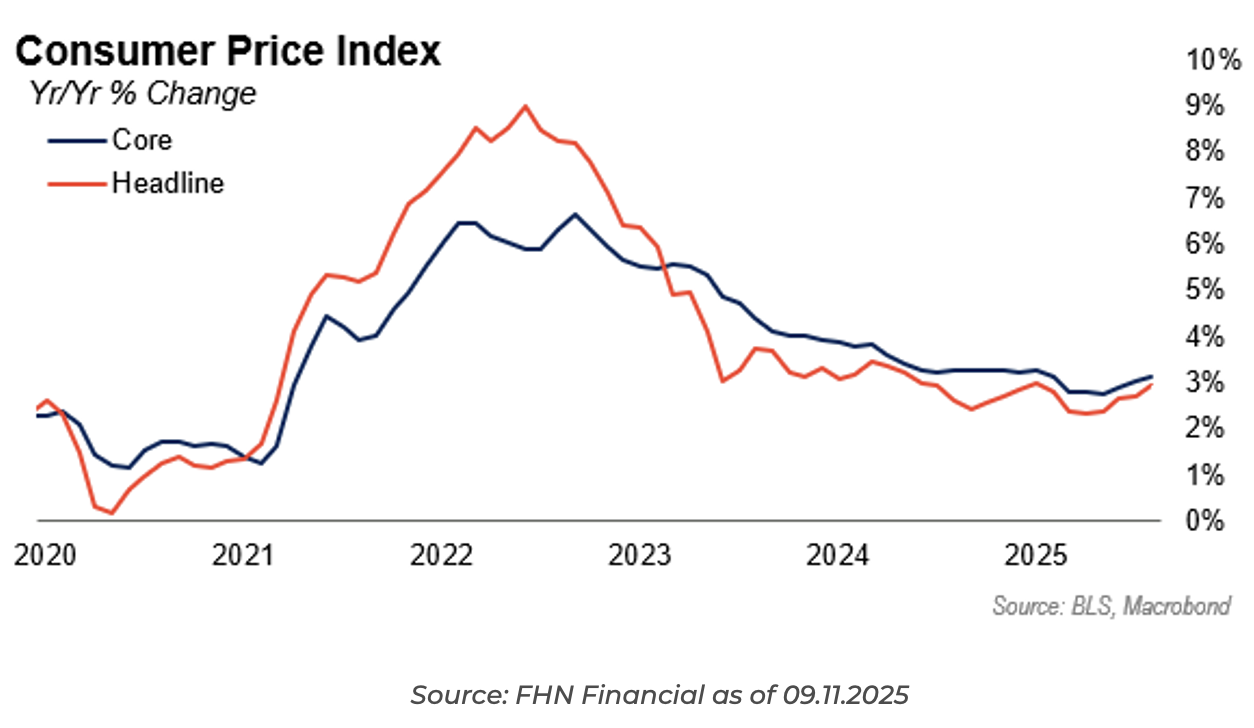

CPI came in a touch hotter than expected in August, with the headline rising 0.382%, rounding to 0.4%, and the core rising 0.346%, rounding down to 0.3%. The consensus was 0.3% for both. The YoY CPI inflation rate rose from 2.732% to 2.939%, while the core YoY rose from 3.049% to 3.112%. Bear in mind, while today’s inflation rate was a little higher than expected, back when tariffs were imposed earlier in the year, the end-of-summer inflation rate was projected to be much higher than the 2.9% headline and 3.1% core reported today.

Goods vs Services:

- Core goods rose 0.276%, the most since January. (July was almost as high.)

- Core services rose 0.349%, just a hair less than July

Details:

- Food prices increased from 0.0% to 0.45%, with grocery prices rising 0.6% and restaurant prices steady at 0.3%.

- Energy rose 0.7% in August but is up just 0.4% YoY.

- Medical care fell 0.1%, but the YoY rate is 4.2%.

- Rent/OER inflation unexpectedly accelerated. Shelter rose 0.44% in August and 3.642% YoY. The YOY rate has fallen ten months in a row. OER rose 0.382%

- Service components such as lodging-away-from-home (+2.3%) and airline fares (+5.9%) also surprised to the upside.

Inflation has clearly accelerated since May, and it was still accelerating in August. Nevertheless, if the tariffs result in inflation peaking at ~3% this year and receding from there, it is not nearly as bad as projected earlier in the year. Slower moving components like shelter, which have a sizeable weight in the calculation, are slowly moving lower. In contrast, more timely rent data has already rolled over. Alternative CPI calculations using more “real-time” rent data show the CPI calculation much closer to the Fed’s 2% target.

