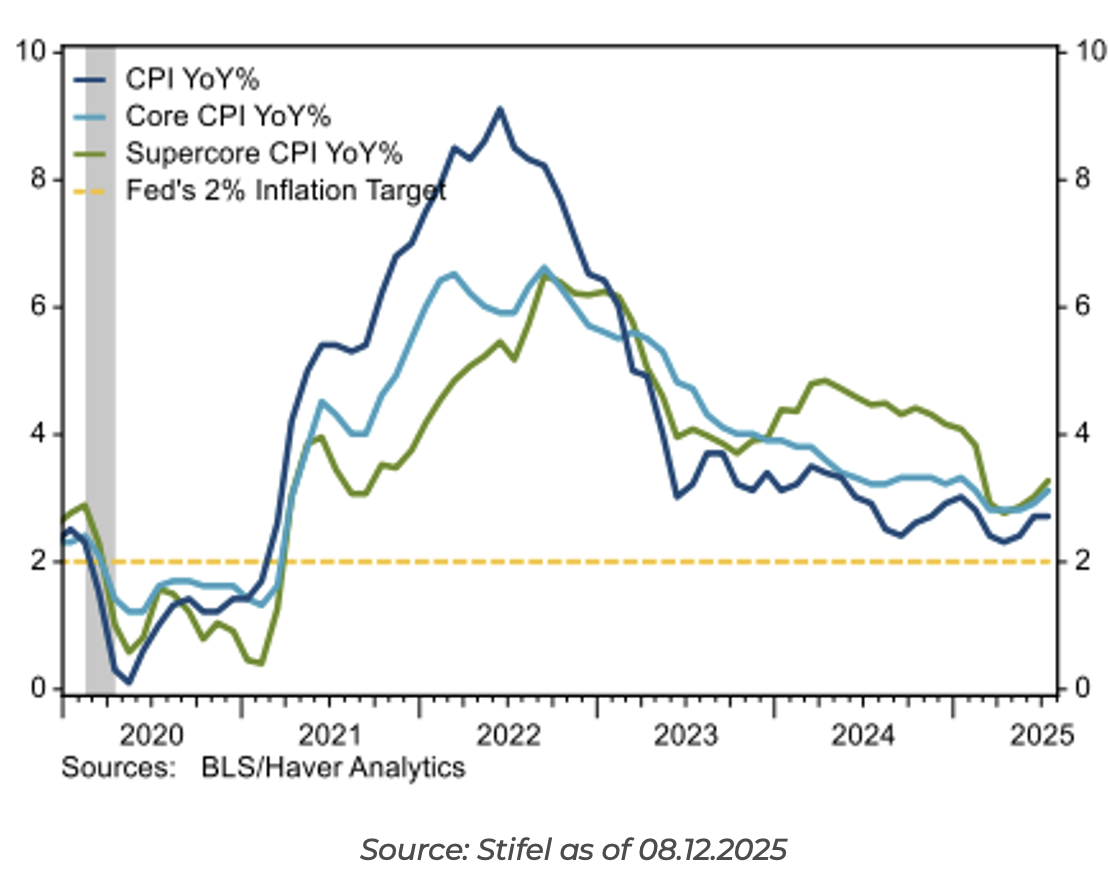

Headline CPI rose 0.20% in July, in line with economists’ expectations. The YoY rate was unchanged at 2.7%. After two warmer months, food prices inched up just 0.05%. Energy prices were also cooler in July, declining -1.1% on a -2.0% drop in motor fuel CPI and lower prices for electricity and natural gas.

