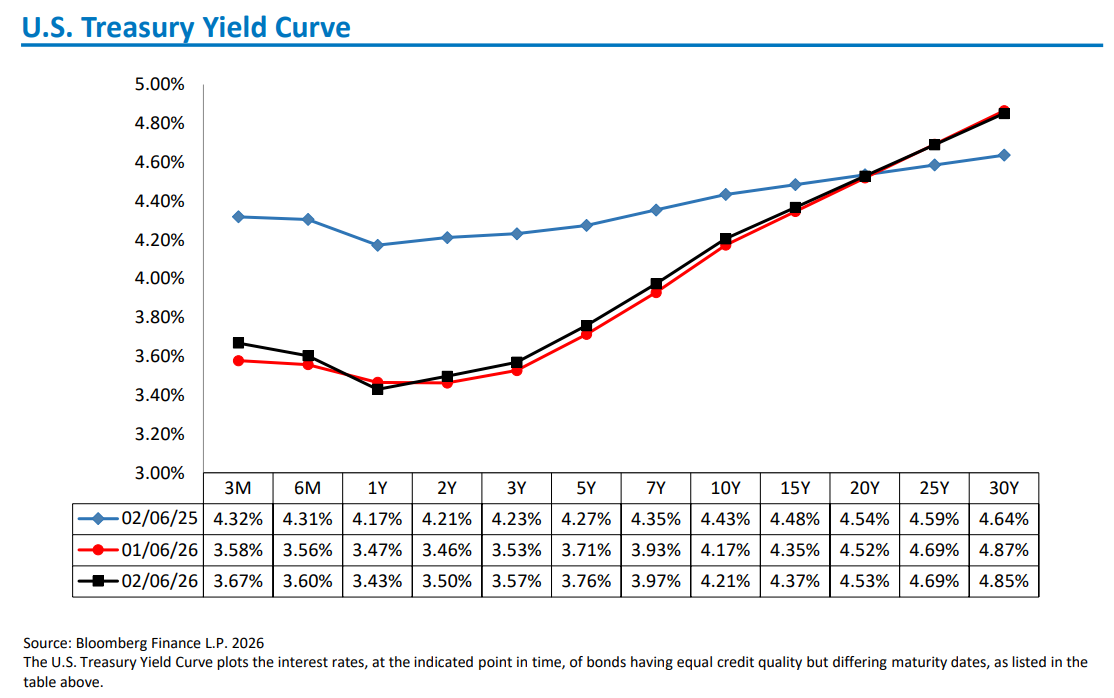

Yield Curve Steepening Trend Continues

The graphic below shows the shape of the current yield curve (black) vs. a month ago (red), and vs. 1 year ago (blue). As the Fed has reduced its policy rate, the yield curve has steepened due to the front end declining while the long end has held at roughly the same levels. The intermediate portion of the curve has benefited from declining front-end rates and improving inflation dynamics (and performed best from a total return perspective).

Data as of 02.13.2026

Data as of 02.13.2026

The consensus call by markets is for further steepening in the curve. While we generally agree, it’s unlikely to be a straight line. If we continue to see strong nominal growth and large fiscal deficits, it will be difficult to see the long end of the curve decline precipitously.

