be something investors focus on in the future, as it could alter market dynamics that investment participants have become accustomed to.

Onward and upward.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2602-15.