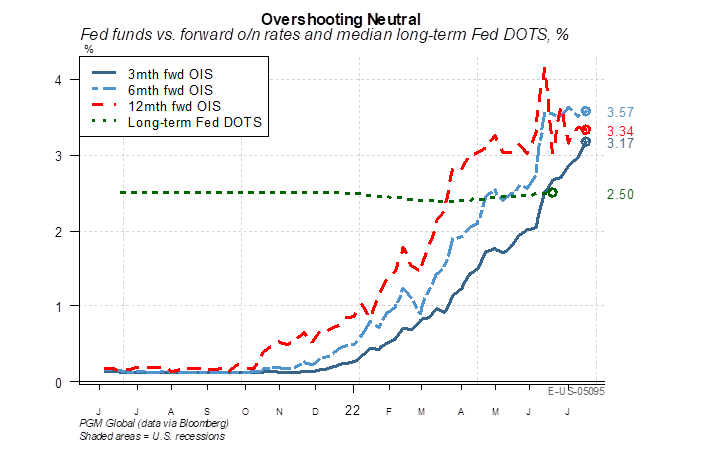

Another Month, Another (BIG) Hike.

Next Wednesday, July 27th, the Fed is expected to hike 75bps and bring their overnight target up to the FOMC’s consensus neutral rate of 2.5%. We believe that more hikes will be needed to tame inflation, which helps explain why there is an additional 100bps of Fed rate hikes priced by year-end. The market envisions Fed Funds to peak in Q1 2023.

Source: Pavilion Global Markets. As of 7/20/22.

Source: Pavilion Global Markets. As of 7/20/22.

