Most financial planning conversations start on the asset side of the client’s balance sheet…how to invest, how to diversify, and how to manage risk. But their liabilities do not receive the same level of care. Debt is not a single, monolithic concept. Different loans carry very different costs, benefits, risks, and planning implications. When viewed together, the client’s overall balance sheet can have even greater benefits through thoughtful construction.

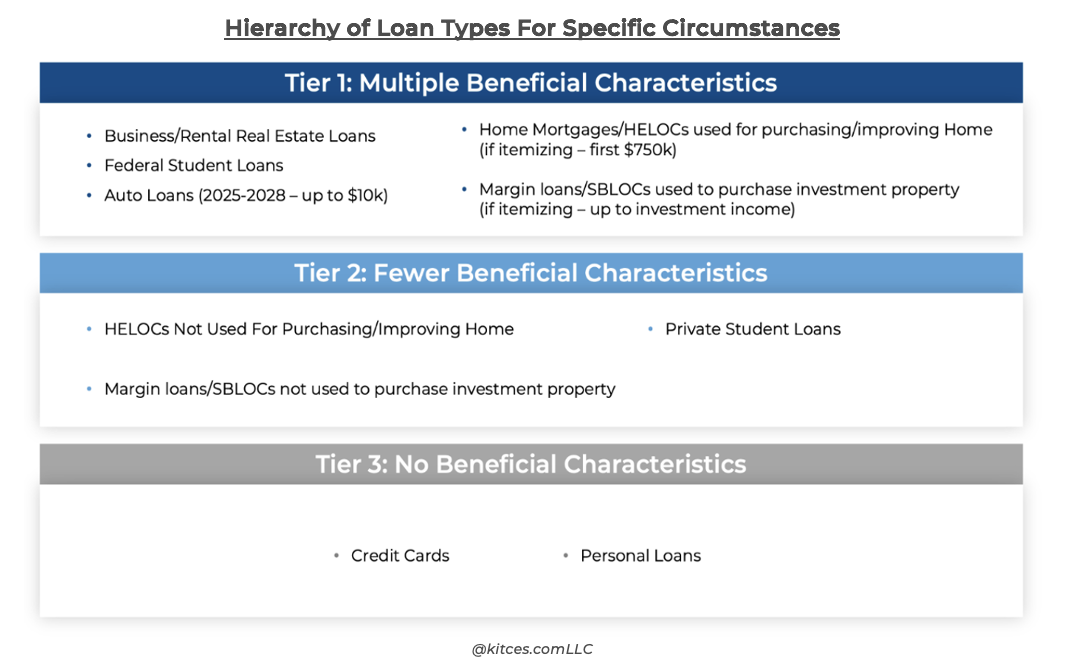

Michael Kitces’ site had a recent blog post that creates a useful way to think about debt as a hierarchy. They presented the following graphic to introduce the discussion:

Thinking through this in more detail, the tiers break down as follows:

Tier 1: At the top, loans that receive the greatest structural advantages, often combining government support, collateral, and favorable tax treatment. Their defining feature is that they are purpose-built to encourage specific financing activities. Because of that, they tend to offer the most borrower-friendly terms. When a client’s need matches one of these purposes, these “Tier 1” loans are usually the first place to look.

Tier 2: In the middle of the hierarchy are loans that share some, but not all, of those benefits. Examples include private student loans, home equity lines used for non-housing purposes, margin loans, and securities-backed lines of credit (SBLOCs). These are typically collateralized, which keeps rates below unsecured credit, but they often lack subsidies or broad tax deductibility. They serve as flexible tools, useful for bridge financing, liquidity needs, or short-term opportunities.

Tier 3: At the bottom sit unsecured consumer debts such as credit cards and personal loans. These offer little benefit to the borrower: no collateral, no subsidy, and usually no tax advantages. As a result, they tend to be the most expensive form of borrowing and are best treated as a last resort.