Bottom Line:

When we combine the recently released PPI & CPI data, PCE inflation (the Fed’s preferred measure) likely rose +0.3% m/m in Aug, with the core (ex-food & energy) up +0.2%. These are somewhat elevated numbers, but not alarming. With inflation expectations still looking anchored, we are not overly worried about runaway inflation here.

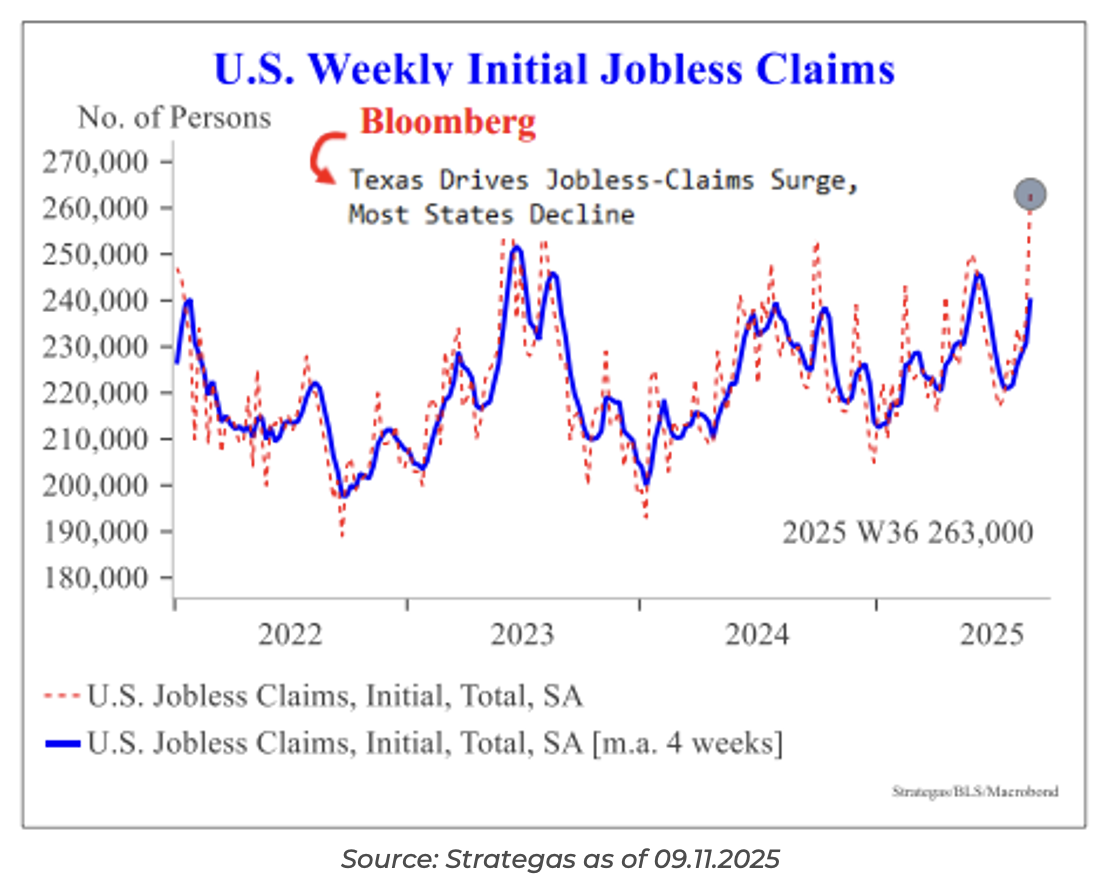

Initial Jobless Claims Spike

In addition to CPI this morning, we also got a report on the weekly initial jobless claims, which rose sharply to +263,000 this week.

This is a more worrisome report vs. the CPI, but if U.S. corporate profits continue growing, as expected, it’s difficult to see layoffs surging in the private sector. Additionally, the bulk of the softening was related to job losses in Texas. ConocoPhillips and Halliburton (two large Texas-based employers) both announced large layoffs, which help explain some of this week’s spike. We’ll continue to monitor the 4-week average of claims to see if this is something more sinister. Keep in mind, one data point doesn’t create a trend.

Initial Claims: 10 Year Look

Additionally, if we take a step back and look at the bigger picture, initial claims appear muted.

Again, a one-week pop doesn’t make a trend but will magnify eyeballs on the future state of the labor market. The Fed appears to be on full alert, as Chair Powell highlighted in his Jackson Hole speech that risks to the labor market likely outweigh the risks of inflation.