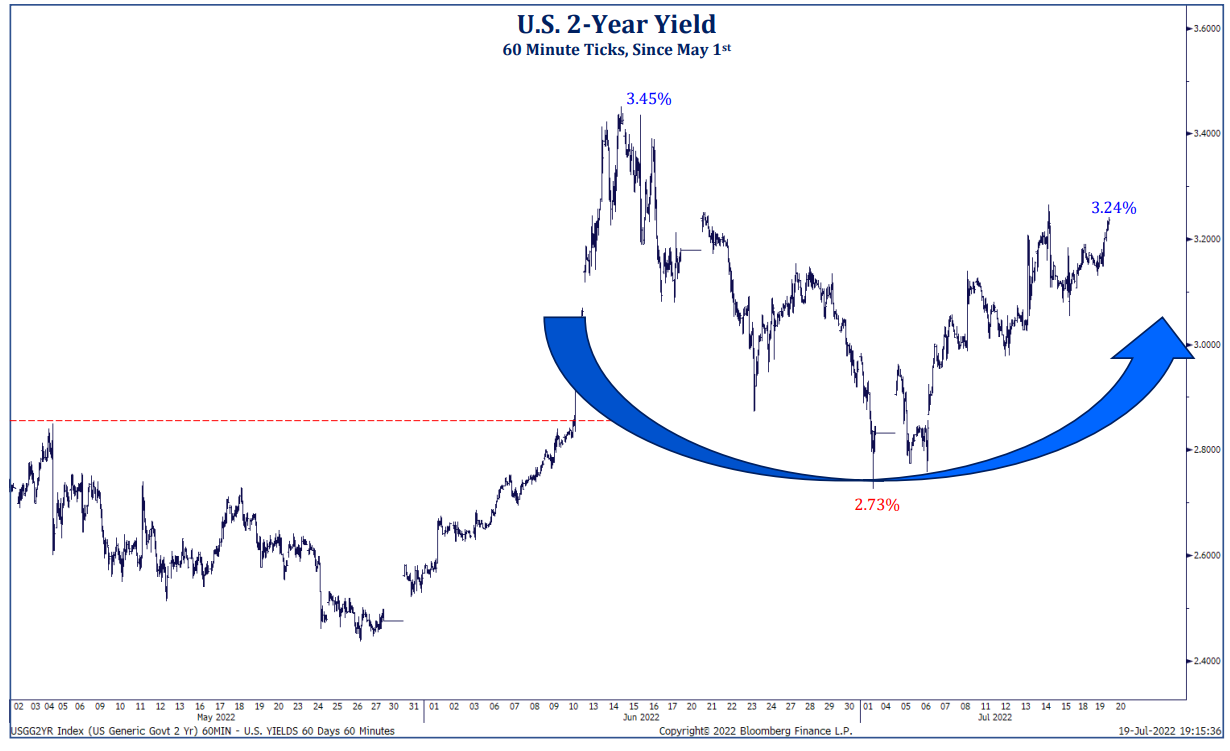

The market has followed the Fed’s every word which can be seen in the pricing of 2 year Treasuries. Following June’s hotter than expected CPI number, the market is expecting the Fed to mean business and continue to hike aggressively. The hikes that have been completed, plus the hikes that are expected to come throughout the remainder of the year, are keeping the front end of the curve elevated. The thing we’d note is the volatility present in the front end of the curve is not something often seen…20+ bps move days have become common.

Source: Strategas. As of 7/20/22.

Source: Strategas. As of 7/20/22.

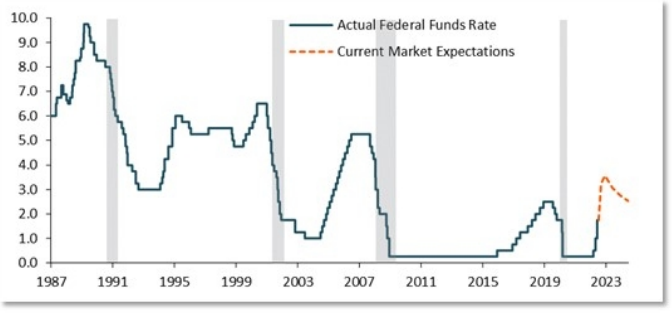

Fed Is Still Hiking and The Market is Already Expecting Cuts

In theory, it makes sense given that a recession in the next two years is the base case. What makes us nervous is that inflation is much higher than anything we have seen in the modern Fed era (i.e., the post-Volcker era, when the Fed started carrying out monetary policy in a way similarly to today).

As shown by the orange line below, the market currently expects the Fed to continue to hike to the 3.5-3.75% range by the end of the year. Starting in the first quarter of 2023 however, the market expects the Fed to reverse course – albeit gradually. There are more than 80 bps of CUTS priced in for 2023 and another 25 bps for 2024.

While we are not saying that the Fed will ignore the effects of a recession, they will likely be forced to utilize a different playbook given pricing instability. What we are saying is we believe the Fed’s response to a recession could be different due to high inflation and a tight labor market.