Introducing Box Spreads

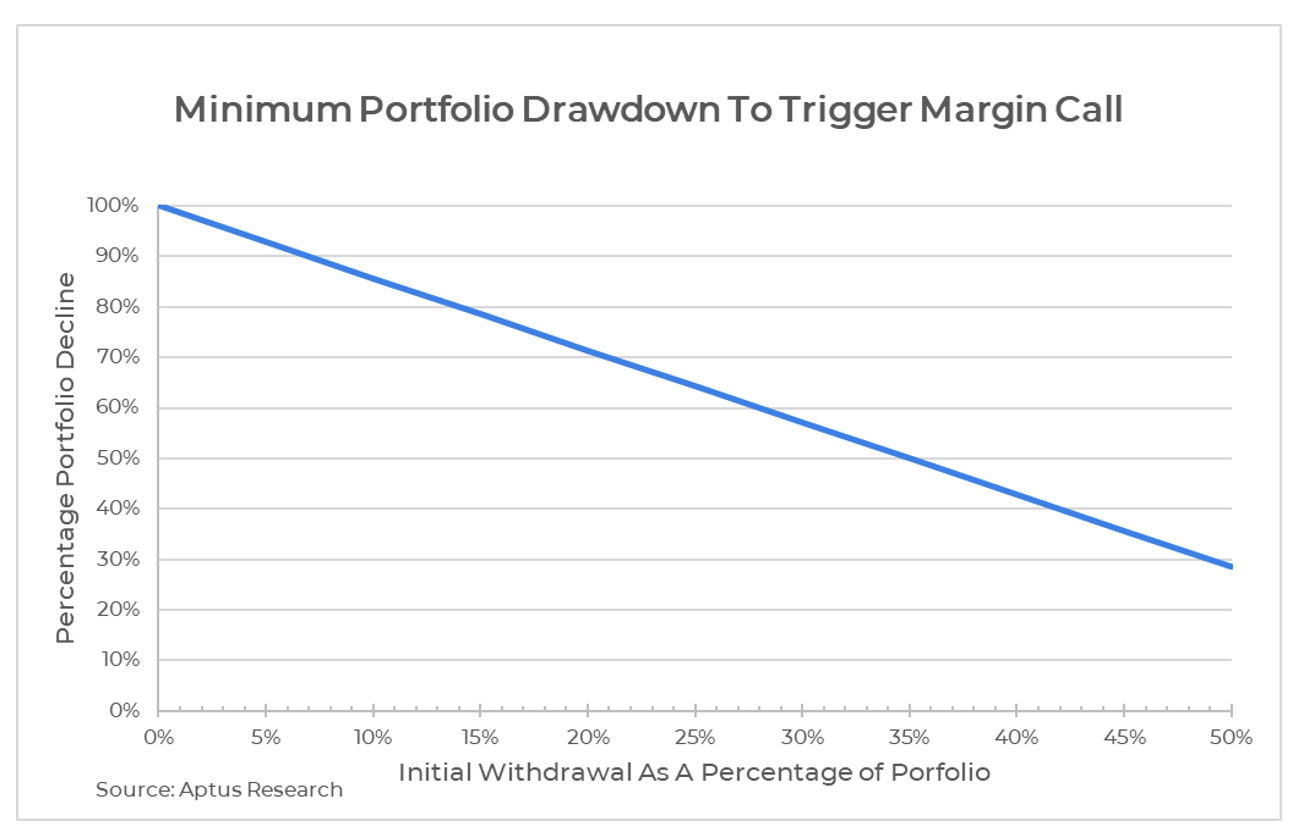

Within this framework, portfolio-backed lending occupies an interesting space. Many affluent clients with sizable taxable portfolios turn to margin loans or securities-based lines of credit (SBLOC) rather than selling appreciated assets. The appeal is obvious: fast access to cash and no initial forced realization of capital gains. The downside is that these loans can have much higher interest rates relative to other collateralized options, and their interest is generally not deductible. They also introduce the risk of margin calls if markets fall sharply.