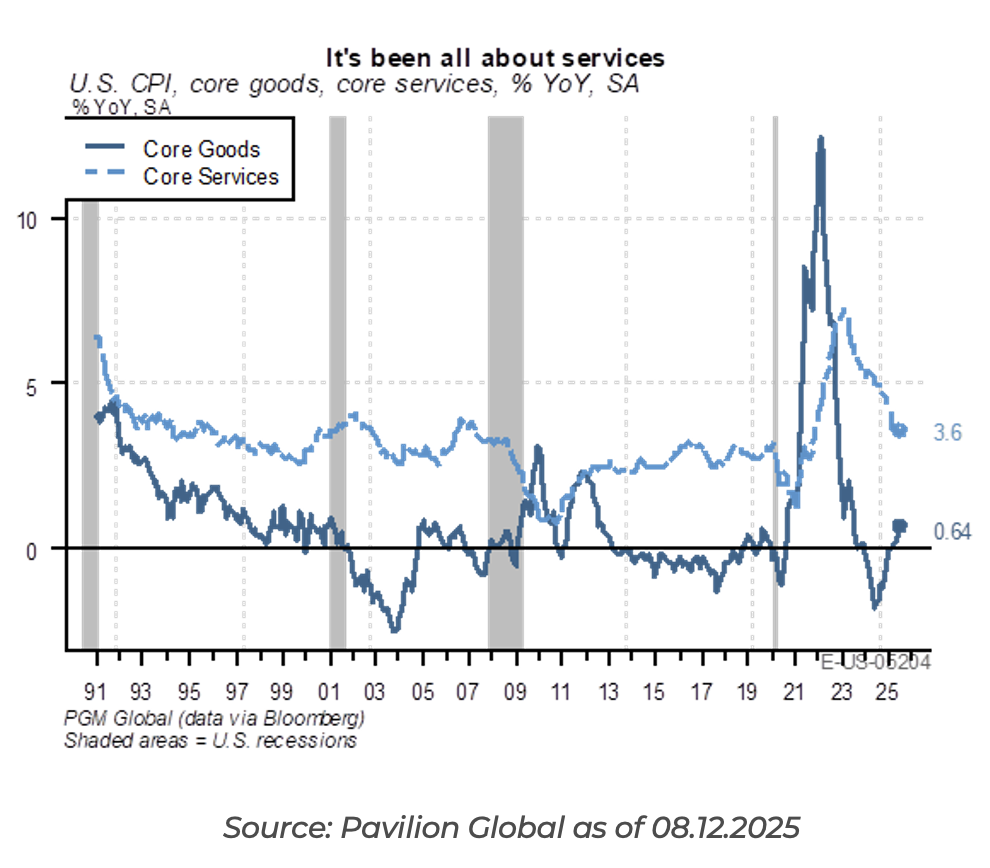

Core CPI rose 0.32% MoM, the second-largest increase in over a year. YoY the core CPI increased 3.1%, up from 2.9% in June. Core goods CPI rose 0.21%, the largest increase in five months but still only reflecting a minimal increase from the pre-tariff trend.

There were some categories of tariff-exposed goods that saw price increases (apparel +0.1%, furniture +0.9%, toys +0.2%, and recreational prices +0.4%), but there were also ones that saw price declines, like appliances, which fell -0.9%. Used vehicle prices, which were expected to rise based on auction sales data and following the auto tariffs, rose just 0.48% MoM.

Goods & Services Tug of War

More of a concern in July was the 0.36% increase in core services CPI, the second-largest increase in the last ten months. Housing rents remained warm but did pull back to 0.28%. Excluding housing rents, supercore CPI (defined as core services excluding housing) rose a concerning 0.48% in July (3.3% YoY), the second largest gain in 16 months (in fairness, this is a more volatile measurement).

Contributing to the rise was a 4.0% jump in airfare CPI, the largest pop in three years, which more than offset a -1.0% decline in lodging prices. Elsewhere, the core services categories were broadly warmer. Medical care services rose 0.79%, the largest increase in six years, on a 2.6% jump in dental services. Ultimately, we believe at least some of the service-related pricing data is impacted by summer vacations, etc., which could normalize over the next couple of months as school starts back.