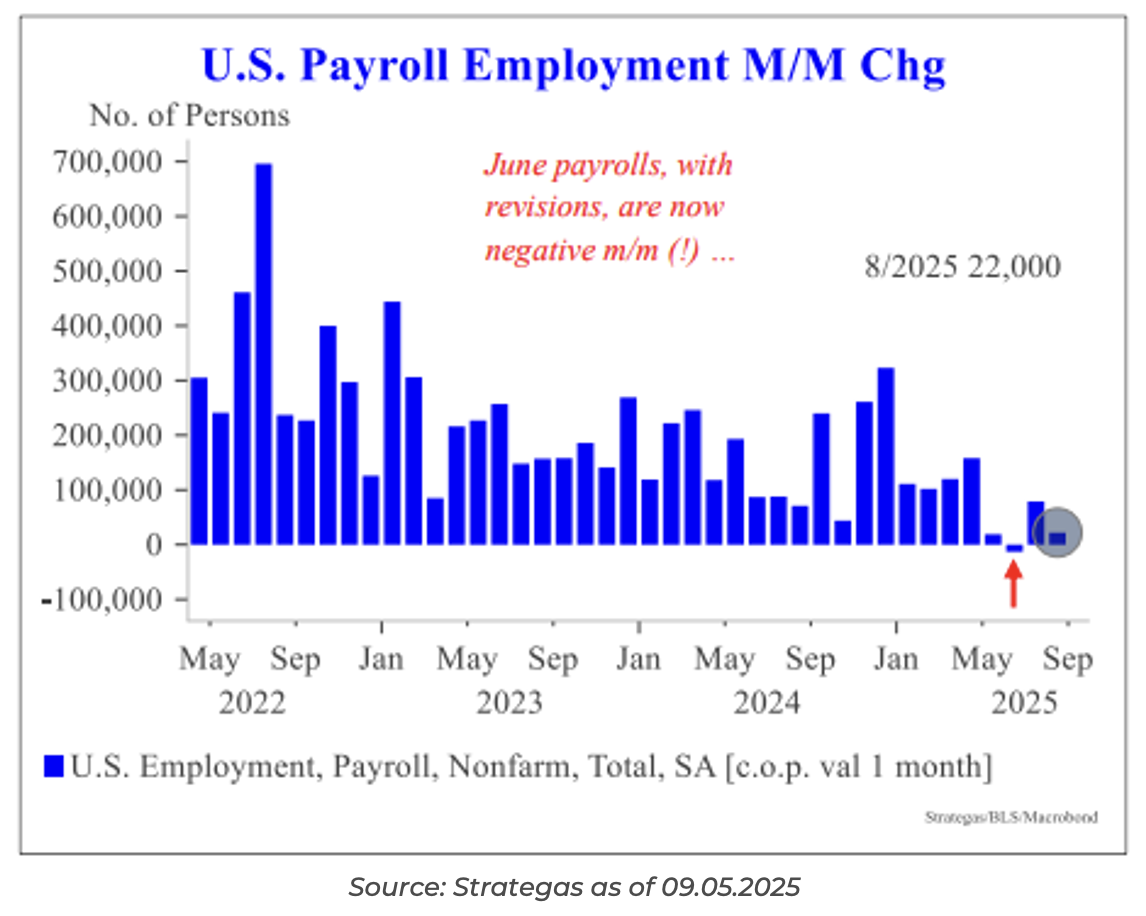

Nonfarm Payrolls

Last Friday, we got another weak job report. The headline NFP print came in at only +22k vs +75k expected jobs added. The report shows the revisions from last month were real. Job growth has slowed to being barely positive. Hiring was concentrated in education/health +46k, and leisure and hospitality at +28k. Other categories were negative, including a -25k reduction in goods-producing jobs. The unemployment rate rose from 4.248% to 4.324% with a slight rebound in the participation rate to 62.3%.

The noisier household employment survey was up 288k this month, with average hourly earnings +0.3% m/m. This data is more volatile but can be another signal to watch during turning points.

Weakening trends in the labor market are sparking concerns that the Fed is behind the curve. Weaker real-time data likely cements a September rate cut of 25bps. Markets are now pricing in ~3 cuts in 2025 and 3 more by the end of 2026 (i.e., 6 rate cuts in total), bringing the Fed Funds “Terminal Rate” down to ~2.75%.