Source: PSC. As of 7.21.22

Source: PSC. As of 7.21.22

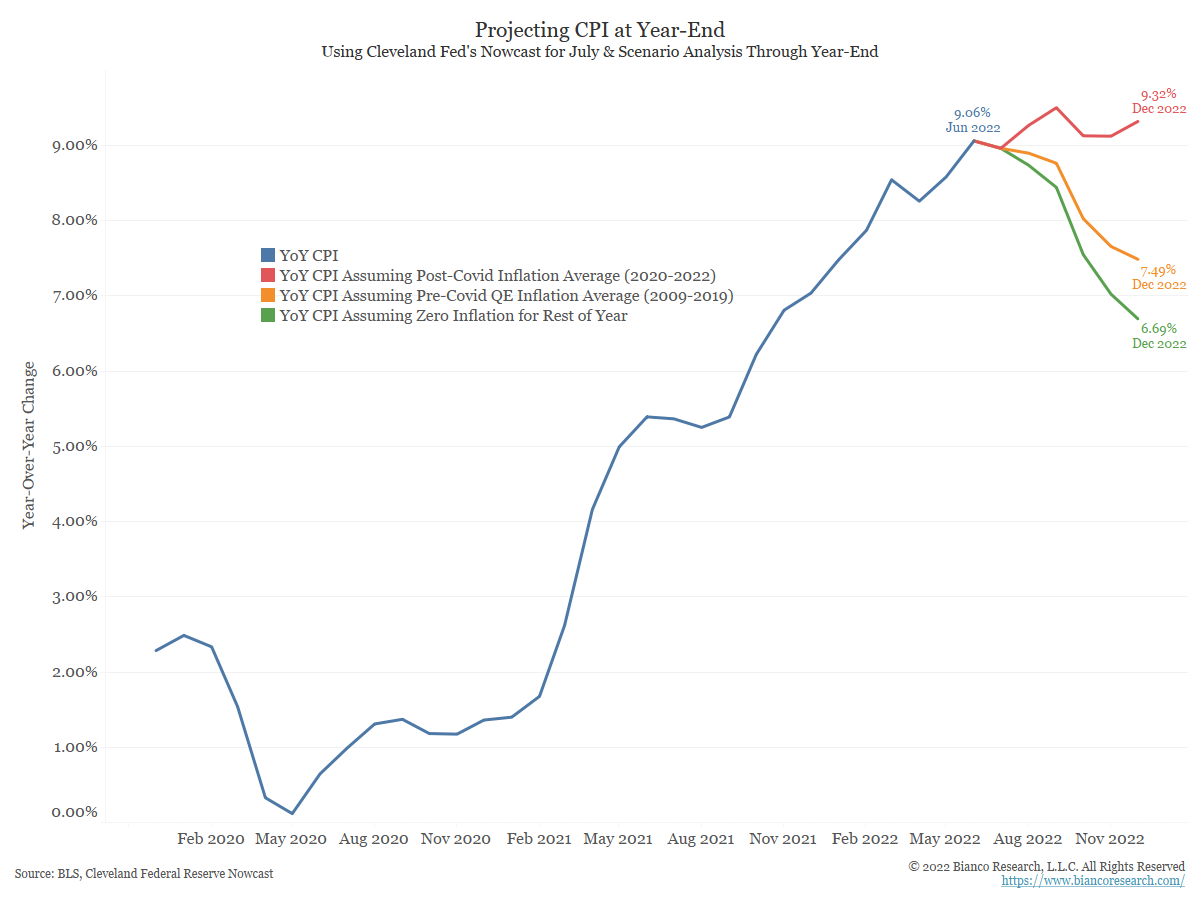

Inflation… Higher for Longer. Just Look at the Math.

Even if we have hit peak inflation, the YoY number will be elevated into 2023. The green line below shows CPI will end the year with a 6.69% growth rate even if no additional inflation is printed this year.

In other words, the month-over-month numbers for July through December could be 0% and inflation will still be almost 7% year-over-year. Anyone calling for sub-6% CPI by year-end is calling for DEFLATION over the next six months – this seems unlikely to us.

Source. Bianco Research. As of 7/6/22.

Source. Bianco Research. As of 7/6/22.