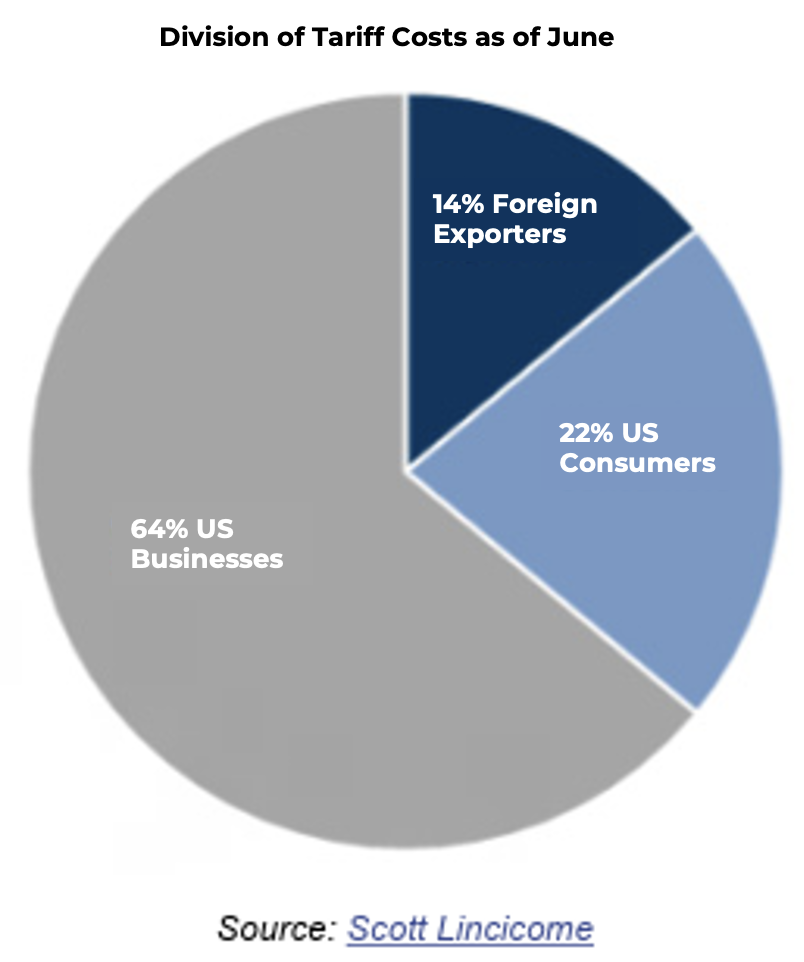

Tariffs are Biting Businesses More than Consumers… So Far

As of 08.13.2025

As of 08.13.2025

The July CPI report does reflect firmer prices, particularly when excluding the large decline in energy costs, but not the type of increase expected to be seen from tariffs. While there is some noisy evidence of higher prices across some categories of goods, it appears that a large portion of the tariffs are being absorbed by businesses at this point.

Time will tell if this can continue, as the rundown from pre-tariff stockpiles could lead to higher consumer prices. Our takeaway from the report was that the previous trend of cooling in services inflation has stalled.

Market Reaction

Fed Funds futures following this week’s CPI reading have the market pricing in expectations for ~2.5 25bps cuts this year (a 50bps September cut is gaining traction) and another 3 cuts next year.

We believe the Fed should resume rate cuts to get the policy rate closer to neutral (we think it sits somewhere in the 3-3.5% range) and look through the short-term price noise from tariffs. We think their employment mandate will continue to come more into focus, given the recent softness in the labor market. The big point here is bringing policy closer to neutral…not into stimulative territory.