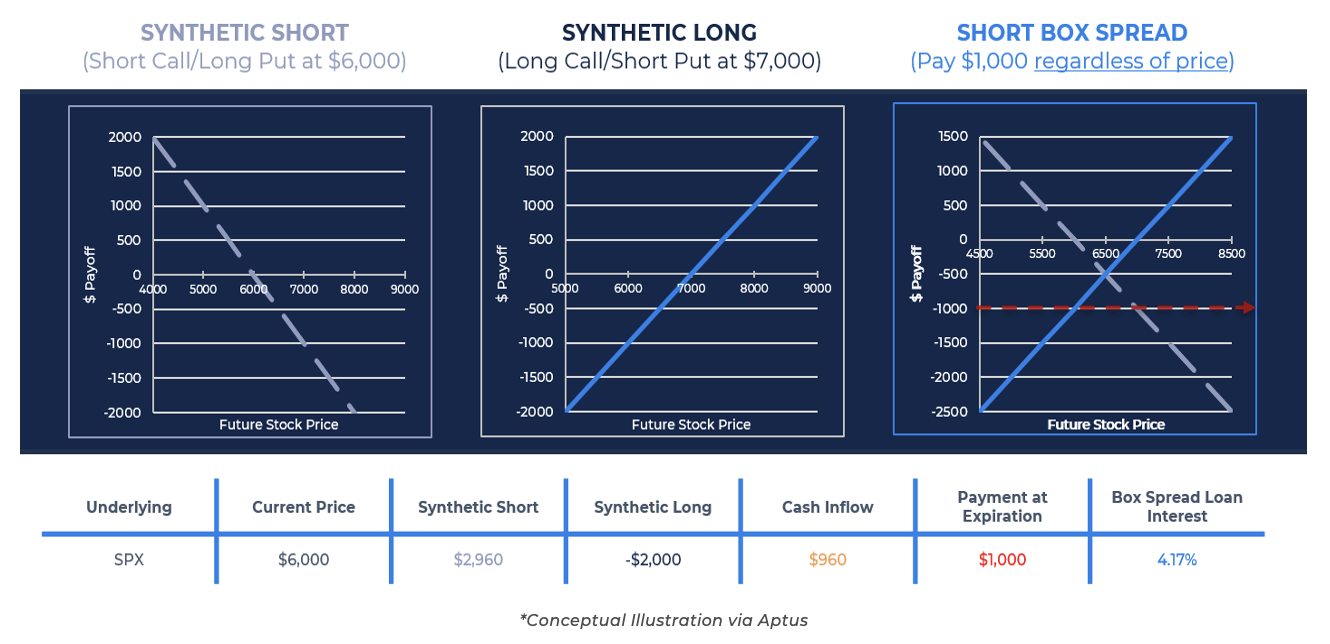

This is where box spreads enter the conversation. A box spread is a strategy executed in the options market that synthetically replicates a fixed-term loan. While the mechanics are complex, the economic result is simple: the borrower receives cash today and commits to repaying a known, higher amount at a future date. Because option pricings are closely tied to “risk-free interest rates”, box spreads often produce borrowing costs that resemble closer to Treasury yields rather than the typical custodial margin rates.

Box spreads differ from traditional loans in their tax treatment. Instead of generating interest expense that nets against investment income, the cost of borrowing shows up as capital losses from options positions. Those losses can be used to potentially reduce capital gains tax by offsetting other gains elsewhere in the portfolio.

The Risks and Opportunity

Since the Options Clearing Corporation (“OCC”) guarantees options contracts, there is limited counterparty risk at settlement. The primary risk is portfolio volatility. Because they are implemented in margin accounts, a severe market decline can trigger a margin call if the borrowed amount is too large relative to portfolio value (the first graphic demonstrates this).