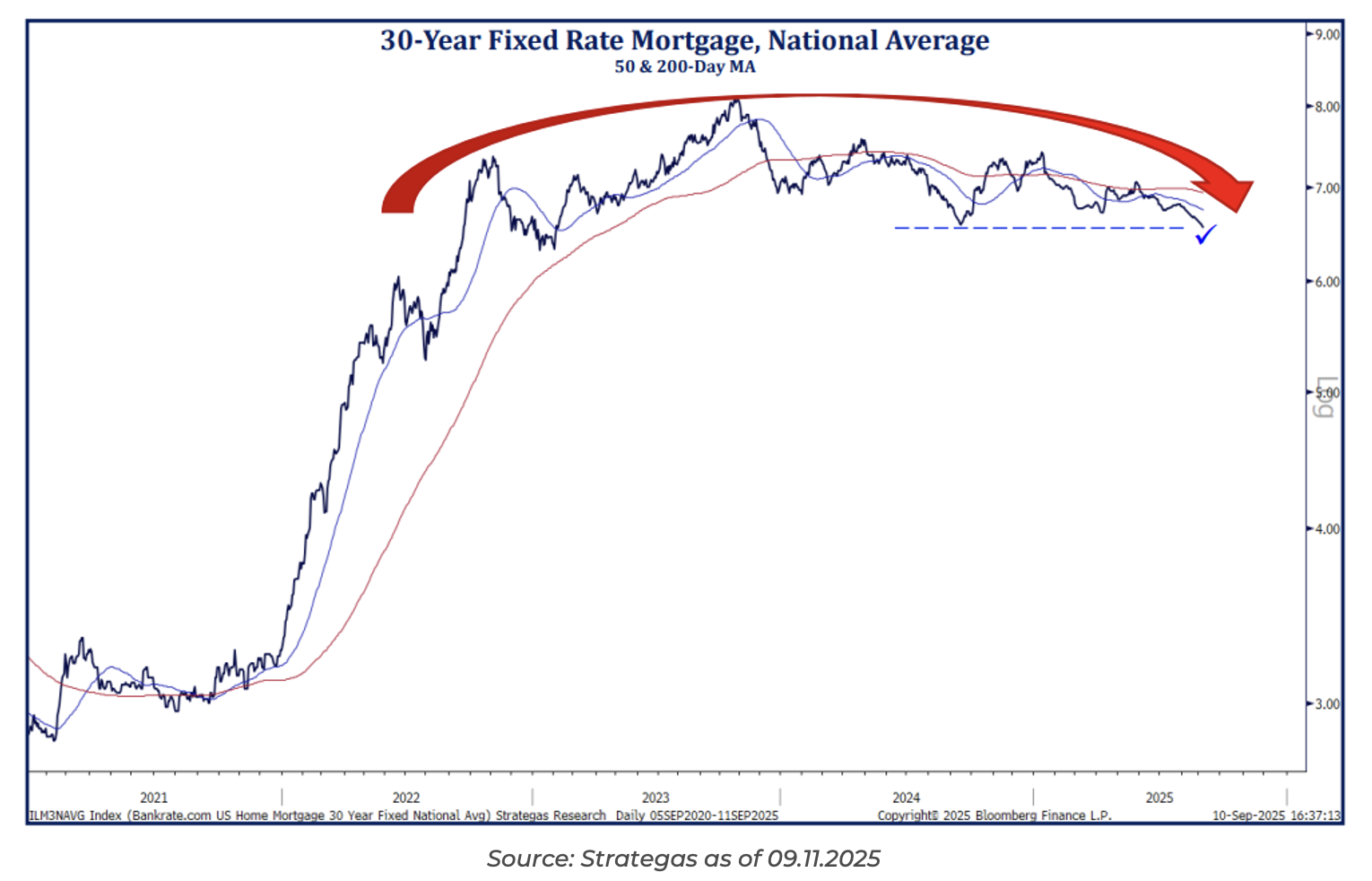

Mortgage Rates Continue Stepping Lower

We have all seen the charts showing that housing affordability is in a difficult spot. High mortgage rates along with limited housing supply (3% mortgages creating a golden handcuff) have led to a difficult backdrop for potential homebuyers, especially first-time buyers needing a mortgage. The housing market has basically been stuck in quicksand outside of wealthy boomers paying cash for homes.

In order for the economy to function properly long-term, we need housing affordability to improve. While deregulation could help, lower mortgage rates will be the quickest way to see housing activity increase. Additionally, as rates decline, those who did take out mortgages in the last few years will be able to refinance and lower their mortgage payments (increasing monthly disposable incomes). We’re keeping a close eye on mortgage rates, and as they decline, we expect to see activity recover as consumers capitalize on lower financing costs.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2509-15.