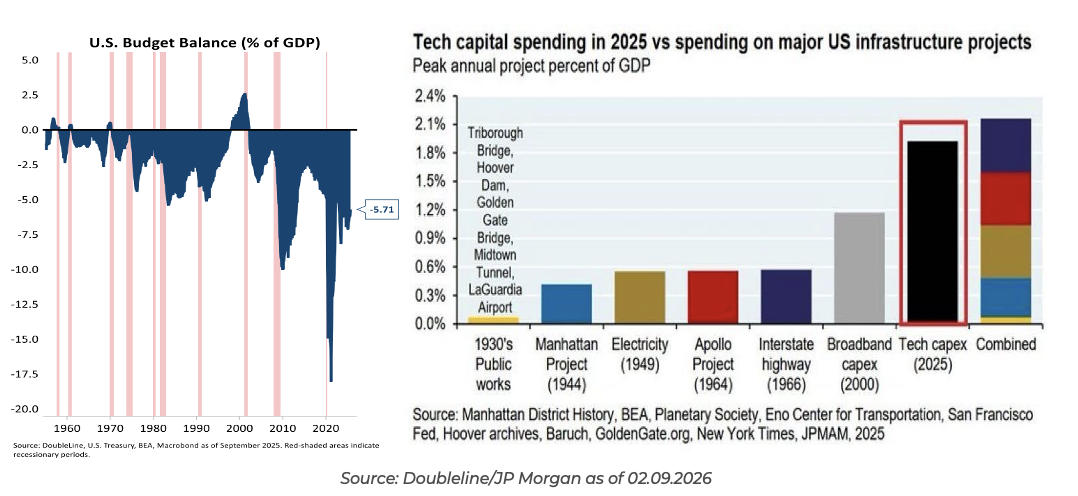

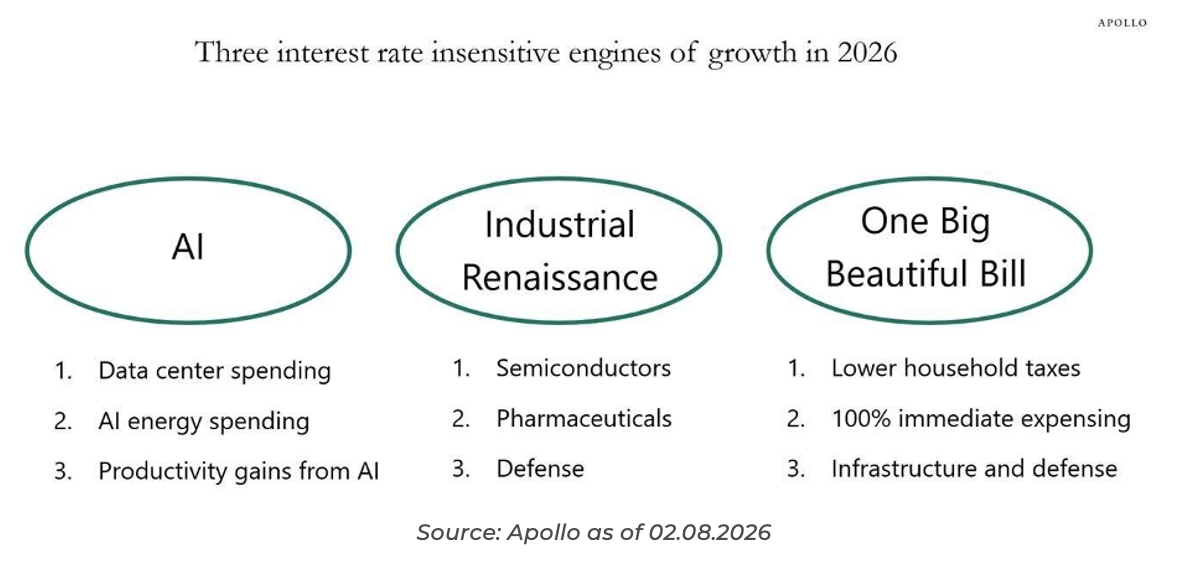

Large Deficits + Private Stimulus

There is no shortage of liquidity backstopping this market. Fiscal deficits in the range of 5-6% of GDP, One Big Beautiful Bill (OBBB) 100% depreciation capex pull-forwards, and consumer tax refunds should continue to support the economy. Fiscal policy, according to the CBO, is expected to lift GDP growth this year by 0.9%.

Additionally, nominal GDP is running around 6-7%, while Mag7 capex spend in ’25 is 1-2% of GDP. S&P 500 companies that have reported earnings have seen 81% beating on EPS, with 70% beating on revenues. While there are no guarantees in this business, it’s hard to see a recession in the short to medium term.

Kevin Warsh’s Fed and the Backstory

We wrote a short bio on Kevin Warsh in the last Bond Market Update after his nomination. Kevin is viewed by the market as a “Hawk”, specifically relating to his comments on the Fed’s (large) balance sheet accumulation over the past ~20 years. We wanted to set the stage a bit on how we think Bessent and Warsh can work together to resculpt the Fed and Treasury relationship and how it might impact the market.

Post-GFC: Steep Increase in Bank Regulation

After policymakers were forced to rescue the financial system in 2008, regulators raised standards on banks to minimize the financial system’s systemic risk. This led to constraining bank balance sheets and forcing banks to hold safe, monetizable assets at all times to protect against future losses or bank runs. These regulations have been costly for banks, and Scott Bessent has pointed to substantial balance sheet capacity for banks if regulations were regulations to ease.