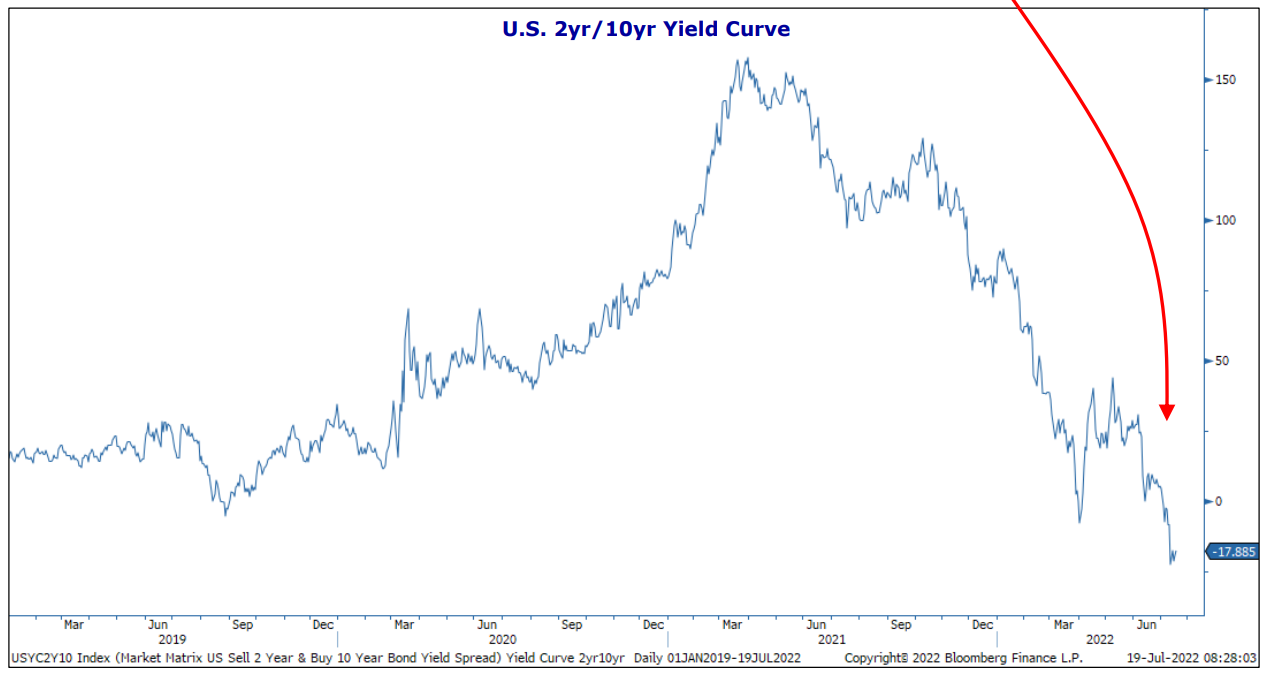

The Curve Has Inverted and Quickly Reverted Back into Positive Territory.

The yield curve has inverted several times in ’22 but each time it has quickly reverted back into positive territory. The latest inversion (happened July 5th) has been different. This time the 2/10 Treasury curve has inverted deeper (~18bps at current levels) as well as longer (the inversions earlier this year only last a day or two). We will say, the 3M/10Y (the Fed and markets favorite recession indicator) curve has not yet inverted, although at the current pace it will be awfully close following next week’s rate hike.

Source: Strategas. As of 7/22/22.

Source: Strategas. As of 7/22/22.

Disclosures

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy. Investing involves risk. Principal loss is possible.

Projections or other forward-looking statements regarding future financial performance of markets are only predictions and actual events or results may differ materially.

The Consumer Price Index (CPI) measures the change in prices paid by consumers for goods and services. The CPI reflects spending patterns for each of two population groups: all urban consumers and urban wage earners and clerical workers.

The 2 Year Treasury Rate is the yield received for investing in a US government issued treasury security that has a maturity of 2 years.

The 10-2 Treasury Yield Spread is the difference between the 10-year treasury rate and the 2 year treasury rate. A 10-2 treasury spread that approaches 0 signifies a “flattening” yield curve. A negative 10-2 yield spread has historically been viewed as a precursor to a recessionary period.

Advisory services are offered through Aptus Capital Advisors, LLC, a Registered Investment Adviser registered with the Securities and Exchange Commission. Registration does not imply a certain level or skill or training. More information about the advisor, its investment strategies and objectives, is included in the firm’s Form ADV Part 2, which can be obtained, at no charge, by calling (251) 517-7198. Aptus Capital Advisors, LLC is headquartered in Fairhope, Alabama. ACA-2207-27.