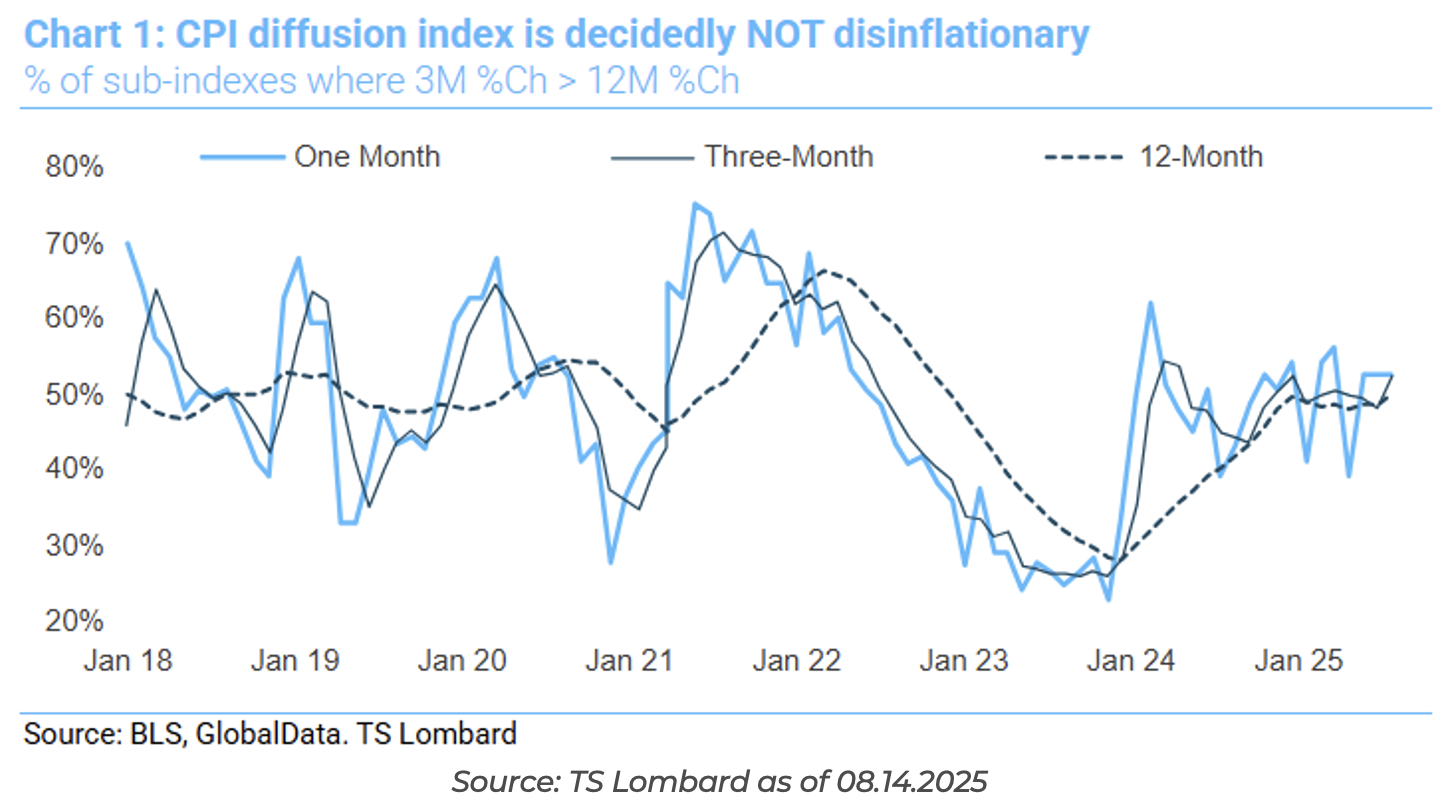

CPI Diffusion Index

Steve Blitz at TS Lombard publishes a CPI Diffusion Index that is quite helpful in seeing the underlying trend of inflation at a deeper level.

The index tracks the percentage of sub-indexes where the 3 month % change is greater than the 12 month % change. The numbers through July stand at 53% for the 1 month, 53% for the 3 month, and 50% for the 12 month. While this level isn’t necessarily indicative of inflation soaring, it’s certainly not disinflationary.