Warsh’s Position in the Matter

Warsh believes the Fed’s balance sheet is too large and should decrease. While this is probably an “easier said than done” task, we believe that to some capacity it can be done. Warsh can reduce the Fed’s balance sheet while also ensuring that banks have ample reserves to maintain control of the overnight rate. Ultimately, it’s bank deregulation that is the critical link to make this possible by creating space on private-sector balance sheets to take down the decline in the Fed’s bond assets.

Vice Chair Bowman is set to release a deregulatory proposal within the month that will lay out the next steps for rolling back the post-GFC infrastructure. Tailored deregulation is needed to boost demand for Treasuries, to avoid tighter financial conditions (at the end of the day, when Debt to GDP is at ~120%, we need to find more buyers for the debt).

Keep in mind that all of this requires a collaborative approach among the Fed, banks, and Treasury to privatize the balance sheet – and do so without negatively impacting bank balance sheets.

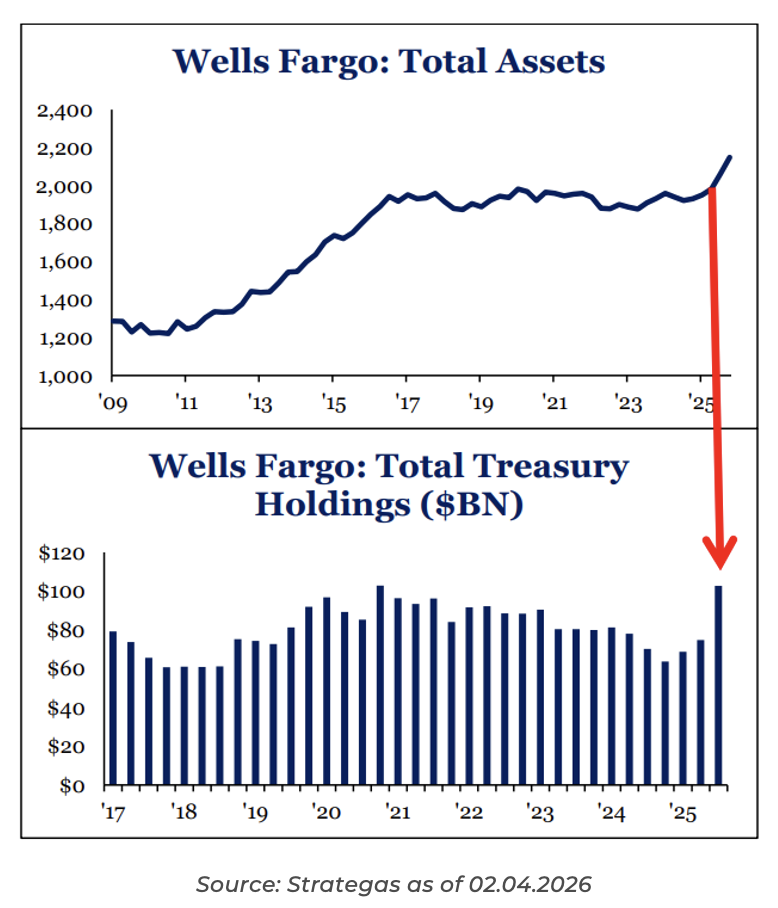

A Real World Example

Last June, the Fed lifted Wells Fargo’s asset cap (allowing it to grow its balance sheet), which had been in place since 2018 and had constrained its balance sheet.

The lifting of the asset cap had immediate results, with Treasury holdings increasing by 37% quarter over quarter in September. The lifting of Wells Fargo’s restrictions could be seen as a test case for when the entire banking sector is deregulated.

