January FOMC

The Fed held its policy rate in the 3.5-3.75% range earlier this week, largely as expected. The vote was 10-2, where Governors Miran and Waller dissented in favor of a -25bp reduction (Bowman did not dissent).

The Fed noted better growth and “some signs of stabilization” in the labor market, which left the Committee feeling well-positioned to stay on hold while they assess the incoming data. In their statement, the Committee upgraded its characterization of growth from “moderate” to “solid,” now, which is undoubtedly a reflection of the recent pickup in GDP to a lofty 4.4% in Q3, with expectations of 5.4% growth at year end.

Job gains have “remained low,” while the unemployment rate has “shown some signs of stabilization.” Labor market momentum has slowed, but hiring remains positive at an average pace of 49k since the start of 2025, and in line with the hiring growth deemed necessary by the Fed to maintain full employment, given the change in immigration policy from the Trump administration (small denominator of labor force).

Powell described the policy stance as “loosely neutral” or “somewhat restrictive” and noted that the December dot plot showed that 15 of 19 FOMC participants anticipate additional normalization. He reiterated his own optimistic interpretation of the inflation data and said that he expects tariff effects on inflation to eventually fade, at which point “we can loosen policy.” It will likely take time for the data to improve enough to create a strong consensus on the FOMC to normalize further, given the Year-over-Year (YoY) rate of core PCE inflation will likely remain closer to 3% than 2% until mid-year.

Bottom Line

Following 175bps in rate cuts the past two years, the Fed opted to move to the sidelines with policy seemingly closer to or even potentially at the neutral level (I still see more cuts coming). The big question remains: What’s next?

Powell made it clear that the “extent and timing” of any additional policy moves will depend on changes in the economic outlook. At this point, with no further compelling evidence of additional cooling in the jobs market, the Committee is likely to cease further rate cuts in the new year, potentially for an extended time. It appears that the market may not believe them.

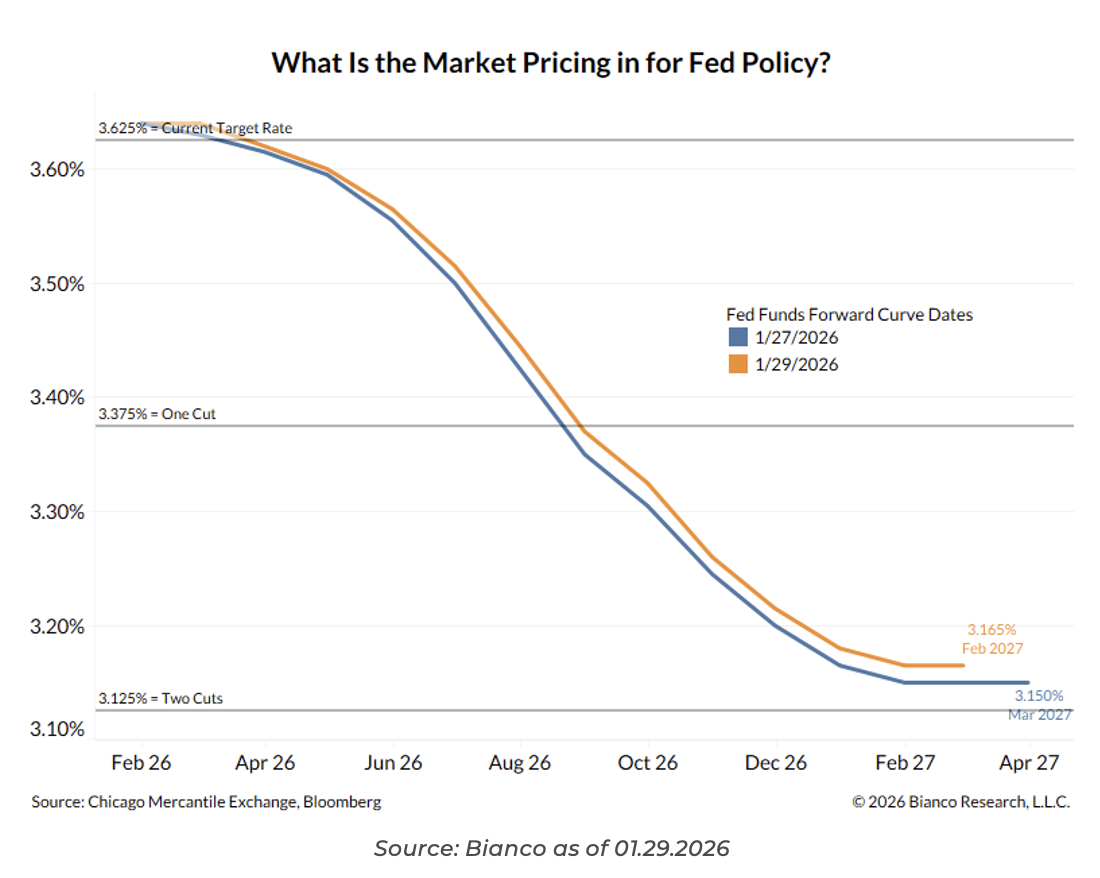

Last year, the debate was over when and how many additional cuts were needed. Now, with only moderate softening in the labor market, above target inflation (58 consecutive months, but who’s counting), and a significantly stronger headline growth profile, the conversation has shifted to whether any further policy easing will be necessary. While the market continues to price in ~ two additional cuts, the majority of officials see just one, with seven still forecasting no adjustments to policy in 2026. The graphic above shows the market pricing of the Fed Fund Futures for the next ~18 months. Even after a mildly hawkish meeting, the market is still optimistic about cuts.

Truflation Sees Continued Disinflation

We’ve written several pieces on the Truflation. We admired how well it led CPI inflation higher before the massive run-up in 2021, how it marked the peak in ’22, and how it has (slowly) been moving lower the past year or so.

The pace of the decline has picked up since December, currently at ~1.23%. The effect of tariffs on goods inflation, the weak housing market on shelter, and softening wage gains should continue to bring down inflation in goods, housing, and services. According to Truflation’s real-time data, U.S. inflation could be about to experience another leg lower.

Productivity Miracle?!

U.S. productivity is improving. After revisions, nonfarm productivity was strong in 3Q, at a +4.9% QoQ annual rate, reducing unit labor costs (productivity-adjusted wages) by -1.9%. High productivity, which restrains unit labor costs, should help anchor inflation.

And the New Fed Chair Nominee is…. Kevin Warsh!

Trump announced he is nominating former Fed Governor Kevin Warsh to be the next Fed Chairman when Jerome Powell’s term expires in May. Warsh comes from Wall Street (Morgan Stanley) but sat on the Fed Board from 2006 to 2011 during the depths of the Great Financial Crisis (he was appointed by George W. Bush and was the youngest Fed Governor ever at age 35).

Warsh will have to wait for Senate approval before taking the seat (he is replacing Miran’s seat, as it expired yesterday). Powell’s seat will be replaced if he ends up retiring in May (the market will view this as another chance for Trump to get another friend at the Fed). The market is viewing Warsh as a hawk, but we’d label him as “practical”.

Warsh is also known for his views regarding the Fed’s balance sheet, which he wants to be smaller. We believe many of the bank deregulation plans in motion will be key in unlocking private bank reserves in order for a smoother transition to a smaller Fed balance sheet. As Mike Tyson says, “Everyone has a plan until they get punched in the mouth”.

Odds for rate cuts have shot up following the announcement, with ~84% chance of a cut by June and 118% chance of a cut by July. The market is now pricing in two full cuts for 2026.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2601-37.