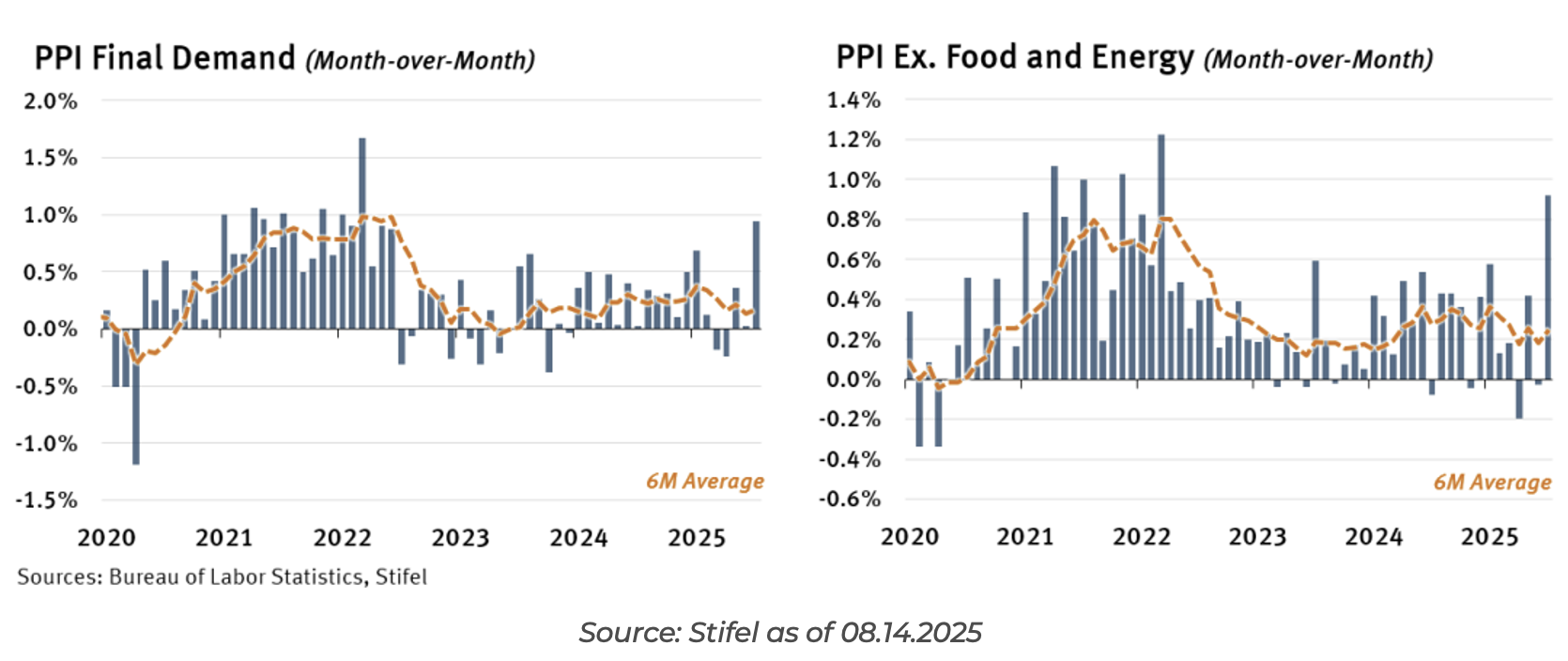

Producer Prices – Warm July

The PPI data for July came in much hotter than market estimates, throwing a little cold water on the hopes for mega rate cuts into the back half of 2025. Producer prices spiked 0.9% MoM in July, the largest increase in three years (market expected a 0.2% increase).

Food prices and energy prices were both firm, up 1.4% and 0.9%, respectively. Food prices were hit by a 39% surge in fresh vegetable prices, a 7.3% increase in eggs, and a 4.6% jump in beef and veal.

Excluding food and energy items, core PPI also posted its largest increase in over three years, up 0.9% on warmer goods inflation and a hot month for services. Core goods PPI rose 0.4%, the largest increase in over two years. Most of the increase came from goods for export.

On the services side, PPI jumped 1.1%, the largest increase in over three years. Services prices were broadly higher, but trade services posted a particularly large 2.0% increase. This reflects wholesaler and retailer margins, which could be an indication that businesses are no longer willing to absorb higher input costs. Also contributing was a 1.0% increase in airfare, the first increase of the year and one of the components used in the PCE report.

Bottom line, there is inflation in the pipeline, but we continue to believe this will look more like a one-time price shift (policy-driven) vs. a sustained increase in the inflation rate. Remember the Fed’s preferred inflation metric is Core PCE, and that is ultimately what drives policy decisions. Taking both CPI and PPI data from July, we can roughly estimate headline PCE rising 0.28% MoM and core PCE rising 0.38% MoM. With that, it is likely to be moderate enough for the Fed to ease -25bp in September.

Stephen Miran: Temporary Federal Reserve Appointee

President Trump selected Council of Economic Advisers (CEA) Chairman Stephen Miran to be his temporary selection for Adriana Kugler’s seat on the Federal Reserve. Kugler’s seat expires at the end of January, and the appointment of Miran is for these last remaining months of the term. We’d expect Miran to step down from the CEA if confirmed, as a member both in the Administration and on the Fed Board would immediately bring independence into play.

The temporary appointment buys time and optionality for the Trump Administration to decide on what to do about the chairman selection next May. Miran will need Senate confirmation even with the temporary appointment. The upside for Trump is that Miran was confirmed by the Senate in March (53-46 vote), meaning that the background process is fresh and does not need to start from scratch. We’d caution that the Senate will treat a Fed Board seat a bit differently than the “President’s economist”. Fed Independence will be the key item for scrutiny and one that Senate Banking Committee member Senator Tillis will likely question aggressively.

Miran’s known for his focus on the dollar, particularly its persistent overvaluation caused by acting as the global reserve currency. The US sends dollars abroad to finance its trade deficit, and those dollars, rather than being used to purchase US-manufactured goods, are instead recycled into dollar-denominated financial assets, driving financial asset prices higher.

A constant “artificial bid” for dollars leads to overvaluation versus other currencies and compounds the negative trade deficit we run. A too-strong dollar makes US manufacturing less competitive, and has been a key factor in hollowing out US manufacturing jobs, especially since China entered the WTO. There are, of course, many benefits of holding the reserve currency…lower interest rates leading to lower debt servicing costs relative to other sovereigns. It can be presumed Miran will join the dovish group of voters at the Fed, pushing for a quicker pace of rate cuts.

Now we wait for the Miran confirmation, which will either be done by the Senate (currently in recess) ahead of the September 16th Fed meeting or by Trump via a recess appointment. The Fed member’s dot plots and forecasts are due on September 12th (prior to the official meeting,) which will put a sense of urgency to get him appointed

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2508-15.