Additional Measures on the Deregulation Front

Liquidity Surcharge Ratio (LCR): The LCR requires banks to hold enough “high-quality liquid assets” (HQLA) to cover 30 days of anticipated cash outflows during a potential crisis. But the determination over which assets are “high quality” and which assets are “liquid” is a question for regulators. Currently, Treasuries, Reserves, and certain other government-issued or guaranteed securities can be held at a 0% haircut, with other assets held at greater haircuts depending on their riskiness. As such, raising haircuts on non-Treasury assets should boost demand for Treasuries among LCR-constrained banks

G-SIB Surcharge: A surcharge applies to the eight G-SIBs (Globally Systematic Important Banks) that is meant to quantify a bank’s “systemic risk.” Due to a quirk in the calculation, the surcharge does not account for economic growth, so growth in the overall size of the banking system leads to surcharge bracket creep as scores increase automatically. Indexing the surcharge to GDP would provide some relief. But if regulators wanted to target the Treasury market directly, they could exempt Treasuries from the G-SIB surcharge entirely.

Enhanced Supplementary Leverage Ratio (eSLR): The eSLR requires the eight G-SIBs to hold capital against all assets on an unweighted basis, i.e., not accounting for the asset’s riskiness. In practice, this discourages banks from holding low-risk, low-yielding assets like Treasuries and Treasury repo. Governor Miran called for a full exemption for Treasuries from the calculation, which would lower the hurdle rate for banks to buy Treasuries. The SLR was paused post-COVID but reinstated after market volatility declined. A permanent reduction would incentivize more bank Treasury purchases.

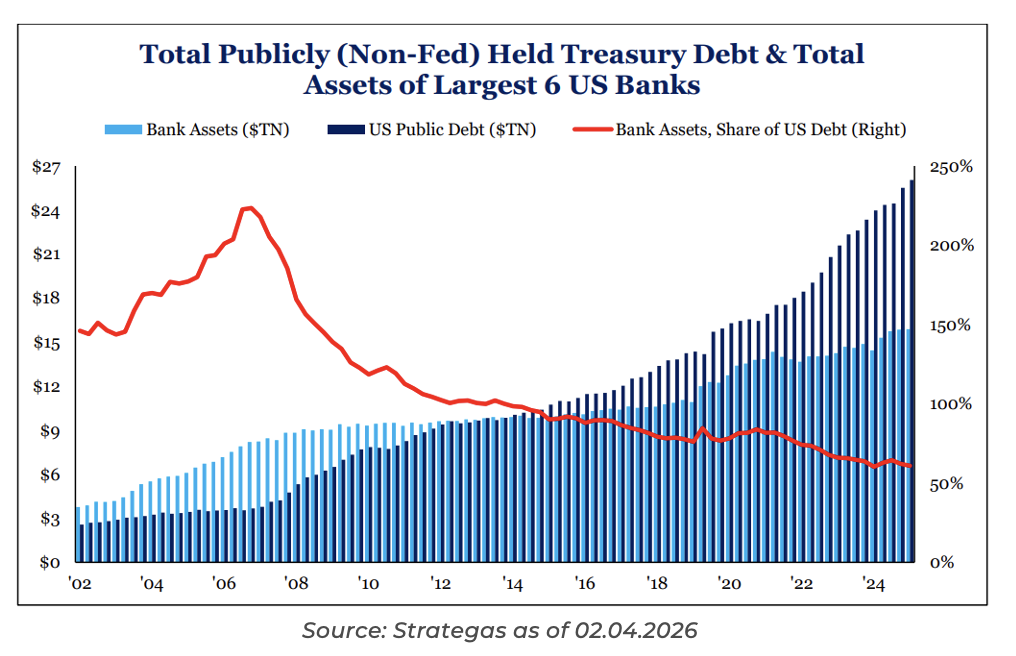

The US Needs Banks to Own More Treasuries

As the US Debt has increased dramatically, the ownership of Treasuries by banks hasn’t kept up. With Warsh as the new Fed Chairman, I think he will have the opportunity to make lasting changes on the Fed, its role in markets (via the balance sheet), deregulation, and interest rate policy.

Undoubtedly, he will be challenged by markets as most incoming Fed Chairs are, but we think he and Scott Bessent (sharing a background under their mentor, Stan Druckenmiller) can press forward with a pro-market agenda to bring rates lower while:

-

- Shrinking/maintaining the Fed balance sheet size as they seek to lower interest rates (per Trump)

- Keeping inflation in check

- Maintaining a strong labor market

I, for one, am glad to see market practitioners at the helm who can listen to the market respond to their decisions as we navigate a wild market, a new era of AI, and lots of (and growing) government debt.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2602-14.