Prudent usage, therefore, means borrowing well below maximum limits and viewing box spreads as a liquidity tool, not a way to over-lever a portfolio. Additionally, early unwinding of a box spread introduces interest rate risk, as changes in market rates and remaining tenor can impact the effective borrowing cost.

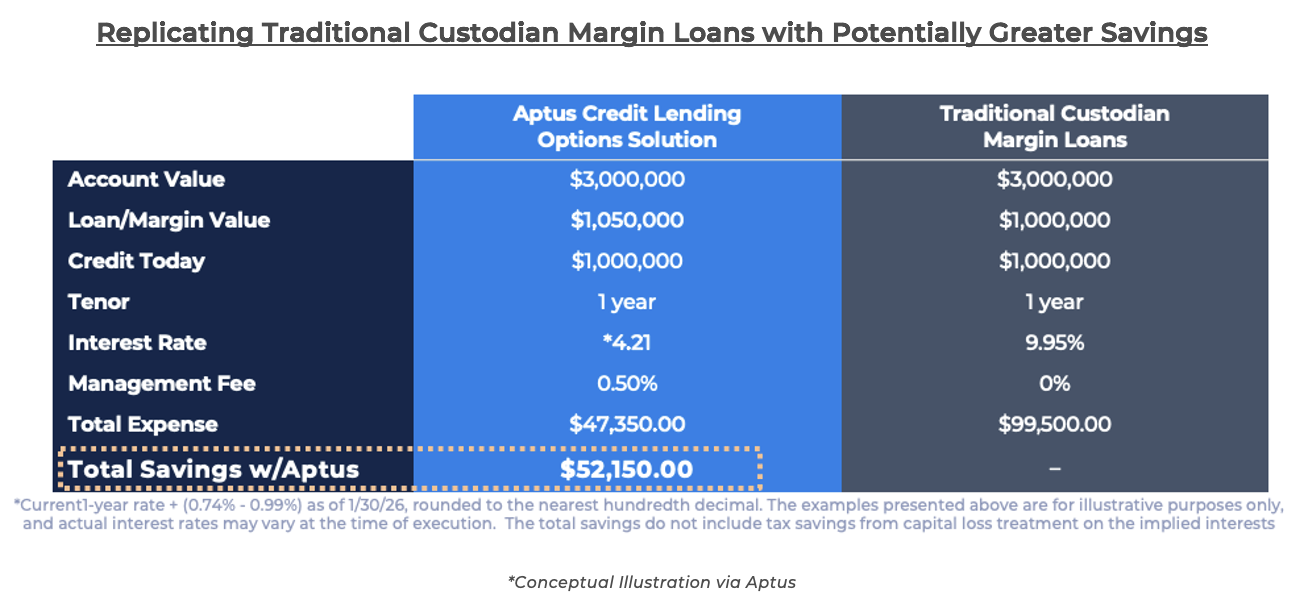

In practice, box spreads may situationally be favored compared to mortgages, business loans, or Federal student loans that occupy the top of the hierarchy. Their primary competitive set, however, is HELOCs, margin loans, and SBLOCs, the traditional “Tier 2” sources of liquidity. This is where the box spreads shine, as they often represent a more efficient alternative. For clients with significant taxable assets and episodic borrowing needs, box spreads can offer a compelling blend of lower borrowing costs and improved tax efficiency.

The broader lesson is that debt choice matters. Just as advisors carefully select asset allocations, they should also help clients choose the right types of liabilities for each purpose. When viewed through the lens of debt hierarchy, borrowing becomes less about “how much” debt a client has and more about its structure and quality. This distinction has the potential to materially improve the long-term outcome of a client’s financial plan.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

*Conceptual Illustration: Information presented in the above charts are for illustrative purposes only and should not be interpreted as actual performance of any investor’s account. As these are not actual results and completely assumed, they should not be relied upon for investment decisions. Actual results of individual investors will differ due to many factors, including individual investments and fees, client restrictions, and the timing of investments and cash flows.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2602-17.